Morgan Stanley Research Report Analysis: CPO Growth Overestimated by 30x, TSMC Capacity is the Real Constraint

TechFlow Selected TechFlow Selected

Morgan Stanley Research Report Analysis: CPO Growth Overestimated by 30x, TSMC Capacity is the Real Constraint

The real opportunity for domestic substitution will only emerge after the CPO industry chain matures and overseas suppliers encounter trade barrier restrictions.

Written by: Rita

TechFlow Guide

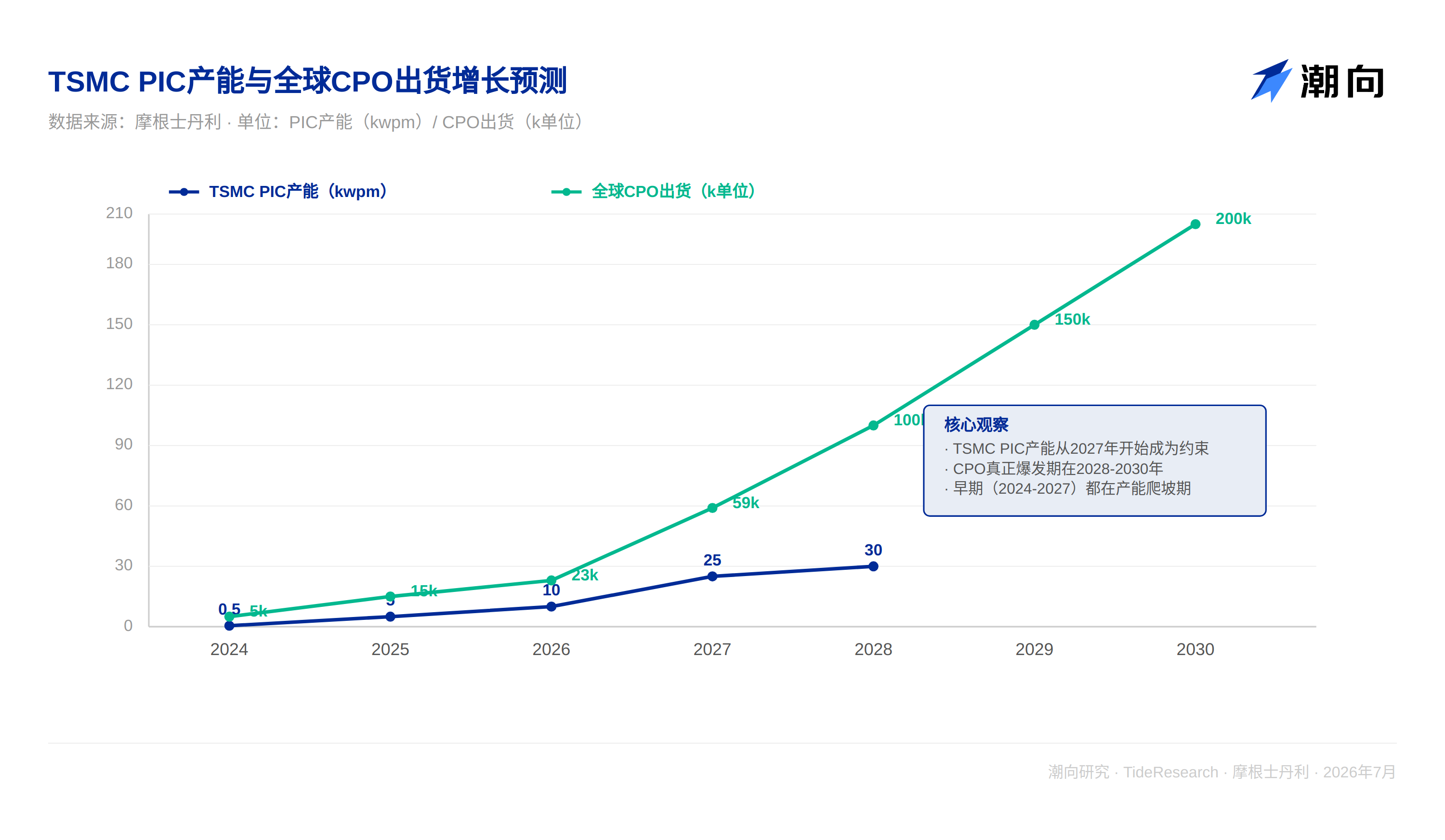

This Morgan Stanley CPO supply chain report shatters the market's pleasant illusions. The story the market is currently telling about CPO is: "AI chip traffic explosion → NVIDIA/Broadcom need co-packaged optics → Spectrum switch order surge → suppliers benefit". However, the supply chain check data in the report tells another story: global CPO switch shipments in 2026 will be only 23k units, and only 59k in 2027, which is an order of magnitude less than market expectations. The real bottleneck is not in technological innovation (GlassBridge is mature), but in TSMC's PIC capacity ramp-up (only 10kwpm in 2026, 25kwpm in 2027) and optical engine yield (currently 20-50%). This means for investors holding NVDA and AVGO, from Q4 2026 to mid-2027, CPO demand may fall short of guidance again, leading to suppressed stock prices. The advice is clear: do not buy into the "CPO theme" in the first half of 2026. Instead, buy after the disappointment in Q2 2027, when TSMC yield data will be clearer and real demand will gradually emerge.

NVIDIA/Broadcom's CPO Orders Are Severely Overestimated

NVIDIA and Broadcom's Spectrum switch shipments in 2026-2027 are far smaller than market expectations. FOCI's report shows that NVIDIA's contribution to FOCI's revenue in 2026 is only 18%, indicating that the actual shipment volume of CPO switches is much smaller than the macro narrative suggests. If you see NVIDIA or AVGO lowering guidance in their quarterly reports in mid-2026 due to CPO demand missing expectations, this disappointment stems from capacity and customer validation pacing issues, not the technology itself. The data provided by Morgan Stanley is cold but undeniable: global CPO switch shipments were 5k units in 2024, about 15k in 2025, and only 23k in 2026. Compared to market expectations in 2024 (many analysts believed 2026 CPO shipments would exceed 100k), the actual figure is less than 22% of expectations.

TSMC's PIC Capacity and Yield Are the Real Constraints

The real constraints come from two links. PIC (key intermediate for optoelectronic interconnects) capacity is the first bottleneck. The report points out that TSMC currently has a monthly PIC capacity of 500 wafers, with future goals to expand from 10kwpm in 2026 to at least 25kwpm in 2027. For benchmarking, TSMC's typical capacity expansion cycle is 12-18 months, meaning that before mid-2027, PIC capacity may still be a bottleneck. This is only the intermediate capacity for PICs; downstream considerations also include the complete optical engine insertion process, packaging yield (currently only 20-50%), and final system integration validation. Looking at last year's actual shipment of 3.9k sets of optical engines, the 2027 target is only 77.8k sets, reaching 486k sets in 2028.

The optical engine yield dilemma is the second bottleneck. The report mentions a key data point: Insertion 2's EPIC wafer test shortened from "one wafer per day" to "one wafer per 6 hours". This sounds very positive, but conversely, it shows how severe the previous yield issues were, necessitating a significant acceleration of the testing process. Current installation yield remains only 20-50%, with a 2028 target of 50%. If yield is still stuck at 30-40% by the end of 2027, it means the actual available optical engine production volume is far lower than nominal capacity.

For investors holding TSMC, the contribution of the CPO business to profits in the next two years may be far less than management's optimistic statements. TSMC usually aggressively emphasizes CPO capacity expansion in financial reports, but actual capacity utilization and yield pressure may lead to gross margins for this business being lower than expected. It is expected that TSM's 2026-2027 financial guidance will include cautious wording regarding CPO (such as "uncertainty in yield improvement"), which could become a pressure point for the stock price. NVDA's Spectrum switch shipment curve (23k→59k→100k) means that this business's contribution to revenue in 2026-2027 is negligible and cannot become a "new growth engine" narrative. If NVDA lowers the growth rate of the data center segment in its 2027 financial report due to Spectrum shipments missing expectations, do not be surprised. AVGO's risk is higher because AVGO's base is smaller than NVDA's. Once Broadcom's CPO orders are lowered, the stock price reaction may be more violent.

CPO Opportunities for Optical Equipment Companies Are Severely Overestimated

The CPO opportunities for US fiber and optical equipment companies (such as Lumentum, Coherent) are severely overestimated. The FAU and optical engine suppliers mentioned in the Morgan Stanley report are mainly Taiwanese and Japanese companies (FOCI, TFC, Senko), but US stock investors will ask: what about such optical equipment companies? The answer given by the report is straightforward: CPO orders are still too small to constitute a game changer. Taking optical engines as an example, actual shipments for the full year 2026 are only 3.9k sets, 77.8k sets in 2027, and reaching 486k sets in 2028. Compared to Lumentum's annual revenue typically in the 1.5-2bn range, even if the CPO business has high gross margins, it will contribute at most tens of millions of dollars in revenue in 2026-2027. More critical is the uncertainty of the technical route: the traditional FAU route faces long-term challenges from Corning GlassBridge. GlassBridge avoids precision manufacturing through passive alignment of glass waveguides, meaning traditional process-intensive FAU may be gradually replaced. GlassBridge itself is not yet widely applied (the report explicitly states "far from reaching mass production stage"), so who ultimately wins this technology contest is uncertain. But if GlassBridge ultimately wins, the long-term revenue space for companies relying on traditional high-precision FAU processes (including US optical device companies) will be squeezed.

The advice for holders of optical equipment stocks such as LITE and COHR is: do not buy or increase holdings just because of "CPO demand". The revenue contributed by CPO in 2026-2027 is negligible and cannot change the overall trajectory of these companies. Focus on the performance of these companies in other high-speed signal applications (such as high-speed interconnects in data centers, 5G base stations, etc.), rather than CPO. If you see LITE or COHR raising guidance based on "CPO order prospects" in 2026, treat it with caution. This may be management exaggerating the significance of small orders.

AllRing Faces CoWoS Capacity Reduction Risk, A-share CPO Participation Low

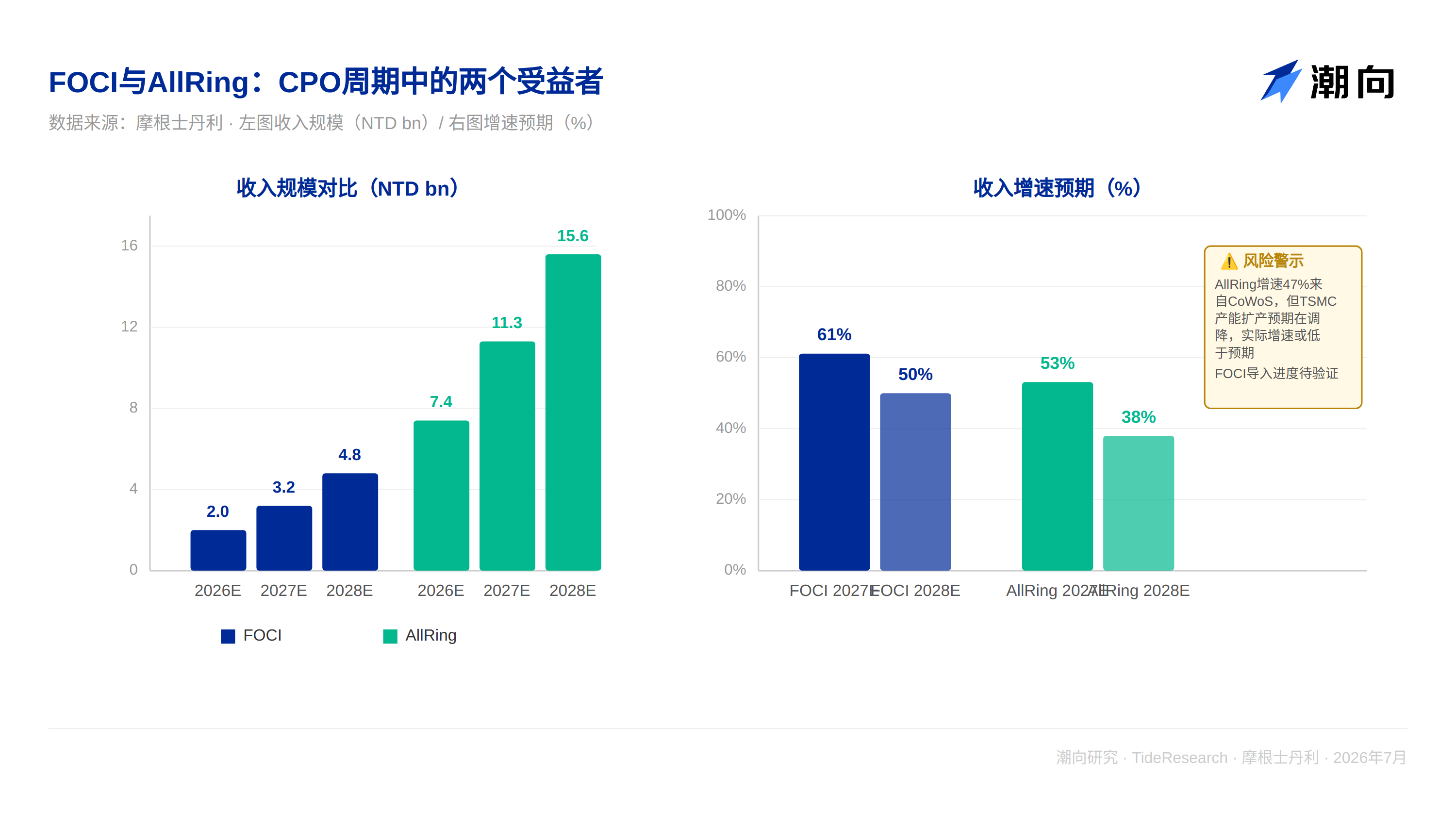

AllRing's story is more complex. In 2026, its CoWoS-related revenue is expected to account for 79% of total revenue, mainly from equipment supply to TSMC and ASE/SPIL. However, Morgan Stanley's supply chain check reveals a shift: TSMC's CoWoS capacity expectation for 2027 was adjusted down from 45kwpm (previously) to 40kwpm, and for 2028 from 75kwpm to 70kwpm. This means TSMC's CoWoS expansion momentum is weakening, possibly because the demand for CoWoS from high-end AI chips is not infinitely expanding, and new processes such as CoPOS may gradually replace it after 2027. AllRing's revenue growth rate expectation for 2027 is 53% (from 7.4bn to 11.3bn), but the premise of this growth forecast is steady CoWoS expansion, steady Flip Chip growth, and rapid implementation of new CPO packaging. A delay in any link (such as TSMC's CoPOS test yield not meeting expectations, or a customer's CPO adoption being postponed) will drag down the overall growth rate.

Regarding A-share CPO participation, the actual situation is more complex than "completely absent". SMIC (688981), as the largest domestic foundry, certainly has R&D investment in CPO processes. Optical module leaders Zhongji Innolight (300308) and Eoptolink (300502) also have relevant product lines in the high-end optical interconnect field. TFC Optical (300394)'s high-end optical connectors are not limited to traditional low-frequency applications. Chip design companies such as Huawei are also promoting their own CPO solutions. The real bottleneck is: A-share companies are still absent in core process equipment (such as PIC processing equipment, optical engine manufacturing) and high-end FAU/GlassBridge links. The main benefits are concentrated in downstream optical modules, chip design, and other relatively mature links. This means that if A-share investors chase "CPO concepts", they actually gain only indirect benefits, rather than direct benefits from core equipment/processes.

TechFlow Perspective

The most valuable thing Morgan Stanley did in this report: revealing the real tight constraints in the CPO cycle, rather than explaining how GlassBridge disrupts FAU. The report points out that what truly determines whether CPO can explode rapidly is whether TSMC's PIC capacity can expand to 25kwpm as scheduled, whether the optical engine insertion yield can quickly climb from 20-50% to higher levels (especially the 2028 target of 50%), and whether system-level validation by key customers such as NVIDIA and Broadcom can proceed on time. If any of these three conditions stall, the entire CPO cycle will be delayed. The key constraint conditions are foundry capacity and process node realization, not the innovation of FAU connectors themselves. In comparison, the technical maturity of GlassBridge itself is relatively certain; the real risk lies in the depth of the supply chain.

The advice for US stock investors is clear: do not chase the high "CPO concept" stock prices of NVDA, AVGO, and TSM. If you see them surge due to strong CPO demand in Q2 and Q3 of 2026, it is instead an opportunity to short. Wait for the disappointment after Q2 2027. At this time, TSMC yield data will be clearer, and real CPO demand will gradually emerge. That is the real buying opportunity. Remain cautious about optical companies such as LITE and COHR. The revenue contributed by CPO in 2026-2027 is too small to support the high valuations of these companies.

The advice for A-share investors is: treat this report as a "contrarian indicator". If you see A-share chip concept stocks surge due to "CPO opportunities", it instead indicates that the market is over-hyping this opportunity, and you should be wary of adjustment risks at this time. Real domestic substitution opportunities will only appear after the CPO industry chain matures and overseas suppliers encounter trade barrier restrictions. Currently, A-shares have almost no substantive participation in high-end chip packaging and optical interconnect fields. In the optical connector field, there is TFC Optical, but TFC mainly makes low-frequency optical connectors for data centers and is not involved in CPO's high-speed optical integration. Photoresists and specialty gases will benefit from chip capacity expansion, but their correlation with CPO is not as direct as US stocks.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of third-party broker research reports. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of Morgan Stanley analysts, represent only the position of that institution, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News