Stock Tokenization Panorama: From Physical Share Custody to Derivatization, How to Bridge the Last Mile?

TechFlow Selected TechFlow Selected

Stock Tokenization Panorama: From Physical Share Custody to Derivatization, How to Bridge the Last Mile?

A brief overview of the evolution of stock tokenization models, and an exploration of the second growth curve in future derivatives and liquidity release.

Author: imToken

Stock tokenization is becoming the most compelling narrative for the convergence of TradFi and Web3 in 2025.

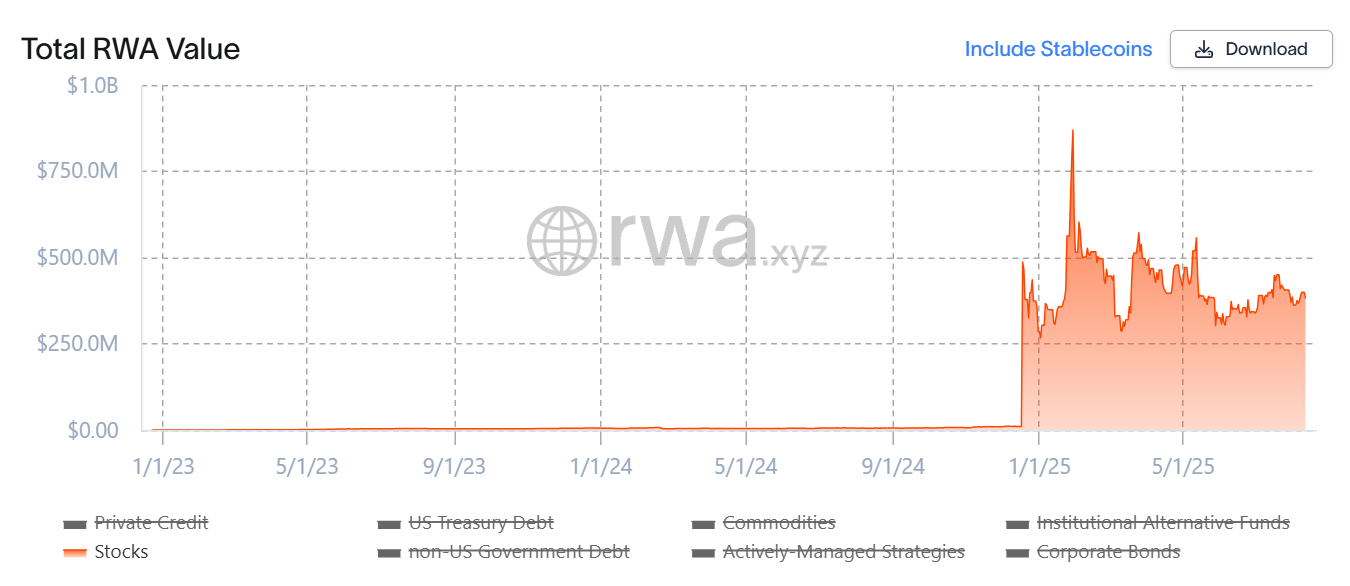

Data from rwa.xyz shows that since the beginning of this year, the market size of stock-backed tokenized assets has surged from nearly zero to hundreds of millions of dollars. Behind this growth lies an accelerating shift of stock tokenization from concept to reality—evolving from synthetic assets to real-share custody models, and now extending toward more advanced forms such as derivatives.

This article provides a brief overview of the evolution of stock tokenization models, reviews key projects, and explores potential trends and shifts in the landscape.

Source: rwa.xyz

I. The Past and Present of U.S. Stock Tokenization

What is stock tokenization?

In simple terms, it's the process of mapping traditional stocks onto blockchain technology as digital tokens, with each token representing partial ownership of the underlying asset. These tokens can be traded on-chain 24/7, breaking through the time and geographical constraints of traditional stock markets and enabling seamless global investor participation.

From a Tokenization perspective, U.S. stock tokenization isn't exactly a new concept (see further reading: "Behind the 'Stock Tokenization' Craze: The Evolution Roadmap of the Tokenization Narrative"). After all, during the last cycle, representative projects like Synthetix and Mirror had already developed a complete set of on-chain synthetic asset mechanisms:

This model allowed users to mint and trade "U.S. stock tokens" such as TSLA and AAPL by over-collateralizing (e.g., SNX, UST), and even extended coverage to fiat currencies, indices, gold, crude oil—essentially encompassing nearly all tradable assets. The reason lies in how synthetic assets work: they track the price of underlying assets and are minted via over-collateralization.

For example, users could deposit $500 worth of crypto assets (such as SNX or UST) to mint synthetic assets (like mTSLA, sAAPL) pegged to the asset’s price and then trade them. The entire mechanism relies on oracle pricing and on-chain contract matching, without requiring actual counterparties, theoretically enabling infinite depth and zero-slippage liquidity.

However, this model does not confer actual ownership of the corresponding stocks—it's essentially betting on price movements. This means that if oracles fail or collateral crashes (as Mirror did during the UST collapse), the system faces risks of liquidation imbalance, price de-pegging, and loss of user confidence.

Source: Mirror

The biggest difference with this wave of "U.S. stock tokenization"热潮 is its adoption of the "real-share custody + mapped issuance" model, which currently follows two main paths, differing primarily in whether the issuer holds regulatory compliance credentials:

-

One path is the "third-party compliant issuance + multi-platform access" model represented by Backed Finance (xStocks) and MyStonks, where MyStonks partners with Fidelity to achieve 1:1 pegging to real stocks, while xStocks purchases and custodies stocks through entities like Alpaca Securities LLC;

-

The other is the licensed brokerage self-operated closed-loop model exemplified by Robinhood, which leverages its own brokerage license to handle everything from stock acquisition to on-chain token issuance;

From this perspective, the key advantage of this current wave of stock tokenization is verifiable underlying assets, offering higher security and compliance, making it more acceptable to traditional financial institutions.

II. Key Projects: Mapping the Upstream and Downstream Ecosystem from Issuance to Trading

In terms of architecture, a fully functional tokenized stock ecosystem must include at least infrastructure layers (blockchain, oracles, settlement systems), issuance layers (issuers), and trading layers (CEX/DEX, lending, derivative trading platforms). Without any one of these layers, the ecosystem cannot achieve secure issuance, effective pricing, or efficient trading.

Within this framework, we see that current market participants are positioning themselves across different segments. Given that infrastructure components (such as blockchains, oracles, and settlement networks) are relatively mature, the battleground for competition lies mainly in issuance and trading. Therefore, this article focuses on representative projects that directly impact user experience and market liquidity.

Ondo Finance: RWA Leader Expanding into Stock Tokenization

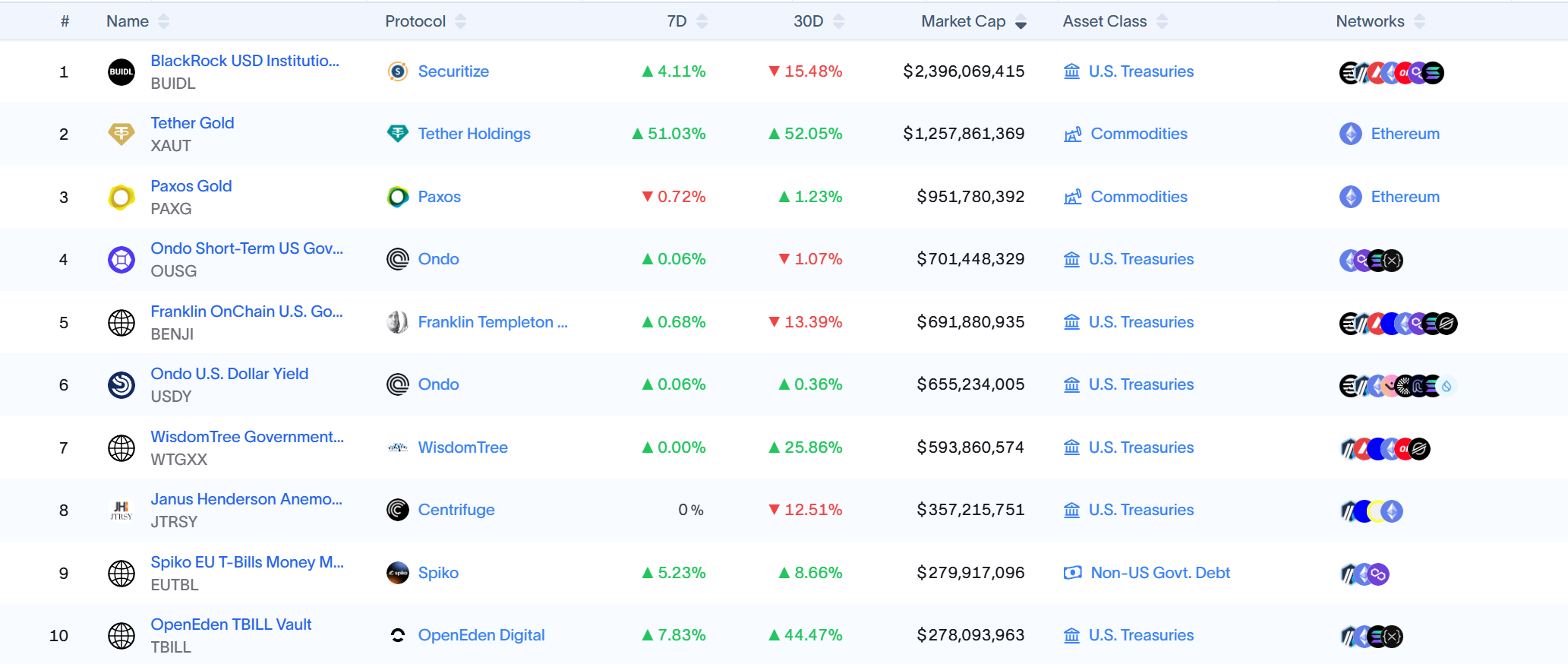

First is Ondo Finance, the leading project in the RWA tokenization space. Initially positioned as a platform for tokenizing bonds and U.S. Treasuries, Ondo Finance continues to hold a top-ten position by volume in the RWA sector, driven by its two flagship products USDY and OUSG backed by U.S. Treasury bonds, as of the time of writing.

Source: rwa.xyz

However, starting last year, Ondo Finance has expanded into the stock market by partnering with regulated custody and clearing institutions such as Anchorage Digital to securely custody real U.S. stocks and issue equivalent tokenized assets on-chain. This model not only provides institutional investors with compliance assurance but also builds cross-asset liquidity pools on-chain, allowing tokenized stocks to be combined and traded with stablecoins and RWA bonds.

Last month, Ondo Finance announced plans with Pantera Capital to launch a $250 million fund to support RWA projects. Ondo's Chief Strategy Officer Ian De Bode stated that the capital will be used to acquire equity and tokens in emerging projects.

Injective: A Blockchain Tailored for Financial RWA

Injective has always positioned itself as "financial infrastructure," being one of the high-performance blockchains dedicated to financial applications. Its proprietary on-chain matching engine and derivatives trading modules are specifically optimized for latency, throughput, and order book depth.

To date, the Injective ecosystem has aggregated over 200 projects spanning decentralized exchanges (Helix, DojoSwap), on-chain lending (Neptune), RWA platforms (Ondo, Mountain Protocol), and NFT marketplaces (Talis, Dagora).

In the RWA space, Injective’s strengths lie in two areas:

-

Broad asset coverage: Injective-based projects like Helix already support trading of various tokenized assets including U.S. tech stocks, gold, and foreign exchange, expanding the spectrum of RWA assets on-chain;

-

Direct integration with traditional finance: Injective has partnered with major financial institutions such as Coinbase, Circle, Fireblocks, WisdomTree, and Galaxy, establishing end-to-end workflows from off-chain custody and clearing to on-chain mapping and trading;

Thanks to this positioning, Injective functions more like a dedicated blockchain foundation for RWA—providing issuers with stable, compliant channels for asset management, offering trading platforms and aggregation tools a fast and low-cost execution environment, and laying the groundwork for future derivative and composite use cases of stock tokenization.

Source:Injective

MyStonks: Pioneer of On-Chain U.S. Stock Liquidity

As a pioneer in this wave of U.S. stock tokenization, many users have likely encountered MyStonks’ tokenized U.S. stocks on-chain. It partners with Fidelity to ensure that on-chain tokens are fully backed by real shares.

In terms of trading experience, MyStonks uses a Payment for Order Flow (PFOF) mechanism, routing orders to professional market makers for execution, significantly reducing slippage and transaction costs while improving speed and depth. For ordinary users, this means enjoying liquidity close to traditional brokers while retaining the benefits of 24/7 trading.

Notably, MyStonks is not limiting itself to on-chain spot trading. It is actively expanding into derivatives, lending, staking, and other diversified financial services. In the future, users won’t just be able to leverage-trade tokenized U.S. stocks—they’ll also be able to use their holdings as collateral to obtain stablecoin liquidity, or participate in portfolio investment and yield optimization strategies.

Backed Finance: Compliance-Oriented Cross-Market Expansion

Unlike MyStonks’ focus on U.S. stocks, Backed Finance adopted a broader, cross-market and multi-asset vision from the start. One highlight is its strong alignment with Europe’s MiCA regulatory framework.

The team operates under Swiss legal frameworks and strictly complies with local financial regulations when issuing fully backed tokenized securities on-chain. It has established a share purchase and custody system with partners like Alpaca Securities LLC, ensuring a 1:1 mapping between on-chain tokens and off-chain assets.

In terms of asset scope, Backed Finance supports not only U.S. stock tokenization but also ETFs, European securities, and specific international index products, offering global investors diversified options across markets, currencies, and assets. This means investors can configure portfolios of U.S. tech stocks, European blue chips, and global commodity ETFs on a single on-chain platform, breaking down geographical and temporal barriers of traditional markets.

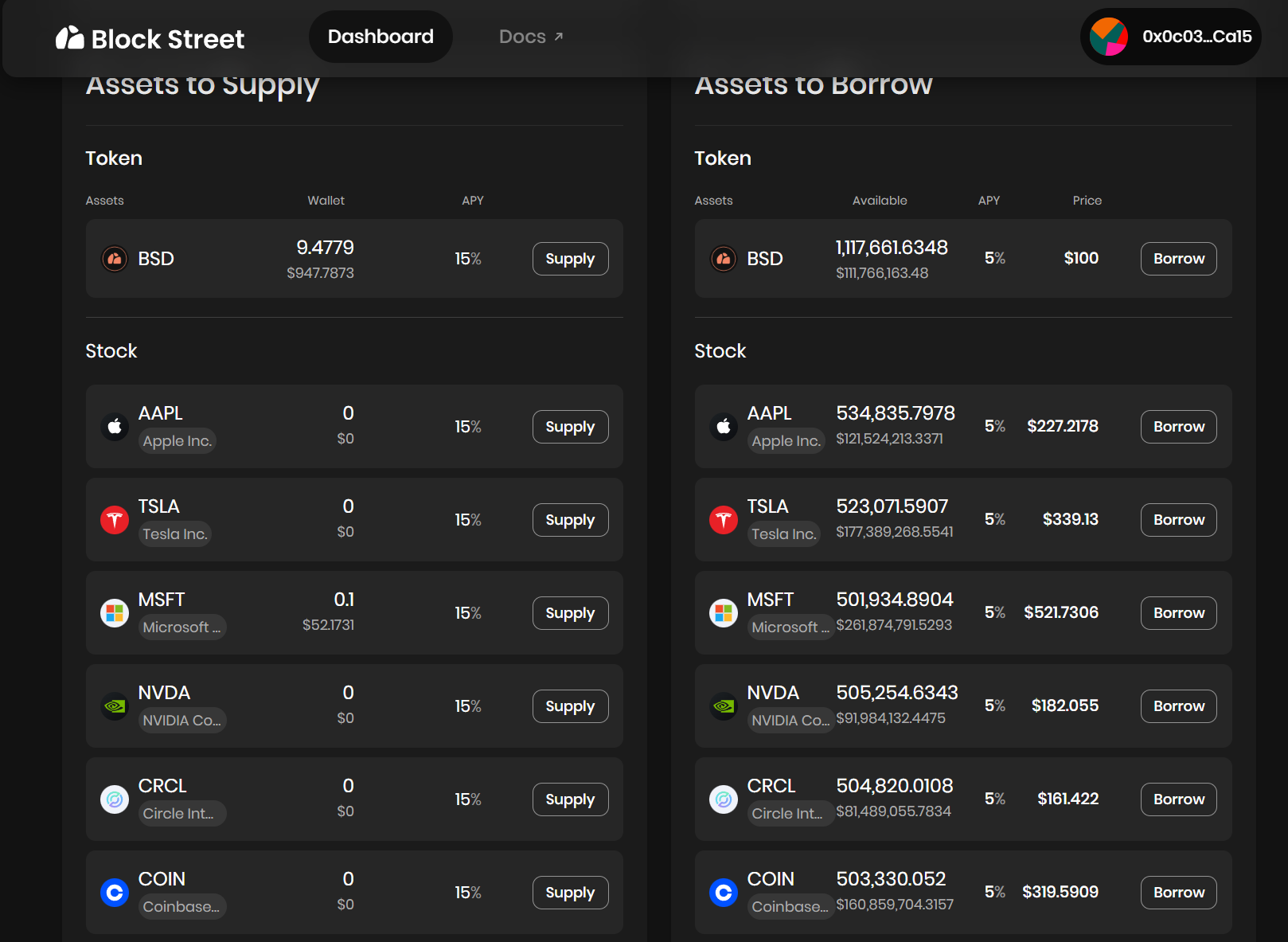

Block Street: Unlocking Liquidity for Tokenized Stocks

Block Street, one of the few DeFi protocols currently focused exclusively on tokenized stock lending, targets a downstream yet highly promising direction: liquidity unlocking.

This is a largely untapped niche within the "trading layer" of tokenized stocks. Take Block Street as an example—it offers direct on-chain collateralization and lending services to holders: users can deposit tokenized U.S. stocks like TSLA.M and CRCL.M as collateral and receive stablecoins or other liquid on-chain assets based on loan-to-value ratios, enabling a "keep assets, unlock liquidity" capital utilization model.

Block Street recently launched its test version, allowing users to convert tokenized stocks into usable capital without selling their positions. This fills a gap in the DeFi lending space for tokenized stocks and raises the question of whether similar lending, futures, and other derivative offerings might create a "second curve" for the tokenized stock market.

Source:Block Street

III. How Can We Further Tear Down the Walls?

Objectively speaking, the biggest advancement of this new wave of U.S. stock tokenization is the "real-share custody" model combined with lowered entry barriers:

Any user needs only download a crypto wallet and hold stablecoins to bypass account opening requirements and identity verification via DEXs, buying U.S. stock assets anytime, anywhere—no U.S. brokerage account, no time zone differences, no geographical or identity restrictions.

Yet the problem remains that most current products are still limited to the initial stages of issuance and trading, effectively remaining at the level of digital certificates, failing to transform them into widely usable on-chain financial assets for trading, hedging, and capital management. This creates a clear shortfall in attracting professional traders, high-frequency capital, and institutional participation.

This situation resembles ETH before DeFi Summer—back when it couldn't be lent out, used as collateral, or integrated into DeFi protocols. Only after protocols like Aave introduced "collateralized lending" did ETH unleash trillions in liquidity. Similarly, tokenized stocks must follow this logic—turning dormant tokens into "collateralizable, tradable, composable live assets" to break through current limitations.

Therefore, if the first curve of the tokenized U.S. stock market is growth in trading volume, the next curve will be increasing capital efficiency and on-chain activity through expanded financial tools. Only with such product evolution can the market attract broader on-chain capital flows and form a complete capital market cycle.

Under this logic, beyond instant buying and selling, richer derivative trading at the "trading layer" becomes especially critical—whether it's DeFi lending protocols like Block Street, or future shorting tools, options, and structured products that enable reverse positions and risk hedging.

The key lies in who can first build highly composable, liquid products—who can offer an integrated on-chain experience combining "spot + shorting + leverage + hedging." For instance, allowing tokenized U.S. stocks to serve as collateral for loans on Block Street, act as hedging instruments in options protocols, or form part of a combinable asset basket in stablecoin systems.

Overall, the significance of stock tokenization goes beyond simply moving U.S. stocks and ETFs onto the blockchain—it opens the "last mile" between real-world capital markets and blockchain:

From Ondo at the issuance layer, to MyStonks and Backed Finance for trading and cross-market access, to Block Street for liquidity release, this sector is gradually building its foundational infrastructure and ecosystem closure.

The RWA arena was previously dominated by U.S. Treasuries and stablecoins. But as institutional capital accelerates its entry and on-chain trading infrastructure continues to improve, once tokenized U.S. stocks become composable, tradable, and collateralizable live assets, stock tokenization is poised to become the largest and most scalable asset category within the RWA landscape.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News