Interview with Tom Lee: There Will Be a “Bearish” Correction in 2026, but Bitcoin Will Surge to $250,000

TechFlow Selected TechFlow Selected

Interview with Tom Lee: There Will Be a “Bearish” Correction in 2026, but Bitcoin Will Surge to $250,000

Don’t try to time the market—those who truly make money are long-term investors.

Compiled & Translated: TechFlow

Guest: Tom Lee

Host: Wilfred Frost

Podcast Source: The Master Investor Podcast with Wilfred Frost

Original Title: Tom Lee: Bear Market Coming in 2026 – Use It As Buying Opportunity

Release Date: January 20, 2026

Key Takeaways

Tom Lee is the co-founder and head of research at Fundstrat Global Advisors, chairman of Bitmine Immersion—an Ethereum-focused financial firm—and chief investment officer of Fundstrat Capital, which manages the rapidly growing Granny Shots ETF series (currently managing $4.7 billion in assets).

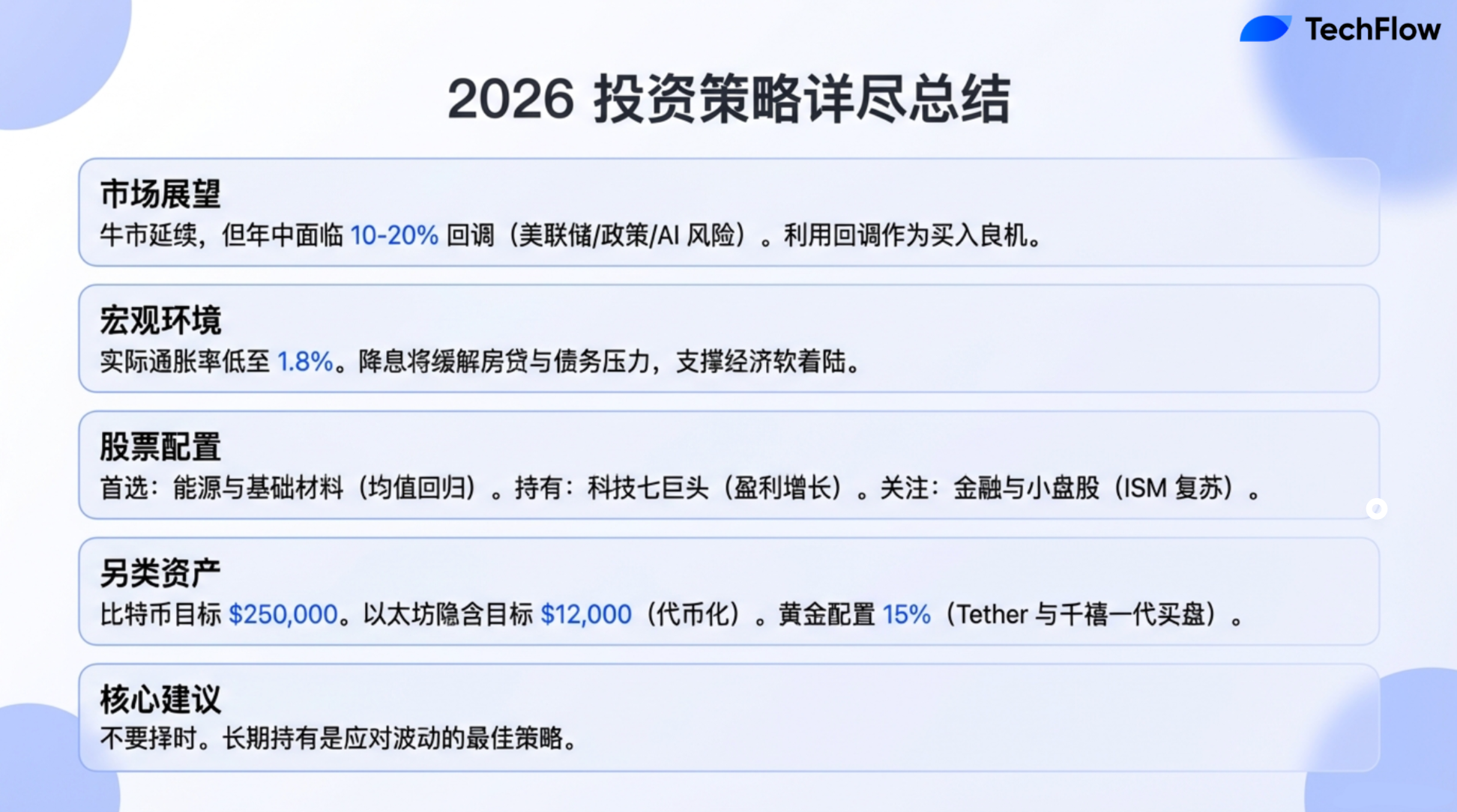

In this episode, Tom shares his market outlook. He believes the decade-long bull market that began in 2022 is still in its early stages. Although there may be a sharp market correction this year—feeling like a bear market—equity markets are poised for a strong rebound in 2026. He highlights three major shifts investors must navigate this year: new Federal Reserve leadership, a more interventionist White House, and the ongoing repricing of artificial intelligence (AI) enthusiasm. While he remains bullish on the “Magnificent Seven,” he suggests cyclical sectors such as energy, basic materials, financials, and small caps could become more compelling investment opportunities.

The discussion also covers gold, cryptocurrencies, and demographic trends. Tom argues that gold is currently undervalued and reveals that Tether may be one of the largest private buyers of gold today. He notes that millennials are rediscovering the value of gold, while younger generations gravitate toward cryptocurrencies. He maintains that Bitcoin remains "digital gold," while Ethereum is his top-pick cryptocurrency. He explains how last October’s deleveraging event caused crypto to decouple from gold's price trajectory and predicts significant gains for both Bitcoin and Ethereum as banks and asset managers accelerate blockchain adoption.

Additionally, Tom discusses Bitmine’s $200 million investment in MrBeast’s Beast Industries. He views MrBeast as one of the most influential media assets of this generation and believes financial education and Ethereum could become core components of future products reaching billions globally.

Highlights of Key Insights

- Bitcoin will reach a new all-time high this year, hitting $250,000.

- Tether has become the largest private buyer of gold.

- This year’s correction might be around 10%, but even a 10% drawdown will feel like a bear market.

- Every market pullback is an excellent buying opportunity.

- Our top sector picks this year are energy and basic raw materials.

- Banks have already started embracing the efficiency gains offered by blockchain technology.

- Silver and copper may perform well this year. Copper, as an industrial metal, closely correlates with the ISM index. If copper prices rise, I believe it will drive performance in basic materials stocks.

- When we look back at 2026, we’ll see it as a continuation of the bull market that began in 2022.

- There are several critical shifts in the market. First is the new Fed leadership, second is White House policy direction, and third is the market still trying to assess AI’s true value. Together, these factors could trigger a “bear-like” correction.

- Last year, investors overreacted to escalating tariff negotiations and uncertainty. This year, market reactions are likely to be more rational, with estimated reaction magnitude halved.

- Fed rate cuts can actually relieve economic pressure for many Americans.

- Once the Fed chair transitions or further rate cuts occur this year, it will ultimately benefit the stock market.

- Oil prices may appear weak or volatile in the short term, but developments in data centers and shifts away from alternative energy sources will support higher oil prices going forward—making energy stocks attractive.

- Bitcoin is digital gold, but the people who believe in this theory do not overlap much with traditional gold owners.

- Crypto adoption curves remain steeper than gold because far more people own gold than crypto.

- The most important advice I can give investors is not to try timing the market—those who truly make money are long-term investors.

- Cryptocurrencies are being embraced by younger generations—it has become part of their daily lives.

Market Outlook for 2026: A Bull Market with Pullbacks

Wilfred Frost: Welcome to The Master Investor podcast, I’m Wilfred Frost. Today’s guest is someone very familiar—Tom Lee. Tom is co-founder and research head at Fundstrat Global Advisors, chairman of the Ethereum asset management company Bitmine Immersion, and oversees the Granny Shots ETF—a fund focused on tech and innovation investments. We’re honored to have you here in London for our show.

It’s early 2026 now, Tom, and I noticed your remarkably accurate forecast for this year’s market path: a rally at the start, followed by a significant pullback, then another strong rebound by year-end. Does that accurately reflect your outlook for 2026?

Tom Lee:

I believe when we look back at 2026, we’ll see it as a continuation of the bull market that began in 2022, showcasing stronger economic resilience. However, I think the market faces several key transitions, two of which stand out. The first is the new leadership at the Federal Reserve. Markets typically test new Fed chairs’ policies, and the process of identifying, confirming, and reacting to those policies can spark a correction. The second factor is White House policy direction. In 2025, White House policies significantly impacted tech consulting and healthcare. In 2026, more industries, sectors, and even countries may come under focus. This shift introduces greater uncertainty—evident in rising gold prices reflecting risk concerns. These two factors could lead to a market pullback.

Wilfred Frost: You mentioned two factors—are there others?

Tom Lee:

Yes, a third factor is that the market is still assessing the real value of artificial intelligence (AI). While we believe AI remains a powerful market driver, questions linger about its long-term potential, energy demands, and data center capacity. Until these are clarified, the market may need other strong catalysts—like the recent rebound in the ISM manufacturing index or a housing recovery driven by lower interest rates. But these shifts also bring uncertainty. So collectively, these three forces could produce a “bear-like” correction.

Wilfred Frost: How deep do you expect this correction to be? A 20% peak-to-trough decline, or something milder?

Tom Lee:

Probably around 10%. But even a 10% pullback will feel like a bear market. It could go to 15% or 20%, potentially bringing the market back down to its starting level. Despite a strong beginning to the year, I expect a period of negative returns—but I believe the overall market performance by year-end will be very strong.

Wilfred Frost: Last August, you said we were at or near the beginning of a 10-year bull market. Do you still hold that view? In other words, if the market does correct, would you consider it a prime buying opportunity?

Tom Lee:

I’ve always believed every market correction is a great buying opportunity. Last year, when tariffs triggered a market drop on April 7, it turned out to be one of the best times in five years to buy equities. Many stocks hit new highs afterward and surged strongly. So yes, if the market corrects as expected this year, it will be an excellent entry point.

Drivers of the Long-Term Bull Market

Wilfred Frost: Last August, you suggested we might be at the start of a new 10-year bull market, citing reasons like a surge in prime working-age population, younger generations inheriting substantial wealth, and U.S. leadership in innovation—especially AI and blockchain. Are you still confident in these three long-term drivers?

Tom Lee:

Yes, in fact, they seem clearer now.

First, the U.S. benefits from favorable demographic trends, contrasting sharply with many countries facing shrinking workforces.

Second, regarding wealth transfer, there’s growing recognition that Gen Z, millennials, and Alpha generations will inherit vast sums over their lifetimes. While this may worsen inequality, it also means a new cohort of wealthy young individuals, while others build wealth through effort.

On AI, evidence mounts that we're advancing toward superintelligence. Progress is rapid, especially in robotics and integration with other technologies—reinforcing U.S. advantages. As for blockchain, its impact extends beyond firms like BlackRock and Robinhood. Jamie Dimon recently stated blockchain solves many financial service problems. I believe the banking sector has begun accepting blockchain-driven efficiency gains.

Wilfred Frost:

You remain firmly bullish on the long-term bull case and expect recovery post-correction. How can we better anticipate when this initial pullback might arrive? I recently heard your CNBC interview where you said markets often peak on good news—which sounds counterintuitive. Are we already seeing such positive signals suggesting a near-term market peak?

Tom Lee:

That’s hard to answer definitively. Right now, some signs are anecdotal. Our institutional clients aren’t positioned with extreme optimism, and until both public and institutional investors fully digest good news without pushing prices higher, I believe equities still have room to run. That’s why solid performance in the first week of January was encouraging, and ending the month with gains reinforces strength early in the year.

Margin debt is another indicator to watch. We track NYSE margin debt, which is at an all-time high—but its year-over-year growth is only 39%. Historically, local market peaks coincide with margin debt growth nearing 60%. So further leverage acceleration is possible—and that could signal a near-term peak.

Macro: Trade Wars and the Federal Reserve

Wilfred Frost: Let’s discuss macro factors. Starting with trade, I recall you said last year that trade war impacts weren’t as bad as feared. But over the weekend, new tariff threats emerged—this time involving Greenland and targeting the UK and EU. The UK may cave, while the EU could retaliate. Does this concern you in the short term?

Tom Lee:

There’s concern, but not severe. Last year, investors overreacted to escalating tariff talks and uncertainty, causing sharp declines. But this year’s reactions are likely to be more measured—perhaps half as intense. Uncertainty remains, though—such as how the Supreme Court rules on tariffs. An unfavorable ruling could weaken U.S. negotiating power, prompting more extreme White House actions and greater uncertainty. Still, recent reports suggest the Court may uphold Trump’s policies. So the outcome isn’t clear yet.

Wilfred Frost: Another key macro issue is the Federal Reserve. When we spoke last August, you said Fed rate cuts are good for markets, but questioning Fed independence is harmful. But I sensed you didn’t take the threat of intervention too seriously then. How do you see it today?

Tom Lee:

The situation remains similar. The Fed does face implicit threats, including DOJ investigations. Yet, voices within the administration still emphasize not fully undermining Fed independence. History shows the Fed remains one of the world’s most critical institutions—undermining its credibility and autonomy brings massive uncertainty.

We also know Chair Powell’s term ends this year. So the current stance feels like “letting time pass,” knowing a new chair will soon be appointed. Once a new chair takes office, I believe the White House will be satisfied. Current speculation on successors keeps shifting—Hasset’s odds seem lower now, while WH and Rick Reer are gaining traction. Broadly, markets expect rate cuts this year to exceed what economic data alone would justify.

Wilfred Frost: So, once the Fed chair changes or further rate cuts occur, will that ultimately be positive for equities?

Tom Lee:

Yes, I believe it will be positive for stocks. Since 2022, inflation has dominated market attention partly because the Fed fought it aggressively to preserve credibility. But based on underlying data, real inflation is lower than reported. For example, “real inflation” stands at 1.8%, as does median inflation. Housing costs keep headline CPI elevated, but home prices are actually falling. And housing cost calculations in CPI lag reality. So I believe the Fed has room to cut. If affordability becomes an issue, mortgage rates need addressing—and rate cuts help. Consumer installment debt burdens can also ease. Thus, Fed rate cuts can genuinely reduce financial stress for many Americans.

Sector Allocation: Energy, Materials, and Tech

Wilfred Frost: Let’s talk about investor sector allocation. Have the biggest stocks—like “MAG 7” or “MAG 10”—run too far? Are they no longer suitable for 2026 investing?

Tom Lee:

We remain bullish on the “MAG 7” due to confidence in their earnings growth. As long as they grow, they should outperform the market. But this year, our top sector picks are energy and basic materials. Back in early December, we identified these as preferred areas. Partly due to mean reversion—energy and materials performed poorly over the past five years, and historically such prolonged weakness often marks a turning point. Geopolitical dynamics also favor these sectors now.

I expect the ISM index to break above 50 again, combined with Fed rate cuts—meaning industrials, financials, and small caps could perform well. So while we like the “MAG 7,” cyclical sectors may offer more interesting opportunities this year.

Wilfred Frost: Let’s start with energy. I remember you said you’re not optimistic about near-term oil prices but remain bullish on energy stocks.

Tom Lee:

Correct. Oil prices and energy stocks don’t always move together. Energy stock valuations reflect expectations of future oil prices. I believe near-term oil prices may be weak or volatile, but long-term drivers—like data center expansion and shifts from alternative energy—will push prices higher, allowing energy stocks to perform well.

Wilfred Frost: On basic materials, especially metals, commodity prices have seen incredible runs. Perhaps we can tie this into crypto later. If metal prices correct, will these stocks underperform? Does your thesis depend on stable gold, silver, and copper prices?

Tom Lee:

Yes, if gold, silver, and copper post negative returns this year, the investment case for basic materials weakens. But we believe that despite gold’s big run, silver and copper may perform well. Copper, as an industrial metal, closely tracks the ISM index. Rising copper prices should lift basic materials stocks.

Wilfred Frost: Financials were a favorite of yours last August—and your call was spot-on. Those stocks have rallied strongly. Looking at their charts now, their gains seem almost unbelievable. Do you still like them? Their price-to-book ratios are no longer cheap.

Tom Lee:

No, they’re not cheap anymore—but I believe their business models are being positively redefined. Banks are heavily investing in tech and AI, positioning them as major beneficiaries of the superintelligence era. Labor costs are banks’ largest expense, and I believe they’ll reduce staffing needs going forward—boosting margins and reducing earnings volatility. I think banks will be revalued more like tech companies. When I started covering banks in the 90s, they traded at 1x book or 10x P/E. Now, they deserve premium valuations.

Wilfred Frost: I’d like to dive deeper into tech and AI-related stocks. You remain bullish—and your predictions over the past 15 years have been remarkably accurate. But you said only 10% of AI stocks will succeed over the next decade, which surprised me. Still, you’re bullish on the space, right?

Tom Lee:

Yes, this is typical in fast-growing fields. Look at the internet: if we examine the stock universe from 2000—25 years ago—only 2% of companies survived. But those 2% generated returns so large they dwarfed losses from the other 98%, delivering strong net outperformance versus the S&P 500. So in AI, even if over 90% of stocks fail, the winners will more than compensate.

Today’s listed companies are usually more mature, but that’s changing. For the first time, increasing numbers want to go public—not just via IPOs, but SPACs too. Meanwhile, alternative investments—VC, PE, private credit—aren’t delivering strong returns to LPs. So capital is shifting from alternatives to public markets, fueling listings. Over the past 12 months, many newly public stocks have performed strongly—so opportunities remain abundant.

Wilfred Frost: On mega-cap and ultra-large stocks, valuations are fascinating. Most are reasonable given their high growth. I heard you say something striking on another podcast—that these companies may evolve into consumer-like businesses, warranting premium valuations. That reminded me: did Warren Buffett see this earlier, like with Apple? Is that your view? Could Nvidia maintain its valuation even if growth slows?

Tom Lee:

Yes, consider Apple. Since its IPO in the 80s, analysts insisted it was a hardware company, refusing to value it above 10x P/E. But Apple built a robust services ecosystem and user retention model, proving it wasn’t just hardware. I recall meeting institutional investors between 2015–2017 who still called Apple a hardware company—now its valuation reflects a different reality.

People now view Nvidia similarly—as a cyclical hardware player—giving it only a 26x P/E. Yet Nvidia has exceptional earnings visibility, but trades at half Costco’s multiple. I believe these stocks still have significant room to re-rate higher.

Wilfred Frost: If macro conditions worsen more than expected, and the market sees your predicted 20% S&P 500 drop, will these stocks fall less—like consumer staples—or behave like volatile growth stocks and drop more?

Tom Lee:

Great question. In corrections, crowded trades tend to fall first (TechFlow note: Crowded trades refer to assets or stocks widely held by many investors. During volatility, especially downturns, investors rush to de-risk, amplifying price drops in these positions.) As MAG 7 are heavily owned, they may sell off initially. But when fear hits, investors often flee *to* the MAG 7 for safety. So I think non-U.S. stocks may fall harder—last year they outperformed U.S. stocks significantly. If trade tensions escalate or global growth falters, non-U.S. equities could see sharper corrections.

ETF Products: Granny Shots

Wilfred Frost: Let’s discuss your recent success stories—like “Granny Shots.” As I mentioned, this is your ETF or series of ETFs. When we spoke last August, AUM was $2–2.5 billion. Now it’s grown to $4.5 billion.

Tom Lee:

Yes, total AUM is now $4.7 billion across three ETFs. Granny GRNY is the largest. Granny J, launched in November, targets small- and mid-caps, with ~$355 million in assets. The income-focused Granny ETF began paying dividends last December. This typically drives inflows due to visible yield. Target yield is ~10%; current AUM is ~$55 million.

Wilfred Frost: For the coming year, is now a good time to invest in small-cap or income-oriented products rather than traditional ones?

Tom Lee:

I’m not one to time the market. Last January, Mark Newton warned of a pullback—the actual drop far exceeded expectations, hitting 20%. But we advised staying fully invested, and investors recovered losses by July.

I believe small- and mid-caps have underperformed for so long that even a correction won’t change their potential for a 5–6 year strong cycle. So I’d still hold them.

Naturally, if the broader market falls, Granny ETFs won’t rise. Investors must understand that. But these ETFs hold the strongest companies tied to major themes—so they should weather corrections better and outperform during recoveries.

Gold and Cryptocurrency

Wilfred Frost: Let’s start with gold, then move to crypto. What drove gold’s strong performance last year?

Tom Lee:

Some reasons are obvious, others less so. Obvious ones: First, greater political and geopolitical uncertainty in the investment environment. Wars worldwide, plus a U.S. president who performs well economically but increases global trade tension and fragmentation. Second, global central banks adopted looser policies, and the U.S. finally entered its easing cycle—including ending QT—supporting gold.

Less obvious: First, Tether (the largest U.S. stablecoin issuer) has become the largest private buyer of gold. Each USDT unit is fully backed by Treasuries, but Tether generates yield from these assets and uses excess profits to buy gold. I believe since July, Tether has been among the largest net buyers.

Wilfred Frost: When you say “believe,” is this based on solid data? Compared to central banks buying heavily lately, how big is Tether’s buying?

Tom Lee:

Yes, we’ve seen supporting data. I can’t specify exact volume, but I believe only one central bank bought more than Tether. Just observe the correlation between Tether’s USDT issuance and gold prices since July—they’re highly aligned.

Another factor: In 2018, we found investment preferences cross generational lines. Baby boomers love gold, Gen X favors hedge funds, and now millennials—entering peak earning years—are rediscovering their grandparents’ love for gold. This revived demand.

Wilfred Frost: I’m a millennial, and I liked gold—but sold too early. About gold: Is it ultimate money, or just a commodity like copper or silver? This changes how we view last year’s returns. Stocks like JPMorgan and Nvidia rose ~20%. But if gold is ultimate money, they actually fell. Your take?

Tom Lee:

At Fundstrat, we haven’t explicitly recommended gold—but maybe we should. You’re right: viewing gold as a commodity makes no sense—its industrial and jewelry sales totaled ~$120B last year, but its market cap hit $30T. Price-to-sales is absurd. And gold isn’t scarce—there’s plenty underground, and all gold is extraterrestrial (e.g., SpaceX might find a gold-rich asteroid, flooding supply).

Yet gold has served as a store of value for centuries. As you said, it acts as a dollar alternative. So we should treat gold as a dollar substitute—by that measure, all other assets depreciated against it.

Wilfred Frost: If so, will more people adopt this view? What are the implications?

Tom Lee:

Yes, it means gold deserves a place in portfolios. Ray Dalio recommends up to 10% allocation; you mentioned 15%. Assume 15%—but most portfolios hold nearly zero gold. So gold remains severely underowned.

Wilfred Frost: Why didn’t crypto perform as well as gold last year?

Tom Lee:

It’s a matter of timing. Crypto tracked gold closely before October 10. Bitcoin was up 36%, Ethereum 45%—outperforming silver. But on October 10, crypto saw its largest-ever deleveraging event—bigger than FTX in November 2022. Bitcoin dropped over 35%, Ethereum nearly 50%.

The market underwent deleveraging, wiping out liquidity providers—who in crypto act like central banks. About half of market makers were eliminated that day. Until mainstream institutions widely adopt crypto, such internal shocks will remain impactful.

Wilfred Frost: Does that mean you admit Bitcoin isn’t digital gold?

Tom Lee:

Bitcoin is digital gold, but believers don’t overlap with gold owners. Hence, crypto’s adoption curve remains steeper than gold’s—because more people own gold than crypto. Adoption will be bumpy. I see 2026 as a crucial test. If Bitcoin hits a new high, we’ll know the deleveraging phase is over.

Wilfred Frost: Your 2026 Bitcoin price target is $250,000, right? What drives that?

Tom Lee:

Yes, we expect Bitcoin to reach a new high this year. Drivers include rising utility. Banks now recognize blockchain’s value—settlement and final clearing on blockchain are highly efficient. Crypto-native banks like Tether prove blockchain-based banking outperforms traditional models. Tether is projected to earn nearly $20 billion in 2026—ranking among the world’s top-five most profitable banks. Valuation-wise, it could rival JPMorgan or exceed Goldman Sachs/Morgan Stanley.

Tether has only 300 full-time staff vs. JPMorgan’s 300,000. Using blockchain, Tether earns as much as any major bank—sometimes more—despite having less than 1% of M1 and a tiny balance sheet. Yet it’s among the world’s most profitable banks.

Wilfred Frost: Let’s discuss Ethereum. Last August, you said you liked both Bitcoin and Ethereum, but long-term, Ethereum would outperform. Why did Ethereum fall so hard in Q4?

Tom Lee:

Ethereum is the second-largest blockchain. I believe it will remain more volatile than Bitcoin until its scale approaches Bitcoin’s. Crypto markets often price Ethereum relative to Bitcoin. If we treat ETH/BTC ratio as the benchmark, Ethereum still trades below its 2021 levels. Yet compared to four years ago, Ethereum is a superior blockchain.

Tokenization—including dollar tokenization—is a major trend Wall Street is betting on. Larry Fink calls it the biggest innovation since double-entry bookkeeping. Robinhood’s Vlad Tenev wants to tokenize everything. We’re already seeing not just dollars (stablecoins), but credit funds moving toward tokenization. JPMorgan is launching money market funds on Ethereum; BlackRock has tokenized credit funds on Ethereum. So Ethereum is becoming Wall Street’s blockchain of choice. If ETH/BTC ratio returns to 2021 highs while Bitcoin hits $250K, Ethereum could reach ~$12,000. It’s now around $3,000.

Bitmine Immersion and MrBeast Investment

Wilfred Frost: Last week, you announced a $200 million investment in Beast Industries (MrBeast’s company). MrBeast is one of the world’s biggest YouTube influencers. From what I understand, his media influence is staggering, correct?

Tom Lee:

Yes, most on Wall Street underestimate MrBeast’s impact—for two reasons. First, it’s a private company, so we rely on media metrics. Second, he’s iconic among Gen Z, Alpha, and millennials.

He has over 1 billion followers. Only Cristiano Ronaldo exceeds him across TikTok, Instagram, and Meta. His YouTube videos get more monthly viewing hours than Disney and Netflix combined. Each MrBeast video gets over 250 million monthly views; he releases two per month—equivalent to two Super Bowls monthly. Plus, Beast Games on Amazon Prime is the platform’s #1 show, outperforming most movies.

Wilfred Frost: Those stats are mind-blowing. But why didn’t Disney, Amazon Prime, Comcast, or Netflix invest in Beast Industries—while an Ethereum treasury firm did?

Tom Lee:

They’re selective about capital structure. MrBeast (Jimmy Donaldson) is the largest shareholder. Others include Chamath Palihapitiya of Social Capital. Bitmine is the largest corporate investor on their balance sheet. Many firms want in—we were lucky to be invited.

Wilfred Frost: At Bitmine’s annual shareholder meeting last week, you mentioned Beast Industries plans to launch financial products. Is this confirmed? Will you participate?

Tom Lee:

Yes, CEO Jeff Henbold discussed future plans for Beast Financial Services. More details may emerge in coming weeks. They’re brilliant at productizing the MrBeast brand—Feastables chocolate, healthy meals, drinks, creator collabs. With 1 billion fans, further monetization is natural.

Wilfred Frost: Could this benefit Ethereum? Might MrBeast promote Ethereum to his 1 billion fans?

Tom Lee:

Very likely. Global financial literacy gaps are huge—especially among youth, as schools don’t teach it. Financial literacy is vital—many boomers and Gen Xers retire under-saved, and Social Security isn’t reliable. So financial education is one of society’s biggest voids.

MrBeast could become a leader in financial education—bringing immense social benefit. That’s one reason we’re excited—our values align. MrBeast represents kindness and integrity.

On finance’s future, banks now clearly state blockchain is the way forward. JPMorgan wants to build on blockchain; Jamie Dimon says it’s a better way to build banks. Today, banks building smart contracts choose Ethereum. So if financial education goes mainstream, Ethereum should play a role.

Wilfred Frost: Final question—I still find this investment somewhat off-strategy for a treasury firm. You mentioned “moonshot investments” like Orbs—does that mean you acknowledge this is high-risk? Or is it strategic?

Tom Lee:

I understand—it looks risky to those unfamiliar with our logic. But it’s logical. From inception, Bitmine committed ~5% of its balance sheet to “moonshot investments.” At current size, that’s ~$700 million; we’ve deployed ~$220 million so far.

I see Beast Industries as highly promising—it connects us with the world’s largest content creator, possibly the defining media figure of our generation. He’s unprecedented—no one may surpass him for decades. As a treasury firm, our goal isn’t just strengthening the Ethereum ecosystem, but ensuring its long-term sustainability. A potential organic partnership with MrBeast could cement Ethereum’s future. So this is a strong strategic move.

Final Advice

Wilfred Frost: Two final questions. First, what’s your most important advice for equity investors this year?

Tom Lee:

The most important advice I can give is: don’t try to time the market. Doing so becomes your worst enemy. Many want to buy at the bottom and sell at the top. But historically, in both stock and crypto markets, the people who make real money are long-term holders. Even with my warning of 2026 volatility, investors should treat pullbacks as buying opportunities—not exit signals. Too many sell emotionally, miss re-entry, and lose compounding. That distinction matters.

Wilfred Frost: Second, what’s your long-term advice for crypto investors? I suspect it ties to your earlier point—but how should they invest?

Tom Lee:

Many listeners remain skeptical—or avoid crypto entirely—because they feel they can’t grasp it. But cryptocurrencies are being embraced by younger generations—it’s part of their lives, as digital natives. In the future, the line between services and money will blur. This mirrors Bill Gates on David Letterman in 1995 explaining the internet. Letterman doubted it—he belonged to a generation that couldn’t easily accept it. But explain the internet to a 20-year-old then, and they’d instantly get it. Crypto is at that same inflection point today.

Wilfred Frost: So how should people invest in crypto? Do you recommend Bitmine? Should they hold a basket? Invest in treasury firms? Allocate 2:1 to Bitcoin and Ethereum?

Tom Lee:

I suggest a dual approach. First, apply the “Lindy Effect”—invest only in cryptos that have stood the test of time, like Bitcoin and Ethereum. Second, crypto may become an invisible “settlement layer” in finance. Bitmine acts as that layer—and through our investments, we’re evolving into a financial services company. So investing in Bitmine isn’t just backing Ethereum—you’re backing a firm shaping the future of finance.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News