2026 Berkshire Hathaway Annual Meeting Highlights | Greg Abel’s First Public “Stress Test”

TechFlow Selected TechFlow Selected

2026 Berkshire Hathaway Annual Meeting Highlights | Greg Abel’s First Public “Stress Test”

Berkshire’s authority will no longer hinge on individual charisma but will instead be built upon a more diversified operational system.

On Saturday, May 2, 2026, Central Time in the U.S., the annual gathering of the investment world—the Berkshire Hathaway 2026 Annual Shareholders Meeting—took place in Omaha.

The meeting lasted approximately four and a half hours. New CEO Greg Abel addressed multiple hot topics, while 95-year-old Warren Buffett sat front-and-center to speak. CNBC also conducted an exclusive interview with Buffett.

This is the first shareholders meeting held since Buffett stepped “behind the scenes” after six decades at the helm of Berkshire—and marks the inaugural public “stress test” for Buffett’s successor, Greg Abel.

A highly symbolic adjustment this year was seating the heads of Berkshire’s subsidiaries on the main stage alongside Abel to answer questions. This move sends a clear signal:Berkshire’s authority will no longer hinge on individual charisma but will instead be anchored in a more diversified operational system.

WallStreetCN’s summary of key takeaways from the meeting follows:

1) Buffett on markets:

“This is not our ideal environment,” Buffett said, adding that people’s gambling enthusiasm has never been higher.

The most likely buying opportunity arises when nobody else is picking up the phone.

Things people discuss and worry about rarely happen; instead, unexpected black swans are what truly shake markets.

2) Buffett on succession:

“Abel has done everything I used to do—and even more—and he’s done it better in every respect. So we give this decision a perfect score of 100.”

3) Buffett on Apple:

Ten years ago, Berkshire spent $35 billion acquiring Apple shares. Including dividends, that stake is now worth $185 billion—and Buffett did nothing.

“Tim Cook stepping into Steve Jobs’ shoes created one of the miracles of American business management.”

4) Abel on AI:

“AI must deliver tangible benefits to our businesses. We won’t adopt AI for AI’s sake. We’ll deploy AI incrementally, focusing strictly on value creation.”

A deepfake video of Buffett shown during the meeting highlightedthe cybersecurity risks posed by AI.

Data center construction—and its surging demand on power grids—presents massive growth opportunities for utility companies.

Energy costs for data centers must be isolated from those of general grid users.

5) Abel on investing:

He reaffirmed Apple, American Express, Moody’s, and Coca-Cola as the “Core Four” pillars of Berkshire’s equity portfolio.

He emphasized “absolute collaboration” with Buffett on investments.

Berkshire’s investments in Japan’s five major trading houses are long-term and strategic; partnerships with firms like Mitsui O.S.K. Lines (MOL) are deepening.

Berkshire’s internal structure is lean and efficient, with cross-group capital allocation capabilities—no spin-offs or divestitures are planned.

6) Abel on his own “Charlie Munger”:

The Buffett-Munger partnership is “unreplicable.”

“I’m surrounded by outstanding people and have an excellent team of CEOs—I reach out to them and seek their counsel.”

7) Ajit Jain, Berkshire’s Vice Chairman of Insurance:

“Hormuz Strait coverage depends on price,” Jain stated, noting U.S. Navy escort is among the prerequisites for underwriting such risk.

AI is unlikely to soon achieve the sophistication needed to weigh trade-offs in pricing or claims adjudication—that remains many years away.

“If you expect AI to tell you which stocks to buy or sell, I don’t think that will happen.”

Earlier, Berkshire Hathaway released its Q1 earnings report, with highlights below:

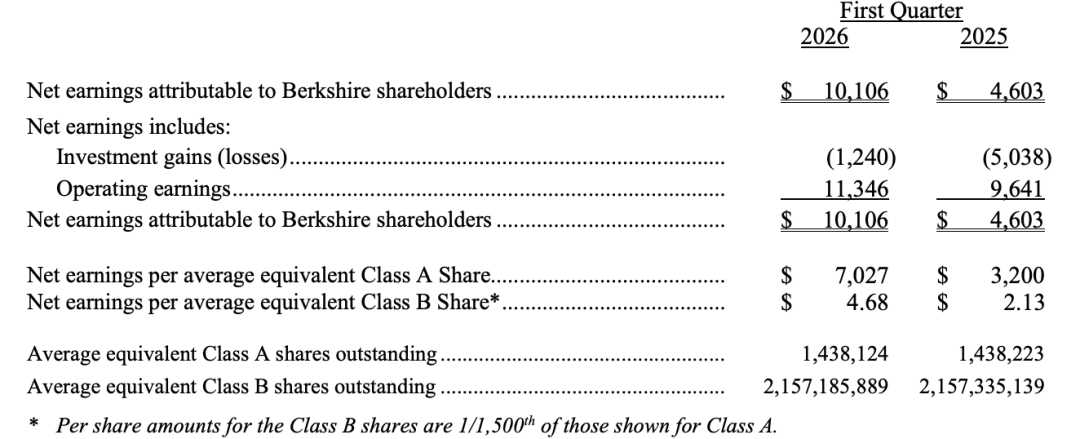

Berkshire Hathaway reported $11.346 billion in operating profit for Q1 2026, up 18% year-on-year. Insurance underwriting profit rose 28%, BNSF Railway’s profit grew 13%, and foreign exchange gains turned sharply positive.

Net investment losses narrowed from $5.038 billion a year earlier to $1.24 billion, driving GAAP net income up ~120% year-on-year.

Cash reserves stood at $397 billion in Q1—the highest in company history.

As of March 31, 61% of Berkshire Hathaway’s total equity portfolio fair value was concentrated in American Express, Apple, Bank of America, Chevron, and Coca-Cola.

Below is a chronological transcript of key moments from the 2026 Berkshire Hathaway Annual Meeting:

In the morning session,Abel co-moderated with Ajit Jain, Vice Chairman of Insurance. In the afternoon session,Abel co-moderated with Katie Farmer, CEO of Burlington Northern Santa Fe (BNSF), and Adam Johnson, CEO of NetJets.

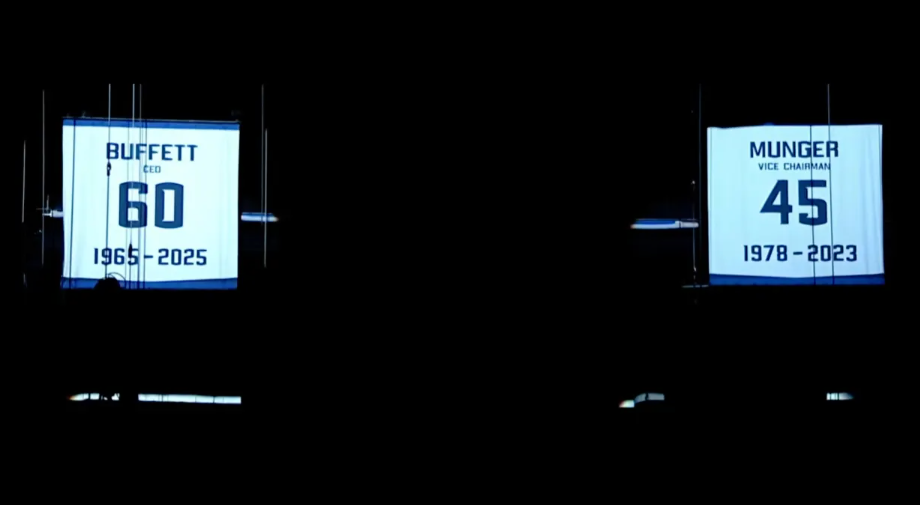

At the opening of the annual meeting, Abel formally retired a jersey bearing the number “60” in honor of Warren Buffett—permanently commemorating the “Oracle of Omaha’s” six-decade tenure at the conglomerate. Jersey retirement is a tradition in sports, regarded as the highest honor bestowed upon an athlete.

The jersey now hangs prominently from the rafters—alongside the retired jersey of the late investment legend Charlie Munger, who wore number “45” to mark his 45 years at the company.

“I’m pleased to announce these two jerseys will hang there forever,” Abel said.

21:20 Opening Remarks – 2025 Annual Meeting

Ninety-five-year-old Warren Buffett entered the front row of the boardroom, guided by staff, drawing enthusiastic applause from shareholders. For the first time in sixty years, Buffett was no longer the undisputed centerpiece of Berkshire’s annual meeting.

The meeting opened with a tribute video montage to Buffett, featuring archival photos and footage set to Huey Lewis and the News’ classic “Back in Time,” interspersed with highlights from past meetings.

Abel introduced key personnel alphabetically—when he reached Buffett, the crowd erupted in applause.

21:45 Buffett Praises Abel: “100% Successful” CEO Choice

Buffett took the microphone from his seat and again lavished praise on Abel. He noted today marked the anniversary of his original announcement naming Abel as his successor.

“This is the best decision we’ve ever made—100% successful. He’s done everything I did—and more. He is the right person.”

21:50 Buffett Praises Apple CEO Tim Cook

During his opening remarks, Buffett invited outgoing Apple CEO Tim Cook to stand—a gesture echoing Berkshire’s own leadership transition from Buffett to new CEO Greg Abel.

Buffett reflected on the immense pressure Cook faced succeeding Apple founder Steve Jobs—and how he exceeded expectations with outstanding results.

Buffett said:

Think about it: stepping into Steve’s shoes—and surpassing his achievements—requires extraordinary courage. It’s one of the miracles of American business history. Thank you, Tim. After Steve passed, we made an investment decision to commit nearly 10% of Berkshire’s resources to Apple—effectively placing that bet in Tim’s hands. And he turned it into a pre-tax return of roughly $185 billion.

Cook announced earlier this month he would step down as CEO, succeeded by Apple hardware chief John Ternus.

22:00 Abel Presents Earnings Report

Abel said the insurance market is “softening” amid intensifying competition. Auto insurance customers are engaging in unprecedented price comparisons.

22:20 CEO Rejects AI Hype, Upholds Buffett’s Investment Philosophy

On AI, Berkshire CEO Abel stated: “We won’t adopt AI for AI’s sake. We’ll only invest where we see real value. AI must deliver tangible, substantive benefits to our businesses. AI applications present opportunities across all our operations.”

Abel said Berkshire takes a cautious stance on AI deployment and governance—sharply contrasting with other CEOs rushing to rebrand or restructure around the technology.

“We’ll deploy AI in focused, value-driven ways. At the same time, we’re acutely aware of AI’s potential risks to humanity and remain highly vigilant.”

22:40 Abel: Data Center Build-Out to Drive Utility Growth

Abel said the large-scale construction of data centers—and the resulting strain on power grids—is creating substantial growth opportunities for utilities.

Citing Iowa’s expansion of hyperscale data centers, Abel noted current energy demand remains well below peak capacity:

Peak load from data centers—their actual electricity consumption—currently accounts for about 8% of total capacity. Industry players generally target 5%–10%, and we’ve already hit 8%. So we expect this ratio to grow another 50%—or more—over the next five years.

Abel stressed isolating data center energy costs from general grid users—and ensuring end-users bear full cost responsibility—was critical. “Hyperscale data center operators, data centers, and all electricity consumers must shoulder the full cost themselves.”

Amid the AI boom, data centers’ strain on regional power grids has drawn scrutiny from environmental and consumer advocacy groups.

22:50 Clayton Homes Hit by High Interest Rates

Abel said prefab homebuilder Clayton Homes faces headwinds as prospective buyers grapple with high mortgage rates and other pressures—clearly driven by current interest rate levels. Consumers face additional challenges.

Abel said the company’s goal is to provide “affordable housing” for U.S. consumers—a comment met with enthusiastic applause.

23:05 First Q&A Question Asked by Buffett: Why Hold Berkshire Long-Term?

Shareholders received an unexpectedly vivid lesson on AI risks during the Q&A. As it began, Abel played a video showing a familiar face.

On the big screen, a man in a suit resembling Buffett introduced himself and asked Abel: “Why should investors hold Berkshire stock long-term?”

Hello, I’m Warren from Omaha. Abel, I’ve followed this company for some time—quite a long time. My question is simple. I’m 95, and aside from time and Cherry Coke, I lack for nothing. I’d like to know—so I can tell my fellow shareholders—why they should hold Berkshire stock long-term.

Abel then revealed the truth: the video was not real—it was an AI-generated “deepfake.” He seized the moment to underscore cybersecurity risks to shareholders.

In answering the AI-Buffett’s question—“Why hold Berkshire long-term?”—Abel highlighted the company’s $397 billion cash hoard as a powerful asset granting Berkshire exceptional flexibility. “We hold cash and U.S. Treasuries for several purposes—we won’t let anyone dictate our actions.”

Abel reiterated Buffett’s enduring core investment and operating principles.

He told investors that holding cash in U.S. Treasuries, maintaining financial independence, flexibly allocating capital, prioritizing tax efficiency, and remaining vigilant against “ABC”—Arrogance, Bureaucracy, and Complacency—remain top priorities:

We’ve heard it countless times: Arrogance, Bureaucracy, and Complacency can quietly erode a company until it collapses. We will never allow that to happen at Berkshire.

He described Berkshire as a unique enterprise—capable of integrating vastly different businesses while deploying capital swiftly and flexibly:

Berkshire is a conglomerate—we recognize that. But we’re a different kind of conglomerate because we allocate capital extremely efficiently. We can shift funds from insurance to non-insurance businesses, invest in equities, or hold cash when appropriate.

Abel said the deepfake video starkly illustrated the AI-driven cybersecurity risks confronting Berkshire:

It’s a timely wake-up call for our team. This is a major, pervasive risk across Berkshire—one we confront daily. Berkshire will actively use technology to detect cyber threats, especially within insurance operations. Abel also clarified that this deepfake video was produced without any involvement or authorization from the “Oracle of Omaha” himself.

23:15 Real Q&A #1: Where Does Human Judgment Remain Berkshire’s Edge Amid AI Tools?

Ajit Jain, Vice Chairman of Insurance: AI is very much in vogue right now. People are rushing into it across both insurance and non-insurance domains. Clearly, if AI lives up to its hype, it will unquestionably be a game-changer.

Currently, we see AI used primarily as a productivity tool—to reduce labor costs and automate routine, repetitive tasks. I don’t believe AI can yet make decisions requiring trade-offs in pricing, claims, or similar areas. That will take many more years.

And I’m inclined to be skeptical. If someone tells me they’ve solved that problem, I’d be surprised. So if you’re counting on AI to tell you which stocks to buy or sell, I don’t think that will happen.

Jain said he’d recently discussed this with Abel, who immediately brought his team onto a call to highlight network risk—a topic they’d already covered.

They quickly moved on to how to improve coding efficiency and code management across insurance operations—a priority they’d flagged. Then, as you mentioned, how to become more efficient. They cited an excellent example:

For instance, if a traditional underwriter assesses risk, they might focus only on the top five largest exposures—your team pointed this out.

Now, we can rapidly identify those top exposures—but technology also lets us quickly spot other risks. We may now examine 15 additional exposures with strong judgment.

23:20 Q2: Balancing Patience and Action

Question: As a young investor navigating uncertainty and rapid technological change, I often struggle to balance patience and action. How do you personally distinguish between the two?

Answer: One of Berkshire’s greatest advantages is patience—and discipline in capital allocation. Over time, opportunities will arise. That doesn’t mean no opportunities exist today, nor does it mean you must deploy all your capital or spend all your money now.

This truly is our daily approach. We recognize the importance of our large cash and U.S. Treasury holdings—as exemplified by our own position. I view this cash as an asset—an enormous opportunity. You’ll feel the moment when an opportunity presents a compelling value proposition. When will we see these?

We’ve articulated our investment philosophy, and a crucial element is deep familiarity with what we invest in. We seek profound understanding—you mentioned technology and its rapid evolution. I always start there, and I know Berkshire has always done so: Do we understand this business? Do we understand this opportunity? More importantly, do we understand the risks?

Then, we aim for a crystal-clear view of its economic prospects over the next 5–10 years. Yes, next year matters—but we don’t invest for one year. A long-term perspective on opportunity is essential. We go further—we intend to hold these investments indefinitely.

So we think: We want a strong conviction about the management team—their capability and integrity. But above all, value must first justify deploying our capital. We won’t rush capital into suboptimal opportunities.

We ensure alignment with our principles—and then, as I said earlier, we act decisively and commit significant capital.

23:25 Q3: Balancing Oversight of Wholly Owned Subsidiaries vs. $288B Equity Portfolio

Question: Abel, your background as an operator differs from Warren’s as a public-market investor. Can you share how you balance your time overseeing wholly owned subsidiaries versus Berkshire’s $288 billion equity portfolio? And relative to Warren’s historical approach, will your operator’s lens alter how you evaluate new investment opportunities?

Abel shared fresh insights on how he views Berkshire’s massive equity portfolio, emphasizing a concentrated strategy anchored in a few core holdings.

He named Apple, American Express, Moody’s, and Coca-Cola the “Core Four,” viewing them as the bedrock of Berkshire’s equity investments. He also highlighted Berkshire’s large stakes in Japan’s five major trading houses as another pillar of the portfolio, underscoring Berkshire’s long-term holding commitment. Beyond these core positions,Abel specifically cited other key holdings including Bank of America, Chevron, and Alphabet. Berkshire purchased approximately $4 billion of Alphabet stock in Q3 2025.

Abel said he will play a more active role in portfolio management—timely adding to or adjusting positions.

He added that he is “fully collaborating” with Buffett on investment decisions.

Abel: I ran various businesses at Berkshire Energy for many years, then served as Vice Chairman of Non-Insurance Operations. Fortunately, Jain and I have held these excellent roles for the past eight—and now nine—years. This gave me a vital opportunity to deeply understand these businesses.

As I’ve noted, we have outstanding businesses and outstanding leadership—but opportunities remain. Still, it reminds me I’ll spend dedicated time on these businesses to ensure sound capital allocation, ongoing risk assessment, and encouragement of excellence in operations. Because, look: as an insider, it’s easy to rely on internal metrics to convince yourself you’re doing fine—you must look outward and ask: What do customers see and feel? What are competitors doing? I believe this is precisely the value we bring through operations.

I mentioned giving Adam Wright broader responsibilities—or having him take on more duties across 32 businesses. He brings exceptional operational knowledge, and we have the insurance team too.

Now, regarding the equity portfolio and time allocation: There remain huge opportunities in deploying capital on our balance sheet. I’ve shared the scale of our cash and U.S. Treasuries. Let me emphasize: If you examine our current equity portfolio—as outlined in my letter—we run a concentrated portfolio. We emphasize this by calling it “core,” but the clearest description is that it truly is a concentrated portfolio. We have what we call “core and concentrated” investments.

In my letter, I highlighted our Japanese investments. Interestingly, if you look at the next tier of companies where we hold significant stakes, I’d add that for these companies, we may still be buying shares or rationalizing positions appropriately. So the first group I emphasized stands just under $200 billion—and remains at that level. We now hold close to $100 billion—or $85 billion. Then adding other Berkshire investments like Bank of America, Chevron, Google, etc., plus another $7 billion, underscores how heavily concentrated our overall portfolio is in a limited set of holdings. Active management of these is actually quite limited—which is precisely what I want to stress.

We understand those businesses. We understand their management teams. These are things Warren and I still absolutely collaborate on and discuss. You don’t need to discuss them daily—but if something arises in these businesses, we’ll discuss it that week or month—perhaps about their direction or lessons learned. Japanese companies just reported earnings within the past 48 hours, making this an active discussion topic. Yesterday morning, Warren and I discussed their results and what we’re seeing there. So these are core—but that doesn’t mean we set them aside or treat them as static holdings we merely monitor.

Ted manages another $20 billion—or slightly less—but his responsibilities extend far beyond that. He clearly helps us across other opportunities—or assists in evaluating risks or capital allocation within our businesses. So we’re fortunate to have these resources—but considering the management required, this is a highly manageable portfolio.

As we’ve noted, deploying this cash and U.S. Treasuries at the right time is a massive opportunity—including equities, operational businesses, and insurance.

Regarding time allocation: Yes, we’ll spend time on operations—and prioritize this, given the significant room for continued improvement and narrowing gaps in operational excellence. We see opportunities in our existing portfolio—either increasing stakes or adjusting sizes. Then we continuously assess other market opportunities—whether acquiring private or public companies outright. Similarly, we consider incremental opportunities where we could acquire partial stakes in companies. These are evaluated identically—as I said, assessing economic prospects—and closely tied to the prior answer.

Jain: I truly believe capital allocation and operations are two sides of the same coin. Warren said something years ago that I find deeply insightful: “A good capital allocator makes a good operating manager—and vice versa.”

Abel: When considering our operating companies, as I mentioned earlier, we have exceptionally deep talent. We have outstanding operators who understand their businesses, industries, and customers. Yes, do we still have room for improvement? Yes—it’s an ongoing process, and we’ll narrow those gaps. But we have outstanding teams here. Whether it’s Jain, myself, or Adam Wright, we spend time ensuring we’re satisfied with our capital allocation approach, understand the risks, and recognize those gaps.

23:35 Q4: Patience Has Opportunity Cost—How Should Long-Term Investors Think About Capital Allocation?

Question: When patience carries real opportunity cost, how should long-term investors think about capital allocation today? How can individuals balance patience and action—especially given Mr. Buffett’s decades-long track record setting the standard?

Abel: Again, our capital allocation approach and long-term orientation align closely with our owners and shareholders present here. They take a very long-term view on investing. We’re fortunate to have this unique owner base in our shareholder roster. And long-term, Berkshire will have major opportunities. This circles back to the patience and discipline in capital allocation. Do we know what will happen tomorrow—or in two or three years? But market dislocations will recur, enabling us to act. This is where our disciplined approach shines—knowing our investment philosophy around these activities.

It’s not that we don’t see outstanding companies today. We’d love to own many. I’ll be cautious. Long-term, we’d gladly hold those companies—excellent businesses with outstanding management teams, which we rigorously assess. I’d say, thinking globally, there aren’t dozens of such companies—but they exist. Yet relative to opportunity, economic prospects, and associated risk, we’re uninterested in acquiring them—even partially or fully—at those prices. That doesn’t mean such opportunities won’t arise in the future.

This is what we prepare for: First, maintaining discipline; second, recognizing core opportunities we value—or value at the right price. This truly circles back to discipline.

You asked how I personally balance patience and action. Again, this aligns with my role—and I’m fortunate to work with Warren, Jain, and others. We do this because we love and believe in Berkshire. Warren brings immense commitment to Berkshire, profound understanding, and passion. Based on this, he aimed to build something truly long-term—including the opportunities it might create. Personally—and I know we all share this—I bring the same passion and fully intend to continue exactly as before.

Jain: You know, insurance—like investing—is a patient game. It’s incredibly difficult to sit idle. When hiring, my go-to line is: “Your job is to say ‘no.’” You’ll be bombarded daily with deals—but your fundamental duty is to say “no.” I say, occasionally you’ll encounter a deal that hits you like a plank—it screams “money!”—then come find me, and we’ll decide together.

You know, jokingly, when everyone else is being hustled by brokers and flown to London, you sit there doing nothing—it’s genuinely hard. I believe the true test of success—in insurance, and certainly in investing—is the ability to say “no.”

23:40 Q5: Insuring Ships Through the Strait of Hormuz

When asked when and how Berkshire would insure ships transiting the war-torn Strait of Hormuz, Ajit Jain, Berkshire’s Vice Chairman of Insurance, delivered a crisp reply: “Simply put, it depends on price.” Laughter and applause erupted instantly.

Jain said Berkshire is participating in a program to insure vessels transiting the Strait of Hormuz—but no policies have been issued yet. The strait has been repeatedly closed or tightly controlled during the U.S.-Israel–Iran war. “We’ve participated on a small scale in a program to underwrite Hormuz Strait voyages—but no policies have been issued yet.”

Jain said U.S. Navy escort for transit vessels would be one condition for underwriting. “The plan is still being refined. But if we secure satisfactory terms—including conditions at the underwriting decision level and U.S. Navy escort guarantees—we’ve provided a price we deem acceptable. However, there’s been no substantive progress yet.”

23:45 Q6: Managing Warren Buffett’s Legacy Equity Portfolio

Question: How do you manage Warren Buffett’s legacy equity portfolio?

Abel: Regarding managing the existing portfolio—and its composition, as you noted, built by Warren—this is a group of companies Warren knows intimately. And I’m highly confident I understand these businesses and their economic prospects. So, when I articulated this in my letter, I truly wanted to convey: Yes, we’re highly satisfied with these companies, we understand them, yes, it’s a concentrated portfolio—but their businesses evolve, and risks may emerge. So we’ll continually assess it—but it’s a portfolio we’re deeply comfortable with.

Warren highlighted Tim Cook’s remarkable success at Apple. Warren and Tim recently discussed this, noting Warren invested in Apple not as a tech stock—but based on its products and how deeply consumers value them. It’s an extraordinary perspective—but one I believe many of us apply similarly.

Take power generation—I know a great deal: how to ensure generation, transmission, etc. But am I deeply curious about how iPhones are manufactured? I’m intrigued by where they’re made and the related risks and challenges. But I fully trust our team when discussing this broadly. We’ll scrutinize and ask: Do we understand its value—and why consumers value that product? That’s ultimately its consumer value.

I believe our unique opportunity—and our great fortune—is that Warren comes to the office daily. It’s fortunate we can discuss potential opportunities and bring diverse skill sets. But ultimately, we’ll quickly narrow the scope: What is this opportunity? Why is it valuable? Why will that company and product endure—for consumers, or users in any sector? Relatedly: Where are the risks? This is essentially Warren’s method—and mine.

Regarding our existing portfolio, we’ll always be clear on what we own. But in understanding opportunities and risks, we’re highly confident in our clarity—and satisfied with our position.

23:50 Q7: Succession Planning for Jain and Abel

When asked about succession plans for Jain and himself, Abel said the board treats such matters seriously: “They’ve developed plans and continue discussing them. So if Jain can’t perform his duties today—or I can’t—the board knows exactly what action to take.”

These succession plans are clearly critical topics. Jain joined Berkshire in 1986 and designed our insurance business, building an unparalleled franchise with exceptional culture and discipline.

When Warren announced the transition plan last year, the first step was convening our top five insurance managers to discuss business and culture. It was an extraordinary opportunity for me to deepen my insurance knowledge base. What I saw in that team was deep managerial and insurance expertise—and the same values and culture Jain emphasizes.

Maintaining a disciplined culture is challenging. In insurance, telling underwriters accustomed to active deal flow to “take a few months off” isn’t easy. But Jain has an outstanding team—and our board treats succession with great seriousness. We have a plan in place: if Jain or I cannot perform, the board knows exactly what to do.

Regarding culture and underwriting discipline, I follow simple rules. Very few people are involved in actual decisions—my top three have worked together for over 35 years. Compensation is fixed salary—not complex formulas that let individuals capture upside while Berkshire bears downside risk. We insulate them from market volatility so they can confidently do the right thing.

Over the years, I’ve seen all these compensation plans. I once told Warren: “Give me a compensation plan, and I’ll game it—and you won’t discover it for years.” Plus, employees lose and want to renegotiate; win and walk away with everything. It’s a massive challenge.

23:55 Q8: When Will Berkshire’s Utilities Phase Out Fossil Fuels?

Question: When will Berkshire’s utilities phase out fossil fuels, shift to renewable alternatives, and stop inflicting irreversible harm on the environment—and my generation’s future?

Abel: We operate these assets as stewards—serving our states and customers. First and foremost, we must absolutely comply with current laws—including federal law. Our team is committed to both compliance and doing things right. We have resource plans—and timelines for phasing out coal and gas units—largely driven by state policy. States determine how we operate and how long these assets run, because customers ultimately bear the costs and risks.

Look at our Iowa utility: ~93% of its energy comes from renewables—leading the nation—and at affordable costs. Yet we still operate coal plants, using them only to stabilize the system during peaks unless absolutely necessary.

The challenge is that hyperscale data centers place heavy strain on the system. If AI continues growing, carbon-based unit usage will increase—putting pressure on the system and entire industry.

01:20 Abel Returns to Stage for Afternoon Session

Greg Abel returned to the CHI Health Center stage in Omaha, Nebraska, to host the afternoon session of Berkshire Hathaway’s Annual Shareholders Meeting.

Joining Abel were BNSF Railway CEO Katie Farmer and NetJets CEO and Consumer Services & Retail President Adam Johnson.

01:25 Q9: How Geopolitics Affects Berkshire Subsidiaries

Question: How is the current Middle East geopolitical situation affecting Berkshire’s subsidiaries?

Abel: It impacts all our businesses in multiple ways. But what I’m most proud of is that we run these businesses with a long-term lens. When the phone rings, you know challenges arise—but that’s okay. We’ll explore, strive, and always find a way forward. Regarding the Iran war and Middle East conflict, I see our teams adopting this attitude again: “This is the reality we face. What’s the best solution for customers? How can we continue serving them as we always have?”

I mentioned LSBI Pipeline’s drag-reducing agents—they typically don’t sell much to the Middle East, but when they tackle this challenge, many things happen. This doesn’t mean our businesses haven’t been directly affected. Our chemical group’s input costs doubled in a short time. Over time, prices rise per our contracts, rebalancing the situation. In running our businesses, we simply roll up our sleeves and operate steadily over the long term.

BNSF CEO: Railroads are excellent barometers of industrial and consumer economic health, given our broad commodity exposure. We see several distinct impacts from the Middle East conflict. Supply chain disruptions created opportunities for some commodities—like aggregates and steel—whose demand is rising. Our largest business segment is intermodal—rising fuel prices make our intermodal service more competitive. But overall, if fuel prices stay high long-term, consumer demand suffers—and ripples across all our businesses.

Yes, we see some impact. Some major retailers say consumers now must choose what to buy. If high fuel prices persist, I truly believe this customer impact will ripple across our businesses.

NetJets CEO and Consumer Services & Retail President Adam Johnson said cost increases—including oil briefly hitting $100/barrel—have begun suppressing demand in certain areas:

On the consumer goods side and physical retail, this is indeed affecting some demand. Acknowledging these pressures, Johnson said his businesses are accustomed to navigating volatility and adapting when necessary. “We’re prepared for these situations and ready to adjust. But this is indeed impacting some retail and consumer goods businesses.”

01:35 Q10: Managing Berkshire’s Decentralized Model—How Does BNSF Stay Competitive?

Question: Berkshire’s model relies on decentralization—each manager operates their subsidiary as a CEO. Which operating units require more oversight? How are underperforming managers handled? BNSF’s profitability lags competitors—how will it maintain competitiveness against rivals and new technologies?

Abel: I emphasized decentralized operations, risk discipline, and capital allocation. We have outstanding leaders and enterprises—closest to their customers—who deliver excellent group-wide results when they think like owners.

But decentralization doesn’t mean abdicating accountability. Autonomy means embracing immense responsibility—and pride in doing things right. We hold high expectations—do they manage risk? Do they act as Chief Risk Officers? Are they skilled at allocating capital on hand? If we see underperformance or poor decisions, that’s when we intervene and discuss.

BNSF CEO: We fully recognize that driving efficient operations, maintaining a competitive cost structure, and narrowing the profitability gap with competitors remain critical.

Our top priority in 2025 is improving carload efficiency. Enhancing the carload network releases resources, creates capacity, and allows handling equal—or greater—freight volumes with fewer assets. In Q1, we handled more freight than Q1 last year—but used 260 fewer locomotives.

Second is our technology transformation. We’re attracting data scientists and operations research specialists—placing them alongside our operations staff in the Network Operations Center to develop digital twins and predictive ETAs for customers. Our Q1 fuel efficiency set a record.

Regarding truck competition: Among all railroads, we have the largest intermodal network. We used to run trains with five people; now most trains run with just two. But we also need permission to innovate—and regulatory support enabling railroads to compete with trucks.

NetJets CEO: I returned on June 1, 2015. I asked: “How many people truly understand both ends of our business?” NetJets is complex—we fly to thousands of airports across 150 countries. I didn’t like the answer—it was far too few.

We rebuilt culture from there. I recall preparing my first board meeting, talking about growth. Abel kindly pulled me aside: “Why don’t you ease Warren’s mind a bit and focus first on reducing debt?” That was a lesson I’ve kept close.

We spoke about safety and service. Warren acquired NetJets in 1998 after becoming a customer, saying: “I want safety. I want service.” We’ve stayed intensely focused on keeping everyone on that path. This is largely why we repaid debt, returned cash to Berkshire Hathaway, and became leaders in service.

01:50 Q11: Tariff Impact on Portfolio?

Question: Is Berkshire Hathaway seeking tariff relief or compensation programs for wholly owned operating businesses facing import-cost pressures? How significant is this impact across the portfolio?

Abel: Tariff impact across our portfolio mirrors the Middle East discussion. We experienced this in the government’s first term and learned lessons—so we’re better prepared. We’ll simply roll up our sleeves and manage it ourselves. We’ll find ways to keep serving customers—recovering tariffs via direct customer contracts or products we manufacture. Our team has handled this superbly. Many details remain unclear—we’re not actively pursuing these measures.

BNSF CEO: No compensation, but let me address tariff impact. Early in 2025, we saw some customers ship ahead of tariff implementation—boosting freight volume. Then volumes stabilized in H2 2025, and into 2026, our customers adapted and adjusted to tariffs. That said, this creates uncertainty. From a planning perspective, it’s extremely difficult for our customers—leaving some capital in manufacturing facilities on hold. It’s the uncertainty of tariffs—not the tariffs themselves—that’s the real impact we see with customers.

NetJets CEO: I’ll cite Berkshire Hathaway Automotive Company—its new-car sales this year are slightly down year-on-year, partly due to tariffs. The issue is tariffs change daily—just understanding this “bouncing ball” is itself a full-time job.

Across our 32 consumer, service, and retail companies, average founding age is 88 years. When I call those CEOs, they say: “We’ve dealt with tariffs for 100 years.” Think of the past 7–8 years’ CEOs—we’ve navigated global pandemic, 40-year-high inflation, and now this “bouncing ball” of tariffs. Businesses have handled these issues superbly—and I believe our future position is quite strong.

01:55 Q12: Japanese Investment Portfolio

Question: Berkshire’s investments in five Japanese trading houses are passive—good businesses bought at good prices, financed in yen. Your deal with Mitsui O.S.K. Lines (MOL) is fundamentally different: a ten-year joint M&A and reinsurance partnership. This is an operational integration depth Berkshire has never attempted internationally. What does this look like in practice? Does it signal a shift toward more active international partnerships under your leadership?

Abel: MOL has performed exceptionally well. I previously framed this as a strategic relationship—not a financial transaction. We like our 2.5% investment in MOL—it’s a long-term commitment. This mirrors our other five Japanese investments—we truly view them as permanent, as they transcend mere investment to reflect relationships we aim to build there. You’ll continue seeing this—detailed underwriting opportunities where we jointly participate in MOL’s risks and returns, effectively representing 2.5% of their books today. This remains part of the financial transaction—but also embodies tremendous trust.

The third point discussed is the partnership’s emphasis on various elements—and how this relationship evolves remains undefined. So we’ll let it develop organically. This partner shares our culture and values. Undoubtedly, it will be outstanding for many years to come. As for absolute acquisitions in insurance or other fields—that will evolve over time, clearly a topic for Jain and MOL’s executive team. If such opportunities arise, we’ll be delighted.

02:00 Q13: Will Berkshire Spin Off Businesses or Be Split Up?

Question: Are there any foreseeable future scenarios where Berkshire would spin off businesses or be split up? If so, what would trigger them?

In responding to this shareholder question, Abel stated he expects Berkshire Hathaway will neither split up nor spin off subsidiaries. He emphasized the absence of bureaucratic layers in Berkshire’s structure—and the conglomerate’s unique ability to flexibly allocate capital across business units. “We’re a conglomerate—but an efficient one. We have no layered management hierarchy.”

Abel said Berkshire is committed to long-term ownership of acquired companies—but may consider selling in certain circumstances. “We buy something to hold forever. When we acquire a utility, we tell regulators it’s a permanent holding. But it must be a viable relationship. If it breaks down, we’ll seek a better path.”

Abel said unresolved labor disputes or reputational risks could prompt Berkshire to divest a business.

Nonetheless, Abel concluded: “We do not contemplate spinning off subsidiaries or splitting the group.”

When considering this, in some cases we may not be the optimal owner of a business. If we can’t resolve labor issues—or face reputational risks we’re unwilling to expose Berkshire to—that business doesn’t belong in the Berkshire family. If a business is unsustainable—and no longer generating operating cash for shareholders—if others can run it more successfully, we must consider it.

We take our obligation to ensure proper capital allocation extremely seriously. We’ve already announced the sale of PacificCorp’s utility in Washington State. In Washington, the policies PacificCorp was expected to implement significantly impacted costs in our other states. Our other states bore costs imposed by another state—so we exited, finding an excellent buyer. When we buy something, we always approach it with “forever” in mind—but it must be a viable relationship. If it breaks down, we’ll find a better path.

Regarding the second part of the question: Absolutely no splitting. We’re a conglomerate—but an efficient one, with no layered management and no committees dictating how our businesses operate. Many conglomerates end up with layer upon layer of costs that add no value to the whole—but we won’t do that.

Our conglomerate structure operates without bureaucracy or bloated costs—allowing highly tax-efficient capital transfers across groups. We won’t spin off subsidiaries or split any group.

02:10 Q14: Safety First or Seizing More Investment Opportunities? Tech Stocks or Cash-Flow Companies?

Question: Compared to Warren, what’s the most important evolution in your personal framework for evaluating cash-flow certainty and margin of safety? Specifically, are you more inclined toward tech companies exhibiting similarly strong cash flows?

Abel: On how Warren views investment methodology—our margin-of-safety approach and how we handle it—we are absolutely aligned. This starts with our culture and values—and how we’ve approached everything over the years.

If I revisit energy opportunities, it quickly shifts to: Do we truly understand the associated risks? When we acquired NV Energy, three major risks immediately came to mind—prompting urgent discussion with Warren. Our immediate dialogue was: Economic merits fully understood—then straight to the biggest risks. One risk was rooftop solar disrupting the business. That risk surfaced 12–18 months later—and we managed it successfully. Our risk-thinking differs—we view them through Berkshire’s lens, looking ten years ahead: What will this business look like in ten years? If we can’t envision that, we won’t proceed. We must have a vision for the future—that’s central to our approach.

Now on tech companies: We’ll never say a specific industry is mandatory for us. If a tech company presents an opportunity we understand—with clear risks and reasonable valuation—its sector alone won’t disqualify it.

02:15 Q15: Who Is Abel’s “Charlie Munger”?

Question: Warren had Charlie’s partnership for most of his CEO tenure—naturally reducing investment decision error risk. Who will serve as Abel’s Charlie?

When asked who would be his “Charlie Munger,” new CEO Greg Abel declined to name any single individual—instead highlighting his entire surrounding team. “You surround yourself with outstanding people—and they’re already here.”

Abel named Adam Johnson—Berkshire’s Consumer Services & Retail President and NetJets CEO—as well as Ajit Jain, Vice Chairman of Insurance, and Katie Farmer, BNSF Railway CEO. All three executives appeared onstage with Abel on Saturday.

He said, “Within our CEO group, we’re extraordinarily fortunate to have outstanding people—and for any specific situation, I proactively reach out to any of them for counsel.”

Abel: We’re extraordinarily fortunate to still have Warren as our Chairman—enabling an outstanding transition. We have an exceptional board—and I can easily contact any member based on the situation. When answering Warren’s question in Omaha, I said we want Berkshire to endure. I want to lead Berkshire—and I’ll be a strong leader. But you surround yourself with outstanding people—and they’re already here.

In non-insurance operations, I’ve been fortunate to work with Adam’s 32 companies—and another 18. Clearly, I have an excellent working relationship with Jain—and am fortunate to regularly seek his advice. Then there are our CEOs—we’re fortunate to have such an outstanding group—and I’ll contact any of them for situation-specific counsel.

Fortunately, thanks to Berkshire—and how it was built—we have extraordinary resources at our disposal. Berkshire will endure—and endure as a team.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News