21Shares Research Report: HYPE’s Price-to-Sales Ratio Is Only Half That of CME; Bullish Target Price Is $70

TechFlow Selected TechFlow Selected

21Shares Research Report: HYPE’s Price-to-Sales Ratio Is Only Half That of CME; Bullish Target Price Is $70

The market is valuing HYPE as a legitimate exchange business—not a speculative altcoin—at a multiple of 13–15x annualized revenue.

Author: 21Shares Research Team

Translation & Editing: TechFlow

TechFlow Insight: The 21Shares Research Team has released an in-depth report on Hyperliquid, arguing that Hyperliquid has evolved from a crypto derivatives DEX into a fully-fledged, 24/7 multi-asset exchange. During the February Iranian airstrikes, CME halted trading, yet Hyperliquid priced WTI crude oil perpetual contracts nearly 48 hours earlier. Traditional assets now account for 35% of trading volume; its revenue approaches CME’s, while its valuation multiple is only half that of CME. This report outlines bull and bear case valuations—well worth a careful read.

On February 28, U.S.-Israeli coalition forces launched airstrikes against Iran, plunging traditional markets into darkness. The Chicago Mercantile Exchange (CME) suspended operations, and legacy infrastructure failed to respond. Hyperliquid did not pause. This blockchain-based derivatives exchange operates 24/7, pricing WTI crude oil perpetuals in real time—reaching $111.53—while traditional-market traders could only watch helplessly.

This episode highlights Hyperliquid’s emerging role as a critical trading venue and index during geopolitical turmoil—providing real-time price discovery during weekend gaps. When traditional markets reopened on March 2, WTI surged above $110, and the price gap between Hyperliquid and CME had fully closed. Hyperliquid didn’t merely react faster—it effectively completed shock pricing nearly 48 hours ahead of traditional systems.

That narrative alone is compelling. What transforms it into an investment thesis is what followed. Fast-forward two months: WTI still trades ~$500 million daily on Hyperliquid, remaining among the top five most-traded assets on the platform.

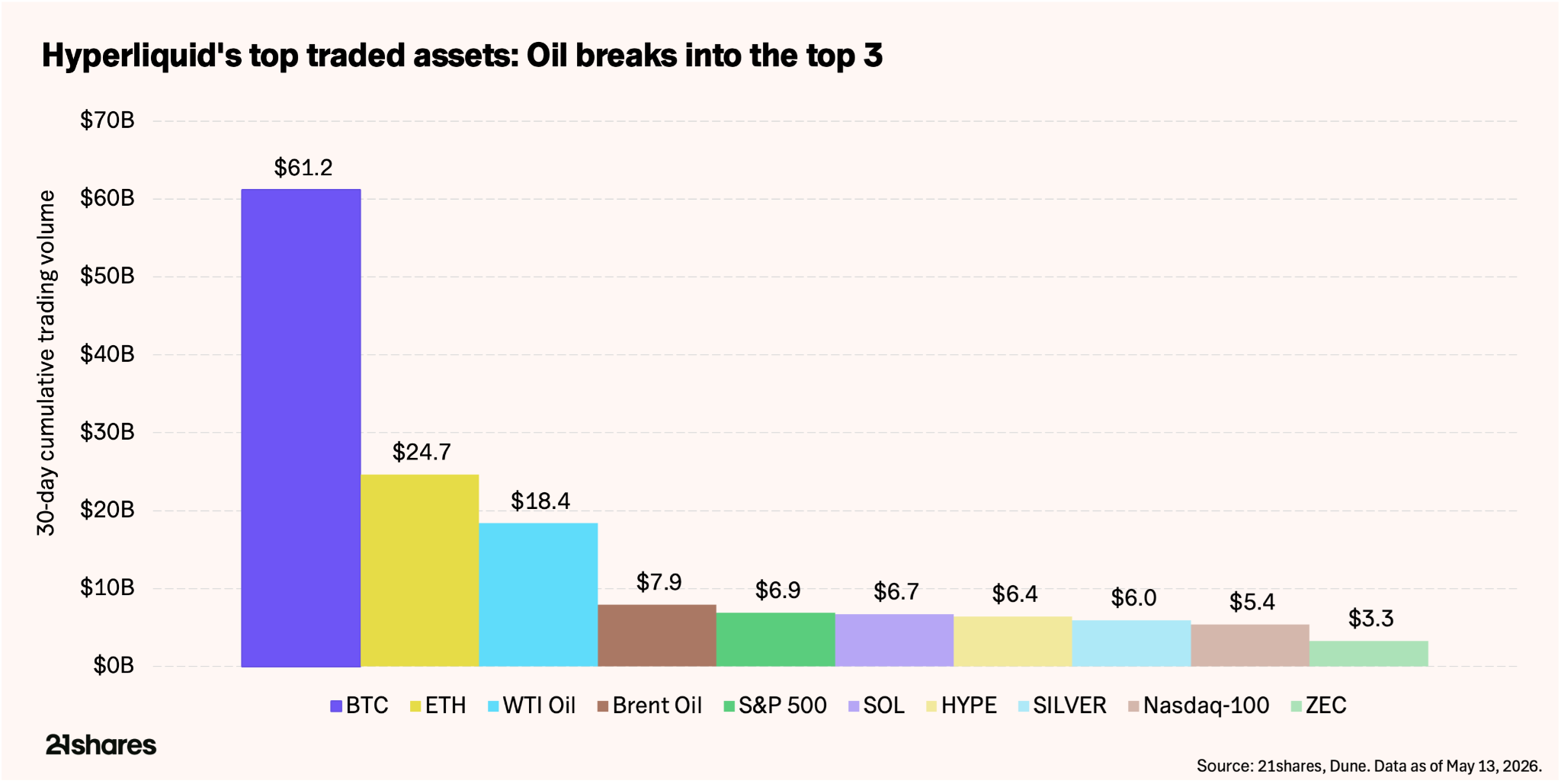

Bitcoin remains Hyperliquid’s highest-volume asset—but traditional assets—including the S&P 500, silver, Nasdaq-100, WTI, and Brent crude—now occupy half of the top ten traded assets. Individual equities such as Micron Technology (MU) even crack the top ten on certain days. We believe this illustrates Hyperliquid’s ultimate trajectory: it is no longer just a crypto perpetuals exchange—it has become a true “everything exchange,” enabling users to trade perpetual contracts on virtually any asset class.

Caption: Distribution of Hyperliquid’s top ten traded assets

Hyperliquid’s Business Model Is Evolving

This report helps you understand how to value Hyperliquid appropriately—and which key metrics and risks investors should monitor.

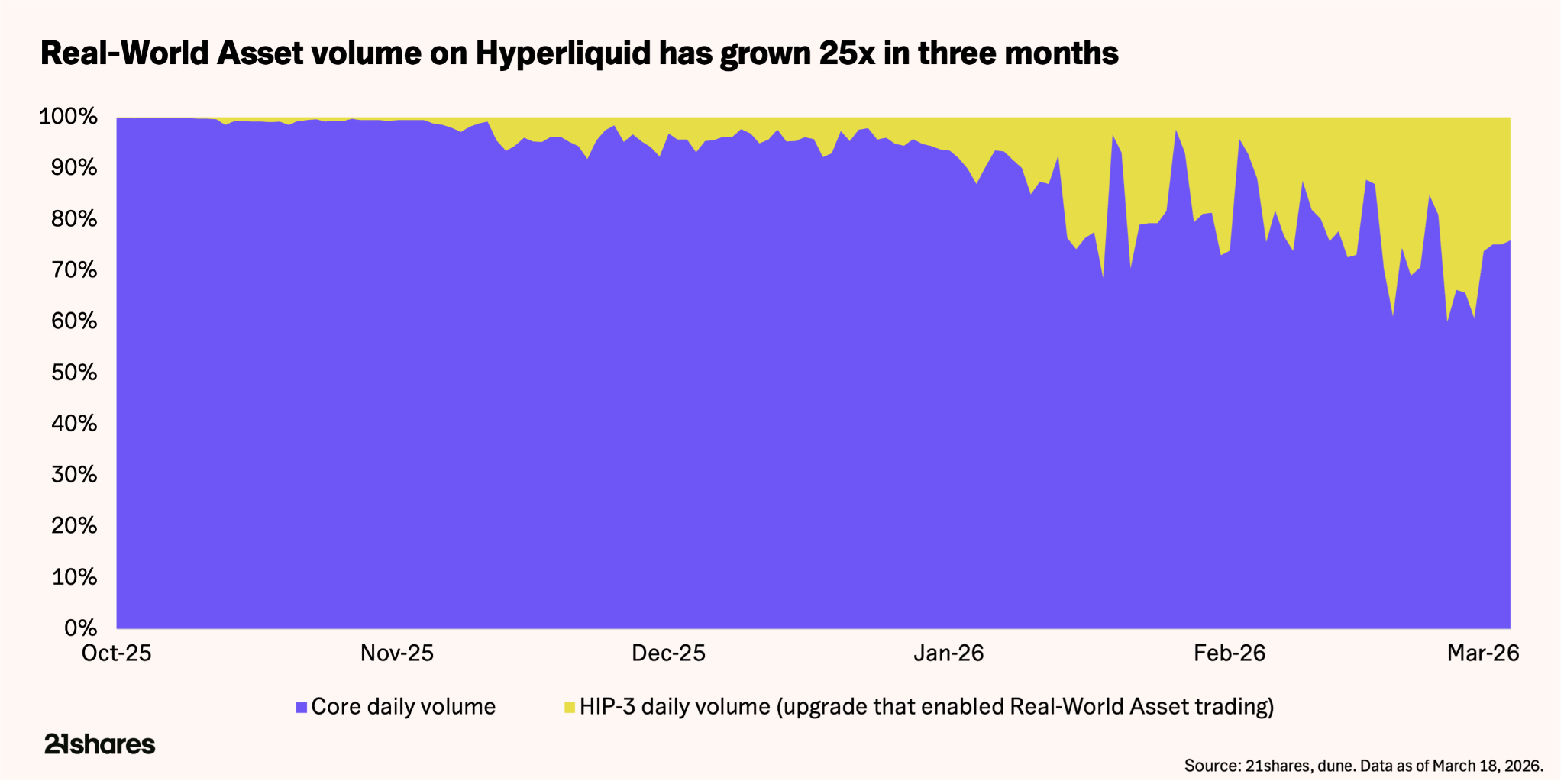

Historically, Hyperliquid derived most of its revenue from digital asset trading, making its business model highly correlated with broader crypto market trends. However, the rapid growth in non-digital asset trading volume has fundamentally broadened the platform’s core business model.

HIP-3 is the protocol’s permissionless framework, enabling anyone to launch new perpetual futures markets. HIP-3 currently accounts for ~35–37% of total trading volume—a 600–800% increase since end-2025. Open interest (OI) across these markets reached $1.7 billion in mid-May, up over 150% since February. Commodities make up ~$730 million of that OI, with crude oil alone representing ~20%.

The pace of change is rapid. Crypto trading pairs—the platform’s original business—have declined from ~90% to ~65% of total volume. Five of the current top ten traded assets are traditional-market instruments, such as commodities. A platform once dedicated solely to crypto derivatives is increasingly resembling a macro-focused exchange.

Hyperliquid’s bull case rests precisely on this asset-class diversification. In early May, HIP-4 launched—focusing on prediction markets and options—accelerating Hyperliquid’s evolution toward becoming the “everything exchange.”

Follow the Money

Hyperliquid’s data places it among the most profitable protocols in the digital asset space—and positions it for direct comparison with leading traditional derivatives exchanges:

- Cumulative historical trading volume: $4.22 trillion. Of this, $2.9 trillion occurred in 2025—roughly on par with CME Group’s $3 trillion in crypto derivatives contract volume.

- Cumulative protocol revenue: $1.15 billion. Revenue in 2025 alone totaled $873 million, compared to CME Group’s $6.5 billion for the same period.

Additionally, the HYPE token features a sustained buy-side force and value-return mechanism—the Assistance Fund. This fund automates token buybacks using 97–99% of platform-generated fees; cumulative buybacks have already exceeded $1.5 billion. This “share repurchase program” scales linearly with trading volume—requiring no board approval—and every trade directly impacts token supply dynamics.

At current operating rates, the implied buyback yield stands at ~13% of circulating market cap. For context: CME Group approved a $3 billion share repurchase program at end-2024 but deployed only $532 million—annualizing to ~$1.06 billion against a ~$105 billion market cap, yielding ~1%. Hyperliquid’s capital return efficiency is thus ~13x higher than CME’s—though accompanied by commensurately higher risk.

HYPE serves both as the medium of payment for trading fees and as collateral required to deploy new HIP-3 markets. Launching each new perpetual contract market currently requires locking up 500,000 HYPE tokens—valued at ~$19.5 million. As the platform expands into additional asset classes, HYPE is simultaneously withdrawn from circulation across multiple vectors. At current volume levels, the protocol is net deflationary: ~1.95 million HYPE tokens are bought back monthly, exceeding ~1.75 million tokens unlocked or released from staking.

Crunching the Numbers

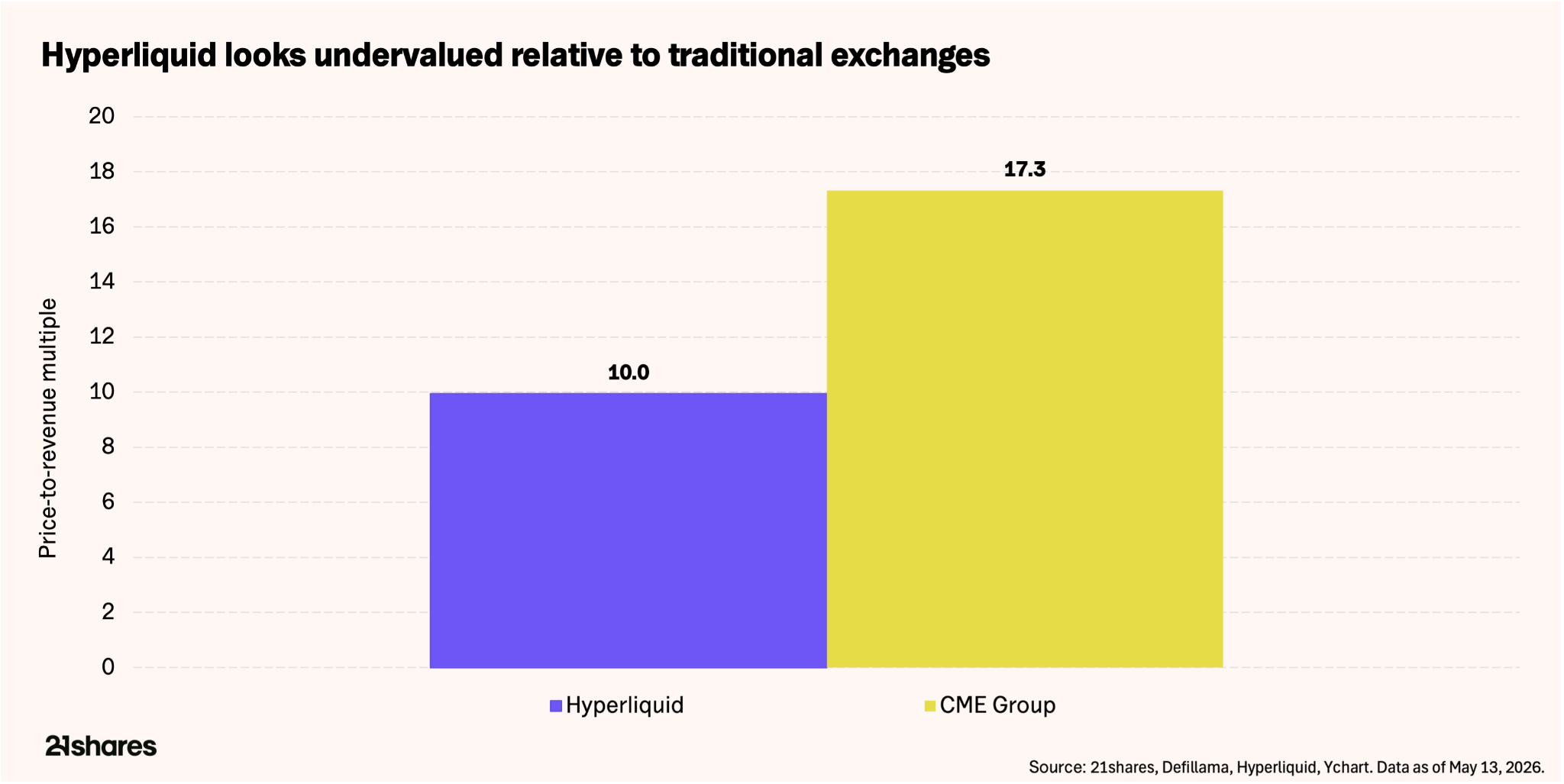

HYPE’s current circulating market cap stands at ~$9.4 billion. Against the past 12 months’ $944 million in revenue, Hyperliquid trades at a price-to-revenue (P/R) ratio of ~10x—compared to CME Group, the world’s largest derivatives exchange, which trades at a P/R of 17.32x, with a ~$110 billion market cap and $6.5 billion in 2025 revenue.

Caption: HYPE vs. CME—P/R ratios and revenue per employee

The market is already pricing HYPE using traditional exchange valuation frameworks. The real question is whether Hyperliquid’s revenue quality justifies such a comparison. To illustrate the blockchain infrastructure’s efficiency advantage over traditional systems: Hyperliquid generated $873 million in 2025 revenue with just 11 employees—$79.36 million per employee. By contrast, CME Group’s $6.5 billion revenue was produced by 3,875 employees—$1.7 million per employee. The disparity is stark.

On a fully diluted basis—including all 1 billion HYPE tokens (most of which remain locked)—the valuation rises to ~$37 billion, implying a P/R of ~38–39x. This figure holds only if revenue grows substantially before full token unlock. Yet given Hyperliquid’s >100% annualized user growth—and expansion into commodities, prediction markets, and beyond—this growth premium may be justified.

Rather than assigning a precise target price to the token, consider the following scenarios:

Bull Case: If geopolitical tensions persist, commodity trading remains elevated, traditional asset traders continue flocking to Hyperliquid after market close, and HIP-3 open interest grows to $3–5 billion, annualized revenue could reach $1.2–1.5 billion. Applying CME’s 16–17x P/R multiple implies a market cap of ~$15–17 billion—corresponding to HYPE at ~$62–70. Further acceleration is possible if options and prediction markets gain traction in coming months.

Base Case: Under similar assumptions, HIP-3 open interest grows to $3.2–5.3 billion, pushing annualized revenue into the $1.0–1.1 billion range. At a 17x P/R, implied market cap reaches ~$17–18 billion—corresponding to HYPE at ~$75.

Caption: Comparison of three valuation scenarios (Bull/Base/Bear)

Bear Case: If non-digital asset trading cools, buybacks may fail to offset token unlocks, and annualized revenue declines to $350–450 million. Applying a more conservative 10x multiple—reflecting slower growth and higher dilution—implies a market cap of ~$3.5–4.5 billion, corresponding to HYPE at ~$15–19—representing a 51–62% decline from current levels. This scenario does not yet factor in upcoming revenue diversification from prediction markets and options trading.

The market is validating our bullish thesis: Bitcoin is down 9% YTD, yet HYPE is up over 50%. This decoupling stems from HYPE’s ongoing shift toward diversified revenue. HYPE is not risk-free—it simply swaps crypto beta risk for geopolitical volatility. Whether this dynamic persists depends on geopolitical developments and team execution.

Risks That Demand Attention

HYPE carries several core risks investors must weigh alongside protocol growth:

Centralization and Attack Vectors: The 2025 JELLYJELLY and POPCAT token attacks nearly drained $230 million from the liquidity treasury, forcing validators to manually intervene and delist the assets. Though effective, this exposed the platform’s capacity for centralized action when fund security is threatened.

Regulation: Hyperliquid continues to geo-block U.S. users; on-chain commodities operate in a regulatory gray zone. Resolving this may require HYPE to obtain licenses—similar to Polymarket’s acquisition of a CFTC-regulated entity to legally serve the U.S. market.

Geopolitical Reversal: HIP-3 revenue benefits directly from global tensions. A cooling of macro volatility could rapidly erode the current “geopolitical VIX” premium driving platform usage—and thereby impact token value.

Issuance vs. Buybacks: Though the protocol is currently net deflationary, its ability to absorb ongoing token unlocks hinges entirely on sustaining high trading volumes.

Conclusion

Crude oil is trading on-chain—not out of decentralized idealism, but because every other market shut down. That distinction—utility over ideology—is the essential difference between Hyperliquid’s current narrative and prior DeFi stories.

Valued at a 13–15x annualized revenue multiple, the market is pricing HYPE as a legitimate exchange business—not a speculative meme coin. Its margin of safety hinges on whether non-crypto trading volume can sustain, whether buybacks can continue outpacing dilution, and whether new features deliver as expected.

The data itself—at minimum—merits your serious attention to HYPE. Whether it belongs in your portfolio depends on your judgment of the world beyond the charts.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News