Goldman Sachs Research Report Analysis: DDR5 Spot Prices Up 20%, 2027 HBM Pricing Forecast Raised Over 3 Times

TechFlow Selected TechFlow Selected

Goldman Sachs Research Report Analysis: DDR5 Spot Prices Up 20%, 2027 HBM Pricing Forecast Raised Over 3 Times

The market is factoring the traditional DRAM shortage into the upside potential for HBM annual pricing negotiations.

Written by: Rita

TechFlow Guide

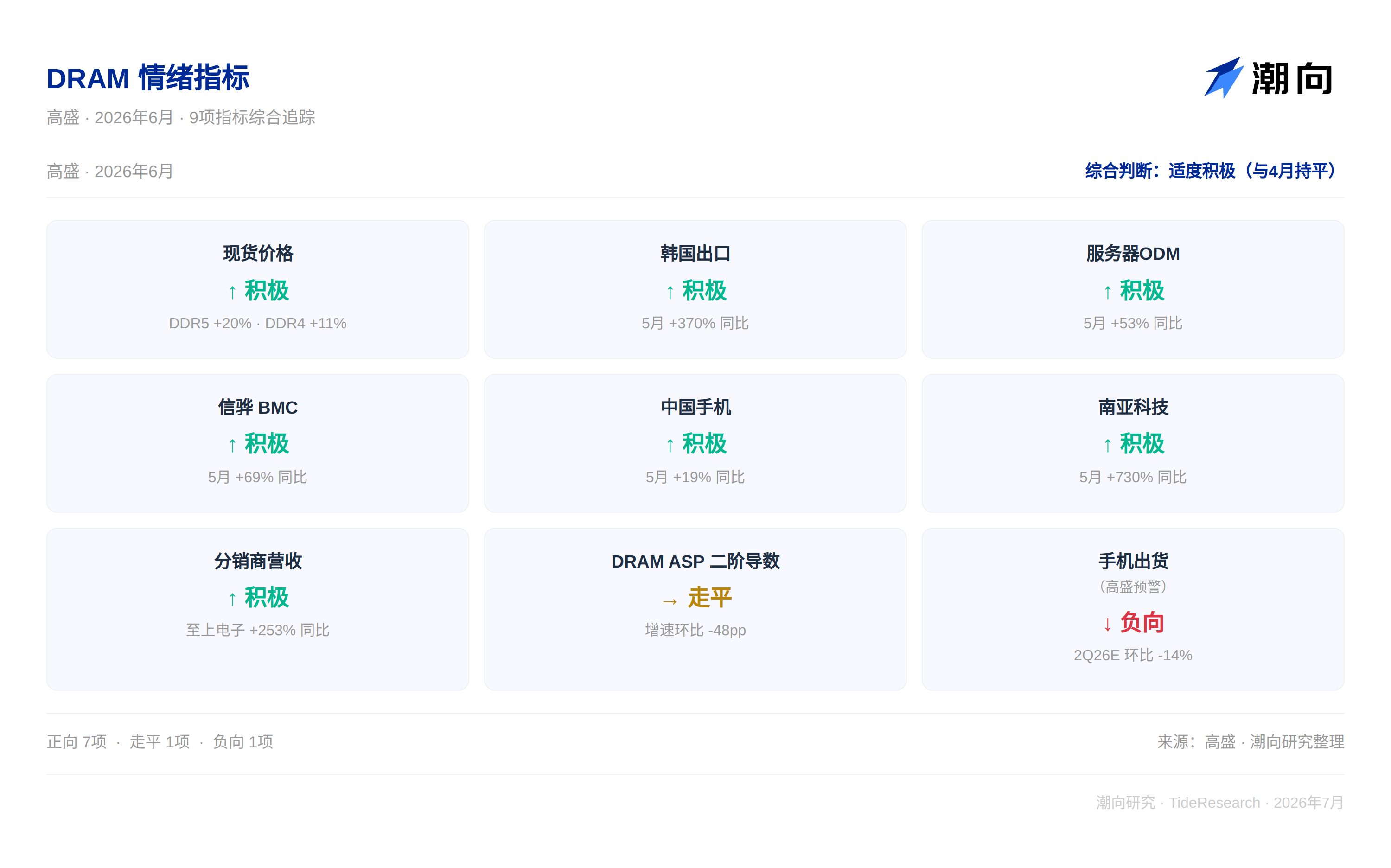

Goldman Sachs released the DRAM Sentiment Index monthly report on June 30, with 7 out of 9 indicators pointing positive, 1 flat, and 1 negative, overall judgment "moderately positive", flat compared to April. But what is truly noteworthy are two things: the price increase inertia of DDR5 is weakening, while the pricing expectation for 2027 HBM is being rapidly revised upward.

DDR5 spot prices have risen 20% since May, South Korea DRAM exports hit a new record high in May, a year-on-year increase of 370%. Nanya Technology has seen triple-digit revenue growth for 10 consecutive months. But the second derivative of Samsung DRAM ASP has turned negative, dropping 48 percentage points, indicating that the acceleration of price increases is weakening. Goldman Sachs this time raised the 2027 Samsung HBM price growth expectation from +14% to +44%, and explicitly stated "there may be upside risks". The storage story is switching from "how much more can it rise" to "how to price after the rise".

DDR5 Price Increases Are Still Running, But Acceleration Is Decreasing

DDR5 16Gb spot prices have risen 20% since May 1, 25% higher than May contract prices. DDR4 8Gb rose 11% in the same period, 45% higher than contract prices. The high premium of spot over contract indicates tight short-term supply and demand, with buyers willing to pay a premium to secure goods.

But the second derivative of Samsung DRAM ASP is worth noting. Goldman Sachs estimates Samsung's Q2 2026 DRAM ASP will rise about 46% quarter-on-quarter, while Q1 rose 93%. The price increase magnitude has shifted from jumping to slow growth. ASP growth rate decreased by 48 percentage points quarter-on-quarter. After the price increase base becomes higher and higher, the increase range will narrow on its own; there is no issue on the demand side.

Servers and Mobile Phones Are Supporting Volume

Taiwan's four major server ODMs (Inventec, Quanta, Wistron Infotek, Wistron) saw May revenue increase 53% year-on-year, rack-level AI servers and ASIC AI server shipments are both ramping up. The world's largest BMC supplier Silicon Motion saw May revenue increase 69% year-on-year, continuing to grow on the high base of 75% in the same period last year.

Mainland China mobile phone shipments in May increased 19% year-on-year, positive growth for two consecutive months. Goldman Sachs China team expects Q2 2026 shipments to decrease 14% quarter-on-quarter, the reason is that storage price increases are raising complete device costs and suppressing terminal demand. This judgment itself constitutes an interesting tension: storage price increases benefit storage manufacturers, but excessive price increases will backfire on downstream demand.

HBM Expectations Are the Biggest Change This Time

Goldman Sachs made a key adjustment to 2027 HBM pricing in the report, raising Samsung HBM price growth expectation from +14% to +44%, more than tripled. The logic is that the current strong pricing trend of traditional DRAM will become the reference system for HBM annual pricing negotiations. The price difference between traditional DRAM and HBM is being widened, giving HBM room for price increases.

Goldman Sachs also explicitly stated "there may be further upside risks", because HBM supply and demand are tight, and the price difference between traditional DRAM and HBM is still expanding. If this judgment materializes, it means the 2027 storage prosperity peak may be higher than the market thinks.

South Korea Export Data Can Verify the Heat

South Korea's May DRAM export value hit a record high, increasing 21% month-on-month and 370% year-on-year, surpassing the previous high in March. Nanya Technology's May revenue increased 730% year-on-year, marking the 10th consecutive month of triple-digit growth, driven by strong DDR4 price increases. Taiwan distributor Sis International's May revenue increased 253% year-on-year and 54% month-on-month, reflecting strong willingness downstream to secure goods.

Samsung Remains the Most Direct Target in This Track

Goldman Sachs maintains a Buy rating on Samsung Electronics, common stock target price 480,000 KRW (currently about 323,000, 49% upside), preferred stock target price 360,000 KRW. Valuation method is 12-month forward EV/EBITDA sum-of-the-parts valuation. Downside risks include significant deterioration in storage supply and demand, sharp contraction in mobile phone profits, and loss of mobile OLED market share.

TechFlow Perspective

The detail truly worth noting in this Goldman Sachs monthly report is: 2027 HBM pricing expectation raised from +14% to +44%. The market already knows that DDR5 is still rising, but the upward revision of HBM pricing is new. This means the market is converting the shortage of traditional DRAM into upside space for HBM annual pricing negotiations.

Another noteworthy data point is the ASP second derivative turning negative. The cycle has not peaked yet, but the phase of "rising faster and faster" has passed. Now entering the phase of "still rising, but rising slower". Historically, storage stocks in this phase mainly earn money from earnings realization, with limited space for further valuation expansion.

For Chinese investors focusing on US stocks and A-share storage concepts, this report hints at two clues: in the short term, DDR5 and DDR4 spot premiums remain, but the accelerated rise phase is nearly over; in the long term, the upward revision of HBM pricing indicates the 2027 peak is higher than previously imagined. The intersection of the two determines how positions in storage stocks should be allocated now.

Disclaimer

This article is TechFlow Research's organization and interpretation of third-party brokerage research reports. Ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage analysts, representing only their affiliated institution's stance, not representing TechFlow Research's views, nor constituting any investment advice.

Market involves risks, decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News