How should we interpret the divergence between gold and oil prices?

TechFlow Selected TechFlow Selected

How should we interpret the divergence between gold and oil prices?

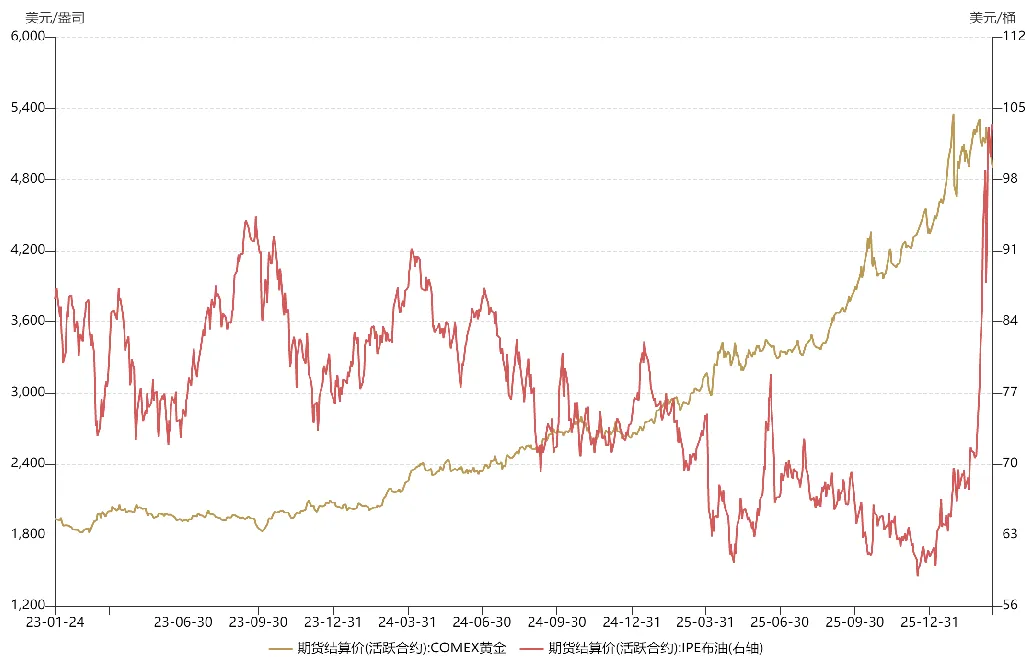

Since the outbreak of the Middle East war, gold and oil prices have experienced multiple fluctuations, and their trends have diverged, with different underlying causes.

Since the outbreak of the U.S.-Iran war, crude oil and gold—two commodities highly sensitive to geopolitical developments—have exhibited sharply divergent price trends: the former surged significantly, while the latter dipped modestly. Why is this happening?

As a natural currency, gold serves three primary safe-haven functions: hedging against geopolitical risk, inflation risk, and U.S. dollar risk. Gold prices are simultaneously influenced by these three forces, and thus its safe-haven role manifests to varying degrees across different phases.

Since the end of 2023, precious metals have entered a super bull market, with gold surging from $1,800 to over $5,000. This extraordinary upward momentum stemmed from gold fulfilling all three safe-haven roles—geopolitical, inflation, and dollar hedging—concurrently.

In October 2023, large-scale hostilities erupted between Israel and Hamas, escalating regional instability atop the ongoing Russia-Ukraine war. In 2024, the Red Sea crisis unfolded, with the Bab el-Mandeb Strait effectively blockaded. In 2025, Trump’s return to office further destabilized the international order. All these developments reflect deepening geopolitical chaos—and collectively underpin gold prices.

On the other hand, the U.S. economy shifted from overheating to stagflation in 2023. In 2024, amid political pressures, the Federal Reserve launched an aggressive easing cycle—even though inflation remained unresolved—reigniting dollar liquidity. On one side stood prolonged monetary easing; on the other, mounting risks of secondary inflation. Gold thus served dual roles—as both a hedge against dollar depreciation and against inflation—providing powerful fuel for its rally.

With all three safe-haven functions fully activated, how could gold not rise? Beyond that, benefiting from the Fed’s easing cycle, bull markets emerged across both emerging and developed markets—including both A-shares and U.S. equities.

Turning to oil: last year’s oil price center was notably lower than the year before, as Trump—upon taking office—courted OPEC to significantly ramp up crude output, aiming to pressure Russia into concessions at the negotiating table. This strategy initially bore fruit, with Putin repeatedly softening his stance on peace talks. Had the U.S.-Iran war not broken out, a ceasefire agreement between Russia and Ukraine was expected to be signed in the first half of this year.

Since the Middle East conflict erupted, gold and oil prices have undergone multiple swings, with their trajectories diverging for distinct reasons.

For gold: in mid-to-late January (half a month before the war began), as the probability of U.S.-Iran confrontation steadily rose, gold prices climbed—reflecting gold’s geopolitical safe-haven attribute. At the time, mainstream market expectations held that this conflict would resemble last year’s “Midnight Hammer” operation: relatively brief, and therefore more of a short-term, tactical move.

After the U.S. executed a “decapitation strike” against Iran, gold briefly rebounded—but soon plunged sharply. This occurred because major capital flows rotated out of gold and into crude oil. With gold positions already heavily concentrated, major investors sold gold to generate liquidity for new long oil positions. In other words, the “position rotation” from gold to oil directly drove gold down and oil up.

Meanwhile, overseas markets began pricing in a protracted U.S.-Iran war, pressuring risk assets like U.S. equities and triggering massive redemptions. The U.S. financial system faced a liquidity crunch. As the asset second only to cash in terms of liquidity, gold was aggressively sold off—not because international investors turned bearish on gold per se, but as a self-preservation measure amid the liquidity crisis. Thus, the heavy selloff in early March was not driven by fundamental pessimism toward gold, but rather by liquidity-driven defensive positioning.

If it were merely a liquidity crisis, the situation would be manageable: gold prices would typically form a “deep V” pattern, offering attractive entry points. But complications deepened after mid-March, as overseas sentiment toward the U.S.-Iran conflict grew markedly more pessimistic—not only fearing long-term closure of critical straits, but also anticipating large-scale attacks on each other’s energy infrastructure. Such scenarios would keep oil prices elevated for extended periods, inflicting devastating damage on the global economy—and potentially triggering a collapse of the international order. Under such expectations, the Fed might delay rate cuts—or even restart a hiking cycle, as it did in 2022. Based on this outlook, gold prices collapsed, with the correction breaking recent historical records.

In short, gold’s geopolitical safe-haven function remains intact—but the current plunge is primarily driven by shifting market expectations regarding reversal of Fed monetary policy. Gold’s “anti-dollar” safe-haven property—i.e., its inverse correlation with the dollar—has now overwhelmed its geopolitical and inflation-hedging attributes, becoming the dominant driver. Compared to prior corrections, gold’s fundamentals have changed: this is no longer about liquidity stress or profit-taking, but rather overseas concerns about tightening Fed policy. These concerns are mirrored across risk assets—including A-shares and U.S. equities—since when the nest falls, no egg remains unbroken.

Since the outbreak of the U.S.-Iran war, crude oil prices have likewise experienced a roller-coaster ride—driven largely by misperceptions among overseas investors regarding geopolitical dynamics. After the “decapitation strike,” oil prices rallied continuously, peaking near $120 per barrel. Yet in early March, Trump signaled that “the war would soon end,” prompting markets to execute the so-called “TACO” trade—betting on de-escalation in Iran—and sending oil prices tumbling nearly 30%. Unlike tariff disputes, however, geopolitical crises lie beyond Trump’s unilateral control: he cannot extricate himself cleanly while key straits remain blockaded. Ultimately, markets corrected their oil outlook, and prices resumed their upward trajectory.

Markets sometimes misprice geopolitical events—but such mispricing isn’t necessarily negative: falling oil prices can create accumulation opportunities, enabling latecomers to enter positions.

Looking ahead, gold and oil price trajectories hinge on the pace and evolution of the U.S.-Iran conflict. If it escalates into a protracted war akin to Russia-Ukraine, gold may lack allocation appeal in the first half of the year, and investors may instead prioritize energy-chain exposure in the near term. Yet the situation remains fluid: a pivotal turning point in the U.S.-Iran war may yet emerge—one that will determine whether the Strait of Hormuz can be reopened in the short term. That outcome rests squarely on Trump’s next move.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News