Artemis Deep Research Report: Anchored on Hyperliquid, $PURR Is the Only Crypto Treasury Stock with Genuine Bottom-Layer Profitability

TechFlow Selected TechFlow Selected

Artemis Deep Research Report: Anchored on Hyperliquid, $PURR Is the Only Crypto Treasury Stock with Genuine Bottom-Layer Profitability

PURR has no debt, no preferred shares, and no recurring expenses. Behind its 18.8 million HYPE tokens lies the only mainstream protocol generating positive returns in 2025.

Author: Zheng Jie

Translated and edited by TechFlow

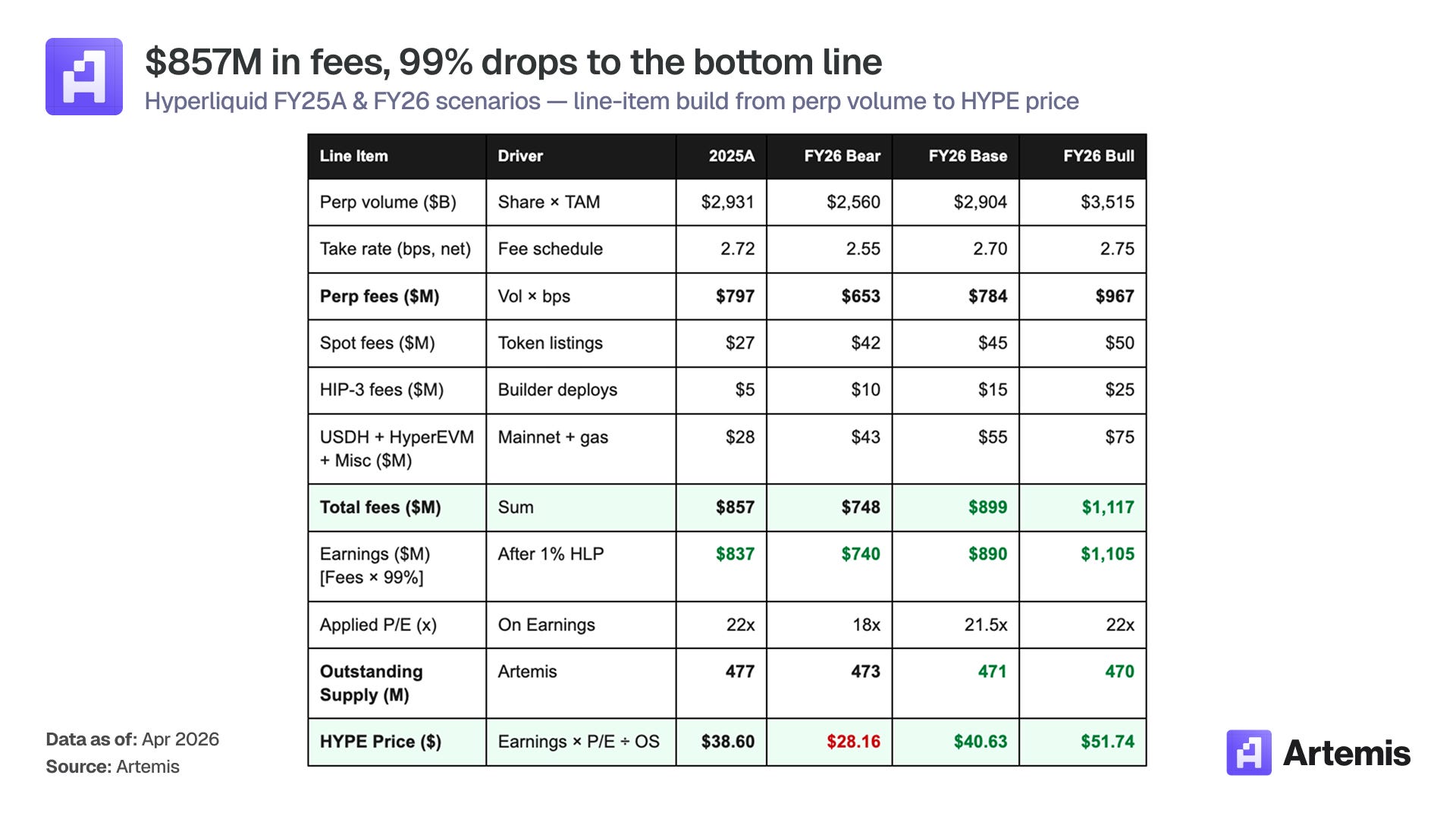

TechFlow Intro: Artemis is a leading data analytics firm in the crypto industry. This report is authored by Zheng Jie, an analyst at Artemis. Strategy’s (formerly MSTR) market NAV multiple has fallen from 6x to 1.15x; the Digital Asset Treasury (DAT) sector has collectively lost its allure—but the author argues PURR should not be lumped in with the rest. Strategy spends $2.3 million daily servicing debt; BMNR and Forward Industries are underwater on their ETH and SOL holdings; meanwhile, PURR holds HYPE—a token backed by an 11-person operation generating $857 million in annual revenue, with 99% of that revenue allocated toward buybacks and burns.

Conclusion

The market is pricing PURR using the same framework applied to another MSTR: issuing shares at a premium, buying more tokens, and increasing tokens per share. We believe this pricing is incorrect. Strategy spends $2.3 million daily to service interest payments—$835 million annually—on its senior preferred stock and convertible bonds secured against 780,897 bitcoins, while bitcoin itself generates zero cash flow. Its market NAV multiple has plummeted from over 6x at its peak to just 1.15x today.

PURR carries no debt, no preferred stock, and no recurring expenses. Its 18.8 million HYPE tokens represent exposure to the only major protocol generating positive earnings in 2025: $857 million in fee revenue ($797 million from perpetuals, charged at 2.72 basis points), 99% of which flows into the Assistance Fund, with $837 million allocated for buybacks and burns and near-zero operating costs.

Token structure is inherently deflationary: ~19 million tokens repurchased and burned annually, versus ~7 million tokens released from staking reserves. The stock currently trades at 1.12x market NAV.

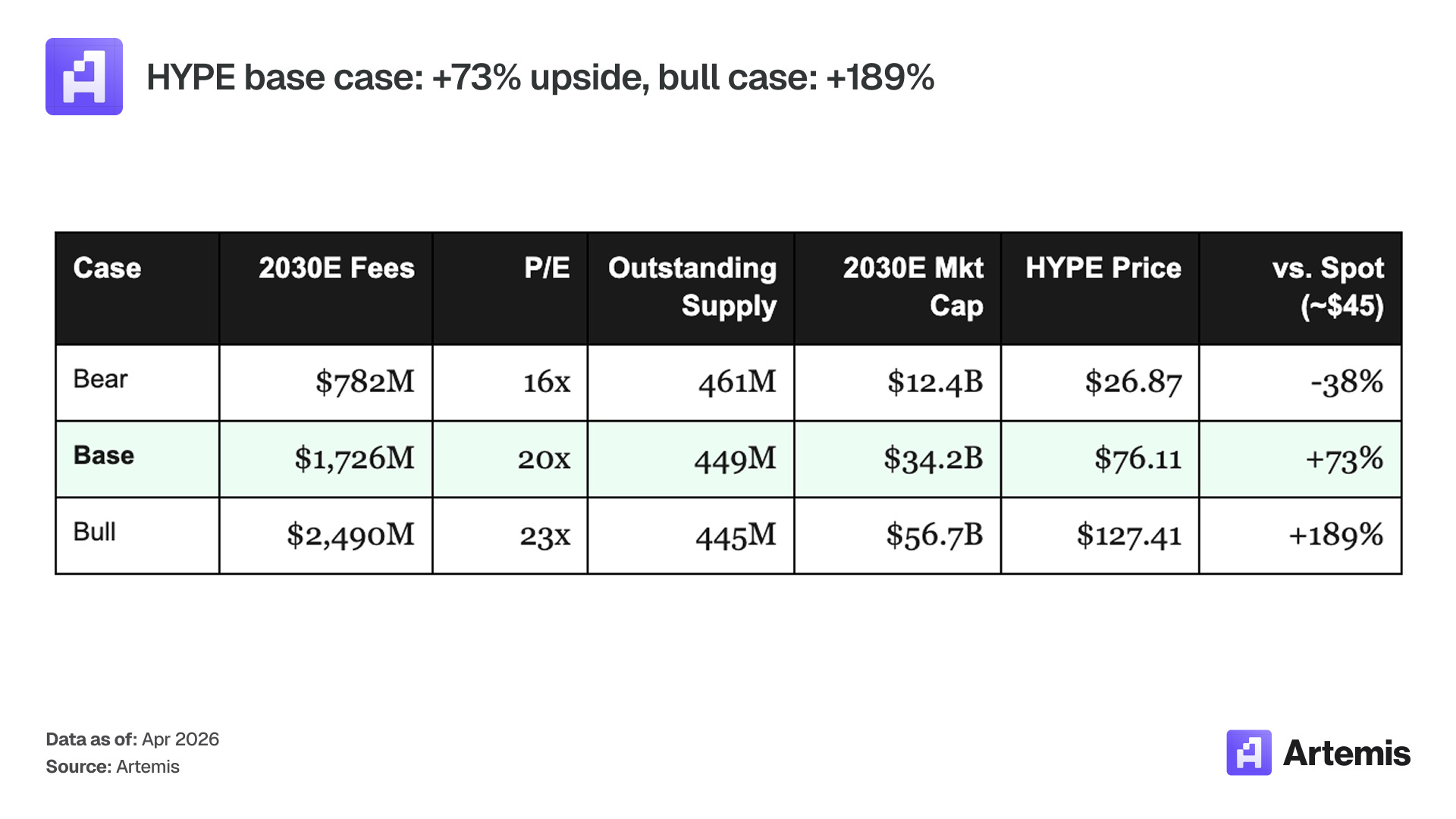

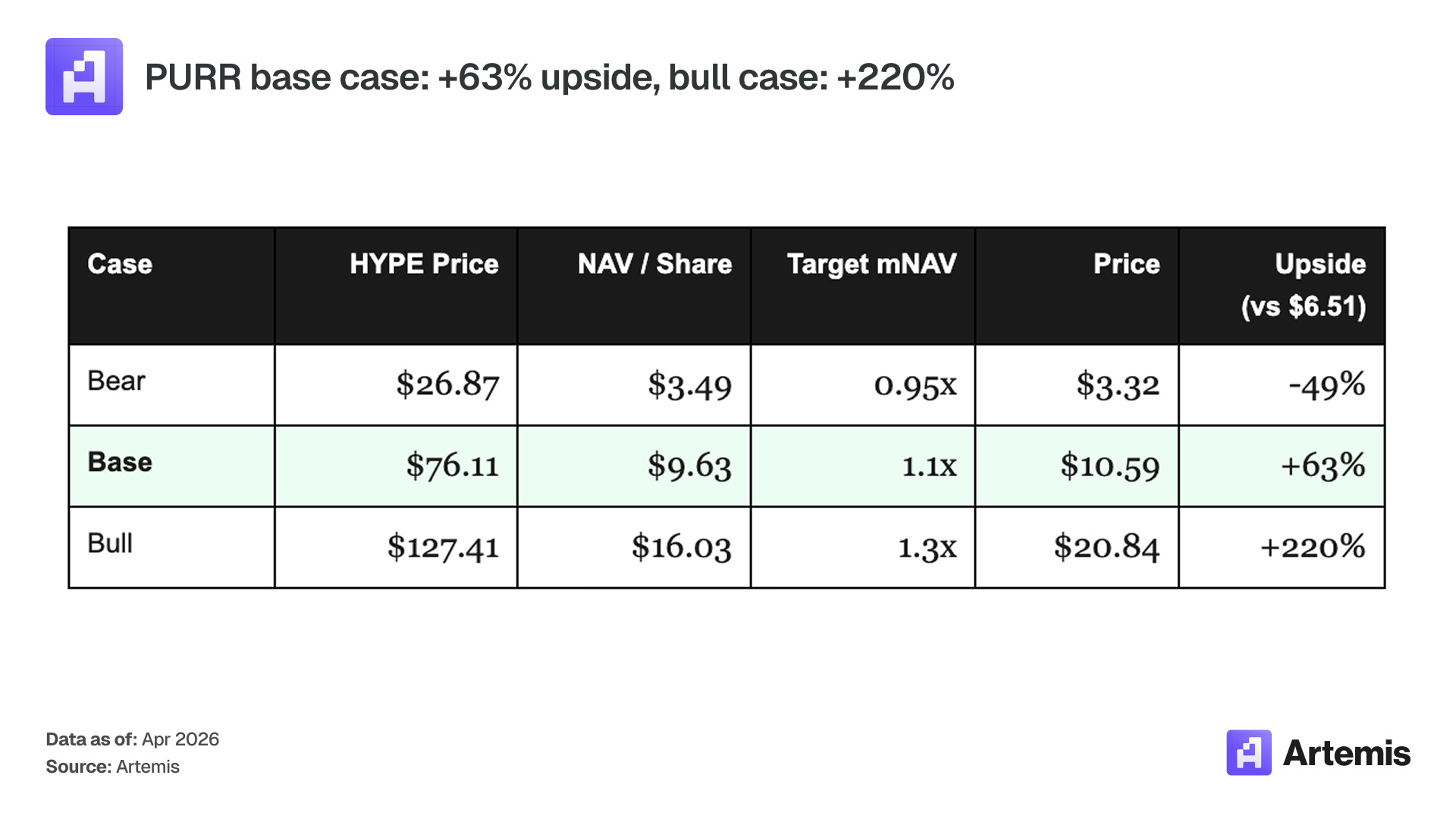

Our base case assumes HYPE reaches $76 by 2030, implying $1.71 billion in projected earnings and a 20x P/E ratio. PURR maintains a 1.1x market NAV, corresponding to a share price of $10.59 and ~63% upside over five years. In the optimistic scenario, HYPE reaches $127, with a 1.3x market NAV, yielding a share price of $20.84 (+220%). In the pessimistic scenario, HYPE falls to $27, the P/E compresses to 16x, and the market NAV slips to 0.95x, resulting in a -49% return.

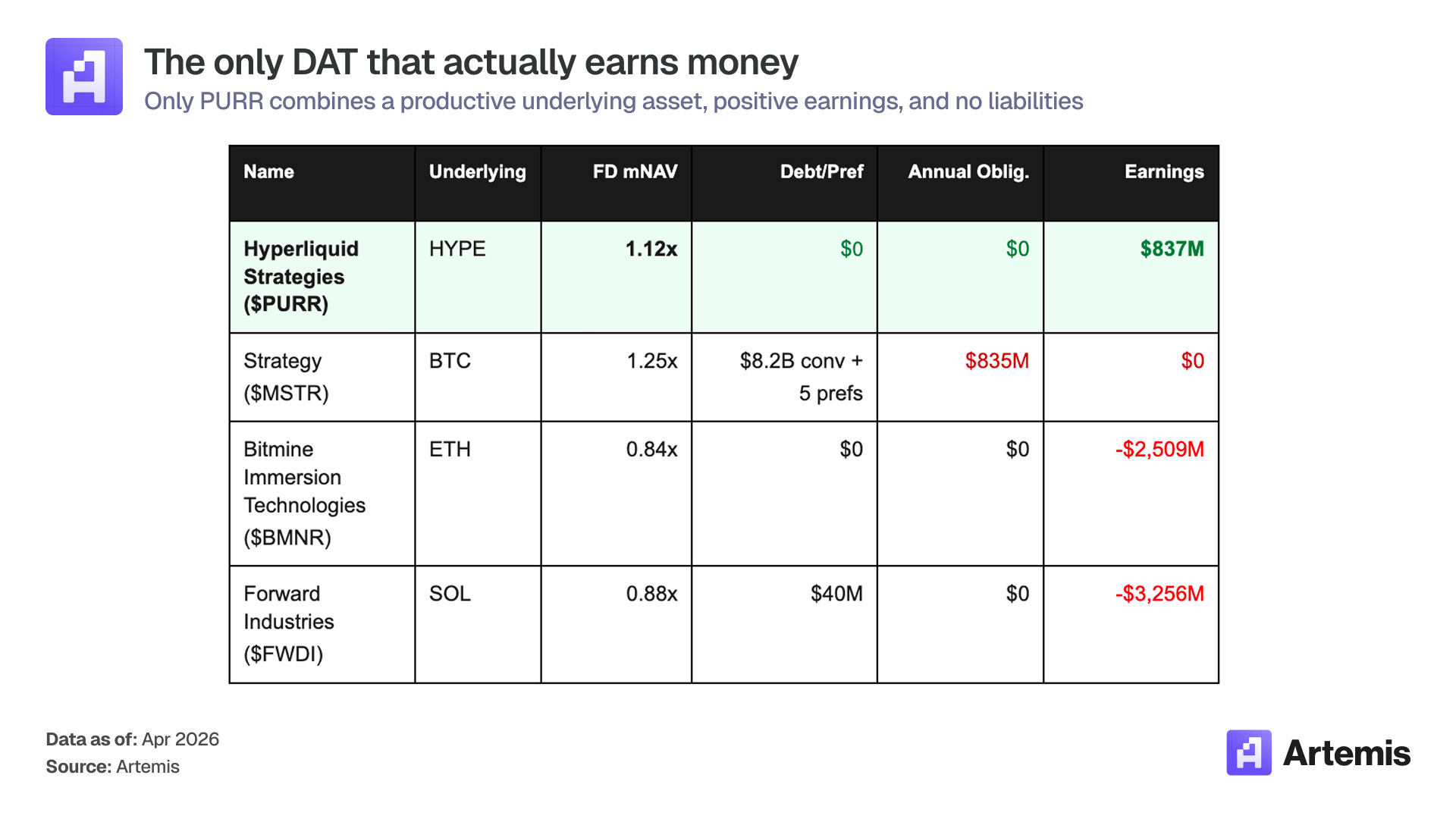

Comparison: PURR’s Unique Position Within the Crypto Treasury (DAT) Sector

Caption: Among all DAT companies, only PURR satisfies all three criteria: underlying assets generate cash flow, the entity reports accounting profits, and it carries zero liabilities.

What Is PURR?

Hyperliquid Strategies Inc. (Nasdaq: PURR) is a Digital Asset Treasury (DAT) company whose sole mission is to accumulate and hold HYPE—the native token of the Hyperliquid protocol. The company was formed in December 2025 through an $888 million merger involving Sonnet BioTherapeutics, Rorschach I LLC (a SPAC sponsored by Paradigm), and a newly established entity backed by Atlas Merchant Capital.

Its balance sheet is the cleanest across the entire DAT sector: 18.8 million HYPE tokens, $112.6 million in cash, and zero debt, zero preferred stock, and zero convertible bonds. In January 2026, the company authorized a $30 million share buyback program. As of February 3, 2026, $10.5 million had been deployed to repurchase ~3 million shares, reducing fully diluted shares outstanding to 150.8 million. An additional $1 billion equity line—separate from its cash balance—stands ready as contingency firepower should HYPE decline.

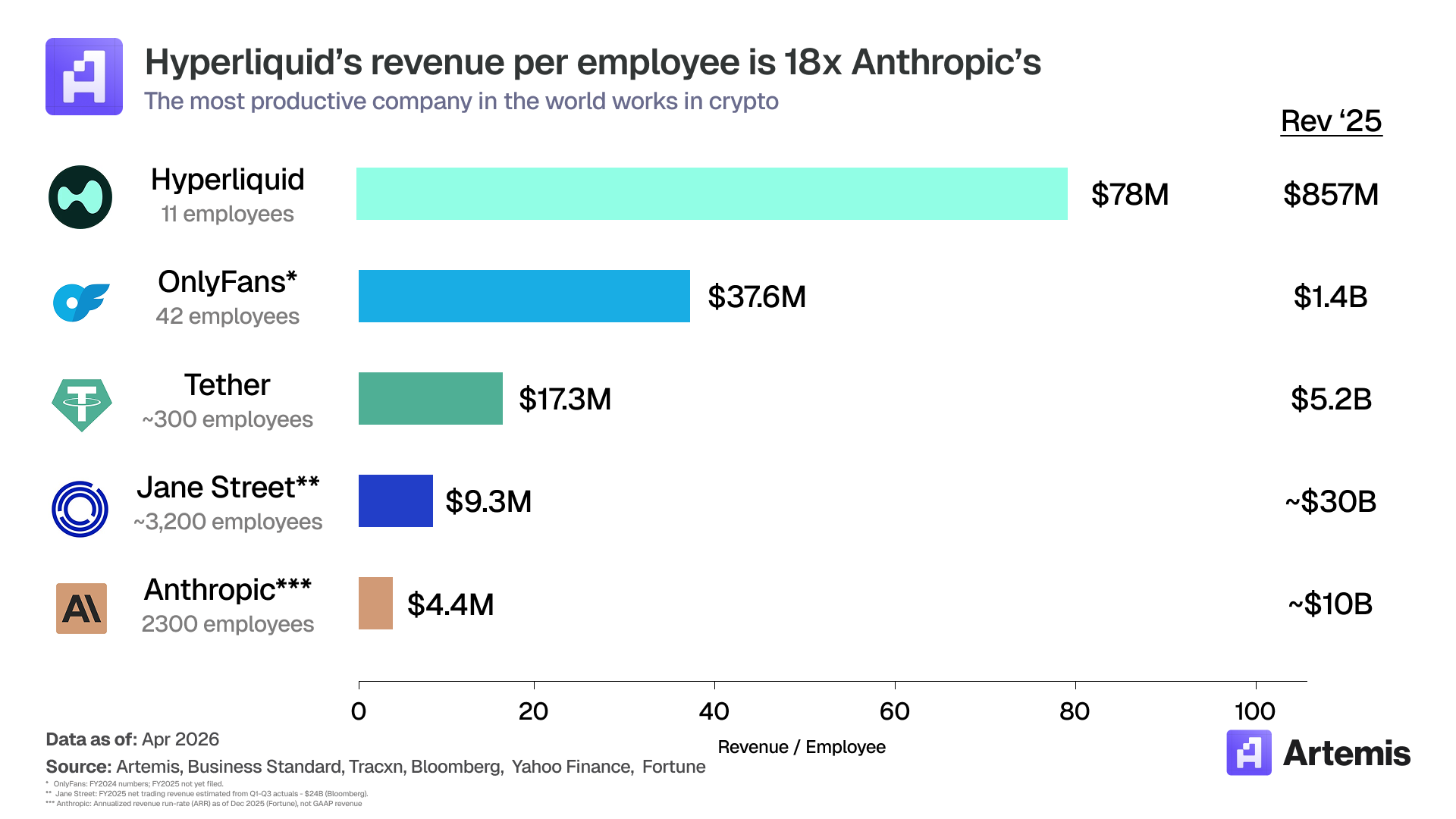

What truly differentiates this structure is the underlying asset. HYPE functions as an equity instrument for Hyperliquid—a perpetual futures exchange that generated $857 million in fees in 2025 with only 11 employees (annualized revenue per employee: ~$78 million—the highest among all global corporations).

Caption: Hyperliquid protocol fundamentals: $857 million in 2025 fees, with 99% flowing into the Assistance Fund for HYPE buybacks and burns.

The Fee Engine

Hyperliquid is an exchange.

Its business model is “trading volume × fee rate,” with marginal costs approaching zero.

Fee allocation is divided across six categories:

Caption: Hyperliquid fee waterfall: spot/perpetual fees, HLP treasury share, Assistance Fund buybacks, staking releases, etc.

Argument One: The Only Profitable Underlying Asset

Every DAT company listed on U.S. exchanges today holds assets that either generate no yield (e.g., BTC) or—in the case of PoS chains—lose money once issuance required to sustain chain operations is factored in. Ethereum generated $526 million in fees in 2025 but paid out $3.035 billion in staking rewards; Solana generated $680 million in fees but distributed $3.936 billion in staking rewards. Hyperliquid generated $857 million in fees.

We must clarify our definition of “earnings.” For Hyperliquid, earnings = fees net of the 1% HLP treasury share (3% prior to August 30, 2025), with 99% of that amount flowing into the Assistance Fund for buybacks and burns: $857 million in fees translates to $837 million in earnings. For Ethereum and Solana, the comparable metric is fees minus staking issuance, since these chains cannot operate without staking rewards—validators must be paid in tokens. This represents a real operational cost; both chains posted negative net cash flow at publication time. Hyperliquid’s $312 million in staking issuance originates from pre-allocated reserves—not exchange revenue—and thus falls outside this calculation. On an adjusted basis ($545 million), Hyperliquid is the only protocol with positive cash flow.

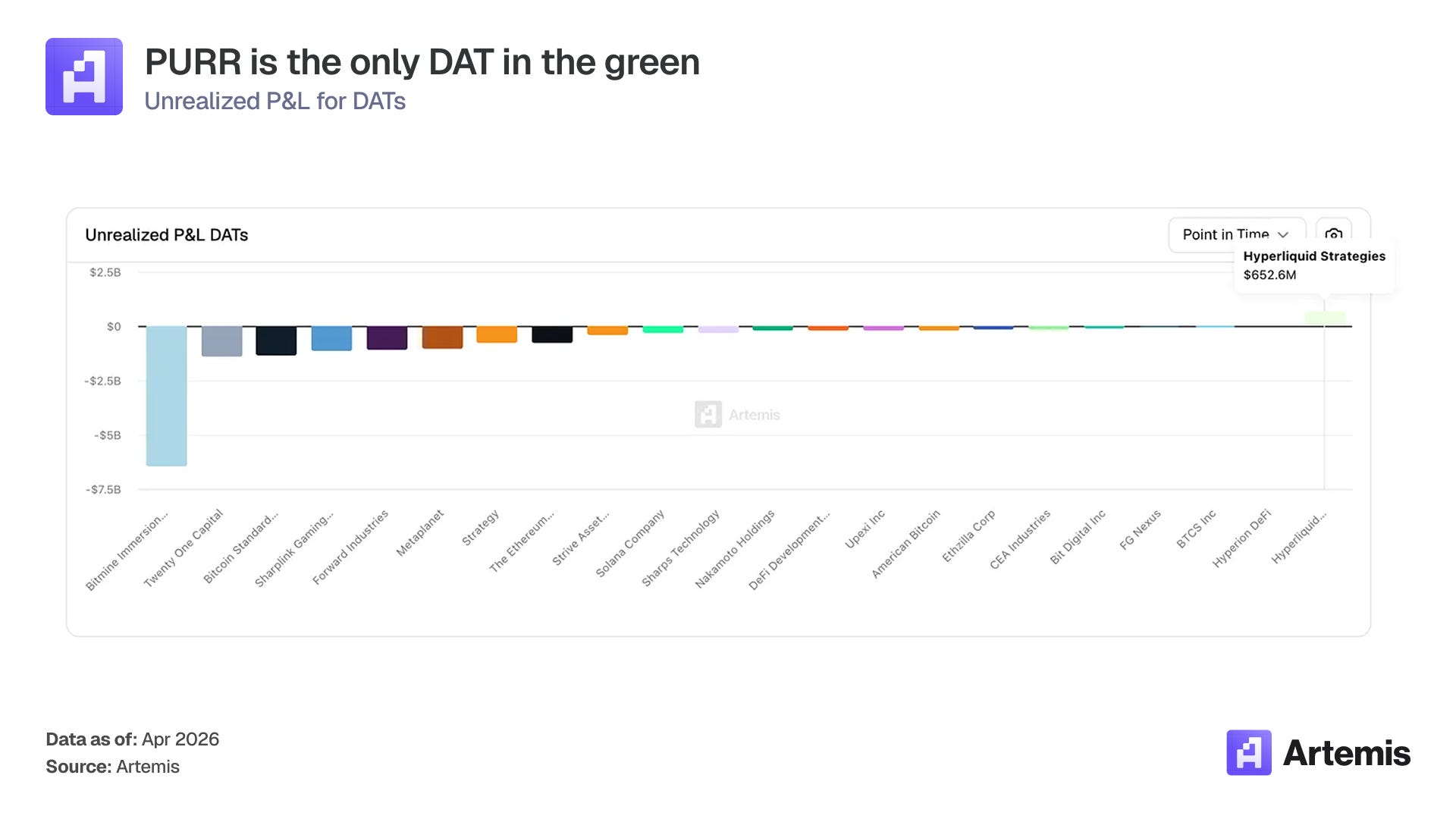

This divergence is directly reflected in DAT companies’ balance sheets. BMNR’s average ETH acquisition cost is $2,826; Forward Industries’ average SOL acquisition cost is $232. Both are currently underwater.

Caption: Unrealized gains/losses across DAT companies: Only PURR’s HYPE position shows substantial unrealized gains (~$600 million)

PURR is the only DAT company holding a material unrealized gain—its HYPE position is up ~$600 million. Not only does the underlying asset generate earnings—it is also appreciating in value.

Five growth drivers are compounding this advantage:

- HIP-3: Transforming Hyperliquid into a Listing Platform. Launched in October 2025, HIP-3 allows any developer to deploy permissionless perpetual contracts on any asset—including commodities, equities (China, Korea, Japan), FX, and alternative assets—by staking 500,000 HYPE. This transforms HL from a crypto-native trading venue into a universal listing layer. During the Strait of Hormuz crisis, TradeXYZ deployed a crude oil market on HIP-3 that processed $305 million in nominal volume over a single weekend; cross-asset weekend prices showed an R² of 0.785 relative to traditional markets’ reopening prices (calculated by Blockworks’ Shaunda). Total addressable market (TAM) expands from $3–5 trillion in crypto derivatives to >$100 trillion in global derivatives. Each HIP-3 deployment requires permanent staking of 500,000 HYPE—same for HIP-4. At scale, 20 markets would lock up ~10 million HYPE (2.1% of circulating supply).

- DAT as Developer Partner. At current prices, 500,000 HYPE is ~$23 million. Most builder teams lack capital to self-fund deployments. Large HYPE holders like PURR (18.8 million HYPE) are natural counterparties: providing funding or co-deploying HIP-3/HIP-4 markets in exchange for fee-sharing arrangements. This creates a revenue stream and ecosystem influence inaccessible to individual HYPE holders.

- HIP-4: Options and Event Markets. Testnet launched March 2026; mainnet targeted for Q4 2026. Deribit—the options exchange acquired by Coinbase—processed >$1.875 trillion in options notional volume in 2025, capturing >85% of the total market (~$2.2 trillion). Options currently account for only 3% of crypto derivatives (per Coinglass: $85.7 trillion total). If on-chain options achieve 15% penetration and HL captures half, that yields $165 billion in notional volume × ~8 bps (options spreads are wider than perpetuals; Deribit charges 12 bps) = $135 million in annual fees. Base-case model assumes $50 million in 2026, rising to $130 million by 2030. Prediction markets open a second revenue stream under HIP-4 (Polymarket’s annualized fees already approach $700 million).

Caption: Deribit options market data: >$1.875 trillion in 2025 options notional volume (Source: Deribit)

- Builder Codes: Negative-CAC Distribution Channel. ~40% of HL’s daily active users now access the platform via third-party frontends (Phantom is largest). Developers receive a share of fees on every trade routed through their frontend—cumulative payouts exceed $40 million (Dwellir data). Contrast with Coinbase’s $400–600 CAC per funded account; HL’s customer acquisition cost is negative. This explains why our model projects perpetual volumes growing from $2.9 trillion in 2025 to $5.2 trillion in 2030 (base case). Distribution is outsourced.

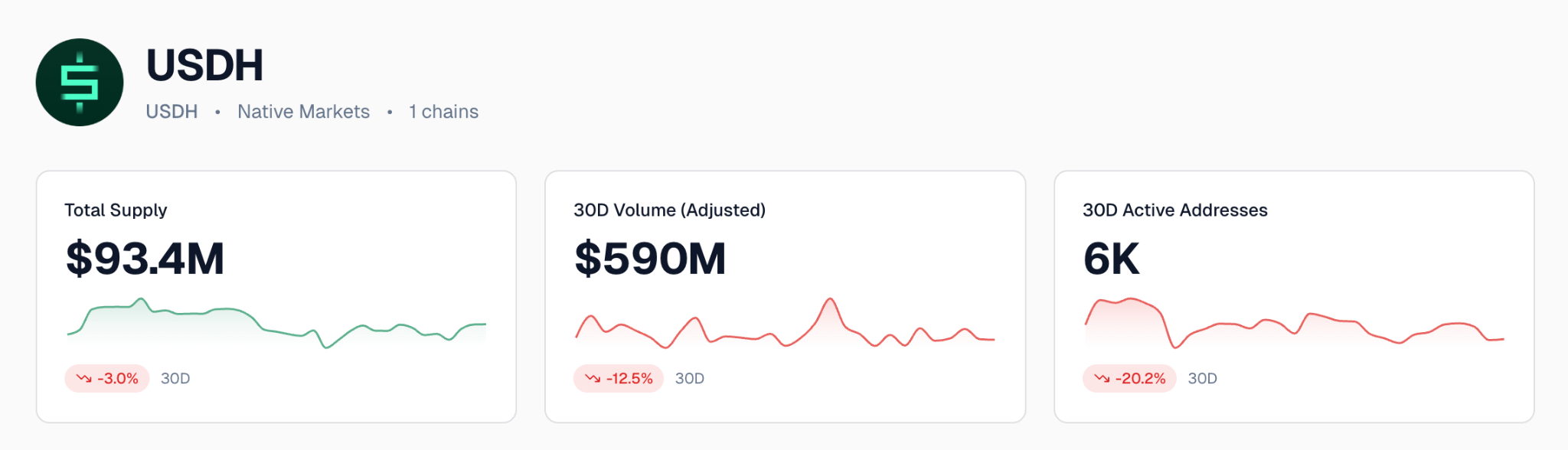

- USDH: Native Stablecoin with Fee Sharing. Native Markets secured USDH issuance rights in September 2025. Reserves are held in BlackRock-managed funds, with 50% of reserve yield flowing into the Assistance Fund.

At current supply (~$93 million) and a 3.7% U.S. Treasury yield, USDH contributes ~$1 million annually to the Assistance Fund for buybacks. At $2–5 billion supply, that rises to $40–100 million/year. With HIP-4 potentially requiring USDH for settlement, this is a powerful tailwind for Native Markets’ stablecoin.

Caption: Stablecoin supply comparison (Source: Artemis Stablecoin Dashboard)

All this expansion requires no headcount increase at Hyperliquid. Every growth vector—HIP-3 listings, HIP-4 options, Builder distribution, USDH float—is outsourced to external teams who bear listing and distribution risk in exchange for fee shares. The 11-person core team focuses solely on protocol development and fee infrastructure. This is a platform-scale model: throughput, listed assets, and frontends all grow—while headcount remains flat.

Argument Two: Buying This Shell at Cost

Strategy’s playbook is issuing shares at a premium, converting cash into BTC, and calling it financial engineering. The problem? Once the premium vanishes, the mechanism reverses—and the entire DAT sector sits precisely there today (Strategy down from 6x to 1.15x). PURR runs in the opposite direction: its stock trades near 1.12x NAV, and its $30 million buyback program activates only when the market prices PURR below the NAV of its token holdings. Every dollar spent buying back shares below NAV mechanically increases the number of HYPE tokens per share. This mechanism works bidirectionally: Below NAV, management buys back shares, increasing HYPE per remaining share. Above NAV, they can issue new shares at a premium to buy more HYPE—again increasing HYPE per share. Both directions accrue value to existing shareholders.

No other DAT company has this mechanism. Strategy, BMNR, and Forward Industries all issued shares to buy tokens—but none have initiated buybacks as premiums compressed. Shareholders get diluted on the way up and receive nothing on the way down.

Direct HYPE ownership offers several advantages: no corporate-level management fees, no dilution risk from equity lines, no regulatory risk specific to PURR’s management, and full exposure to token appreciation. Staking and airdrop rights are reserved exclusively for direct holders.

But PURR provides four things unavailable to direct HYPE holders:

- Automatic Appreciation Without Additional Risk: Buybacks are funded entirely from existing balance-sheet cash—no margin calls, no liquidation risk, and no action required by holders. Direct holders may use perpetuals or lending to leverage, but that introduces counterparty and liquidation exposure.

- Regulatory Moat: PURR and HYPD are currently the only two Nasdaq-listed instruments offering HYPE exposure. Any enforcement action targeting Hyperliquid’s KYC-free operations would likely redirect institutional demand toward this shell.

- No Obligations: No debt to repay, no forced selling, no preferred stock.

- Tax Efficiency: PURR is taxed as ordinary stock. Holders over one year qualify for long-term capital gains (federal max 20%), can hold within IRAs and 401(k)s for tax-deferred or tax-free growth, and can perform tax-loss harvesting against other equity positions. Direct HYPE holders pay ordinary income tax (max 37%) on each staking reward, lack tax-advantaged retirement accounts, and face unresolved IRS guidance on airdrop cost bases. For top-bracket U.S. investors, this shell roughly halves the tax drag.

The underlying exchange generates $1.76 in earnings per circulating HYPE token ($837 million ÷ 477 million circulating supply). This metric was jointly introduced by Artemis and Pantera Capital in August 2025.

Valuation & Scenarios

Valuation proceeds in two steps: first, fundamental valuation of HYPE (2030 projected earnings × terminal P/E ÷ circulating supply), then conversion of HYPE price to PURR’s per-share NAV using the target market NAV multiple.

HYPE Valuation Scenarios

HYPE is valued on earnings (fees × 99% after HLP deduction) multiplied by terminal P/E:

Caption: Three HYPE 2030 valuation scenarios: base case $76 (20x P/E), optimistic $127, pessimistic $27 (16x P/E)

PURR Valuation Scenarios

Translating HYPE scenarios to PURR uses this formula: Adjusted per-share NAV = (18.8 million HYPE × price + $112.6 million cash − $95.8 million deferred tax liability + $4.5 million adjustments) ÷ 150.8 million fully diluted shares, multiplied by the target fully diluted market NAV multiple. Historically, DAT stocks with productive underlying assets reprice their NAV multiples to 1.1–2.0x during bull cycles, with 1.0x being the sector norm.

Caption: Three PURR 2030 valuation scenarios: base case $10.59 (+63%), optimistic $20.84 (+220%), pessimistic $3.32 (−49%)

Base case: HYPE reaches $76 by 2030, adjusted per-share NAV = $9.63, valued at 1.1x NAV → $10.59/share, +63% over five years.

Optimistic case: HYPE reaches $127 by 2030, adjusted per-share NAV = $16.03, repriced to 1.3x → $20.84/share, +220%.

Pessimistic case: HYPE falls to $27, adjusted per-share NAV drops to $3.49, market NAV slips to 0.95x → $3.32/share, −49%. Base-case CAGR ≈ 10%, but returns are asymmetric: downside is cushioned by zero liabilities and a protocol still generating $782 million in fees; upside benefits from both HYPE appreciation and market NAV re-rating.

Management & Equity Structure

PURR is a balance-sheet-driven company. Its sole function is capital allocation: when to buy HYPE, when to repurchase shares, when to draw on the equity line, and when to do nothing. The team responsible for these decisions collectively brings over 80 years of experience in capital markets, bank balance-sheet management, and exchange infrastructure. Paradigm—the SPAC’s cornerstone investor—is the world’s largest crypto-native fund ($12.7 billion AUM). D1, Galaxy, and Pantera round out a shareholder roster bridging traditional finance and crypto. Bob Diamond’s institutional network serves as both a distribution channel and a conduit for asset allocators seeking HYPE exposure but unable or unwilling to custody tokens or navigate crypto tax complexity.

- Bob Diamond (Chairman): Former CEO of Barclays, Co-Founder of Atlas Merchant Capital

- David Schamis (CEO): Co-Founder of Atlas Merchant Capital, former Partner at JC Flowers

- Eric Rosengren (Director): Former President of the Federal Reserve Bank of Boston (2007–2021)

- Larry Leibowitz (Director): Former COO of NYSE, Operating Partner at Atlas Merchant Capital

Cornerstone investors include Paradigm, D1, Galaxy, and Pantera.

Risk Factors

1. HYPE Price Decline

PURR is a leveraged position on HYPE price. A crypto bear market would compress trading volume, fees, and buyback capacity. The pessimistic scenario models exactly this: TAM stagnates at $85 trillion, HL’s market share holds at 3%, fees slide to 2.3 bps, and P/E falls to 16x—yielding HYPE at $27 and PURR at $3.32 (−49%). Circulating supply is ~477 million; the pessimistic scenario assumes 35% team token vesting between 2026–2027.

Mitigation: Zero debt eliminates forced selling. Even in the pessimistic scenario, Hyperliquid still generates $782 million in fees and $774 million in earnings, ensuring buybacks continue to exceed staking issuance—keeping the token deflationary (net ~23 million tokens burned annually). The $1 billion equity line is optional—not mandatory.

2. Regulatory Enforcement Against Hyperliquid

Hyperliquid operates without KYC. The Futures Industry Association has formally petitioned U.S. regulators to enforce restrictions on U.S. residents accessing offshore perpetual contracts. Any adverse enforcement action would directly depress HYPE. HIP-3’s expansion into traditional financial assets (silver, crude oil, equities) increases regulatory exposure—commodity perpetuals could attract CFTC scrutiny beyond current crypto-specific enforcement.

Mitigation: PURR itself is a fully compliant Nasdaq-listed entity. Regulatory enforcement would most likely drive U.S. institutional demand toward PURR as the regulated, SEC-approved vehicle for economic exposure to HYPE.

3. Equity Line Dilution

The $1 billion equity line can be drawn if HYPE declines—but issuing shares at the wrong price dilutes existing shareholders. In the pessimistic scenario (HYPE at $27), PURR’s adjusted NAV is $3.49/share; issuing shares then implies pricing below $6.51/share.

Mitigation: This line is optional and fully at management’s discretion. Current posture favors buybacks over issuance. As of early February 2026, $10.5 million of the $30 million buyback program had been executed, repurchasing ~3 million shares and reducing fully diluted shares to 150.8 million. Paradigm-led governance provides no incentive to dilute its own stake.

4. DAT Premium Compression

Any premium above NAV built during rallies will rapidly compress upon sentiment reversal. Strategy’s 6x market NAV premium collapsed to 1.15x in under 12 months. The optimistic scenario sees PURR re-rate to 1.3x NAV ($20.84); if sentiment reverses and the multiple resets to 1.1x, the loss is capped at the difference in market NAV multiples.

Mitigation: PURR’s current market NAV is 1.12x. Relative to Strategy’s peak premium of >$5 per $1 of NAV, PURR’s premium is just $0.12. Upside asymmetry remains: 1.3x is a modest valuation in bull cycles—historically, DAT stocks with productive underlying assets have traded above 2.0x. At 1.0–1.1x, the shell’s value simply equals the underlying assets.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of advice. The views expressed herein are those of the author alone and should not be construed as recommendations to buy, sell, or hold any asset. The author or related entities may hold positions in the assets discussed herein. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News