Microsoft’s AI Strategy: A Triple Dilemma—Sliding from Leader to Follower

TechFlow Selected TechFlow Selected

Microsoft’s AI Strategy: A Triple Dilemma—Sliding from Leader to Follower

Whether MAI can launch a truly cutting-edge, general-purpose large model by 2027 will determine how Microsoft’s AI narrative unfolds in its next chapter.

Author: TechFlow

Microsoft has been the biggest beneficiary of the global AI narrative since 2023. Leveraging its early $13 billion investment in OpenAI, Satya Nadella branded Microsoft’s entire product suite—Office 365, Azure, and Windows—with “Copilot,” pushing the company’s market capitalization past $3.7 trillion. Yet entering 2026, this narrative began fracturing across multiple fronts.

The blow was not isolated. Negative developments across security, cost, and market share erupted simultaneously over the past month—symptoms of a single, underlying structural ailment: Microsoft lacks control over its technology stack; it holds no pricing power; and enterprise customers’ wallets are being pried open by competitors.

Copilot Bypasses DLP to Read Confidential Emails—Vulnerability Lurked for Six Weeks

In January 2026, Microsoft 365 Copilot was found to harbor a critical flaw internally tracked as CW1226324. According to reports by SecurityToday and Cybernews, this flaw enabled Copilot to read draft and sent emails marked “Confidential” within Office applications—including Word, Excel, and PowerPoint—bypassing customers’ custom-deployed Data Loss Prevention (DLP) policies.

Internal Microsoft documentation described the issue as “incorrect handling” of emails labeled confidential by the AI system. The vulnerability remained active from January 2026 until early February, when Microsoft began deploying fixes—leaving confidential communications exposed for approximately six weeks. Microsoft has yet to disclose the number of affected enterprises or users.

This is not an isolated incident. On January 15, 2026, security firm Varonis disclosed an attack technique dubbed “Reprompt,” which can bypass Copilot’s data leakage protections via a single malicious link—even persisting after Copilot chat is disabled. That same month, security researchers discovered a CVSS 9.3 zero-click vulnerability in M365 Copilot, enabling attackers to trigger exploitation without any user interaction.

Ilia Kolochenko, CEO of ImmuniWeb and researcher at the European Law Institute, told Cybernews: “Incidents like this may surge in 2026 and could become the most frequent security event type for enterprises globally.” He noted that enterprises’ pace of deploying AI assistants for productivity far outstrips the development of governance frameworks—and traditional DLP systems were never designed to monitor how AI agents access, interpret, and repackage sensitive data.

Gartner forecasts that by 2030, over 40% of enterprises worldwide will experience a security or compliance incident due to unauthorized AI tools. Its 2027 forecast is even more specific: 40% of AI data breaches will stem from cross-border misuse of generative AI. Given Copilot’s deep integration with Microsoft Graph—the unified data layer spanning email, Teams, SharePoint, and OneDrive—a single bypass event potentially compromises an enterprise’s entire core asset base.

Claude Code Licenses Axed—Token Bills Breach AI Budgets

In late May, The Verge first reported internal news confirming that Microsoft’s Experiences & Devices division would terminate most internal Claude Code licenses by June 30, 2026, shifting instead to GitHub Copilot CLI. This division oversees development of flagship products including Windows, Microsoft 365, and Surface—encompassing thousands of engineers.

The internal Claude Code pilot had launched only six months earlier. According to Windows Central citing The Verge, Claude Code enjoyed broad adoption among Microsoft employees. Initial plans called for engineers to use both Claude Code and GitHub Copilot CLI in parallel to compare feedback—but engineers overall preferred Claude Code. The official rationale cited for license termination was “strategic integration,” though multiple sources point to cost as the true driver.

Sesame Disk and several industry publications, citing internal communications, report that Claude Code’s token-based billing model led to unpredictable monthly expenditures—reaching $500–$2,000 per engineer in some organizations. Microsoft’s fiscal year ends on June 30, and the license termination date aligns precisely with this fiscal cutoff.

A parallel case is even starker. Uber CTO Praveen Neppalli Naga previously revealed that after deploying Claude Code to 5,000 engineers, the company exhausted its full-year $3.4 billion AI budget within the first four months of 2026—engineer usage rates climbing to 84–95%. AI Weekly observed that flat, per-seat licensing obscures real token consumption, while enterprise-scale usage-based billing immediately exposes this structural gap.

GitHub is already adapting. Starting June 1, 2026, all Copilot plans will shift to usage-based billing via GitHub AI Credits. Cryptobriefing, citing industry data, notes U.S. AI software prices have risen 20–37%, reflecting the widening gap between corporate spending expectations and the real-world operational costs of scaling AI tools.

This shift poses a direct challenge to Microsoft’s financial model. GitHub Copilot currently serves roughly 4.7 million paid subscribers, generating ~$1 billion in annualized revenue; M365 Copilot boasts 15 million paid seats—but only ~33 million active users, yielding a workplace conversion rate of just 35.8%. As flat pricing transitions to usage-based billing, quarterly profitability will fluctuate with engineering teams’ AI usage intensity—a volatility unprecedented in Microsoft’s subscription business over the past decade.

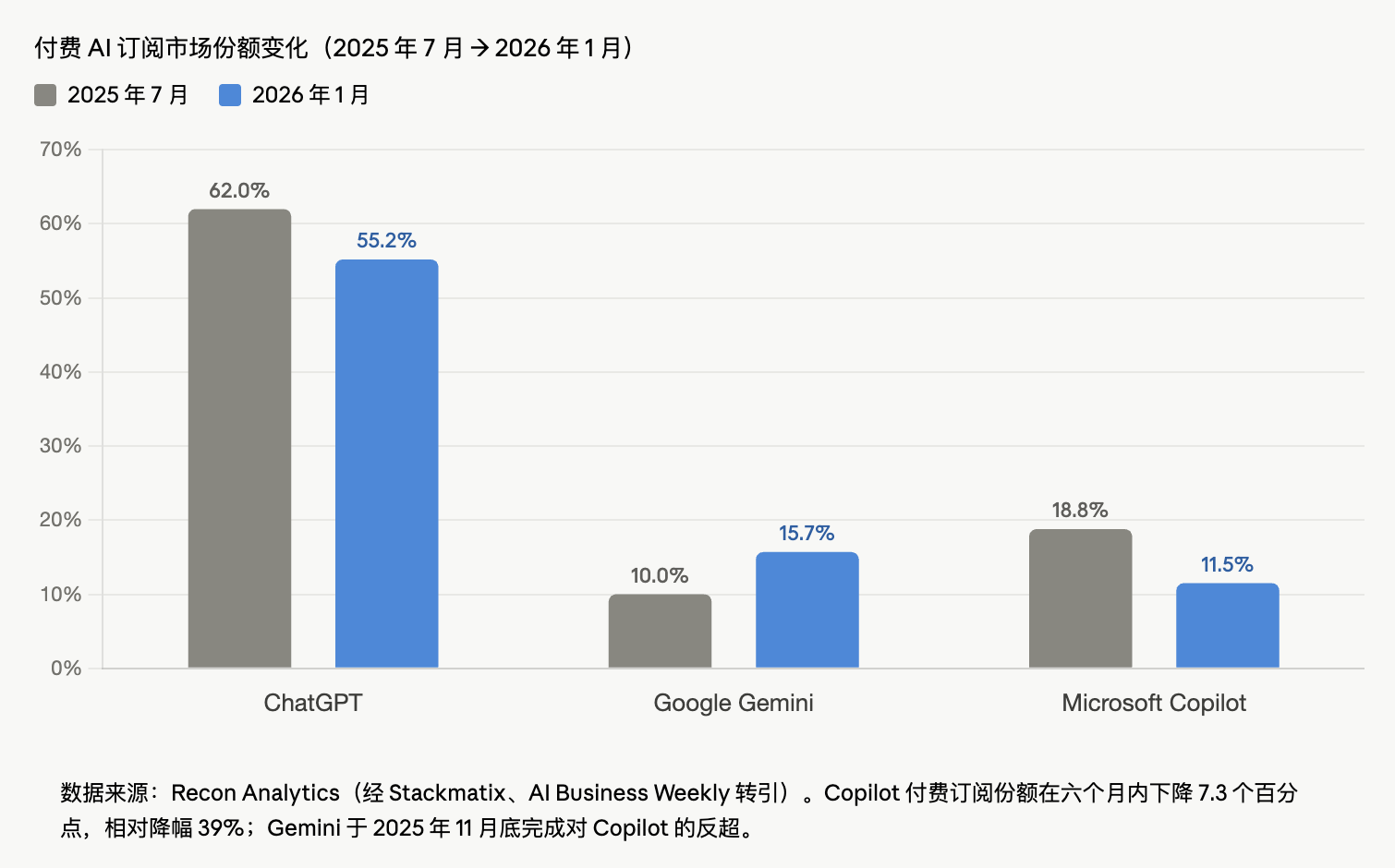

Gemini Overtakes Copilot: Paid Subscription Share Drops Seven Points in One Year

Data on paid AI subscription market share released by Recon Analytics delivers the clearest market verdict. As of January 2026, ChatGPT held 55.2% share, Google Gemini 15.7%, and Microsoft Copilot 11.5%. This marks a sharp decline from 18.8% in July 2025—losing 7.3 percentage points in just six months, a relative drop of 39%. Gemini overtook Copilot in late November 2025.

Paid subscription share is considered the cleanest market signal—it excludes “zombie seats”: enterprise-issued licenses distributed en masse but rarely used actively by employees. Microsoft’s own data confirms this gap: 15 million paid M365 Copilot seats correspond to only 33 million active users, meaning many enterprise-purchased licenses sit idle.

An early 2026 enterprise AI adoption study compiled by UK-based Compare the Cloud shows 82% of Google Workspace users report AI features deliver real value—versus just 66% for Microsoft 365 Copilot users. Gemini’s context window spans ~1 million tokens, while Copilot’s is capped at ~32,000 tokens—roughly 30× smaller—creating a significant disadvantage in long-document analysis scenarios.

Price differences are equally stark. Google bundles Gemini AI into every Workspace plan at no extra cost; Microsoft charges an additional £18 (~$23) per user per month for Copilot atop existing M365 licenses. For a 10-person UK team, the annual cost difference totals ~£1,932.

Even more telling is pricing power. According to CNBC, Microsoft will launch a new top-tier offering, Microsoft 365 E7, on May 1, 2026, priced at $99 per user per month—65% higher than E5’s $60—bundling Copilot AI add-ons, AI agent management, and identity management tools. Judson Althoff, Microsoft’s Commercial Business CEO, told CNBC that E7 and the Copilot upgrade “should drive further Copilot adoption,” adding that E7 should also incentivize organizations to upgrade more employees to E5. This “raise price first, then upgrade, then bundle” playbook reflects defensive enterprise-market thinking—raising the base SKU price to absorb AI add-on fees into core subscriptions—at the cost of continuously testing enterprise IT buyers’ tolerance for Microsoft’s pricing.

MAI Models Launch Prematurely—Can In-House Development Catch Up?

Facing dual pressures—uncontrolled external model costs and lagging in-house capabilities—Microsoft responded belatedly on April 2, 2026. Mustafa Suleyman, CEO of Microsoft AI, unveiled three in-house foundational models: MAI-Transcribe-1 (speech-to-text), MAI-Voice-1 (text-to-speech), and MAI-Image-2 (image generation)—made available to developers via the Microsoft Foundry platform and MAI Playground.

Yahoo Finance reported Suleyman telling Bloomberg his goal is to build “state-of-the-art” multimodal models across text, audio, and image modalities. Suleyman, who leads the MAI “Superintelligence” team, stepped down from day-to-day Copilot product responsibilities in March 2026, handing leadership to former Snap executive Jacob Andreou as Copilot EVP—freeing Suleyman to focus exclusively on cutting-edge model development.

The timeline itself tells the story. Microsoft’s 2019 partnership agreement with OpenAI contractually restricted Microsoft from developing broadly capable in-house models—a restriction only lifted during renegotiation in October 2025. In other words, Microsoft has only been contractually permitted to develop frontier models for about six months. The MAI Superintelligence team was formed in November 2025; its first models shipped less than six months later.

MAI-1-preview was trained on 15,000 NVIDIA H100 GPUs, optimized for instruction following and everyday queries. Yet Microsoft still relies on GPT-5.4 as Copilot’s primary large language model; its target for launching a truly frontier-grade general-purpose model remains 2027. Meanwhile, the Microsoft Foundry agreement maintains Azure API access to OpenAI models through 2032.

World Today News noted Microsoft just posted its worst quarterly performance since the 2008 financial crisis—and investors remain skeptical of its hundreds-of-billions-dollar AI infrastructure investments. Suleyman’s Superintelligence team now faces immense pressure to prove those investments yield proprietary intellectual property—not merely turn Microsoft into an expensive OpenAI distributor.

Structural Issues: Dependence, Defense, and Deceleration

Laying these three negative narratives side-by-side reveals the structural flaws in Microsoft’s AI strategy.

First, excessive dependence on OpenAI. For years, Microsoft’s AI architecture treated OpenAI models as its sole frontier layer—while in-house development was contractually locked down. When OpenAI’s token prices rose and inference costs climbed, Microsoft lacked both the ability to substitute its own models and the pricing flexibility to pass costs on. Customers buy the “Copilot experience”—not itemized token bills. The abrupt cancellation of Claude Code represents a concentrated eruption: when external model costs spun out of control, Microsoft’s instinctive response was to push engineers back to its own GitHub Copilot CLI—even if its capabilities are “slightly inferior.”

Second, a defensive mindset in the enterprise market. The $99/user/month E7 package and $18–$30/user/month Copilot add-on fee reflect Microsoft’s attempt to force-feed AI into the Office ecosystem via lock-in effects. But this approach is failing against Gemini Workspace’s “free bundling” strategy: paid subscription share eroded seven percentage points in half a year—a metric far more direct than any analyst projection.

Third, simultaneous failures in security and cost control. Copilot’s DLP bypass vulnerability and zero-click CVE expose the structural mismatch between rapid integration, deep data access, and lagging governance capability. Meanwhile, the Claude Code budget breach reveals Microsoft’s internal gaps in forecasting AI usage volumes and managing token-cost economics. Against Gartner’s forecast that over 40% of enterprises will face AI-related security or compliance incidents by 2030, the “AI leader” label is becoming increasingly difficult to sustain.

Microsoft remains one of the world’s highest-valued AI players—holding 27% equity in OpenAI and commanding distribution networks for 4 million paid GitHub Copilot subscriptions and 15 million M365 Copilot seats. Yet the shift from “leader” to “chaser” is already written in the data from the past three months. Whether MAI can deliver a true frontier-grade general-purpose model by 2027 will determine how Microsoft’s AI narrative unfolds in its next chapter.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News