Ethereum’s Ballmer Moment: While Everyone Is Bearish, the Circulating Supply Is Disappearing

TechFlow Selected TechFlow Selected

Ethereum’s Ballmer Moment: While Everyone Is Bearish, the Circulating Supply Is Disappearing

The surface narrative is bearish, but the underlying fundamentals are growing steadily.

Author: Ben Lakoff

Translated and edited by TechFlow

TechFlow Intro: When the Bankless founder dumped all his ETH and 19-year-old developers flocked to Solana, the bearish narrative around Ethereum had become consensus. Yet Ben Lakoff, Partner at BanklessVC, argues this mirrors Microsoft’s “Ballmer era”—a surface-level bear story masking steady, underlying fundamental growth. A 30% staking rate, ETF inflows, and regulatory clarity are shrinking the circulating supply; meanwhile, crypto regulation has evolved from an existential threat into a formal legal framework—precisely the moment to step in.

Welcome to the May on-chain transaction flow summary.

This month’s thesis section is slightly longer, so I’ve placed it upfront. All funding rounds, fund raises, and hackathon results follow at the end.

Ethereum’s Ballmer Era

Last month, David Hoffman sold all his ETH at $2,070 and published a thoughtful article explaining why. It went viral across X (formerly Twitter).

David then appeared on the Chopping Block podcast—a conversation I greatly enjoyed. Tarun said Ethereum is “stagnating” because no 19-year-olds want to build there. Max Resnick labeled the Ethereum Foundation “risk-averse.” And the bullish Haseeb dubbed the entire bear thesis: “Ethereum’s Ballmer era.” That framing resonated deeply with me.

This framework is too good to let pass.

Yes, I’m long crypto. I’m long BTC. I’m long ETH… I’m long this trend. But pretending the bear narrative is weak would be self-deception—so I’d like to elaborate further on my stance. These are my views—not necessarily those of BanklessVC, and certainly not investment advice.

The Bear Narrative Has a Name—and It’s Right

The substance is real. In fact, we’ve fallen another 10% since that article was published.

David’s argument: ETH as money is inherently a long-term bet—and the rollup-centric roadmap makes it even longer. Ethereum is a “giver, not a taker”… designed to distribute blockspace at cost. L2 profit margins reach 98% of blob revenue. Gas limits are gradually rising past 100 million+. The BPO fork aggressively expands blob supply. The surge in stablecoins—from $3 billion to $163 billion—creates value for Circle and Tether, not ETH. Meanwhile, SOL, NEAR, BNB, and TRX have revalued themselves as fee-driven comparables. Mechanically, he’s correct. The protocol is designed for abundant blockspace—which is precisely the opposite of what you’d want for fee-driven value capture.

Tarun’s “stagnation” point is the cultural version of the same issue. Talent follows founder energy—and that energy now resides on Solana, Monad, Hyperliquid, and whatever comes next (perhaps not Ethereum, perhaps not crypto). Resnick’s “risk-averse EF” is the institutional version: the Foundation, at a moment demanding competitiveness, remains devoutly focused on safeguarding network integrity.

Haseeb is right. A “Ballmer era”: slow product cadence, botched transitions, sharper competitors with killer instinct, and loud, correct critics.

What Microsoft Actually Paid During Its Ballmer Era

Steve Ballmer ran Microsoft from 2000 to 2014. The meme: “Wasted 14 years.” Missed mobile, missed search, missed social, shipped Vista, threw chairs.

That’s the meme I remember—but what the meme omits matters. Microsoft stock flatlined for over a decade, while its enterprise franchise compounded relentlessly underneath. Dividends did most of the work. Office and Windows licensing kept printing money throughout the “Microsoft is dead” narrative. Then Satya took over—and MSFT rose 10x.

The lesson (at least in Microsoft’s case) is that deeply integrated, enterprise-loved, time-tested infrastructure often compounds steadily—even amid its own bearish narratives. Those narratives are often superficially correct—yet insufficient to short.

Ethereum remains the largest trusted-neutral public blockchain for tokenized assets. BUIDL launches there. ~66% of USDC supply lives there. Deepest DeFi liquidity resides there.

But the lead is narrowing rapidly. BUIDL isn’t just on Ethereum anymore (now ~40%, down from ~85% a year ago). USDC exists across 34 chains. Western Union chose Solana—not Ethereum—for USDPT. Institutional defaults are shifting from singular “Ethereum” to plural “public blockchains.”

Still bullish for the incumbent—just no longer monopolistic. Whether 19-year-olds want to build there is a genuine long-term concern. But it’s not the question determining the next two years.

Beneath the Noise: The Circulating Supply Is Collapsing

This is the part most bear narratives ignore.

~30% of ETH is staked. Treasury corporations hold another >6%—and growing. BitMine alone holds 4.47% of supply and publicly targets 5%. Spot ETFs continue absorbing more. The March 17 SEC/CFTC ruling classified staking rewards as non-securities—unlocking the entire staking ETF pipeline. Five additional issuers (Fidelity, Franklin, Invesco, 21Shares, VanEck) await Q2 decisions on staking amendments.

Every ETH staked via ETF is ETH that cannot be sold on price impulse. Net issuance runs at ~0.23% annualized. The circulating supply is shrinking faster than that—and on most days, these receiving endpoints are bidding against each other. Math doesn’t care if ETH is boring.

So David is right: ETH won’t reprice due to fee burns. The roadmap chose abundance. But ETH *can* reprice due to circulating supply compression, staking yield demand, and institutional Schelling-point premium—without winning the fee war. At least in the near term.

Crypto’s TAM Continues Rising

Zoom out from ETH. The real story over the past 12 months is that crypto regulation has shifted from an existential threat to a formal legal framework.

The GENIUS Act is law. Payment stablecoins now operate under a federal regime. The CLARITY Act passed the House last July, cleared the Senate Banking Committee on May 14, and structurally looks likely to pass before the midterms. Stablecoin circulation exceeds $280 billion—and is compounding. Tokenized Treasuries are scaling. Spot ETFs now exist across an expanding set of assets.

This isn’t crypto’s death rattle. It’s crypto becoming a regulated, trillion-dollar slice of the financial system—where boring institutions are *required* to plug in.

In prior bear markets, we genuinely worried whether this ecosystem would survive. But there are caveats—and they matter.

First: Crypto winning ≠ decentralized crypto winning. The truly terrifying bear scenario isn’t David’s fee math. It’s “blockchain wins” looking like Canton, JPM Onyx, DTCC’s permissioned ledgers, and a few Avalanche subnets—with the public crypto asset complex capturing virtually no real value.

That world exists (and is concerning)—but I’ll bet on the public chain side, for several reasons. Pure permissioned chains as the institutional answer have been pitched for a decade—and continue losing adoption (maybe this time is different?). The architecture actually winning is permissioned assets *on public chain rails*: BUIDL, BENJI, Ondo’s USDY. Tokens enforce KYC and transfer restrictions; settlement runs on Ethereum, Solana, and other public infrastructure. Empirical track records of KYC pools coexisting alongside open public pools (Aave Arc, Compound Treasury) show they fail.

This remains bullish for public chains as settlement layers—including ETH. But it’s weaker than full DeFi composability. Permissioned assets can’t freely compose with open pools—but gated-access versions are the winning model.

Second: The question is no longer *whether* crypto adoption will happen—but *which* crypto captures it. The honest answer is: not all will flow to ETH—but the vast, institutionalized, regulated, “trusted-neutral-required” portion almost certainly will. Because the alternative is asking Tier-1 banks to settle tokenized assets on chains run like startups… unlikely.

This is where the Ballmer framework underestimates the bull case. It only works if the underlying market keeps growing. And crypto’s underlying market *is* growing—fast, and in the most regulator-blessed, institutionalized way possible.

The Barbell Strategy: Long the Trend, Not Extremism

The bear narrative I take seriously isn’t the fee analysis—it’s leadership and competition. The EF may indeed need its “Satya moment.” The killer-instinct vacuum is real. Solana, Monad, and Hyperliquid aren’t slowing down. ETH/BTC and ETH/SOL may consolidate or drift lower before turning.

The positioning around this is simple: stop being an extremist.

Hold ETH for the time-tested/institutionalized/circulating-supply-compression trade. Hold SOL for the consumer/throughput/distribution trade. Hold BTC for macro hedging. Hold a small basket of next-gen L1s and application-layer winners—where cultural energy is actually flowing.

I know. ETH is a $250B asset, macro-sensitive, and your capital allocation always involves trade-offs. I’m not an extremist—but I’m still long ETH. Here’s why:

The circulating supply is shrinking faster than issuance.

Q2 staking ETF approvals are a live, date-stamped catalyst.

The CLARITY Act’s passage broadly unlocks institutional crypto. Clearer rules enable regulated capital to deploy massively across the entire asset class. ETH’s moat remains its incumbent network effects + trusted neutrality—making it the default public-chain settlement layer for tokenized assets, even as its lead narrows.

The bear narrative is so loud it’s become consensus. Historical hit rates for consensus bears after a 60% drawdown from $2,000 are low.

The option value of a “Satya moment” is unpriced. If the EF is restructured—or a more aggressive entity emerges to lead protocol development—that’s pure upside space absent from any bear model.

I see this trade as “David is partially right—and ETH still works.” Microsoft worked under Ballmer. Crypto adoption is winning. The asset you most want to own is the one most deeply embedded in the part of crypto the U.S. government just spent two years building rules for.

Step back and listen to what regulators are actually saying. The SEC and CFTC are telling you they want finance rebuilt on-chain. Move the dollar on-chain. In that world, how could this *not* be wildly bullish? Maybe if you’re a cypherpunk, this isn’t the world you envisioned… gated assets, KYC rails, everything permissioned. But for public chains as settlement infrastructure? Unambiguously bullish.

This is the critical inflection point in the cycle. AI is the center of attention—period. It’s hot, parabolic—and as an early investor, that’s exactly the problem. You want to deploy capital where it’s *not* hot. When a sector is this overheated, it’s hard to deploy capital without paying a premium—except at the very earliest seed/pre-seed stage.

Crypto, right now, is *not* hot. The bear narrative is consensus. Energy is elsewhere. This is the setup you *want*—not the one you’re trying to flee.

Over a long enough timeline, everything becomes AI—and everything becomes blockchain. One of those is priced *as if it’s already happened*. The other just secured a two-year, legally enshrined head start—while everyone looks elsewhere.

Strap in. Now onto the rest of May’s crypto/web3 funding:)

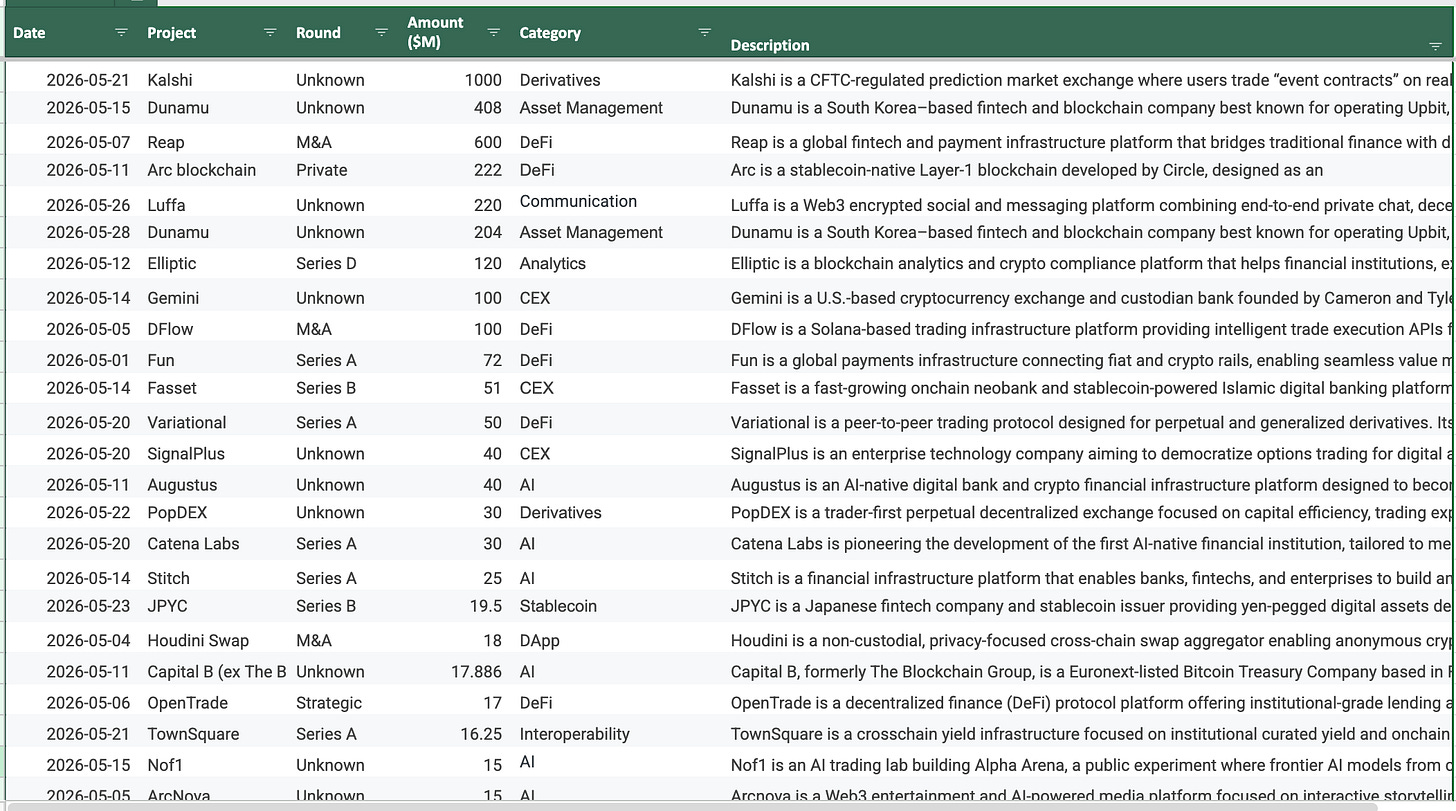

Top 10 Crypto Funding Rounds

Kalshi | Series F | Prediction Markets | $1B | 2026-05-07

Led by Coatue, with participation from Sequoia, a16z, IVP, Paradigm, Morgan Stanley, and ARK Invest. This $1B round values Kalshi at $22B—double its $11B valuation just five months earlier. Annualized trading volume tripled to $178B in six months; institutional volume grew 800%. Kalshi is regulated by the CFTC—not crypto-native—so consider it asterisked on this list. But it now commands >90% of U.S. prediction market activity—the cleanest on-ramp story crypto currently has.

Dunamu (Upbit) | Strategic Investment | Centralized Exchange | $408M | 2026-05-28

Three Samsung-affiliated entities (Samsung Securities, Samsung SDS, Samsung Card) agreed to acquire a 4% stake in Dunamu—the operator of Korea’s largest crypto exchange, Upbit—for ~$408M ($612.8B KRW) from Kakao. Each buyer cited positioning ahead of Korea’s upcoming Digital Asset Basic Act—for KRW-pegged stablecoins, tokenized securities, and on-chain settlement. Part of a May sprint transferring ~14% of Dunamu’s equity to Korean giants like Hana and Hanwha. Closing scheduled for June 19.

Circle (Arc) | Token Presale | Infrastructure/Stablecoin | $222M | 2026-05-11

Circle raised $222M (FDV: $3B) for Arc—the institutional L1 it’s building for stablecoin settlement and tokenized assets. a16z crypto committed $75M; BlackRock, Apollo, ICE, Standard Chartered Ventures, SBI, Janus Henderson, General Catalyst, Marshall Wace, ARK, Haun, and Bullish also participated. This is 2026’s clearest signal that traditional finance is choosing its lane: a regulated stablecoin issuer building its own chain—with the world’s largest asset managers on its shareholder list.

Ripple (Ripple Prime) | Debt Financing | Infrastructure/Main Brokerage | $200M | 2026-05-11

Ripple secured $200M in debt financing from a fund managed by Neuberger Specialty Finance to expand lending capacity for its multi-asset main brokerage, Ripple Prime. Existing institutional loans serve as collateral. Since Ripple acquired the platform in 2025, Ripple Prime’s revenue has tripled YoY. Traditional finance credit now secures the loan book for crypto main brokerages.

Elliptic | Series D | Compliance / AI × Crypto | $120M | 2026-05-12

Led by One Peak ($120M round, $670M valuation), with participation from Nasdaq Ventures, Deutsche Bank, and UK Commercial Bank. Largest pure-equity VC round this month. Elliptic is building proxy-based AML/compliance tooling. Interpreted post-April: this is the operational and compliance layer DeFi keeps being reminded it needs—now backed by traditional finance capital.

Fun | Series A | Payments/Consumer | $72M | 2026-05-01

Colead by Multicoin Capital and SignalFire, with Infinity Ventures, Pharsalus Capital, and Justin Mateen participating. Fun is a crypto/fiat on/off-ramp powering financial platforms like Polymarket. Largest consumer/payments VC round this month—a clean bet on the prediction market and consumer crypto hype cycle.

Fasset | Series B | Stablecoin/Payments | $51M | 2026-05-14

Led by SBI Group ($51M round), with Investcorp and Arz Portföy participating. Fasset is a stablecoin-powered neobank targeting emerging markets, with ~$32B annualized transaction volume. Real-world validation of the stablecoin-as-payment thesis—and happening where it matters most: corners of the world where dollar rails genuinely change lives.

Variational | Series A | DeFi/Derivatives/RWA | $50M | 2026-05-20

Led by Dragonfly, with Bain Capital Crypto and Coinbase Ventures participating. Variational operates an RFQ-based platform for on-chain perpetuals on real-world assets: oil, gold, silver, copper. The team believes RWA perpetuals may surpass BTC and ETH perpetuals within a year. Most intellectually substantive small deal this month.

OpenTrade | Strategic/Growth Round | Stablecoin/RWA | $17M | 2026-05-06

Supported by Mercury Fund and Notion Capital for $17M to scale its yield infrastructure for RWA-backed stablecoins. Another data point for this month’s dominant theme: yield-bearing stablecoins backed by RWA collateral.

Cycles | Seed Round | Infrastructure/Clearing | $6.4M | 2026-05-21

Led by Blockchange Ventures, with Coinbase Ventures, Compound VC, and Primitive Ventures participating. Cycles is building a privacy-preserving multilateral clearing network for on-chain finance and stablecoins. Small in scale—but precisely the kind of institutional-grade plumbing required before the “next $10T inflow” story materializes.

Click here to view all May funding rounds

May Crypto VC Fund Raises

After a busy April, new fund announcements were quieter this month—but two major moves…

Haun Ventures | $1B Fund II | May 2026

Katie Haun’s firm raised $1B across an early-stage fund and a later-stage crossover fund—pushing AUM above $2B. Three priority themes: next-gen financial infrastructure, asset tokenization and new markets, and the “agent economy” where AI systems transact on behalf of humans. Capital will deploy over the next 2–3 years.

a16z crypto | Crypto Fund V: $2.2B | May 2026

The fund we flagged in March as targeting ~$2B officially closed at $2.2B. Full-stack, 10-year term, focused on real-world applications: stablecoins, payments, financial services, perpetuals, lending, prediction markets, asset tokenization. a16z’s characterization: crypto fundamentals are at an “all-time high.”

Reminder: If you’d like to learn more about Bankless Ventures’ Fund II, please fill out this form—we’ll be in touch!

ETHGlobal NYC 2026 | June 12–14, 2026

New York City, in-person. Preceded by ETHConf NYC (June 8–10) and Pragma NYC.

Base Onchain Summer Hackathon | ~June 2026 (dates TBD)

Online. Base’s flagship onchain hackathon; last edition attracted >7,500 developers, with sponsors including Stripe, Shopify, Farcaster, and Zora. (2026 dates unconfirmed—verify on Devfolio.)

ETHGlobal Lisbon 2026 | July 24–26, 2026

Lisbon, Portugal, in-person. Pragma Lisbon on July 25.

Solana Frontier Hackathon | April 6 – May 11, 2026

Online. Crypto’s largest startup competition—~2,857 submissions over five weeks. Prizes: $30K grand prize, $10K each for 20 outstanding teams, plus $2.5M in VC funding and accelerator admission from Colosseum. Winners not yet announced as of month-end; judging ongoing—watch blog.colosseum.com in early-to-mid June.

ETHPrague 2026 | May 8–10, 2026

Prague, Czech Republic (Town Hall). Fifth edition; conference + hackathon, focused on Ethereum’s “solarpunk” future.

Solana Mobile Hackathon | April 2026

Online. Concluded—400+ apps submitted by developers from 66 countries.

Solana Frontier Demo Day | June 2026 (dates TBD)

Online. Final demos from Frontier hackathon teams—expected shortly after winners are announced.

ETHGlobal NYC Demo Day | June 14, 2026

New York City. Project reviews and presentations on the final day of the hackathon.

ETHPrague 2026 Closing Demo | May 10, 2026

Prague. Demos and judging on the final day of the ETHPrague hackathon.

Accelerator Applications Open

Solana Incubator (Batch 5) | Applications Open / Early Deadline ~June 5

New York City. 3-month program starting September 2026; rolling review, with preference for early applicants. Seeking 4–6 teams (existing Solana teams, web3 teams considering Solana, or web2 teams adding web3).

Alliance DAO (ALL18) | Applications Open / Rolling Review

Hybrid (virtual + in-person retreat). ALL18 begins September 7, 2026; interview decisions made ~2 weeks post-application. ~5% acceptance rate; median graduate raise: $3.5M, $25M valuation.

a16z Crypto Startup Accelerator (CSX) | Applications Open (confirm next cohort)

In-person, 9-week program held twice yearly in different cities. $500K for 7% equity; ~3% acceptance rate.

Outlier Ventures Base Camp | Rolling Applications

Hybrid (virtual + in-person). 12-week accelerator accepting early-stage applications for 2026 in DeAI, DeFi, RWA, and DePIN.

Techstars Web3 | Applications Open

Hybrid (virtual + in-person). Reports indicate 2026 applications are open.

That wraps up May!

Thanks everyone—and good luck!

Ben Lakoff, CFA

https://twitter.com/benlakoff

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News