A Deep Dive into Shadow’s 2026 Key Focus Areas

TechFlow Selected TechFlow Selected

A Deep Dive into Shadow’s 2026 Key Focus Areas

In 2026, the Shadow Protocol will focus on building deep liquidity, internalizing MEV arbitrage revenue, burning 900,000 idle tokens, and launching xSHADOW Vaults to strengthen its already-profitable, sustainable economic model.

Author: Shadow Exchange

The Shadow Protocol has been live on the Sonic platform for over a year. During this period, it generated $26.52 million in revenue (or $46.6 million including rebases), while token emissions totaled only $21.61 million. This translates to a net surplus of $4.91 million (or approximately $25 million including rebases).

More importantly, despite declining overall activity on Sonic, Shadow remained profitable over the past 180 days. During this time, it generated $2.1 million in revenue against $1.5 million in emissions—yielding a net surplus of $600,000.

In 2026, our focus is to build upon this foundation: concentrating liquidity where it delivers the highest efficiency, internalizing more of the value Shadow previously lost, eliminating idle supply, and continuing to build $xSHADOW.

New Focus

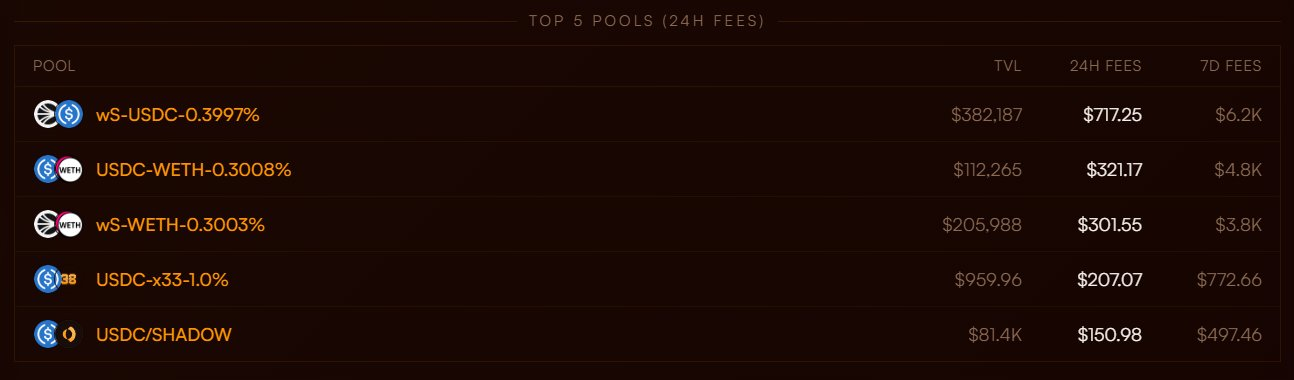

Liquidity-driven revenue generation has always been central to Shadow’s operations. Rewards naturally flow to pools that generate real fees—a core pillar of the protocol.

What’s changed is our focus. Over recent months, we’ve actively concentrated capital into assets that foster the deepest, most durable liquidity and enhance the profitability of internal arbitrage—for example:

The significance of these pairs extends far beyond surface-level metrics or TVL. After analyzing market structures across multiple blockchains, one conclusion stands out: the vast majority of trading volume for core assets comes from arbitrageurs and professional market makers—the very participants responsible for maintaining market equilibrium.

On certain blockchains, such activity is abundant—almost taken for granted. On Sonic, however, it is not. That means more work must be done at the DEX layer—and Shadow chooses to engage directly rather than wait for liquidity and volume to emerge organically.

This creates a clearer economic loop:

- Deep liquidity attracts and supports arbitrage/market-making capital flows

- Those flows generate fees and MEV opportunities

- Resulting revenue flows back to protocol participants

Simultaneously, we’re reducing emissions across the board. While the $S / $USDC pool remains the ecosystem’s most critical liquidity hub, increasing depth in markets where added liquidity directly improves internal arbitrage economics is prudent under current market conditions.

Our original goal was simple: every $SHADOW token emitted must create more value than its cost. That principle has held true since Shadow’s inception.

Now, our aim is to further enhance sustainability by diversifying revenue streams and increasing the value generated by the liquidity we choose to support.

We’ve already partnered with select market makers and professional liquidity providers to establish deep liquidity in core markets—and will continue expanding those collaborations where appropriate. If you or your team are interested in deploying deep liquidity on Shadow, please reach out directly.

Reverse Arbitrage

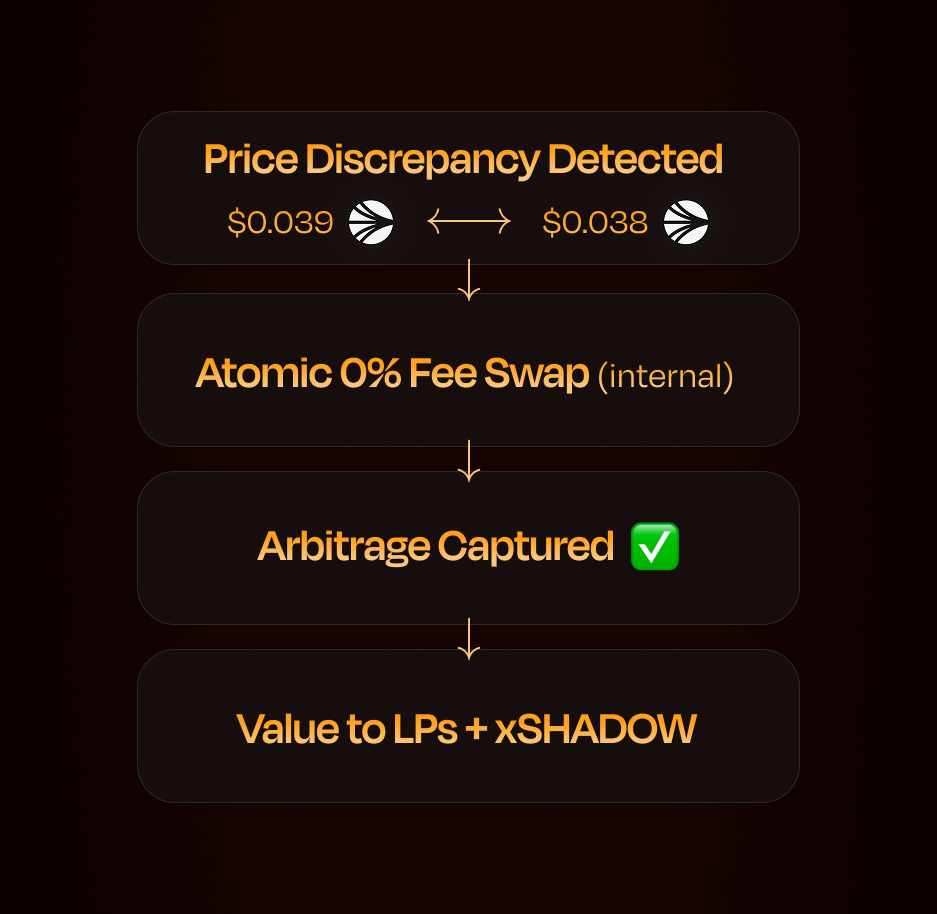

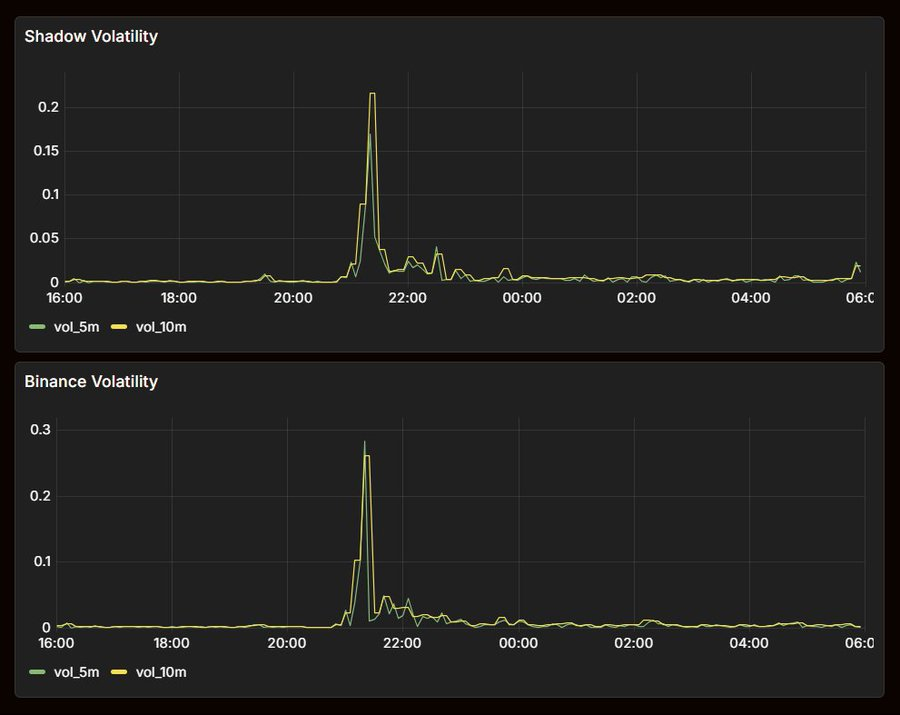

Shadow is deploying a permissioned reverse arbitrage bot, combined with deeply concentrated liquidity positions in core assets, to capture MEV before external bots can extract it.

How It Works

As an exchange operator, Shadow can execute zero-fee swaps atomically within its own liquidity pools in the same block. The bot does not need to monitor the mempool or compete in gas auctions. Instead, it identifies price discrepancies within Shadow’s liquidity pools and executes corrective trades before external arbitrageurs act.

External bots must pay standard swap fees, creating a no-arbitrage band around the pool price—in which trading yields no profit. The higher the fee, the wider the band, and the more opportunities go unclaimed.

Shadow’s arbitrage bot operates internally at 0% fee—meaning no price band exists. Even the smallest price discrepancy becomes actionable. Shadow captures spreads uneconomical for any other operator and retains that value within the protocol—precisely targeting those opportunities using deeply concentrated liquidity.

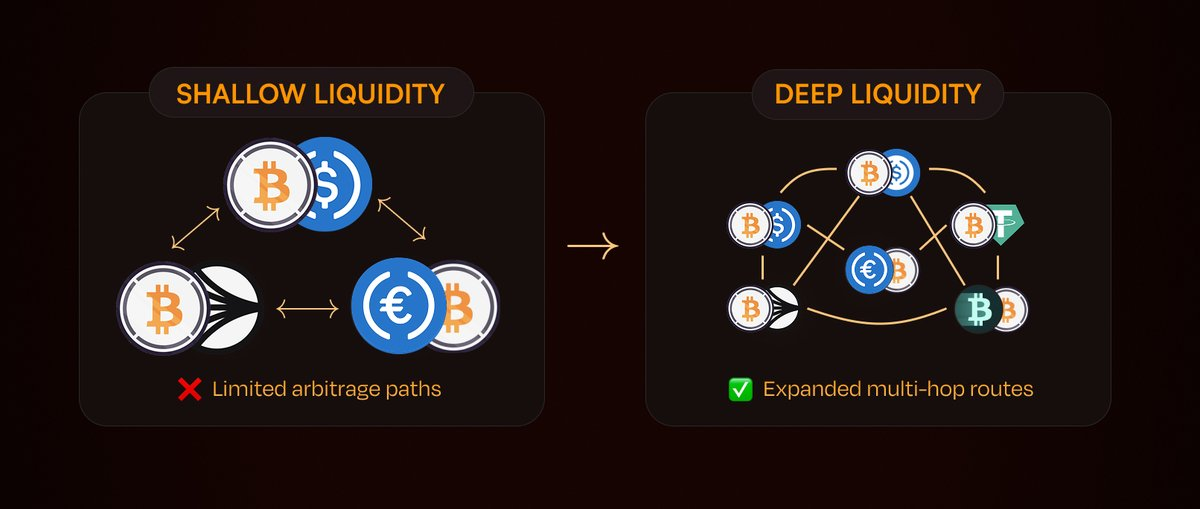

Scaling

The relationship between liquidity and arbitrage revenue is non-linear. Deeper pools support larger trades and generate more arbitrage opportunities. More genuinely deep pools mean more price relationships, more cross-asset trading paths, and more ways for Shadow to capture value before external bots intervene.

Crucially, this revenue growth isn’t fully dependent on Sonic. Every new pair, protocol, and trading venue expands the potential arbitrage surface. Stablecoins, wrapped assets, bridged assets, and cross-chain paths—all increase arbitrage space. As Shadow tightens spreads and deepens liquidity in core revenue-generating pairs (e.g., $S, $ETH, and $BTC), internalized MEV and arbitrage revenue become increasingly significant.

LP Protection

Internalizing MEV directly protects liquidity providers from three forms of value leakage: LVR (Loss-versus-Rebalancing), where arbitrageurs trade against stale pool prices; adverse selection, where harmful capital flows systematically extract value from LP positions; and external bot extraction, where value entirely leaks out of the ecosystem.

Shadow intercepts that value and returns it to participants.

This is critical because arbitrage costs aren’t evenly distributed across venues. Lower-liquidity venues bear disproportionate price-adjustment costs. In CEX–DEX arbitrage, CEX depth is near-infinite—meaning DEX LPs absorb nearly all rebalancing costs. Shadow’s reverse bot breaks this dynamic by capturing spreads before external arbitrageurs exploit the imbalance.

Dynamic Fees

Dynamic fees work in tandem with the bot to reinforce this advantage. During periods of high volatility, fees surge dramatically—to capitalize on volatility and protect LPs from harmful flows at precisely the most critical moments. When markets stabilize, fees decrease to remain competitive, improve execution efficiency, and sustain healthy trading volume. Unlike passive systems that adjust only after volatility manifests in pool metrics, Shadow’s fee model monitors CEX and DEX data—pricing risk before arbitrage opportunities even arise.

The underlying math is straightforward:

Each arbitrage event extracts value from the pool—but that extracted value splits into two parts: fees returned to LPs and residual profit retained by the arbitrageur.

When the fee-to-volatility ratio is high, fees absorb the vast majority of extracted value—86–95% flows back to LPs as fee income. Combined with Sonic’s sub-second block times, Shadow’s pools now operate under conditions where the fee barrier virtually eliminates all Liquidity Risk Value (LVR). Now, the reverse bot captures the remaining value.

In other words, dynamic fees reclaim most value during normal trading, while internal arbitrage closes any remaining gaps. LVR can never be fully eliminated—but dynamic fees and internal arbitrage reduce it to the lowest possible level.

Value Distribution

All captured value flows back to protocol participants via the x(3,3) system—no team cut. Captured value is redistributed through vote incentives and SHADOW buybacks, flowing back to the exact trading pairs that generated the revenue. Thus, the liquidity generating revenue is the same liquidity benefiting from it.

This distinguishes Shadow’s approach from models like Uniswap’s proposed fee auctions.

In Uniswap’s fee auction structure, arbitrageurs effectively bid on how much to extract from LPs—and resulting revenue flows to the protocol token, not back to the LPs bearing LVR. Shadow flips this model:

Fees are optimized to minimize LVR as much as possible; 100% of value captured by the bot flows back to the protocol and its participants. Because all revenue recirculates, LPs are structurally better off than they would be without any internalization mechanism.

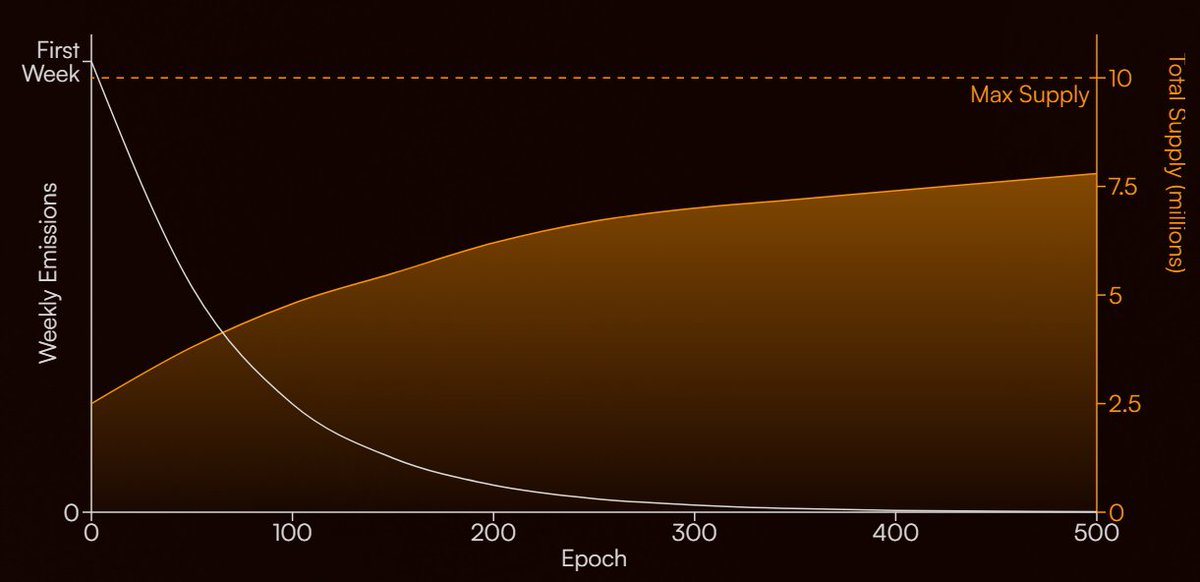

Token Burn

The Shadow token launched with an initial supply of 3,000,000 $SHADOW. Today, total supply stands at ~4,332,675 $SHADOW. Since the original tokenomics, three allocation categories have remained largely inactive: Partners, Reserve, and Community Incentives.

These tokens contribute little to liquidity, governance, or protocol growth—they serve primarily to inflate total supply.

We will burn them.

This burn removes 900,000 $SHADOW—30% of the initial supply and ~20.8% of current total supply. Post-burn, effective supply will stand at ~3,432,675 SHADOW.

Idle token supply serves only to inflate numbers—and benefits no one. Burning these tokens aligns Shadow’s effective supply more closely with its actual economic reality.

xSHADOW Vaults

Users can currently automate operations via x33—automatically voting and compounding rewards into their holdings. This works well for passive $xSHADOW holders but lacks fine-grained control: all value is automatically reinvested into $x33 / $SHADOW, even if users prefer holding other assets.

xSHADOW Vaults exist to solve exactly that. They deliver identical governance and yield exposure—but let users choose how to realize those rewards.

The first two strategies will target $S and $USDC, with additional strategies rolling out soon.

How It Works:

The system automates the following workflow:

- Automatically votes to maximize weekly rewards

- Automatically claims fees, vote incentives, and rebase rewards

- Automatically converts rewards into the user’s chosen target asset

Ultimately, users enjoy all $xSHADOW advantages—without manual intervention or being locked into perpetual compounding in x33 or $SHADOW.

Why This Matters

Discussions around vertical integration are intensifying. A prevailing view holds that blockchains must directly own the economic stack to route value back to their native tokens. The common assumption is that standalone applications are structurally misaligned with L1s—they optimize for their own tokens, while blockchains collect only gas fees. This framing treats each app as a value extractor, overlooking the possibility that protocols can do the opposite.

Shadow has generated over $26 million in revenue since launch—and maintained consistent net profitability. The $S treasury uses this revenue, trading fees, and vote incentives to directly purchase $S tokens. The entire process is automated, on-chain, and verifiable—requiring no human action. This isn’t a promise of future buybacks—it’s happening now.

A protocol that’s already profitable, already sustainable, and now directly investing profits into on-chain $S tokens aligns more closely with ecosystem ideals than any original design that hasn’t yet allocated revenue toward $S. Integration isn’t measured by codebase ownership—it’s measured by whether verifiable value actually flows into the asset.

Looking Ahead to 2026

As Shadow enters 2026, it has already achieved what most protocols still strive for: a sustainable, net-positive economic model.

Shadow is no longer a protocol trying to prove it can be profitable—it already is.

Our next step is optimization: concentrating emissions where liquidity is deepest, internalizing more value created by trading and arbitrage, delivering better protocol yield realization via xSHADOW Vaults, returning more value to $S, and removing supply that serves no productive purpose.

These initiatives are mutually reinforcing: deeper liquidity → more revenue → stronger sustainability → better product experience for all Shadow participants.

More details will follow with the launch of reverse arbitrage and xSHADOW Vaults.

Wishing everyone a successful and prosperous 2026!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News