Blaming the desolation of the crypto circle on the rise of AI is a form of intellectual laziness.

TechFlow Selected TechFlow Selected

Blaming the desolation of the crypto circle on the rise of AI is a form of intellectual laziness.

The crypto market has not disappeared, just entered a more brutal K-shaped divergence: winners take all faster, ordinary people find it harder to wait for a slow bull market.

K-Shaped Fundamentals: Betting Logic in Extreme Times

History is the victory of the ruthless over the mindless.

I think I have found the answer. The question is: "The crypto industry or Token market, amidst RWA increasingly embracing blockchain and stablecoins steadily advancing towards payments, has completely lost the fundamentals of capital valuation."

This is actually strange. Blockchain is indeed the future of finance, but the focus of the era has shifted to "technological competition." Even if the AI bubble bursts, there are still new frontiers like nuclear fusion, commercial aerospace, and biomedicine.

Blockchain is incredibly awkward. Western peers have no Eastern counterparts, leading to a failure of the competition mechanism. Consequently, the market lacks upward momentum, becoming a dumping ground for Tokens or a nihilistic field for Memes.

We cannot change this. No matter how wonderful the mechanism is, it cannot accommodate sovereign-level assets, wrapping digital RMB, tokenized treasury bonds, or listing A-shares on chain.

After thinking it through, the problem becomes simpler. For a market destined to be niche but certain in the long term, how do we return to a market-based valuation system?

The Collapse of the Middle Class

East-West confrontation, rise of hard tech.

These are the two major themes of the crypto industry today, just as the 2008 financial crisis was the midwife of Bitcoin.

Under ideal conditions, stablecoins are the linking channel between opposing worlds, similar to the role of Eurodollars during the Cold War, communicating rigid demands between the two camps.

Now both sides are still defining boundaries, and volatility will continue for some time. It can even be argued that stablecoins are ultimately a kind of substitute for Chinese concept stocks.

Before reaching the boundary, we still need entrepreneurs and VCs to strive, seeking a place to settle and make a living, patiently waiting for the moment to turn the tables and take a seat at the table.

The rise of hard tech will not take away liquid capital from the crypto circle; instead, it is creating new speculative targets. Blaming the desolation of the crypto circle on the rise of AI is a form of intellectual laziness.

- The crypto industry has a limited ceiling; only 55 companies can reach a $1B market cap, while there are currently 1603 unicorn enterprises globally

- The crypto industry is more like a super-sized Alt Pre-IPO system; if you cannot reach NASDAQ, you can try Binance first to test the waters

Do not feel disillusioned with the industry; human movement is the norm. Dawn Song, who "jumped ship" to Meta to do AI, was previously the biggest draw for Oasis Labs raising $45 million. Just treat them as a barometer for the maturity of an industry.

Beyond the Token mechanism, Pre-IPO is also possible, and may even severely impact the pricing logic of offshore assets. Permissionlessness also triggers economic gaming again; this is not isolated, but will become more commonplace.

The real crisis lies outside consensus; namely, the fruits of innovation in the crypto industry will quickly become monopolized by giants. One or two major players will emerge extremely quickly in each track, and then it ends.

Binance, as a transactional bank, took 5 years (2017~2022) to become number one in the industry, but I doubt whether the next generation of products will have such a long development time, or rather, the fight among new giants will be extremely fierce.

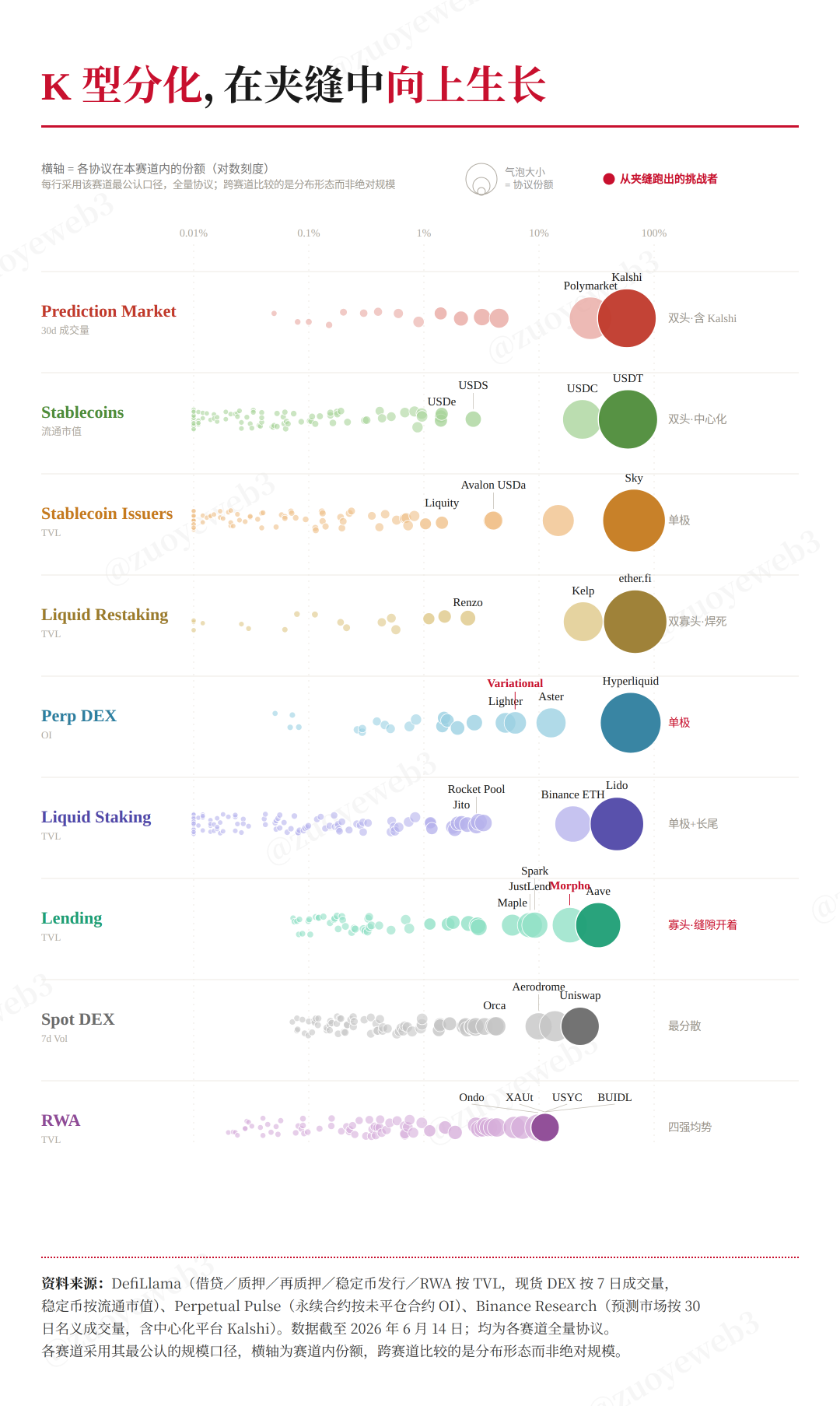

Image Caption: Era of K-Shaped Differentiation

Image Source: @zuoyeweb3

Not only old tracks like stablecoins, exchanges, and lending are like this; PerpDEX, HIP-3, and prediction markets are even faster. TradeXYZ has already ended the HIP-3 war, and $USDH actually survived for only a few months.

As a virtual product industry, crypto itself is no longer an asset target; it must find practical uses and accommodate external assets, instead creating greater volatility.

Volatility is not scary; the problem is that we cannot profit from it. Each track becomes fixed too quickly, leaving increasingly narrow space for individual speculation.

Even in the upcoming era of AI implementation, the process will accelerate further. Recalling since the Vibe Coding narrative, the most severely impacted across humanity is the "middle class":

- White-collar office skills are gradually replaced by Agents

- The technical abstraction layer of SaaS is being chipped away day by day by large models

- Enterprises lack the patience to cultivate talent between junior and senior levels

The above three benefit from the windfall profits of the era, but this also means the distance between Startups and Mag7 is infinitely compressed. SpaceX took 24 years to reach a $2 trillion valuation, while Anthropic reached trillions in just 5 years.

To refine further, for new forces in the crypto industry, the time to enter the 55-member $1B Club will be shorter, but you must choose a new track well and ensure the battle ends quickly.

Good news is, the collapse of tokenomics has already caused the crypto industry to rapidly degenerate from "technological idealism" to "financial services industry." Whoever can find more capital can quickly replace the old guard.

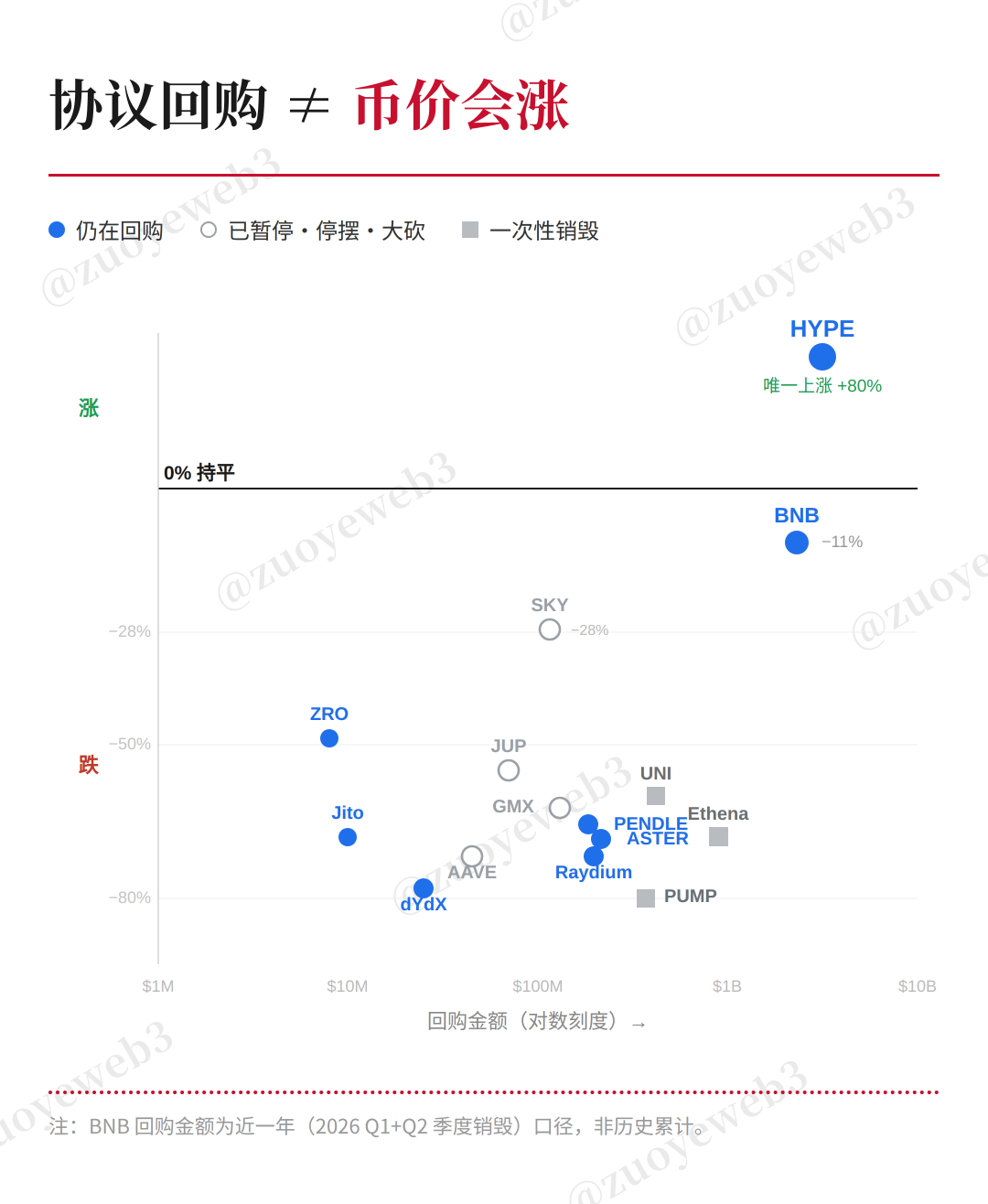

Image Caption: Stagnant Coin Prices Are the Norm

Data Source: @CoinMarketCap

In the past year, buybacks have been unable to stop the overall downward trend of the token industry. In contrast, buybacks in the US stock market have been the fundamental driving force for success over the past three decades.

If open market buybacks cannot convince others to hold assets, it means the underlying power source has reached the time for complete innovation.

Regarding the source of innovation, let us predict from the VC perspective.

Riding on the Back of the Silver Dragon

When Lightspeed Venture Partners introduced Claire Zau to specialize in podcasts, A16Z had already transformed into a primary asset management company. In Q1 2026, the top 6 VCs in the US took nearly 80% of fundraising amounts. Correspondingly, the top 5 startups, accounting for 0.1%, took 73% of funding quotas, reaching $195.6 billion.

The expenditures of AI companies, to a large extent, align with the profit sources of airdrop hunters—both are VC money. Hope AI does not ultimately become altcoins.

Up to now, it is hard to distinguish whether this K-shaped differentiation is triggered by AI, or ultimately creates the CapEx frenzy of the AI era.

In our usual memory, venture capital is an early-stage, small-scale, and experimental technical bet, but under the operation of A16Z and others, it has become a high-stakes gamble that cannot afford to lose.

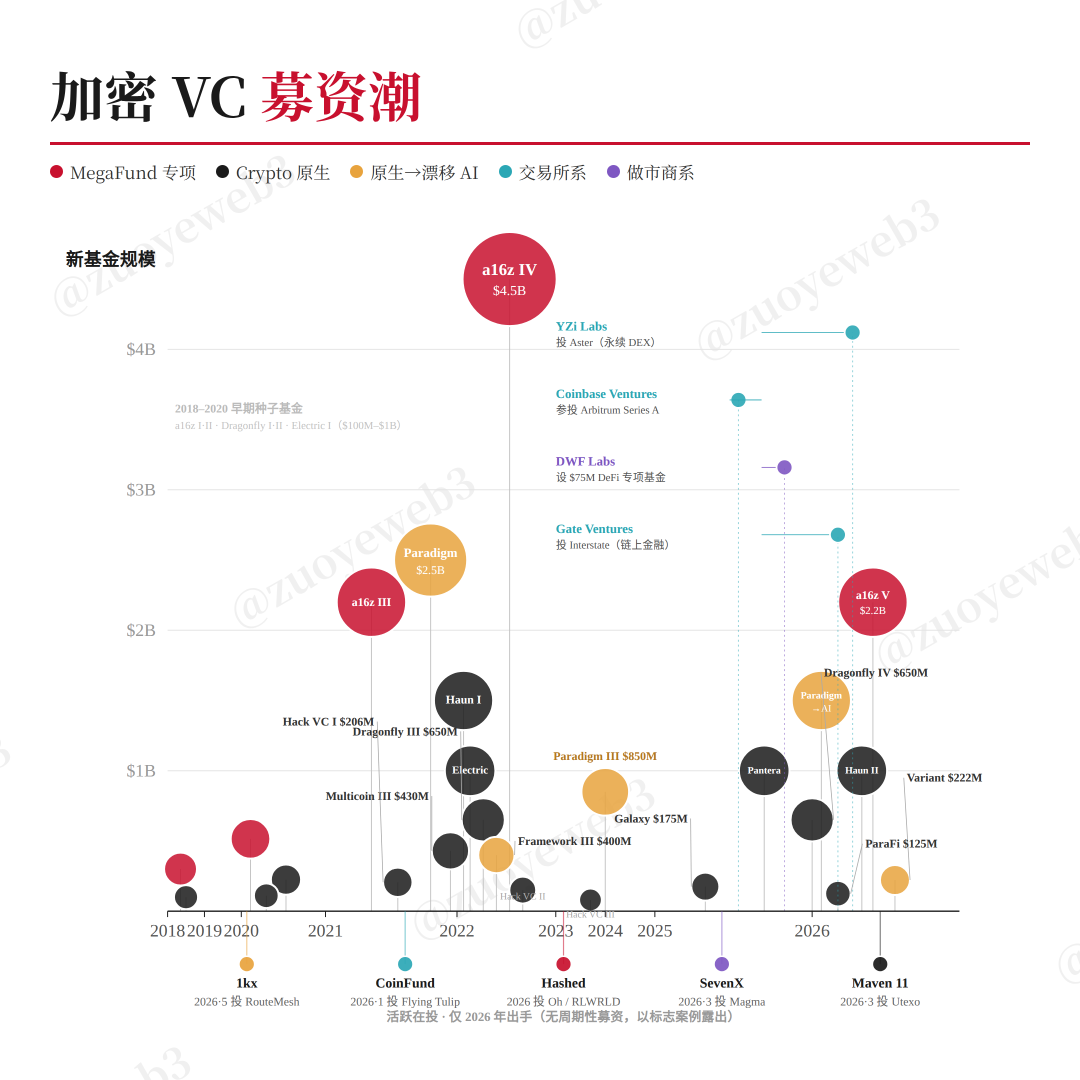

Image Caption: New Fundraising Trends

Data Source: @PitchBook

In this extreme scenario, VCs that can successfully raise funds and invest have turned venture capital into a Ponzi-like capital game.

The glossy return rates of VCs need to be split into three parts: DPI for old LP exits, IRR for existing holdings, and APY for fundraising. DPI is the real APY; the money from new LPs is the TVL attracted by it.

We cannot discover the next project suitable for airdrop hunting from RootData's fundraising projects, nor can we distinguish the proportion of funding amounts actually received. The entire crypto industry has fallen into a non-investment era lacking signals.

Or, transform into a secondary US stock research institution, which is also an important driving force for Pre-IPO and listing US stocks on chain.

No one can create industry-level investment entry signals. Vitalik envisioned using options to reshape DeFi mechanisms. I cannot evaluate right or wrong, true or false, but the mechanism becoming complex is itself a signal.

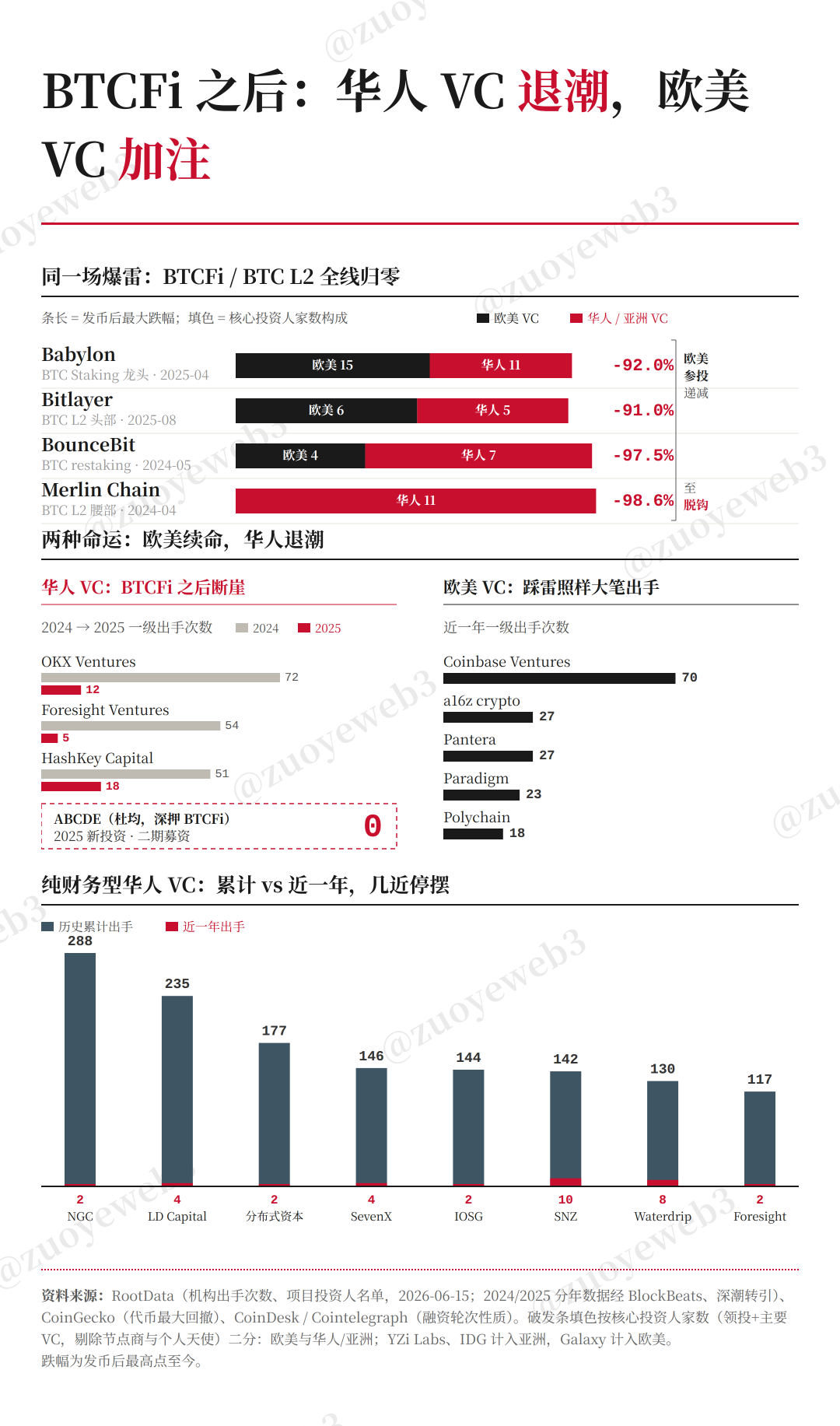

But I can outline the process of the signal collapse for Chinese entrepreneurs. During the BTCFi wave at the end of 2024, a group of Chinese VCs ceased activities, completely unable to exit. It was the despair of being unable to exit even if listed on junk exchanges.

Image Caption: BTCFi Crushes Chinese VCs

Image Source: @zuoyeweb3

Before this, Chinese VCs undertook the dual role of project discovery and initial pricing. After gaining recognition from Chinese VCs, project parties could enter the vision of "more mainstream or more money" US VCs, obtaining higher-level valuation numbers.

However, after US VCs encountered repeated torment from ETH L2 and BTC L2, they can still rely on capital advantages to seize the pricing power of subsequent stablecoins and RWA.

Chinese VCs, after this, are basically out of the new round of Perp DEX competitions. Only Chinese exchange VCs can barely participate. However, from the perspective of the entire industry landscape, Chinese people can only be trapped in the trading track, while broader financial services such as payments (stablecoins) and RWA have encountered dual access restrictions for Chinese entrepreneurs and investors.

The good thing about Water Margin is surrender; the bad thing about crypto is the cycle.

The Agent wave has flooded once, the lobster craze has basically receded, and Coding Agent hype has given way to hardware chips. However, note a long-term trend: we have basically not yet seen the application paradigm under the new technology wave.

The K-shaped differentiation law still applies. The reshaping and transformation of the crypto circle by Agents will almost certainly happen rapidly at a certain hot spot, born in a certain track, and the winning move can be completed within 2~3 months.

If it is not born in this cycle, then we can only continue to lie low. Once the signal is issued, investors and entrepreneurs can feel the super-fast rhythm of the $1B capital pool. This is also the eternal charm of the crypto circle.

Conclusion

This is the most difficult era for entrepreneurs. Either individual Solo, or giant monopoly. There is no longer space for the slow development of growth stocks; time has become a life-pressing lever that needs to be compressed urgently.

Becoming giants means the business format is mature. Although it will reduce speculative space, there is also enough fault-tolerant space to constantly inspire emerging forces.

We compress space and time, constraining to the topic we want to discuss—macro political changes and the fierce AI wave have not made the crypto market disappear, but the feeling of being unworthy of the status is becoming more serious.

From a personal perception, huge problems have appeared in the market structure. The entire industry lacks consumption. From introducing stock index futures to exchange wealth management activities, no one needs retail investors to hold assets long-term, but constantly "urges" users to add leverage.

This is actually very fragmented. The consequence of giving more choices is that users must make choices at all times and cannot stay for a moment, otherwise the market will collapse immediately.

The market is very cold, but capitalization is accelerating, not stagnating. What I think is, can crypto create the next concentrated wave of 1000x returns.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News