Dissecting Semiconductor "Chemical Key" Hydrofluoric Acid Concept Stocks: Industry Chain Already Fully Priced In, Divergence Just Beginning

TechFlow Selected TechFlow Selected

Dissecting Semiconductor "Chemical Key" Hydrofluoric Acid Concept Stocks: Industry Chain Already Fully Priced In, Divergence Just Beginning

The industry chain logic is sound, but the pricing space is already narrow.

Author: David, TechFlow Research

Electronic Grade Hydrofluoric Acid has been in high demand recently.

On July 1, Taiwan's "Economic Daily News" reported that TSMC, Samsung, and SK Hynix are all scrambling to purchase this material, and suppliers have raised prices by 20% to 30%.

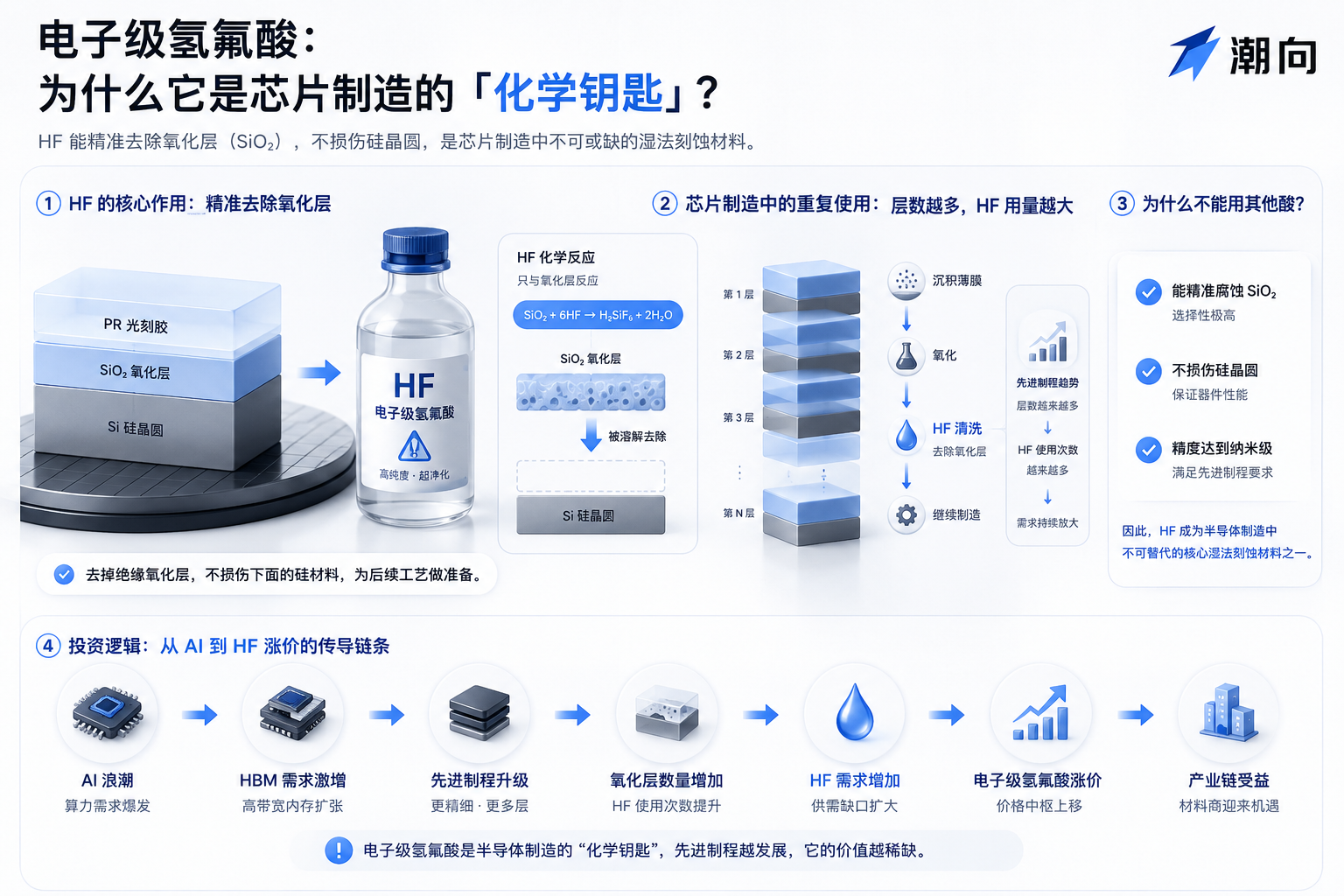

Simply put, during chip manufacturing, a layer of silicon oxide film forms on the wafer surface, which must be precisely dissolved with chemicals to proceed. Electronic Grade Hydrofluoric Acid does exactly this:

Dissolving silicon oxide without damaging the underlying circuits, it is one of the chemicals consumed most heavily in the wafer cleaning and etching processes, known in the industry as the "chemical key".

Hydrofluoric acid production requires fluorspar plus sulfuric acid. Shipping disruptions in the Strait of Hormuz pushed sulfur prices higher, sulfuric acid followed suit, and production costs went up; South Korean local material suppliers were forced to start purchasing raw materials in large quantities from mainland China at a premium about 40% higher than the beginning of the year.

Following this logic, the A-share fluorine chemical sector started moving in mid-May, and the gains have been significant so far, with a batch of related individual stocks trading near their 52-week highs.

Shortages, price hikes, domestic substitution... the market has basically heard and accepted these stories.

At this level, it is more important to figure out which companies in this broad rise have real earnings realization and which are just being pushed by sentiment.

From Fluorspar to G5, A Major Breakdown of the Industry Chain

The raw material chain for Electronic Grade Hydrofluoric Acid is very short: fluorspar (calcium fluoride) plus sulfuric acid, high-temperature reaction generates Anhydrous Hydrofluoric Acid (AHF), which is then repeatedly purified to obtain electronic grade products of different purity levels.

Purity levels are divided into five grades from G1 to G5 according to SEMI international standards, G5 is the highest grade, capable of meeting advanced processes of 14nm and below, meaning those production lines running at TSMC, Samsung, SMIC, as well as storage products like HBM which have extremely high requirements for cleaning purity.

On this chain, the distribution of money is extremely uneven.

- Upstream fluorspar and anhydrous hydrofluoric acid are commodities, large volume but thin gross margins, prices follow the sulfuric acid and non-ferrous metal cycles;

- Midstream ordinary Electronic Grade Hydrofluoric Acid (G1 to G4) has many competitors, transparent prices, and average profits.

- The real money is concentrated in the G5 segment: according to industry data cited by East Money, G5 product spot prices are between 180,000 to 200,000 yuan/ton, leading enterprise gross margins are 50% to 60%. The global high-end G5 supply gap is close to 70%, and spot supply remains tight.

The reason G5 can earn so much lies in two barriers.

- Technology: Purity must reach 7N to 11N (99.99999% to 99.999999999%), the refining capability of the production process directly determines whether the product is usable.

- Certification: Entering the supply chains of TSMC, Samsung, SK Hynix, the certification cycle usually takes two to three years, only after passing can mass supply occur. With the two barriers combined, globally only a handful of enterprises can meet both simultaneously.

In this area, Japanese enterprises have long monopolized this position.

Stella Chemifa, Morita Chemical, and Central Glass combined account for close to 40% of global high-end capacity, with the best technical indicators globally; South Korea's Soulbrain and ENF Technology focus mainly on G3 to G4 mid-to-low end, with very little local G5 capacity, and 90% of anhydrous hydrofluoric acid raw materials rely on imports from China.

Chinese manufacturers have successively broken through G5 in recent years, domestic effective capacity has exceeded Japan, becoming the world's largest high-end supply base. According to G5 capacity and customer certification status, A-share related targets are roughly divided into three tiers:

First Tier: Large-scale G5 mass production, obtained international major factory certification

- Do-Fluoride (002407) — No. 1 domestic G5 capacity, 40,000 tons/year, passed TSMC 3nm, Samsung, SK Hynix, SMIC four certifications, global market share about 25%

- Zhongjuxin (688549) — G5 capacity 30,000 tons/year (another 30,000 tons under construction at Qianjiang base), Juhua Shares and National Integrated Circuit Industry Investment Fund hold shares, bound to SMIC, Hua Hong, CXMT, entered SK Hynix supply chain

- Sanmei Shares (603379) — Total Electronic Grade Hydrofluoric Acid capacity 50,000 tons/year, G5 accounts for over half, passed Japanese and Korean top manufacturer certification, high export proportion

- Binhua Shares (601678) — Existing G5 capacity 6,000 tons/year, already full production overload, 17,000 tons high-end capacity under construction expected to start production in 2027, supplying YMTC, CXMT

Second Tier: Mainly G4, upgrading to G5

- Jianghua Micro (603078) — Old-brand wet electronic chemicals manufacturer, hydrofluoric acid covers G2 to G4, supporting domestic panel and mature process production lines, simultaneously laying out G5

- Jingrui Electronic Materials (300655) — Electronic Grade Hydrofluoric Acid capacity 22,000 tons, mainly G4, G5 grade electronic grade sulfuric acid already mass supplied to SMIC (this company will be mentioned later)

Upstream Resources: Fluorspar

- Jinshi Resources (603505) — A-share's only pure fluorspar resource leader, reserves over 20 million tons, supporting 300,000 tons anhydrous hydrofluoric acid capacity, positioning for pricing power on the cost side

One sentence to summarize the money-making model on this industry chain:

Upstream earns money from resources, midstream earns money from scale, G5 earns money from barriers. In the current price hike cycle, the G5 segment has the largest profit elasticity and is also the segment most fiercely speculated by the market.

Similar Gains, But Completely Different Logic

The chart below is very intuitive, individual stocks across the entire industry chain are almost all trading near 52-week highs. But looking closely, the themes and narratives differ greatly.

Do-Fluoride: Profits Are Real, But Not from Hydrofluoric Acid

Public data shows, Do-Fluoride's net profit attributable to shareholders in Q1 2026 was 376 million yuan (+480%), net profit excluding non-recurring items 380 million yuan (+1724%), one quarter exceeded the full year 2025.

Huaan Securities upgraded to Buy rating, expects 2026 to 2028 net profits of 1.724 billion, 2.335 billion, 3.260 billion yuan, corresponding PE ratios of 29, 22, 16 times respectively.

Where do the profits come from?

According to Sina Finance, in the first three quarters of 2025, the new energy materials sector (mainly Lithium Hexafluorophosphate) revenue proportion was 34.97%, gross margin surged from 8.62% to 19.53%, it is the largest profit engine. Lithium Hexafluorophosphate is a lithium battery electrolyte raw material, has nothing to do with semiconductors.

This round of Lithium Hexafluorophosphate rose from 47,000 yuan/ton in July 2025 to 130,000 yuan/ton in Q1, Do-Fluoride as the world's second largest supplier (shipments about 50,000 tons, market share about 20%), captured all the elasticity of the price hike. Some brokerages calculate that this item alone could contribute net profit over 2 billion yuan in 2026.

On the hydrofluoric acid side, Do-Fluoride itself said on the investor interaction platform in November 2025: "Semiconductor grade hydrofluoric acid market prices are stable, fluctuations are small."

The market buys Do-Fluoride under the label of "Hydrofluoric Acid Price Hike Leader", but its Q1 profit surge relies on Lithium Hexafluorophosphate price hikes, has little to do with semiconductors. And Lithium Hexafluorophosphate prices are already falling back.

Zhongjuxin: Already Up Four Times, But Company Denied the Labels the Market Gave It

Zhongjuxin rose from 52-week low 7.44 yuan to 39.74 yuan, the largest gain on the entire industry chain. Full year 2025 loss 16.59 million yuan. Q1 2026 just turned profitable, net profit attributable to shareholders 6.37 million yuan.

On May 15, the day of the limit-up, the company issued an abnormal fluctuation announcement, three original sentences were: "Electronic Grade Hydrofluoric Acid business sales proportion is limited"; "There is no direct business dealings with Samsung Electronics regarding Electronic Grade Hydrofluoric Acid products"; "No substantive price hike order agreements signed with relevant customers for the above products"...

Zhongjuxin's main business is the overall supply of electronic wet chemicals, hydrofluoric acid is just one category.

Before capacity starts production and profits truly emerge, the current price of 39.74 yuan corresponds to a company that earned 6.37 million in Q1. The gap in between is filled entirely with expectations.

Jianghua Micro, Jingrui Electronic Materials: Business Matches, But Must Distinguish Who Has Orders and Who Is Still Waiting

Jianghua Micro rose over 200% in a year, main business is wet electronic chemicals, laying out G5 grade hydrogen peroxide and ammonia water.

Its advantage is wide product line, broad customer coverage, domestic panels and mature process production lines are all using its stuff. Laying out G5 means it is moving from low-end to high-end, but G5 products are still in customer certification stage, whether it can get advanced process orders, currently no public information can confirm.

Jingrui Electronic Materials rose 130%, 7% from high point, relatively least extreme position in this batch. It has something most peers do not:

G5 electronic grade sulfuric acid already mass supplied to SMIC, revenue proportion raised from 5% to 20%. This is an order already landed. In an environment where the entire chain is generally priced by expectations, companies with real shipments will have relatively stronger resistance to falls during pullbacks.

The rest such as Jinshi Resources rose about 50%, the mildest on the entire chain. It is a fluorspar miner, earns money from resource price hikes, connection to semiconductors is indirect. Fluorspar price hikes, anhydrous hydrofluoric acid costs go high, transmitted to electronic grade product prices; more like the "cost pusher" of the entire chain, rather than a direct beneficiary of terminal demand.

Data Worth Paying Attention To

A-share theme stock short-term pricing and fundamentals are often two different things. For the hydrofluoric acid sector which has collectively hit the ceiling, short-term and mid-term things to watch are different.

Short-term Look at Capital and Sentiment, Not Fundamentals

Do-Fluoride's Dragon Tiger List data from recent limit-ups can explain some things.

June 11 limit-up (closed at 38.19 yuan), turnover 7.92 billion, turnover rate 20.13%. Dragon Tiger List shows institutional special seats net sold 179 million yuan, hot money "Chengdu Series" net bought 226 million yuan, "Quantitative Limit-Up" seats net bought 77.14 million yuan;

June 22 limit-up again, turnover 7.906 billion, institutions net sold 147 million yuan, brokerage seats net bought 490 million yuan. (Above data comes from SZSE public information, all are after-market data for corresponding dates)

Two limit-ups present the same structure: Institutions are selling, hot money is buying.

On June 29, Do-Fluoride topped the Tonghuashun Hot Stock List. Today, July 1, one-word limit-up to 52-week new high.

From experience, when a theme stock simultaneously meets these conditions "topped hot stock list", "continuous limit-up huge turnover", "institutions continuous net sell", it often means sentiment has reached a very high temperature.

Next few possible catalyst nodes:

South Korean manufacturers further price hikes in June to July (Korean media expectation), Do-Fluoride and Zhongjuxin interim reports (around mid-August), CXMT Technology IPO listing (market expects mid-July to early August).

If these events can continue to create topics, short-term sentiment can still support; otherwise, the profit-taking pressure after huge turnover will appear quickly.

TechFlow Analysis

The supply and demand logic of this industry chain is solid. AI expansion pulls demand, Japanese companies not expanding capacity, South Korea relies on imports, prices are indeed rising.

But the stock prices of the entire sector are indeed at high levels, leaders rose three to five times, Dragon Tiger List shows institutions selling, hot money taking over, heat indicators (hot stock list top, huge turnover, ETF premium) all maxed out.

At this position, the importance of industry logic is already less than odds, correct logic can also be priced to leave no space.

If one must find relative positions in this chain, Jingrui Electronic Materials is still 7% away from the high point, least extreme in the entire industry chain, and has landed G5 sulfuric acid orders; Jinshi Resources gain is mildest (about 50%), but it earns money from fluorspar price hikes, relationship with semiconductors is indirect.

August interim report season, may be the hard checkpoint for the hydrofluoric acid sector; those whose earnings cannot catch up with stock prices, will fall back first when sentiment recedes.

Disclaimer: This article is for analysis reference only, does not constitute any investment advice. Stock market has risks, investment needs caution. All data comes from public information, author does not bear any responsibility for data accuracy and completeness.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News