The US stock market is playing a new type of AI roulette game

TechFlow Selected TechFlow Selected

The US stock market is playing a new type of AI roulette game

Who exactly provided this 100 billion?

By Fan Wu

A recent joke circulating in U.S. stock market circles goes like this:

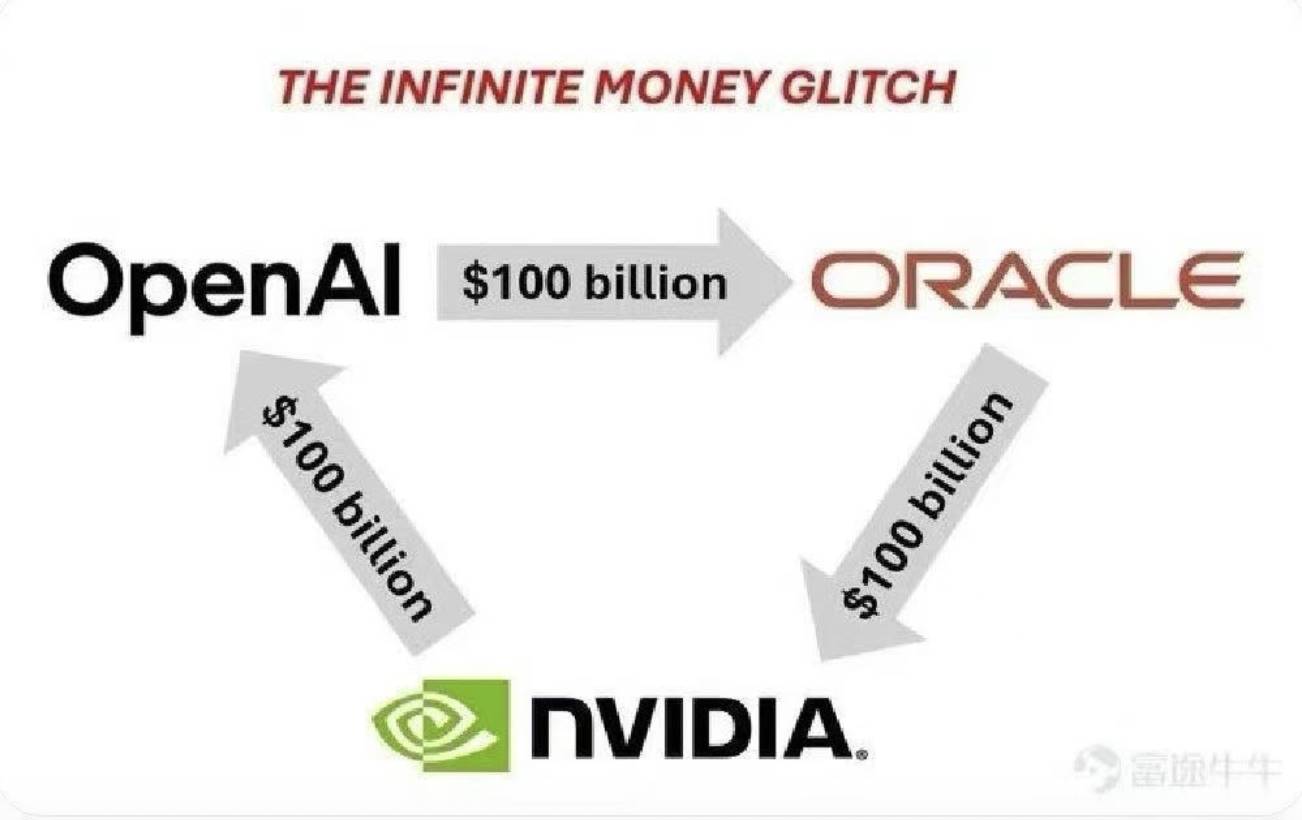

"OpenAI invests $100 billion in Oracle to buy cloud computing services; Oracle invests $100 billion in NVIDIA to buy GPUs; NVIDIA then invests $100 billion in OpenAI to build AI systems. Question: Who actually paid the $100 billion?"

Of course, this is just a joke—the figures and facts are greatly exaggerated, and these three companies aren't literally passing the same money around in a loop. But it does reflect a real phenomenon: a closed-loop new capital narrative.

In this loop, every link represents actual contracts or investments, and each move gets amplified by financial markets, leading to trillions of dollars in market cap gains.

On September 11, Oracle's stock surged 36%, its largest single-day gain since 1992. Overnight, the company’s market value soared to $933 billion, briefly making founder Larry Ellison the world’s richest person, surpassing Elon Musk.

On September 22, NVIDIA and OpenAI announced a strategic partnership, with NVIDIA planning to invest up to $100 billion in OpenAI. NVIDIA closed nearly 4% higher that day, pushing its market cap above $4.46 trillion and igniting a rally across tech stocks, sending all three major U.S. indices to record highs.

The $100 billion figure may sound huge, but it triggered over a trillion dollars in gains across U.S. equities overnight—a textbook case of spending a little to achieve a lot.

The U.S. stock market is playing a new kind of AI roulette game.

The Triangular Loop: How the Money Flows

In the real-world version of this investment maze, three names form a perfect capital loop: OpenAI, Oracle, and NVIDIA.

First Leg: OpenAI’s Hunger for Compute Power

The central character is OpenAI. As the creator of ChatGPT, OpenAI processes requests from 700 million users daily. This scale of AI operation demands massive computational power.

This year, OpenAI signed the largest technology contract in history with Oracle—a five-year, $300 billion cloud computing agreement. Under this deal, OpenAI will pay Oracle about $60 billion annually, roughly six times its current annual revenue.

What is this money buying? 4.5 gigawatts of data center capacity—enough to power 4 million American households. Oracle will build data center campuses across five states, including Wyoming, Pennsylvania, and Texas, dedicated to OpenAI.

For OpenAI, this ensures space and compute resources to run models; for Oracle, it locks in revenue certainty for the next five years.

Second Leg: Oracle Needs Chips

With OpenAI’s massive order in hand, Oracle faces a challenge: how to build these data centers?

The answer is chips—lots of them. Oracle plans to spend tens of billions of dollars on NVIDIA GPUs under its Stargate project. Industry estimates suggest that 4.5 gigawatts of compute power would require more than 2 million high-end GPUs.

Oracle CEO Safra Catz stated bluntly: "The vast majority of our capital expenditures are invested in revenue-generating equipment that will go into our data centers."

These "revenue-generating devices" are primarily NVIDIA’s H100, H200, and the latest Blackwell chips.

Oracle has become one of NVIDIA’s largest customers.

Third Leg: NVIDIA Gives Back

Just as Oracle ramps up GPU purchases, NVIDIA announces a stunning move: investing $100 billion to support OpenAI in building a 10-gigawatt AI data center complex.

This investment will be phased—NVIDIA will contribute funds each time OpenAI deploys one gigawatt of compute. The first phase is expected to launch in late 2026 using NVIDIA’s Vera Rubin platform.

NVIDIA CEO Jensen Huang said in an interview: "A 10-gigawatt data center capacity equates to 4 to 5 million GPUs—roughly our entire annual shipment volume this year."

Thus, a perfect capital cycle is formed:

OpenAI pays Oracle for compute, Oracle uses that money to buy chips from NVIDIA, and NVIDIA reinvests part of those earnings back into OpenAI.

The Wealth Amplifier Between Reality and Illusion

A $300 billion long-term contract leads to Oracle gaining over $250 billion in market cap in a single day; a $100 billion investment drives NVIDIA’s market cap up by $170 billion in one session.

The three companies endorse each other, creating stock price resonance.

There is logic behind the rising valuations.

To financial markets, future certainty is the rarest commodity.

The Oracle–OpenAI contract means Oracle’s cloud revenue is locked in for five years, justifying a higher valuation from investors.

Beyond that, NVIDIA is now using "gigawatts (GW)" as a unit of measurement. One GW roughly equals the size of a super-scale data center. Ten GW implies that NVIDIA and OpenAI are building next-generation AI factories. This narrative—framed in terms of infrastructure scale rather than just "number of GPUs sold"—is far more compelling and easier for markets to embrace.

NVIDIA investing in OpenAI signals, "I believe it will be a dominant future customer"; OpenAI signing with Oracle says, "Oracle can meet my future cloud compute needs," helping OpenAI secure further funding; Oracle purchasing NVIDIA GPUs signals, "NVIDIA’s chips are in high demand."

This forms a stable and thriving industrial chain.

The loop appears flawless, but closer inspection reveals its subtleties.

OpenAI currently generates about $10 billion in annual revenue but has committed to paying Oracle $60 billion per year. Where will the massive shortfall come from?

The answer lies in successive funding rounds. In April, OpenAI raised $40 billion and is expected to raise more.

In reality, OpenAI uses investor funds to pay Oracle, Oracle uses that money to buy NVIDIA chips, and NVIDIA reinvests part of its income back into OpenAI. It’s a cycle driven entirely by external capital.

Moreover, these astronomical contracts are largely based on "commitments" rather than immediate delivery—they can be delayed, renegotiated, or even canceled under certain conditions. The market sees only the headline numbers, not the actual cash flow.

This is the magic of modern financial markets: expectations and promises can generate multiplied wealth effects.

Who Pays the Bill?

Returning to the original joke: "Who actually paid the $100 billion?"

The answer: investors and debt markets.

Firms like SoftBank, Microsoft, and Thrive Capital are direct funders in this game. They pour tens of billions into OpenAI, fueling the entire capital loop. Meanwhile, banks and bond investors finance Oracle’s expansion. Ordinary individuals holding related stocks and ETFs become the silent bill-payers at the end of the chain.

This AI capital rotation game is essentially a form of financial engineering for the AI era. It leverages market optimism about AI’s future to create a self-reinforcing investment cycle.

In this loop, everyone wins: OpenAI secures compute power, Oracle lands orders, NVIDIA gains sales and investment opportunities. Shareholders watch their paper wealth grow—everyone is happy.

But this joy rests on one assumption: that AI’s commercialization can eventually justify these astronomical investments. If that premise falters, the elegant loop could spiral into a dangerous downturn.

In the end, every investor who believes in AI’s future becomes a payer—betting today’s money on tomorrow’s AI era.

Let’s hope the music doesn’t stop.

Disclosure: The author holds shares in NVIDIA and AMD.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News