Recapping the U.S. Stock Market Version of “The Son”: In this podcast episode from two months ago, we thoroughly unpacked Leopold Aschenbrenner’s portfolio logic.

TechFlow Selected TechFlow Selected

Recapping the U.S. Stock Market Version of “The Son”: In this podcast episode from two months ago, we thoroughly unpacked Leopold Aschenbrenner’s portfolio logic.

Forget NVIDIA—why bet on Bloom Energy? What’s his reasoning?

Compiled & Translated by TechFlow

Hosts: Josh Kale; Ejaaz Ahamadeen

Podcast Source: Limitless Podcast

Original Title: Forget NVIDIA | This 24-Year-Old’s $4.5B Bet on AI’s Real Problem (Leopold Aschenbrenner)

Air Date: March 4, 2026

Key Takeaways

Everyone is talking about Leopold Aschenbrenner—24 years old, a $5.5 billion AI hedge fund, the “son of the U.S. stock market.” Yet most discussions stop at “He’s amazing” or “He made a ton of money,” with few actually dissecting his portfolio logic.

Two months ago, Limitless Podcast released an episode analyzing his 13F filing line-by-line:

Why he liquidated all NVIDIA shares, why he allocated 20% of his portfolio to a fuel-cell company, why he accumulated numerous Bitcoin mining firms, and why he shorted Infosys. At the time, this episode generated almost no discussion. Looking back now, nearly all its key judgments have materialized—making it well worth revisiting.

Highlights of Key Insights

Leopold Aschenbrenner’s Investment Performance

- “Last year he managed $1 billion… Today, just one year later, that $1 billion has grown to $5.5 billion.”

- “His fund launched at the end of 2024 with an initial size of $255 million. Within just six months, its performance outpaced the S&P 500 by 8x.”

- “In a 165-page article titled Situational Awareness, he essentially predicted we’ll reach Artificial General Intelligence (AGI) by 2027.”

A Paradigm Shift: From Chips to Infrastructure

- “He sold off NVIDIA, Broadcom, TSMC, and Micron—core AI infrastructure companies.”

- “By late 2025 or early 2026, he believes the market has fully priced in GPU value.”

- “He has shifted focus to the primary bottleneck investors have yet to appreciate adequately: energy and infrastructure.”

- “The existing grid was designed for humans—not for today’s massive AI demand.” This is where his current investments are concentrated.

Core Holding: Bloom Energy

- “Bloom Energy is his largest single position, representing 20% of his entire portfolio… He built a massive stake in the company—$855 million.”

- “Bloom Energy develops solid oxide fuel cells—a technology that converts natural gas directly into electricity usable by data centers. It’s modular and rapidly deployable.”

- “Their backlog stands at $20 billion. Revenue grew ~34% in 2025, and they project another 40% growth in 2026.”

- “If you use products like Bloom Energy’s natural-gas turbines, you don’t need to rely on the grid at all—you simply install them adjacent to your AI data center.”

Infrastructure and the ‘Shortcut’ via Bitcoin Mining

- “Leopold made a major investment in CoreWeave—the largest leveraged bet he’s placed in core GPU infrastructure and energy supply.”

- “He invested heavily in Bitcoin mining companies… because these firms possess two critical elements needed to build AI infrastructure: land and power.”

- “He acquired these companies to obtain their permits and grid interconnection rights—processes that normally take months or even years.”

- “It’s akin to taking over a bar that already holds a liquor license, rather than applying for a new one and waiting years—an exceptionally smart ‘shortcut.’”

Short Thesis & The End of IT Outsourcing

- “He holds a short position in a specific company: Infosys… whose business model relies entirely on providing labor cheaper than Western nations.”

- “He realized these models are now powerful enough not only to automate simple tasks but also to handle critical IT processes—prompting him to initiate a large-scale short.”

Investment Philosophy: A Return to the Physical World

- “Purely software-dependent companies will face severe challenges going forward.” His pivot isn’t merely architectural—it’s a direct investment in the physical world: manufacturing, factories, energy, and infrastructure.

- “These are domains AI cannot build—hardware and infrastructure requiring human labor, permits, and legislation.”

- “Energy is the only resource everyone lacks sufficient access to… Everything revolves around one central idea: powering the future.”

The Young Investment Prodigy: Leopold Aschenbrenner

Josh Kale:

There’s a guy named Leopold Aschenbrenner—he’s 24 years old. Last year, we covered him on this show when he was 23, managing $1 billion focused on emerging frontier AI concepts and technologies. Today—just one year later—that $1 billion has ballooned to $5.5 billion.

This guy, significantly younger than both of us, has just delivered a generational performance—earning more from AI than any other fund in the world. More importantly, AI is the hottest market right now, meaning competition is fierce. Clearly, this guy named Leopold is doing something radically different.

Last week, his latest quarterly 13F filing was released—and finally, we can peek into his recent trading activity. So next, we’ll closely examine these documents to understand exactly what he did to grow his assets under management from $1 billion to $5.5 billion.

Insights from the 13F Filing

Ejaaz Ahamadeen:

He accomplished all this within 12 months. His fund launched at the end of 2024 with $255 million. Within just six months, it outperformed the S&P 500 by 8x, reaching $2 billion. Since our last episode covering his Q3 fund report, it’s grown another $1.5 billion. He’s clearly in the midst of a generational breakout.

He’s extremely young—and he executed a substantial strategic shift. Yet everything aligns with his so-called “bible”: a 165-page article titled Situational Awareness. In it, he essentially predicts we’ll achieve AGI by 2027. In this sweeping piece, he lays out his vision for how the AI revolution will unfold. His predictions have proven remarkably accurate—he foresaw the GPU infrastructure boom, and now he’s signaling another pivotal shift—one we’ll explore in depth shortly.

The Shift: From Chips to Infrastructure

Josh Kale:

I believe the entire investment thesis is shifting—from chips to infrastructure. What we see on screen right now is fascinating. He used Claude to generate a document tracing every change between last year and this year. Perhaps we should start with what he sold—because those positions were massive, including NVIDIA, where he sold $300 million worth of put options in a single quarter.

Ejaaz Ahamadeen:

You’ll notice he sold many stocks that are highly popular—and widely held by investors today. So the question arises: Why did he sell $1 billion worth of these stocks? He sold NVIDIA, Broadcom, TSMC, and Micron—all core AI infrastructure companies.

His NVIDIA sale was profitable—he held $300 million in put options, meaning he likely profited as NVIDIA’s stock declined over recent months. So again—why do this?

In his 165-page paper, he states that by late 2025 or early 2026, he believes the market will have fully priced in GPU value—value derived primarily from companies like NVIDIA and Broadcom, which manufacture these chips and stack them for AI labs like OpenAI and Anthropic to train models.

Now, he’s pivoting attention to the primary bottleneck investors haven’t yet fully appreciated: energy and infrastructure. Today, many AI labs face two main problems: first, they have too many GPUs; second, the existing grid was designed for humans—not for today’s massive AI demand. This is precisely where his current investments are focused.

Selling NVIDIA Puts

Josh Kale:

Seeing him sell NVIDIA puts and fully exit NVIDIA was fascinating. Because when I talk with friends—or with ordinary Wall Street professionals—NVIDIA is the company everyone discusses; it’s the biggest investment. Seeing him walk away from NVIDIA proves once again that he’s always ahead of the curve—anticipating trends before they emerge, not chasing yesterday’s winners. For him, the future lies in infrastructure—a shift from chips to infrastructure-based plays.

This may be where we should dive deeper into his new investments—these are the stocks you should watch. These are his current holdings, the ones he believes will grow. If his thesis is correct, we should see substantial returns. So what new positions did he add this quarter?

Ejaaz Ahamadeen:

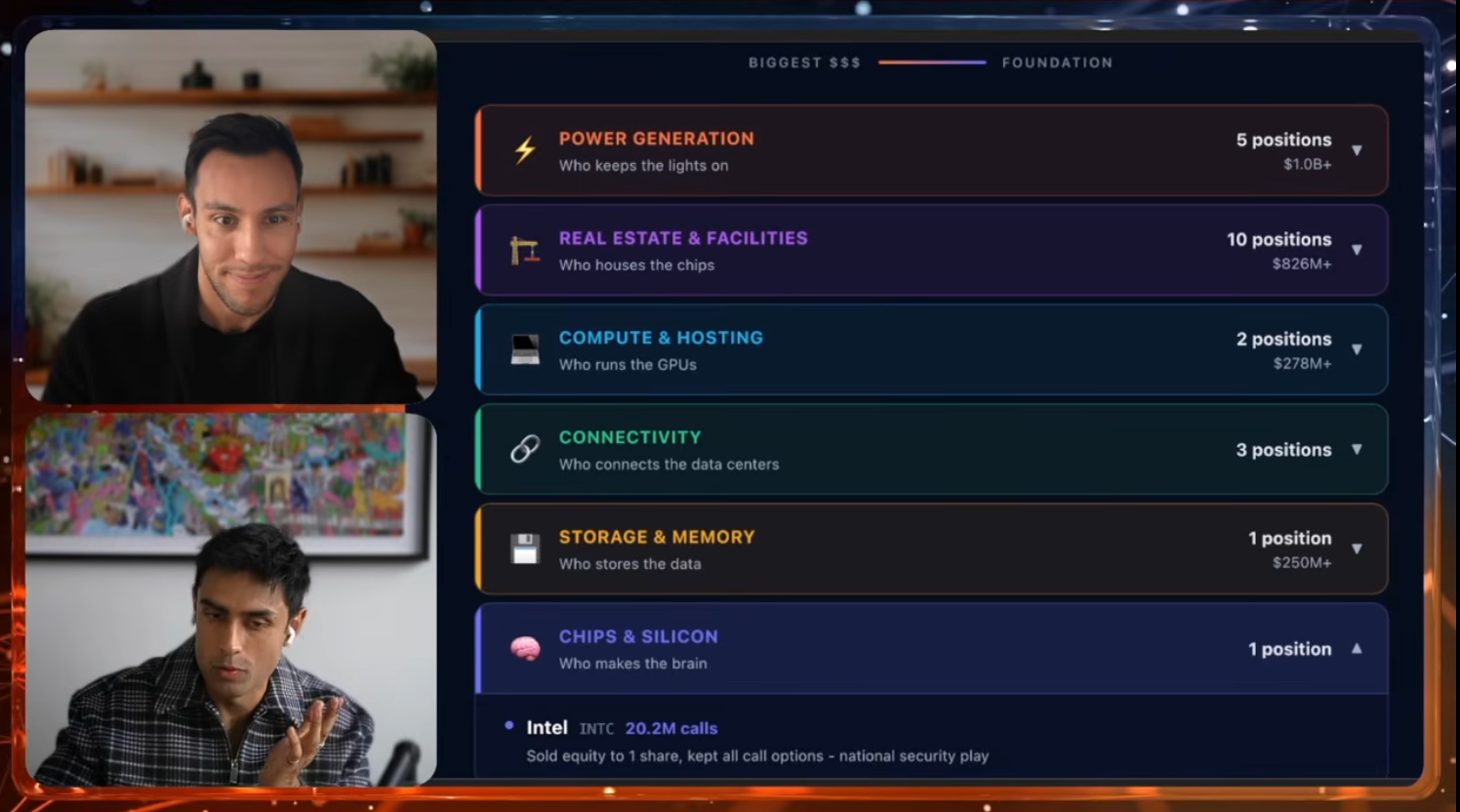

Here’s a clean portfolio chart categorizing Leopold Aschenbrenner’s investments across the AI tech stack. You’ll see categories like power generation, real estate & facilities, compute & hosting, connectivity, storage & memory, chips & silicon, and others.

In fact, let me add something to what I just said—I noticed a clever trade he executed in Intel. He sold his shares but retained a massive long position. Through this move, he freed up liquidity to allocate capital elsewhere. And the primary recipient of that capital? A company in the power generation space: Bloom Energy. This firm was virtually unknown three months ago—but it specializes in building turbine generators specifically for powering AI data centers.

He built a massive position in the company—$855 million. Though this chart shows $876 million, the filing states $855 million.

Bloom Energy: An Energy Innovator

Josh Kale:

Bloom Energy is his largest single holding—20% of his entire portfolio. This is completely unrelated to chips; it’s an entirely different direction. I researched their business—and it truly is fascinating.

Bloom Energy develops solid oxide fuel cells—a cutting-edge technology for on-site power generation from natural gas. Typically, when natural gas reaches data centers, it must pass through turbines for heating and cooling—a clunky energy production process. Bloom Energy’s “fuel boxes” convert natural gas directly into electricity usable by data centers. They’re modular, rapidly deployable, and—so far—face no supply shortages. To my knowledge, they plan to produce 2 gigawatts of power this year.

This is a fascinating energy play. I’ve been searching for the “NVIDIA of energy”—the “chipmaker of energy.” I haven’t found a perfect match yet—but Bloom Energy might just become it.

Ejaaz Ahamadeen:

I also reviewed their latest earnings—they’re a public company. Their backlog stands at $20 billion. Revenue grew ~34% in 2025, and they forecast another 40% growth in 2026—clearly, demand vastly outstrips supply.

You mentioned solid oxide fuel cells. Their natural-gas turbines are especially attractive because they eliminate dependence on the existing grid. As I noted earlier, the grid is under immense strain—humans need power, and AI data centers need power—driving up electricity prices in regions housing AI data centers. With Bloom Energy’s natural-gas turbines, you don’t need the grid at all. Just install them beside your AI data center—and power your GPUs and data center efficiently for training or inference.

Companies like Broadcom and CoreWeave will need this energy—especially hyperscale cloud providers and AI labs. It reminds me of the game Civilization—have you played it? It’s like moving infrastructure and energy-generation facilities into your own small settlement to accelerate its growth. What’s happening here is strikingly similar.

Josh Kale:

Clearly, energy scarcity isn’t the issue—the issue is who can produce the most energy. They do have a massive backlog—but can they manufacture enough units to fulfill it? Manufacturing capacity has become a critical bottleneck. In many such investments, we’re entering the “atomic” world—where manufacturing truly matters. I’d love to dig deeper later to assess whether they can scale production meaningfully. But for now, this is undeniably a critical investment—accounting for 20% of his portfolio. So what other notable positions appear in his new portfolio?

Ejaaz Ahamadeen:

He also added ~$300 million in CoreWeave exposure. Imagine being an AI lab needing GPUs. Purchasing GPUs from NVIDIA is only part of the job. Deploying them into rack servers, supplying power, providing engineering support, maintaining GPU servers and cooling systems—that’s a whole other challenge. You can outsource this to a “new cloud provider”—that’s CoreWeave, which specializes in exactly this.

Broadcom offers somewhat similar services, but CoreWeave is a smaller firm—originally focused on GPU gaming infrastructure, now pivoted exclusively to AI. Leopold made a major investment in CoreWeave. In our prior Q3 discussion, he’d already invested $500 million—and now he’s added another $300 million. His total CoreWeave exposure may now approach $800 million—but there’s more: he also holds ~10% of Core Scientific—the primary supplier building CoreWeave’s energy grids.

If you consider his betting strategy, Leopold’s largest leveraged bets are in core GPU infrastructure (e.g., CoreWeave’s new cloud services) and energy supply (e.g., Bloom Energy)—his two dominant positions in the current fund.

Bitcoin Mining

Josh Kale:

What’s interesting is he’s acquired enough shares in these companies to become an activist investor—capable of actively influencing corporate decisions. That’s fascinating. While reviewing his portfolio, beyond power generation—which is obvious—I noticed his largest new position category is real estate-related: he added roughly 10 real estate-linked positions, tied to Bitcoin mining.

What we’re seeing now is heavy investment in Bitcoin mining companies. This seems odd—and perhaps counterintuitive. After all, crypto markets are struggling, and Bitcoin hasn’t performed well. Why buy Bitcoin miners? Because these firms hold two critical ingredients needed to build AI infrastructure: land and power.

What does Bitcoin mining require? Massive energy and ample space for GPU racks. While Bitcoin mining hasn’t fully collapsed, these firms’ real estate and power assets clearly offer superior risk-adjusted returns. It appears he’s betting these miners will either sell their land-use rights and permits—or pivot directly into AI data centers.

Ejaaz Ahamadeen:

To clarify: His interest in these companies isn’t about mining—he’s acquiring them to secure their permits and grid interconnection rights. Obtaining such permits typically takes months—or even years. That’s why companies like Meta, Microsoft, and OpenAI announced $1.4 trillion in compute partnerships—but those deals haven’t yet translated into shipped models. One reason GPU supply lags behind new generations is that firms can’t secure permits quickly enough.

Leopold bypasses the entire permitting process by acquiring smaller firms that already hold permits. He strips away their crypto operations entirely and repurposes them solely for AI model training—becoming infrastructure providers for AI labs. It’s like taking over a bar that already holds a liquor license, instead of applying for a new one and waiting years—a brilliantly smart “shortcut.”

AGI and Market Trends

Josh Kale:

One of the things I admire most about his investment philosophy—and how it’s been validated over the past year—is its simplicity and efficiency. For instance, Bitcoin mining firms clearly hold permits and energy—and every AI company needs those resources. So why isn’t everyone buying these firms? I think it’s precisely because the idea is so simple—many investors are blocked from acting on it. Yet time and again, his simple ideas prove correct.

Will his 2027 AGI prediction also prove correct? Will we really achieve AGI by 2027?

Ejaaz Ahamadeen:

To test this, we opened a prediction market on Polymarket asking whether OpenAI will announce AGI before 2027. Currently, the probability stands at 13%. So yes—it still looks distant. His investment thesis may be sound, but the timeline could be slightly off.

That probability is indeed low. Still, I must note: he faced criticism for this paper initially—many dismissed his view as bizarre and unrealistic. Roughly 50% believed AGI would arrive within months; others projected 2030. Leopold stands alone in predicting 2027—and currently, he’s the closest to accuracy.

He foresaw GPU importance before the GPU boom erupted. Now, he’s forecasting the energy infrastructure boom before it begins. So I believe he remains ahead of the curve.

Yet his portfolio isn’t all long positions—he holds a short position in a specific company: Infosys, an India-based IT outsourcing firm. Its business model depends entirely on delivering labor cheaper than Western nations (e.g., the U.S. or Europe). In simple terms: “Outsource all your administrative IT work to us—we’ll handle it.”

I believe his bet here reflects observed trends. He saw the rise of tools like Claude Code and GPT Codex 5.3—and realized these models are now powerful enough not only to automate simple tasks but also to handle critical IT processes—prompting his large-scale short.

I think this is one of his more insightful investments—and most aligned with visible trends—demonstrating real conviction with real capital.

Bull Case vs. Bear Case

Josh Kale:

Let’s discuss the bull case and bear case. When stepping into a portfolio like this, what merits criticism—or caution? First, this investor is only 24. I’m unsure whether he possesses the experience many other investors have—though that may be an advantage, at some point, could that advantage collapse?

Another concern is that this fund’s thesis feels like a single-theme bet. If AI infrastructure and related spending slow—or if macro conditions shift—every position in this portfolio could face downward pressure. There’s very little hedging. So yes, the strategy carries inherent vulnerabilities—but for now, all signals suggest continued upward momentum.

Ejaaz Ahamadeen:

If you examine history’s most renowned investors, their success never rested on how much they earned in a single year or quarter—but on whether they could deliver consistent, compounding returns year after year, decade after decade. Leopold’s start is spectacular—his performance dwarfs industry averages for hedge funds, not just in AI but across the board. Yet he still needs to prove himself over longer time horizons. Time will tell.

I’ll just say this: This person—once fired by OpenAI—possesses profound insight into AI’s future trajectory and has made the boldest predictions. He’s the only one whose predictions have thus far proven accurate across the board. He poured immense effort into that 165-page paper—and backed his views with unwavering conviction. So far, that conviction is paying off.

Will things change? Possibly. But you can treat these filings and investments as his real-time tracking tool for bottlenecks in the AI race. Let me emphasize that. Initially, his fund’s thesis centered on GPUs—he believed GPU demand would surge, and the market underestimated that opportunity. Now, he sees that opportunity as fully priced—and the next bottleneck shifting to energy infrastructure.

Consider Elon Musk launching data centers into space. Why? Because the sun delivers more energy. Or Google, Meta, Broadcom, and NVIDIA—all investing in data centers or infrastructure to secure grid access. He’s simply directing capital toward where demand resides—I think that’s intelligent.

Josh Kale:

I recently read a brilliant Naval essay whose core idea is: purely software-dependent companies will struggle going forward—because developing and generating custom software has become trivial. I believe his shift isn’t just about architecture—it’s a direct investment in the physical world: manufacturing, factories, energy, and infrastructure. These are domains AI cannot construct—hardware and infrastructure requiring human labor, permits, and legislation. I believe this is precisely where the future lies.

Energy is the only resource everyone lacks sufficient access to. Whether power generation or real estate investment—everything orbits one central theme: powering the future. In the last earnings season alone, just Google, Amazon, and NVIDIA pledged $65 billion in capex—proof that massive capital will flow into solving this problem. His portfolio is clearly positioned to capture this upside.

Ejaaz Ahamadeen:

Yes, he’s made investments many might deem high-risk. For example, unless you’re deeply familiar with energy infrastructure, Bloom Energy may be entirely unfamiliar. Yet this firm qualifies as a Tier-1—or even top-tier—energy company, especially in portable energy. He connected the dots: the grid can’t meet current demand—so he invested. He committed with extraordinary conviction. We’re talking about allocating nearly one-fifth of his entire portfolio to a single stock.

This is an intensely concentrated, high-risk, high-conviction strategy. But if it succeeds—that’s why his portfolio delivered 4.5x–5x returns in just 18 months. We must commend him—growing $1 billion to $5.5 billion in one year is nothing short of astonishing.

The Future of Leopold’s Investments

Josh Kale:

Overall, his achievement is astounding—and his latest pivot—from hardware to infrastructure to energy—appears correctly timed and highly promising. If you agree with his portfolio, this may represent a compelling opportunity. Of course, this isn’t investment advice—just an overview of his holdings. But it certainly looks promising—and could perform exceptionally well this year.

Josh Kale:

I’m also curious what our listeners think. Do you believe our analysis meets professional standards—or even Leopold’s level? Or do you think we’ve missed something obvious?

Ejaaz Ahamadeen:

You know what I want? I want to know your favorite stock this year.

Josh Kale:

Yes—Leopold bet big on Bloom Energy. So what’s your Bloom Energy? What did we miss—and what could deliver another 5x return this year?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News