FXC Intelligence Report: The State of Stablecoin Cross-border Payments in 2025

TechFlow Selected TechFlow Selected

FXC Intelligence Report: The State of Stablecoin Cross-border Payments in 2025

The industry's foundation began in the field of cryptocurrency trading: that's where it started.

Author: FXC Intelligence

Translation: Will Awang

2025 is the "year zero" of stablecoin cross-border payments, with new announcements emerging almost daily and landmark regulatory documents formally ushering stablecoins into traditional financial endpoints. "We are reaching a tipping point where everyone realizes this is an upgraded payment technology—real businesses and practical use cases are emerging. It's not just crypto mania; it's real applications," said Chris Harmse, co-founder of enterprise-grade stablecoin infrastructure provider BVNK.

But enthusiasm also brings bubbles. Eric Barbier, founder of Triple-A, cautioned: "On LinkedIn and in conference rooms, stablecoins seem to be treated as a panacea—as if they could end world hunger, poverty, or cure cancer tomorrow. That's clearly going too far."

Stablecoins and blockchain technologies are evolving rapidly, reshaping the financial payments landscape and shifting business positioning accordingly. This 100-plus-page frontline market report from FXC Intelligence, *The State of Stablecoin in Cross Border Payments (The 2025 Industry Primer)*, is a valuable practical handbook for stablecoin payments, integrating FXC Intelligence’s cross-border payment data, extensive research, and insights from 14 industry experts.

Therefore, we have translated this document in full, aiming to provide the industry with a concise, solid, and actionable guide to stablecoin payments—including current usage, operational mechanisms, potential market size, application scenarios, challenges to overcome, opportunities, and future outlook.

The full text spans 27,000 words. Enjoy below.

1. The Stablecoin Ecosystem

Though still an emerging technology, stablecoins have made a leap from niche experiments to mainstream attention within just a few years.

"The past 18 months have seen particularly dramatic changes," noted Chris Mason, co-founder and CEO of B2B stablecoin payment firm Orbital. "Early adopters were often high-risk, high-growth players from emerging industries; now, the second wave has arrived—payment providers and traditional banks are collectively awakening."

Iana Dimitrova, CEO of OpenPayd (a fiat financial infrastructure provider), added: "This explosion didn’t happen overnight—it’s the culmination of over 15 years of trial and error. The market has finally reached consensus on the practical value of stablecoins, and the technology itself has reached a threshold for scalable commercialization."

The industry originated in cryptocurrency trading: that’s where it began. Soon after, we started exploring new use cases for stablecoins. — Nikhil Chandhok, Chief Product and Technology Officer, Circle

1.1 A Brief History of Stablecoins

Stablecoins emerged alongside the launch of cryptocurrencies in 2008: tokenized, decentralized, and immutable digital currencies running on blockchain-based distributed ledgers. Stablecoins first appeared alongside Bitcoin, introduced to the world in October 2008 by an anonymous researcher (pseudonym Satoshi Nakamoto) who published a paper titled "Bitcoin: A Peer-to-Peer Electronic Cash System."

From the outset, Bitcoin was positioned as an online payment method without financial intermediaries. Though early adopters conducted limited payment experiments, it gained popularity among internet natives and tech-savvy individuals using cryptocurrencies for speculation. As interest in Bitcoin grew over subsequent years, some began exploring its underlying technology for cross-border payments. However, due to extreme price volatility, lack of regulation, and associations with black-market activities, many struggled to see it as a viable payment technology.

This changed with the advent of stablecoins: a pivotal moment in blockchain development, marking our transition from the early internet era into the modern digital age. Stablecoins are like the emergence of Napster, the P2P music file-sharing platform. — Teymour Farman-Farmaian, Co-Founder & CEO of Higlobe, a company providing dollar-denominated receiving accounts for businesses in emerging markets

The first cryptocurrency issued in stablecoin form was BitUSD, which introduced the concept of pegging one-to-one to fiat currency (specifically the US dollar) in 2014. However, since it was backed by other cryptocurrencies, it did not fully meet today’s definition of a stablecoin.

Other companies quickly followed, but it was Tether that truly introduced the concept of fiat-backed reserves, launching USDT later that year. Over the next few years, USDT steadily gained popularity and attention, though it faced scrutiny over transparency and regulation—eventually prompting Tether to take significant steps to address these issues.

In the early days of stablecoin development, developers were gradually understanding what stablecoins meant and how to use them. In 2018, more regulated stablecoins emerged: Paxos launched what is now known as Pax Dollar (USDP), while Circle, through a partnership with Coinbase, introduced USD Coin (USDC). These regulated, US-based stablecoins became increasingly popular—not only within the crypto space but also attracting interest from mainstream finance. At the same time, participants building financial infrastructure around stablecoins began to emerge, including Fireblocks in 2018 and BVNK in 2021.

However, 2022 and early 2023 saw a major crisis of confidence in stablecoins, triggered by several shocking industry events. First was the sudden collapse of TerraUSD (UST)—an unconventional algorithmic stablecoin whose backing mechanism relied on algorithms rather than cash reserves. When its value fell sharply from its $1 peg, panic-driven trading caused a “death spiral” that briefly affected the value of other stablecoins on major exchanges. Although UST wasn't a traditional stablecoin and companies like Circle, Paxos, and others sought to distance themselves from algorithmic models, the reputational damage to the broader industry was significant.

Despite claims by many participants that their reserves protected them from such risks, the failure of Silicon Valley Bank (SVB) in early 2023 raised new concerns. At the time of collapse, Circle held about $3.3 billion in deposits at SVB, creating initial uncertainty about whether those funds would be secured. This triggered a so-called “shadow run,” as holders feared they couldn’t redeem the stablecoin at a 1:1 rate, causing its trading value to drop to historic lows. While the US government ultimately guaranteed SVB’s reserves and Circle never faced actual redemption risk, the reputational harm was severe—especially for institutions requiring US-resident reserves and strong backing.

During this crisis, overseas adoption of USDT continued to rise, while the circulating supply of USDC in the US steadily declined throughout 2023. From the ashes of this turmoil, a leaner, more robust version of the industry slowly began to emerge. Driven by real demand across key channels and verticals, infrastructure providers saw rising transaction volumes and adoption rates, improving their products accordingly; others launched offerings focused on the true utility of the technology. In late 2023, PayPal launched PayPal USD (PYUSD), delivering a crucial vote of confidence in the sector; meanwhile, other firms worked to educate uncertain stakeholders, build regulatory frameworks, and boost adoption. "Education has been tough, but people are really starting to understand it," said Orbital CEO Mason.

Starting in early 2024, the circulating supply of USDC rebounded, and new payment-focused issuances continued to grow. More recently, Trump’s return to the US presidency has increased institutional support for the technology, accompanied by regulatory measures such as the GENIUS Act.

Since the change in US administration, major financial institutions have increasingly approached companies like ours seeking guidance on where and with whom they can partner to conduct stablecoin operations compliantly. — Guillaume C, EMEA Business Development Director, Paxos, a stablecoin issuer

Today, as adoption rapidly accelerates, the cross-border payments industry shows growing interest, with further growth potential ahead—but the fundamental principles of stablecoins largely align with the premises initially set out by Satoshi Nakamoto in the Bitcoin whitepaper.

We're solving the problem of cash on the internet. — Nikhil Chandhok, Chief Product and Technology Officer, Circle

1.2 Growing Interest in Stablecoins for Cross-Border Payments

As stablecoin technology advances, its use cases in cross-border payments are expanding. As Paxos’s Kendall explains, although stablecoin usage remains primarily concentrated in "crypto-native activities," interest in this area is growing, driven largely by end-user needs.

The evolution of stablecoins began in trading and investment, then gradually took root in cross-border payments during 2022 and 2023. — Michael Shaulov, Co-Founder & CEO, Fireblocks, a digital asset infrastructure provider

This experience is reflected across many firms in the space, including Conduit, which focuses on B2B inter-company payments. However, over the past one to two years, the situation has begun to shift.

Initially, mainly crypto-native payment companies helped their end clients move funds between channels more efficiently. Now, I’ve seen a major shift: many companies—especially large multinationals—are entering the space. They want to understand how to use stablecoins, particularly in challenging regions like Africa, Latin America, and Asia. — Kirill Gertman, Founder & CEO, Conduit, a B2B stablecoin payments company

This has prompted some previously fiat-focused cross-border payment infrastructure providers to enter the market, such as OpenPayd, which added stablecoin functionality earlier this year.

"For us, this evolution felt entirely natural," said OpenPayd’s Dimitrova. "We already had existing customers using our platform for cross-border fiat payments who came to us saying, 'We’re already accepting stablecoin payments via other providers. Can you integrate these assets onto your platform?'" Over the past 18 months, we’ve consistently received such requests. We realized that without offering interoperability, we wouldn’t meet the growing needs of these customers.

Such requests primarily come from enterprises with global trade demands, but stablecoin adoption is also increasing across other areas of cross-border payments, including MoneyGram, which has begun offering stablecoin payment capabilities. In 2022, MoneyGram started sending remittances in USDC, subsequently expanding its capabilities in the field—including launching MoneyGram Ramps, a white-label solution for digital wallet on- and off-ramping, and fulfilling its own cross-border treasury management needs.

MoneyGram is a fintech company with a global digital and cash network. Stablecoins will play a very important role in MoneyGram’s future. They benefit every aspect of our business—from B2B backends to B2C service delivery and how we serve consumers. — Anthony Soohoo, Chairman & CEO, MoneyGram

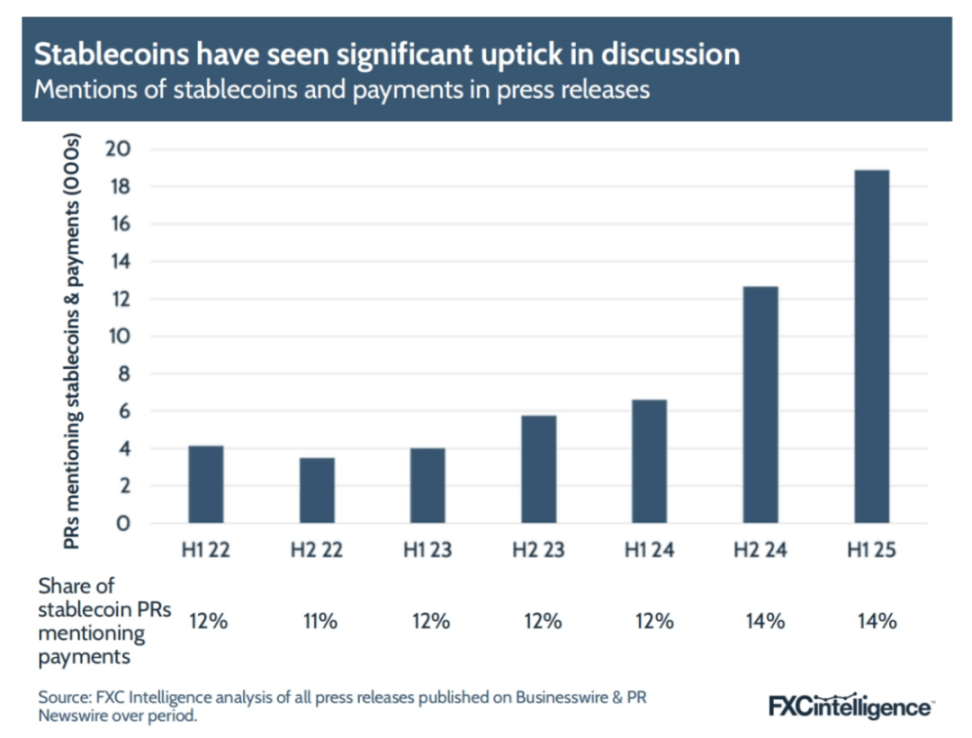

Today, although stablecoins represent a small share of the market, attention toward them has clearly risen. In the first half of 2025, press releases related to stablecoins and payments increased by 186% compared to the same period last year—a faster pace than overall stablecoin-related news. Press releases specifically mentioning both cross-border payments and stablecoins surged by over 1,000%. And that’s just among companies publicly launching stablecoin solutions.

According to BVNK’s Harmse, most companies in the payments industry see the opportunity presented by this technology—even if they haven’t yet spoken publicly about it. "I think 95% of companies see this," he said. "Judging from our ongoing conversations and potential partnerships, many traditional payment firms are actively investing—some even ones you wouldn’t expect."

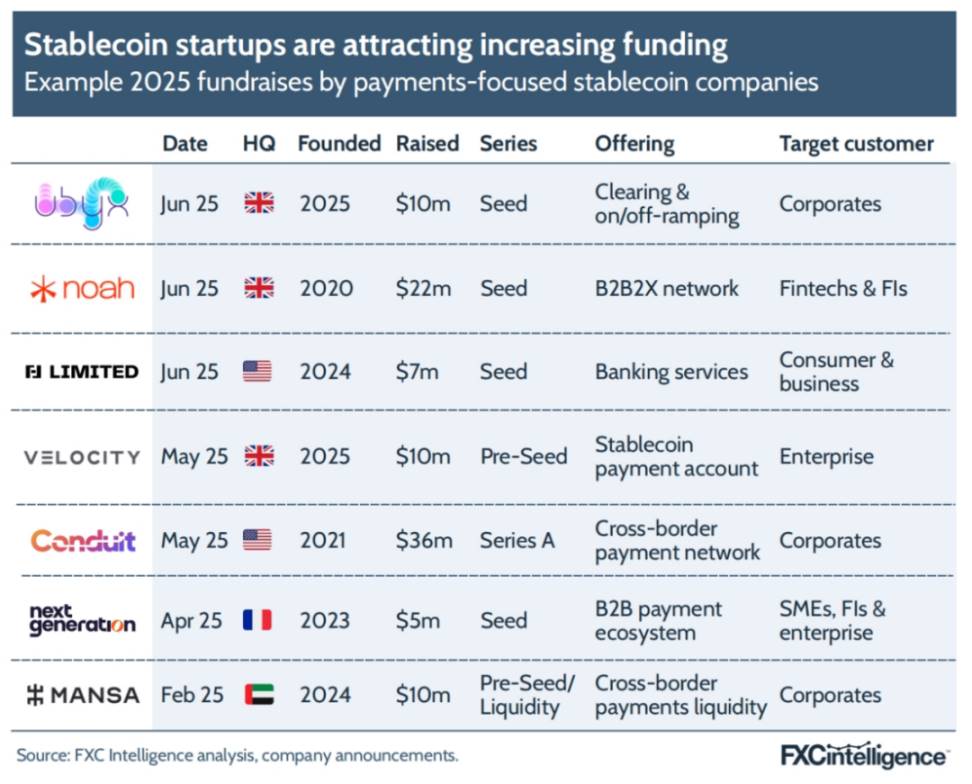

1.3 Surge in Stablecoin Payment Investment

Beyond rising corporate interest, capital continues to flow in. Despite a cooling venture capital environment overall, the stablecoin sector keeps attracting funding, with numerous projects announcing raises over the past year.

"Investors are first looking at the return potential," said Conduit’s Gertman. "When they see our revenue growth trajectory and rapid volume increase, they believe we have a chance to capture a much larger market than today." The company closed a $36 million Series A round in May this year.

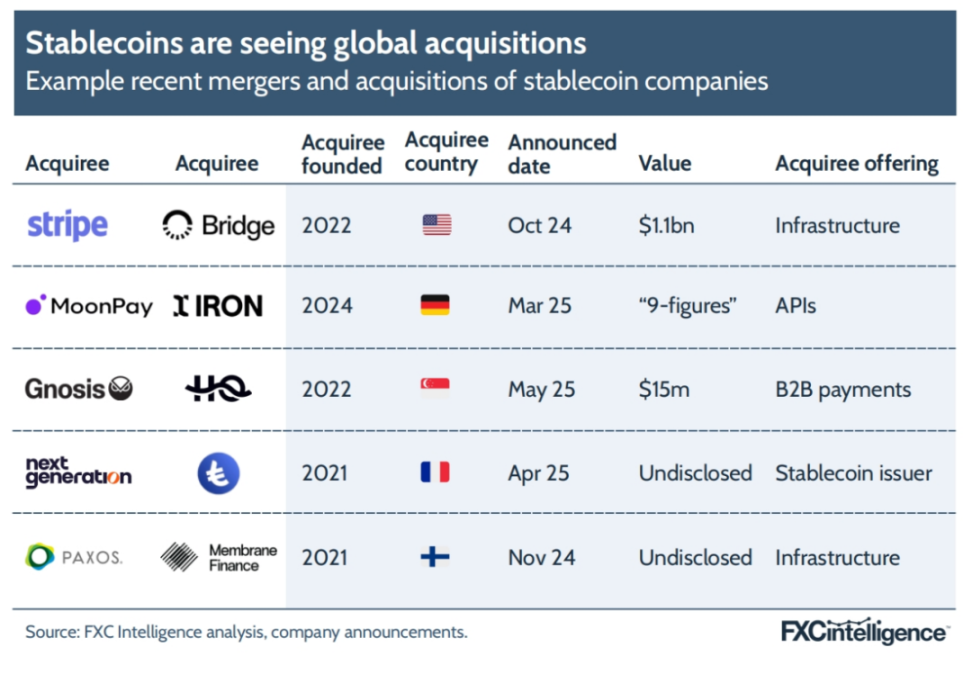

Meanwhile, a series of acquisitions are accelerating: traditional giants aim to quickly acquire capabilities in this space. Despite frequent moves, Stripe’s announcement in 2024 and completion in early 2025 of acquiring stablecoin infrastructure company Bridge is widely seen as a catalyst for the entire industry taking the technology seriously.

"It forced everyone to re-evaluate this space," said BVNK’s Harmse. "We were already talking with multiple top global payment firms, and this acquisition accelerated those discussions several-fold."

For Airwallex co-founder and CEO Jack Zhang, Stripe’s move carried deeper implications: "Stripe is a master storyteller. With this acquisition, they crafted a super brand narrative, putting stablecoins squarely in the spotlight—and arguably fueling today’s stablecoin boom."

2. Current State of Stablecoin Cross-Border Payments

The underlying logic of stablecoin payments is simple: theoretically, they outperform current mainstream solutions across multiple dimensions—speed, reliability, and transparency. Although costs (particularly on- and off-ramp pricing) still need optimization, this depends on further liquidity improvements.

Yet reality isn’t all rosy. Despite growing success stories, stablecoin payments face complex hurdles in implementation; the overall scale of payment scenarios remains small, leaving certain capabilities still under validation.

The key to truly understanding stablecoin potential lies in returning to the user perspective—customers don’t care about the term "stablecoin." Users don’t care what coin you use. What they always care about is three things: security, speed, and best price—unchanged for three thousand years. — Farman-Farmaian, Higlobe

Thus, the real value of stablecoins lies in scenarios where they can "tangibly and reliably improve existing payment experiences." At least currently, such improvements are most concentrated in emerging markets.

"Anytime cross-border elements are involved in a payment, stablecoins shine." — Chris Harmse, BVNK Co-Founder & Chief Commercial Officer

2.1 Emerging Markets: The Main Battlefield for Stablecoins

Whether early bettors on stablecoins or recent entrants, opinions are strikingly aligned: in countries with weak traditional payment systems, stablecoins aren’t just the "best available option right now"—they are the driving force behind the entire "stablecoin cross-border payments" sector.

"Global e-commerce platforms have long felt the pain of collecting, disbursing, and holding funds in countries with poor infrastructure. They’ve quietly sought alternatives in the background—only now are traditional financial institutions catching up," said OpenPayd’s Dimitrova.

The pain points extend beyond simply wanting cheap and fast fund transfers. They include: 1) enterprises unable to access internationally usable payment tools; 2) institutions and individuals trapped in volatile local currencies.

Some agent merchants can’t even open bank accounts—we give them a B2B wallet and settle in stablecoins. — Luke Tuttle, Chief Product & Technology Officer, MoneyGram

However, demand in emerging markets isn’t monolithic—explosive growth in one scenario spawns others, expanding outward layer by layer. One thing is clear: massive cross-border flows moving through "niche channels" have formed a sizable and growing market. Stablecoin players are flooding in, and customer profiles are becoming increasingly sophisticated.

"We’re serving an airline that needs to collect payments across multiple African countries and transfer them back to its European headquarters. Once they grasp the use case, they immediately pilot it," said Conduit’s Gertman.

Not only are clients "upgrading," but local partners are also becoming more professional. "We’ve now integrated 80–90 currency on- and off-ramp partners locally," said Orbital’s Mason. "Amid the stablecoin boom, partners in emerging markets are rapidly professionalizing."

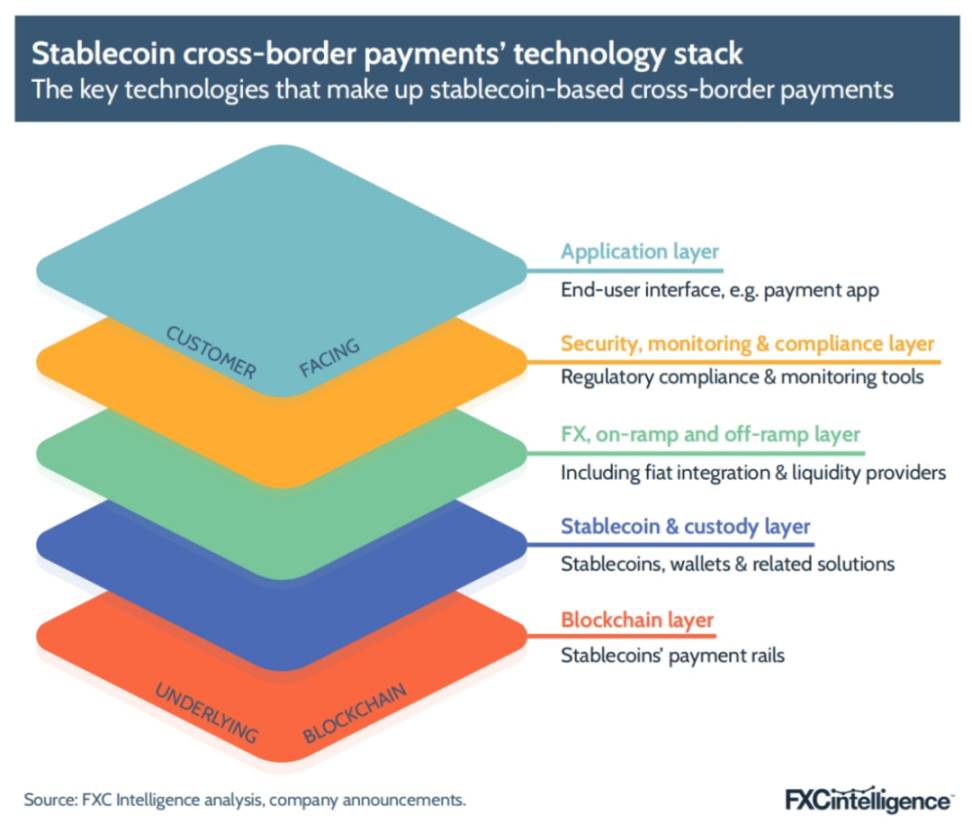

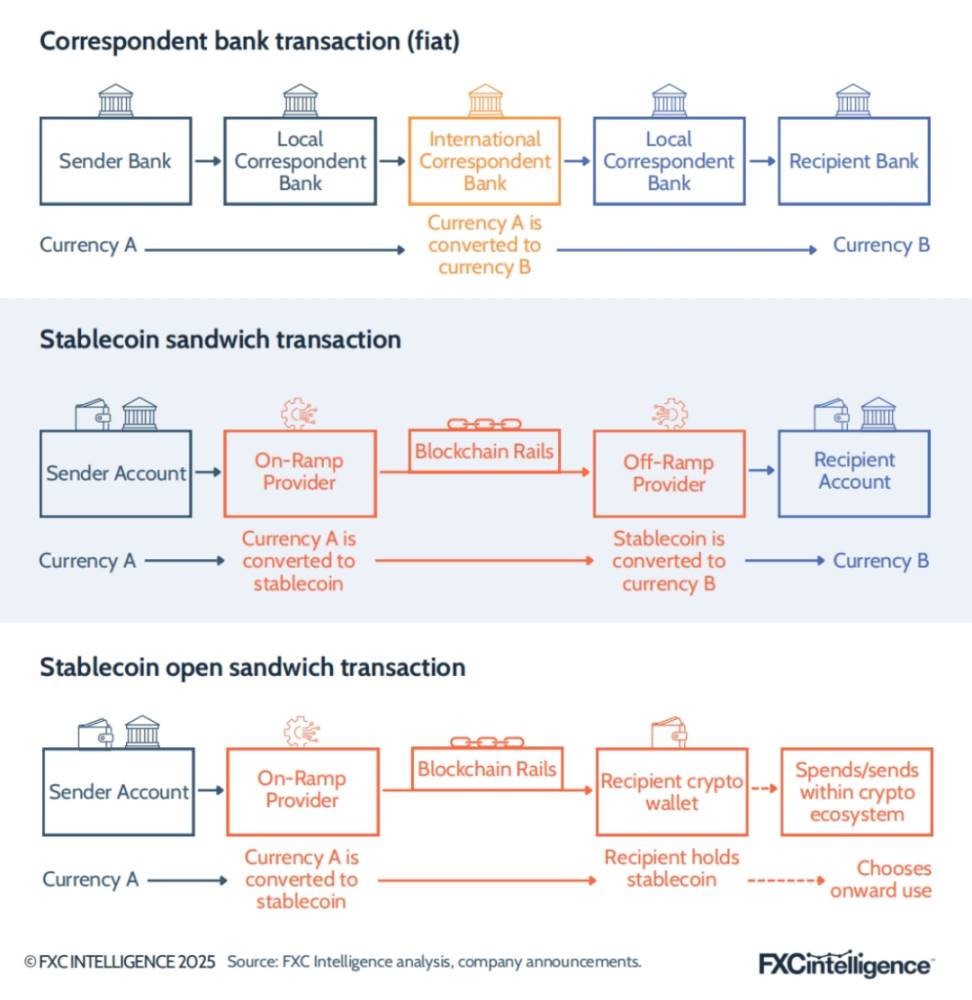

2.2 How Stablecoin Payments Work: The 'Stablecoin Sandwich' and Technical Architecture

In real-world payment flows, stablecoins are just one layer in the entire tech stack—you can imagine the whole architecture as a "sandwich," with stablecoins sandwiched in the middle and multiple layers above and below enabling cross-border value transfer.

At the custody layer, stablecoins move between different "wallets" operating on blockchain networks. Blockchains act as digital ledgers, forming the foundational "rails."

Above the custody layer sits the on/off-ramp layer, which enables seamless conversion between fiat and stablecoins—the core of foreign exchange, fiat onboarding, and payout solutions. Approaches vary significantly, often requiring integration with local banks. Liquidity pools are also needed to ensure users can instantly convert stablecoins into desired fiat currencies.

The compliance layer uses KYC/AML tools similar to those in fiat products, sometimes directly reusing existing systems.

The application layer includes the final user-facing apps, websites, APIs, and embedded interfaces that wrap all four layers together, reducing the experience of "instant cross-border payments" to a single click.

2.3 The 'Stablecoin Sandwich' Model

Despite variations in detail, the standard approach to stablecoin cross-border payments is commonly known as the "stablecoin sandwich," a term first coined in 2021 by Ran Goldi, Senior VP of Payments & Networks at Fireblocks.

In traditional correspondent banking models, cross-border payments must pass through a chain of local bank → international bank → recipient’s local bank, completing currency conversion en route. The "stablecoin sandwich" simplifies this process:

-

Convert sender-side fiat into stablecoins,

-

Transfer internationally via blockchain,

-

Convert stablecoins back into target fiat currency on the receiver side.

This approach is highly attractive in certain markets because it drastically reduces the complexity of the correspondent banking system.

Mason of Orbital illustrated: "In a traditional payment path, sending money to an emerging market might involve six institutions. Suppose my correspondent bank is Sberbank, underneath which is J.P. Morgan—that’s already three banks with regulatory obligations. On the receiving end, there may be three more. Since the destination is Colombia, each institution demands visibility into the payment, and with differing business hours, funds might sit in the system for two weeks before the recipient gets paid."

When payments are for perishable goods or time-sensitive services, such delays are especially fatal, creating unnecessary friction for local businesses, limiting their growth, and hindering internationalization. The "stablecoin sandwich" eliminates this lengthy chain, though it still requires counterparties at both ends to be willing and able to swiftly complete fiat-stablecoin conversions. Initially a challenge, local demand for stablecoins has risen as awareness grows in multiple emerging markets, improving liquidity for such transactions.

"Although local banks in certain markets aren’t technologically advanced, we’re seeing enhanced capability for executable 'stablecoin sandwiches'," Mason added. "For example, someone sends me euros—I instantly buy USDT from a European liquidity provider, then sell USDT in real-time in Mexico and disburse Mexican pesos through my Mexican banking partner. The entire process can be completed in 5–10 minutes or less. To me, this is the golden goose of cross-border payments. It still depends on emerging market capacity, but everyone is catching up fast."

The feasibility of fast, low-cost stablecoin payments hinges critically on the efficiency of the "on/off-ramp currency conversion" step—with the "last mile" being especially critical. This means institutions deeply rooted in the fiat world are better positioned to pivot into this space.

We come from traditional finance and already have the "first and last mile" fiat rails in place—these remain essential parts of the process. Now we just need to introduce new technology in the middle to make payments faster and leaner. — Dimitrova, OpenPayd

However, the last mile isn’t always necessary. As stablecoin use expands, more people want to receive stablecoins directly instead of converting back to fiat. Fireblocks’ Shaulov revealed: "We’re already seeing one side of the sandwich disappear." These transactions are called "open stablecoin sandwiches," and some believe they’ll eventually dominate.

Mike Hudack, Co-Founder & CEO of Sling Money (a consumer-focused stablecoin remittance company), stated bluntly: "People need to gradually accept a reality: one day, no one will on-ramp or off-ramp anymore—the money on-chain will be the money itself. No one will care about the backend—your Visa debit card will actually be powered by stablecoins or tokenized deposits in your wallet."

But when that day will arrive remains uncertain. While demand for "open sandwiches" exists in certain scenarios, most believe the first- and last-mile fiat rails won’t disappear from the market for several years.

Dimitrova summed up: "Interoperability between fiat and stablecoins will remain necessary for the coming years."

3. Opportunities Revealed in Data

Quantifying the current market size of stablecoin cross-border payments is difficult: while total stablecoin transaction volume across blockchains is publicly available, the portion used specifically for cross-border payments is unclear.

Data from Visa and Allium shows that in 2024, total stablecoin transaction volume across all blockchains reached approximately $5.7 trillion across 1.3 billion transactions. In the first half of 2025 alone, volume reached about $4.6 trillion with 1 billion transactions—projected annual figures expected to significantly exceed last year’s. However, the vast majority of these transactions occur in trading contexts, where investors use stablecoins as a "stable parking spot" between volatile crypto trades.

Internal data from leading firms better reflects the size of niche markets. According to Harmse, BVNK (considered one of the largest players in the space) processes around $15 billion annually, about half of which comes from B2B payments—the largest segment in cross-border payments. Gertman said Conduit handles $10 billion in annualized volume, estimating this represents about 20% of the global B2B stablecoin cross-border payment market; Orbital reported an annualized scale of $12 billion.

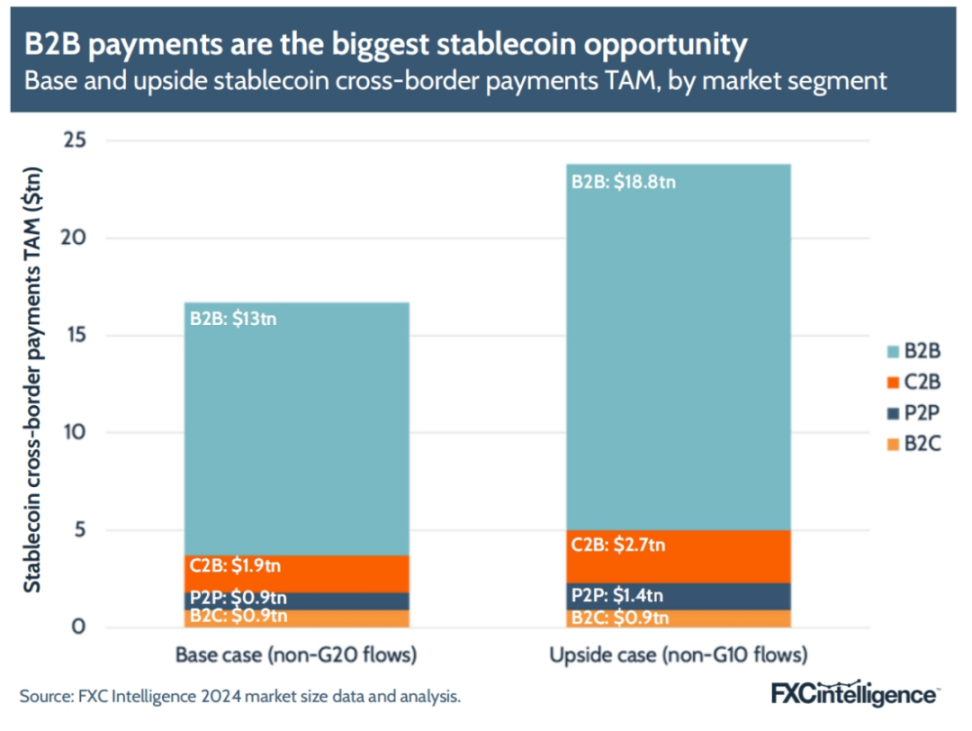

3.1 Addressable Market (TAM) for Stablecoin Cross-Border Payments

Previous data from FXC Intelligence showed that in 2024, the total size of global cross-border payments (including wholesale) was approximately $194.8 trillion, with non-wholesale accounting for $40 trillion. Currently, the actual scale of stablecoins in cross-border payments remains in the "billions of dollars" range, representing less than 1% of the overall market. But its addressable market (TAM) is far higher.

Kendall of Paxos pointed out: "The current total market cap of stablecoins is about $250 billion—that’s nothing. Once fully scaled, I believe it will result from collaborations between regulated firms like ours and trillion-dollar capital sources."

To define the addressable market for stablecoin cross-border payments, focus must center on the geographic regions where companies report fund flows: emerging markets. As Orbital’s Mason summarized: "The most profitable global segments lie precisely along three key funding corridors. On these routes, traditional transaction banks profit handsomely, charging opaque fees and slow settlement times—creating massive pain points:

-

From developed to emerging markets;

-

From emerging to developed markets;

-

Between emerging markets.

This opportunity is mirrored in Fireblocks’ own business footprint. Shaulov said the company primarily serves regional corridors including bidirectional flows between Latin America and the US/Europe; bidirectional flows between Africa and Europe/some US links; and traffic between Asia-Pacific and the US/Europe.

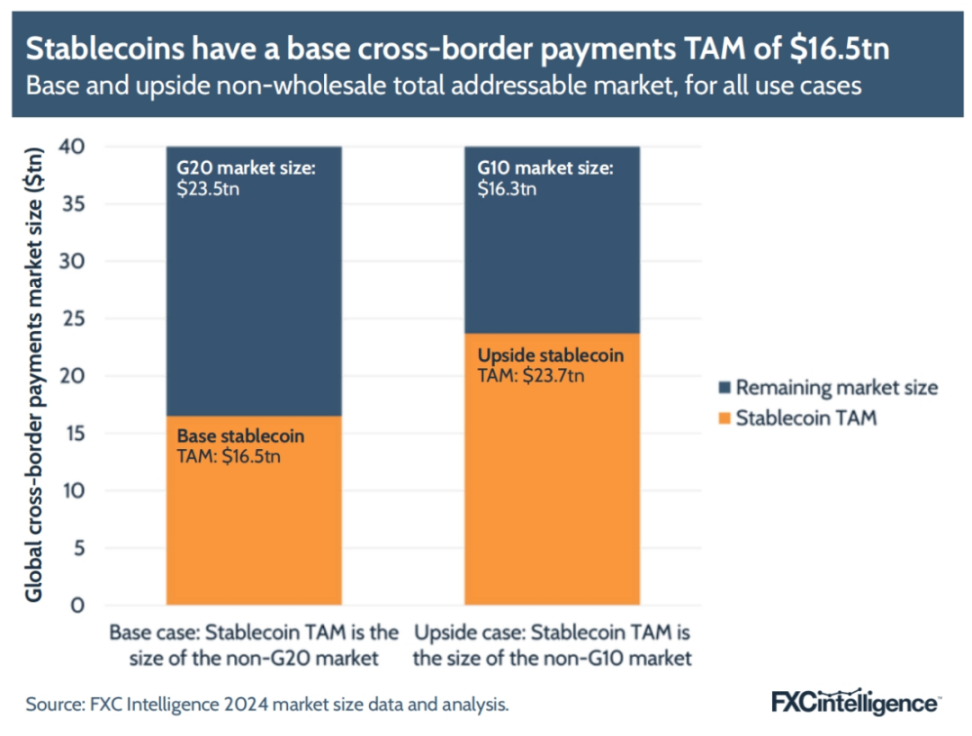

Based on this, a reasonable framework is to anchor the primary opportunity outside G20 markets, followed by markets outside the G10 (Belgium, Canada, France, Germany, Italy, Japan, Netherlands, Sweden, Switzerland, UK, and US).

Therefore, we define "non-G20 markets" as the base addressable market (base TAM) and "non-G10 markets" as the upside case. Under this framework, the base addressable market for stablecoin cross-border payments is currently $16.5 trillion, covering 41% of non-wholesale totals; the optimistic addressable market reaches $23.7 trillion, representing 59% of non-wholesale activity.

By细分场景, B2B remains the largest opportunity—an observation equally valid in fiat cross-border payments. However, differences between G10 and G20 lead to significant gaps between base and optimistic scenarios.

China, though part of the G20 but not the G10, is one of the main capital exporters, making it a key contributor to the optimistic scenario. Beyond China, several countries significantly raise the TAM in specific scenarios. For instance, the gap between base and optimistic scenarios is widest in C2C remittances, because the G10 excludes core C2C-exporting nations within the G20—besides China, these include Saudi Arabia, Russia, UAE, and India.

While emerging markets remain the primary addressable market today, this may not persist indefinitely. Some participants like BVNK have observed minor flows beginning to originate from other markets.

"We’ve noticed 'East-West' flows—for example, sending money from Hong Kong to the US can sometimes be difficult, even with relatively mature financial infrastructures in both locations," said BVNK’s Harmse. "Much of our volume actually comes from B2B payments between global enterprises, not necessarily involving emerging markets."

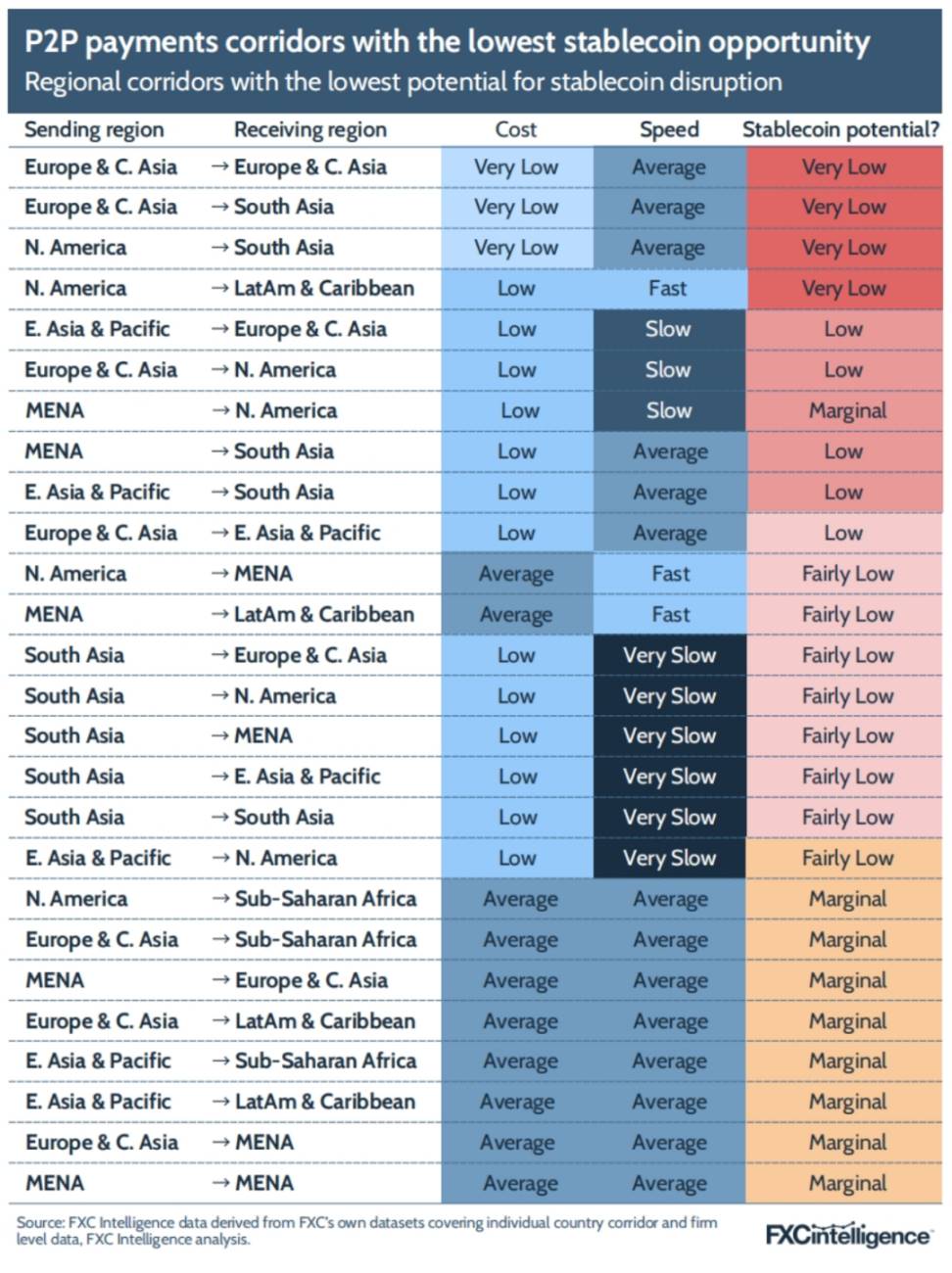

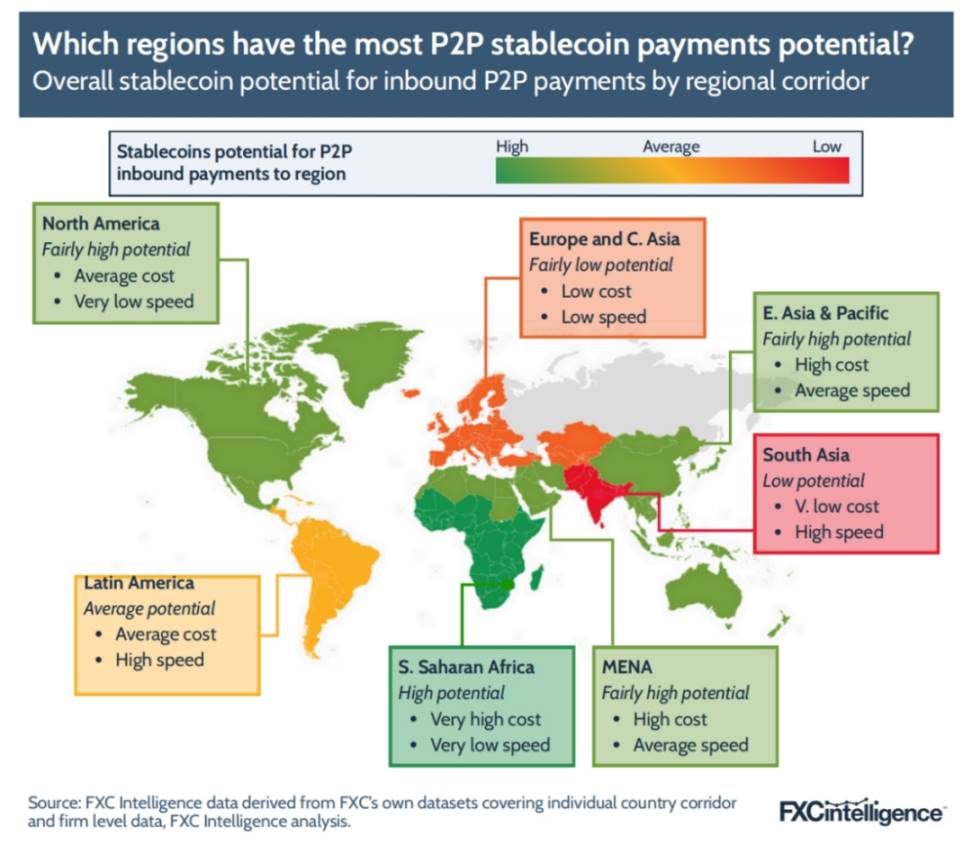

3.2 Regions with Highest Potential for C2C Stablecoin Payments

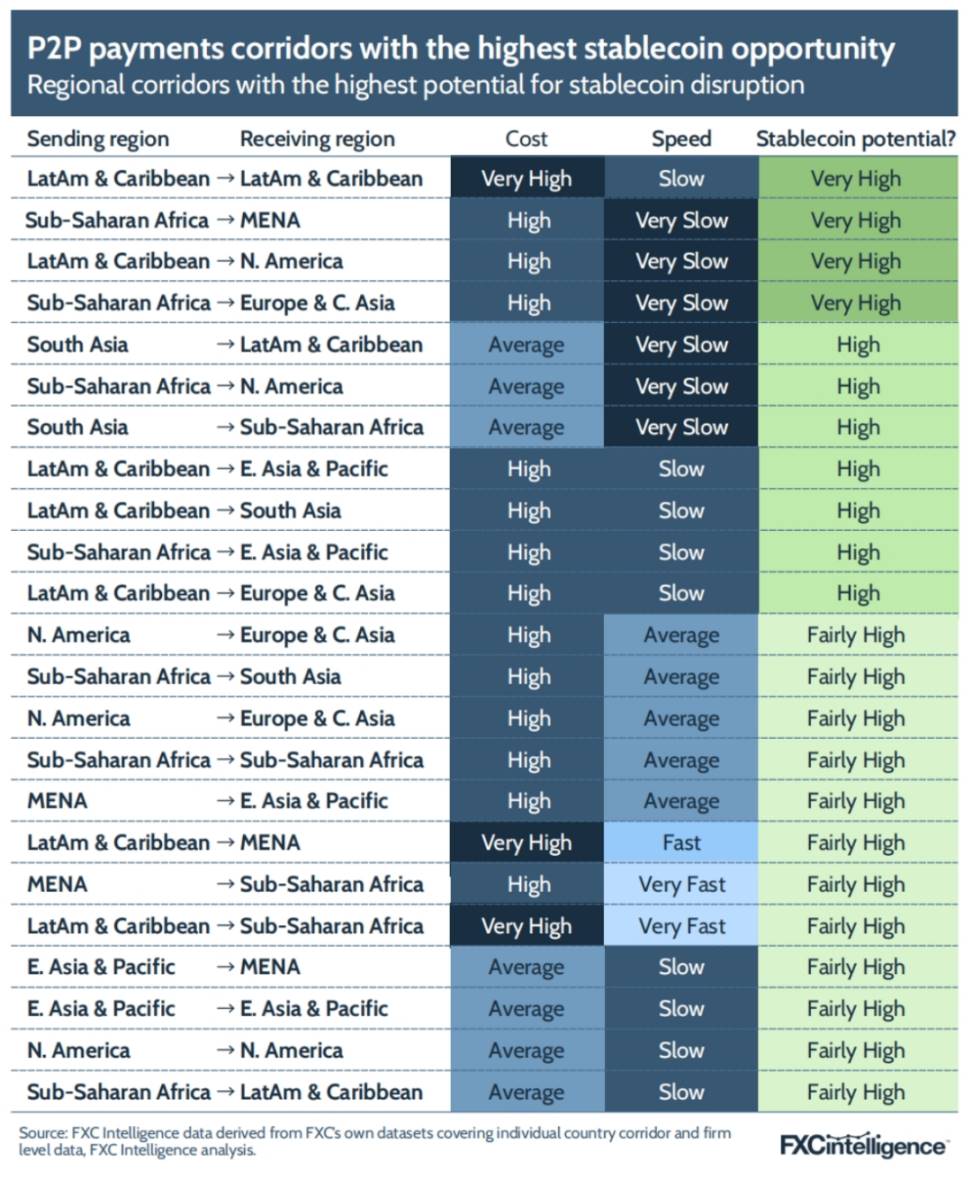

The global opportunity provides a rough outline, but breaking it down regionally reveals clearer focal points for stablecoin cross-border payments.

In providing retail pricing data for the Financial Stability Board’s (FSB) Annual Progress Report on Cross-Border Payments to monitor progress on the G20 roadmap, FXC Intelligence calculated average costs and speeds for different payment types across global regional corridors. By mapping price against speed, it becomes possible to identify which corridors offer the greatest opportunity for stablecoin payments.

In the C2C domain, the following regions stand out due to high average costs and slow average speeds:

-

Intra-Latin America and Caribbean remittances;

-

Sub-Saharan Africa → Middle East & North Africa (MENA);

-

Latin America & Caribbean → North America;

-

Sub-Saharan Africa → Europe & Central Asia.

However, some corridors currently show low potential for C2C stablecoin payments due to already low or very low costs and average or even fast speeds. These include intra-regional remittances within Europe & Central Asia, remittances from Europe & Central Asia to South Asia, and remittances from North America to South Asia or Latin America & the Caribbean.

Looking at global average inbound data, Sub-Saharan Africa as a whole shows the highest potential—extremely high average cost, extremely low average speed; South Asia, as a C2C remittance destination, shows lower potential.

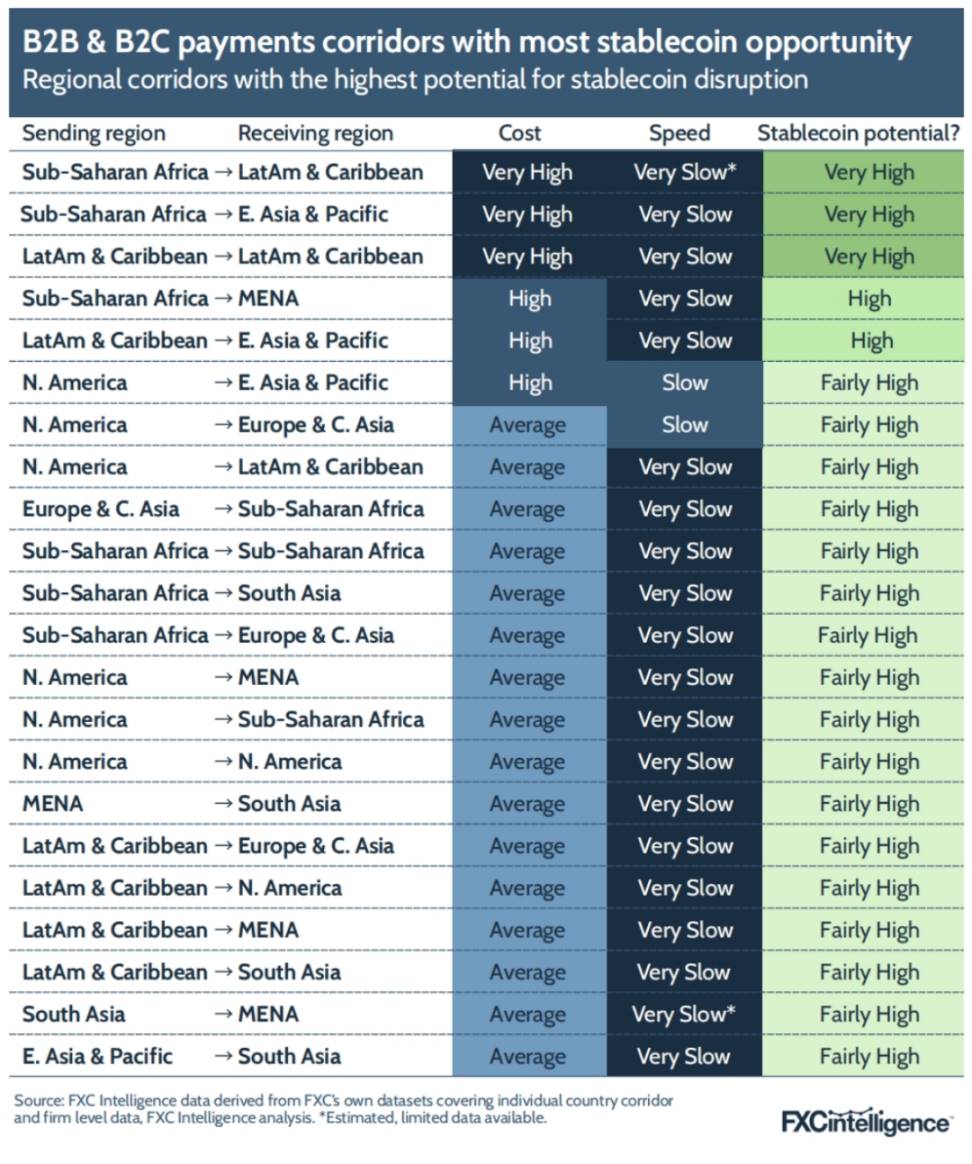

3.3 Regions with Highest Potential for B2B Stablecoin Payments

However, combining B2B and B2C payment data paints a slightly different picture—since specific corridors differ, costs and speeds can vary greatly. For cross-border payments, the regional corridors with the highest stablecoin potential include:

-

Sub-Saharan Africa → Latin America & Caribbean

-

Sub-Saharan Africa → East Asia & Pacific

-

Intra-Latin America & Caribbean corridors

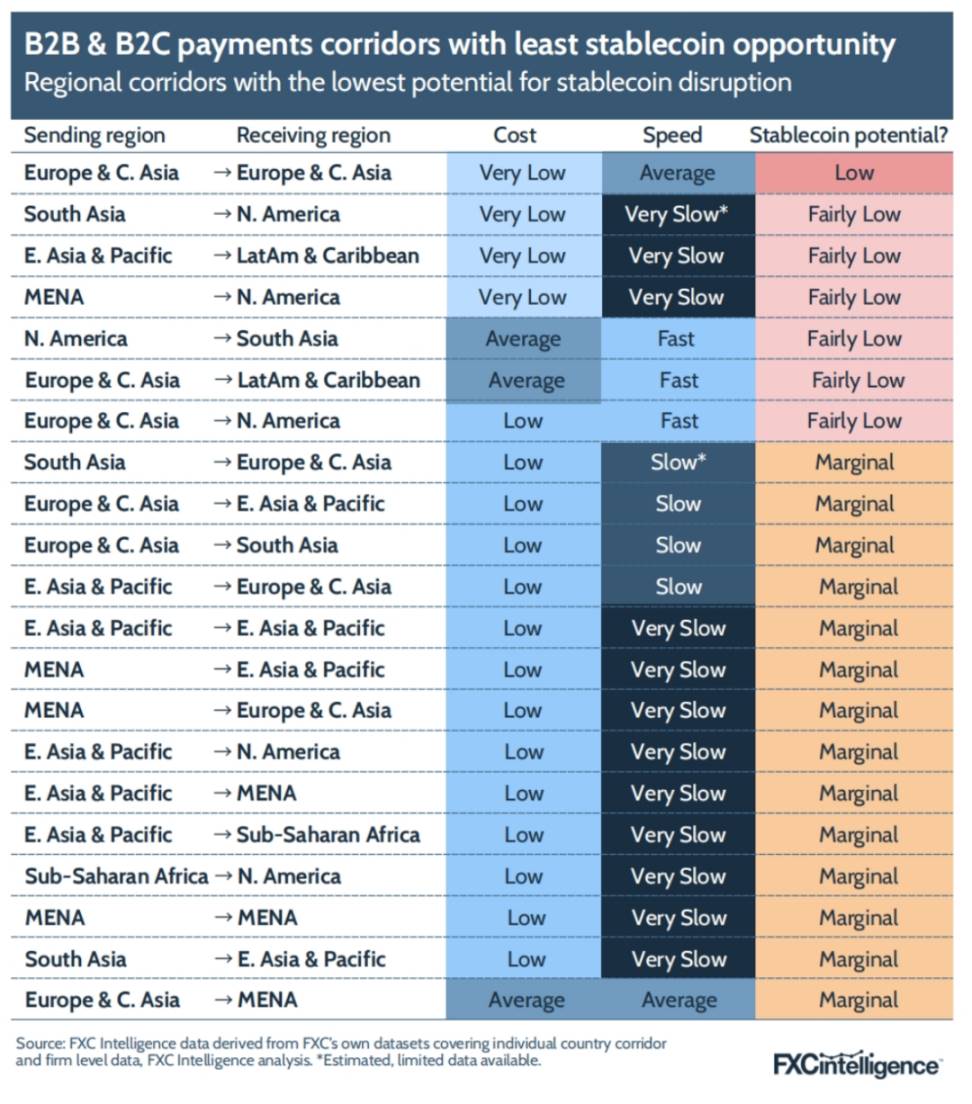

Meanwhile, a very few regional corridors show very low potential:

-

Intra-Europe & Central Asia payments, lowest opportunity;

-

South Asia ↔ North America payments;

-

East Asia & Pacific → Latin America & Caribbean payments;

-

Middle East & North Africa (MENA) → North America payments.

Globally, Europe and Central Asia show the lowest current potential as B2B and B2C cross-border stablecoin payment destinations, despite exceptions in individual countries. In contrast, East Asia and the Pacific, due to high costs and slow speeds, possess the highest average potential as receiving markets.

4. Major Stablecoins in the Market

Although numerous stablecoins are available to buy, hold, and trade, not all are suitable for cross-border payments. Reasons include design—nature of reserve assets, transparency levels—and liquidity—whether there are sufficient counterparties in various currencies—and whether they can be stably integrated into automated technical processes and readily converted into desired fiat currencies.

Only two things truly matter for stablecoins: liquidity—enough participants across various currencies—and API uptime. — Farman-Farmaian, Higlobe

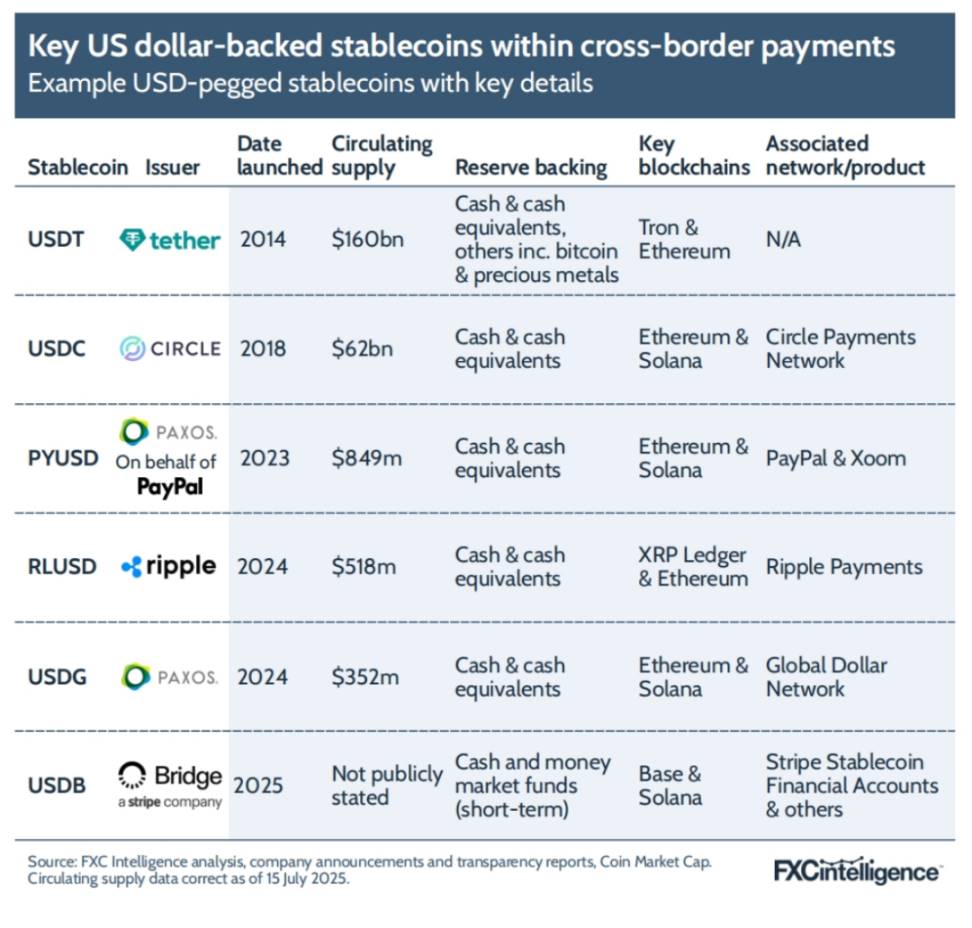

Different needs have led various entities to issue their own stablecoins. In cross-border payment-focused scenarios, the overwhelming majority are pegged to the US dollar. The most well-known are Tether’s USDT and Circle’s USDC, which dominate by market cap; there are also smaller-circulation coins that attract attention due to their issuers.

PayPal’s PYUSD is still small in scale but has shown steady growth by being usable across multiple PayPal products (including Xoom remittances and PayPal checkout). Ripple launched RLUSD last year, primarily for use on its own blockchain network, which long supported cross-border payments via the XRP crypto asset. The newest entrant is Global Dollar (USDG), issued in November by Paxos Singapore, designed to comply with multi-regional stablecoin regulations and serve as the core of its newly launched "Global Dollar Network" payment network. Stripe’s subsidiary Bridge also launched USDB, dedicated exclusively to its cross-border payment solution. Unlike others, USDB isn’t available to retail traders but serves solely as an internal settlement token within Bridge.

4.1 Which Stablecoins Dominate the Market?

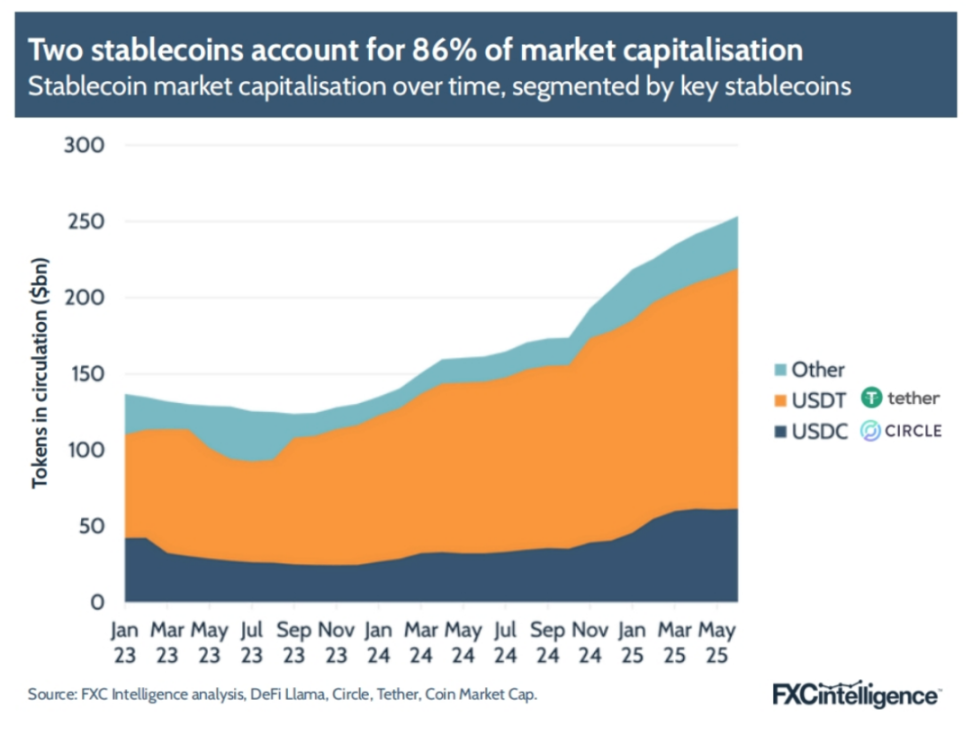

Even within payments, despite numerous options, USDT and USDC maintain absolute dominance, collectively accounting for over 80% of total market cap. USDT remains significantly larger in volume, making it the preferred choice for some service providers; USDC’s scale is also substantial enough to be the top choice for many compliant institutions.

Key differences exist in their reserve compositions, potentially raising concerns: USDT includes non-traditional assets like Bitcoin and precious metals in a small portion of its reserves; USDC’s reserves consist solely of cash and cash equivalents held in US domestic banks. Coupled with USDT’s reserves being held offshore and less frequent transparency reporting, some US financial institutions remain cautious. Nonetheless, most industry players don’t mind using USDT, and due to its massive circulation, it remains essential in certain scenarios.

"Personally, I believe Tether always has sufficient reserves to support USDT liquidity," said Orbital’s Mason.

4.2 Differences Across Blockchains

While stablecoins are the technological core, the blockchain "rail" they operate on is equally critical; varying chain capabilities directly affect their suitability for payment scenarios.

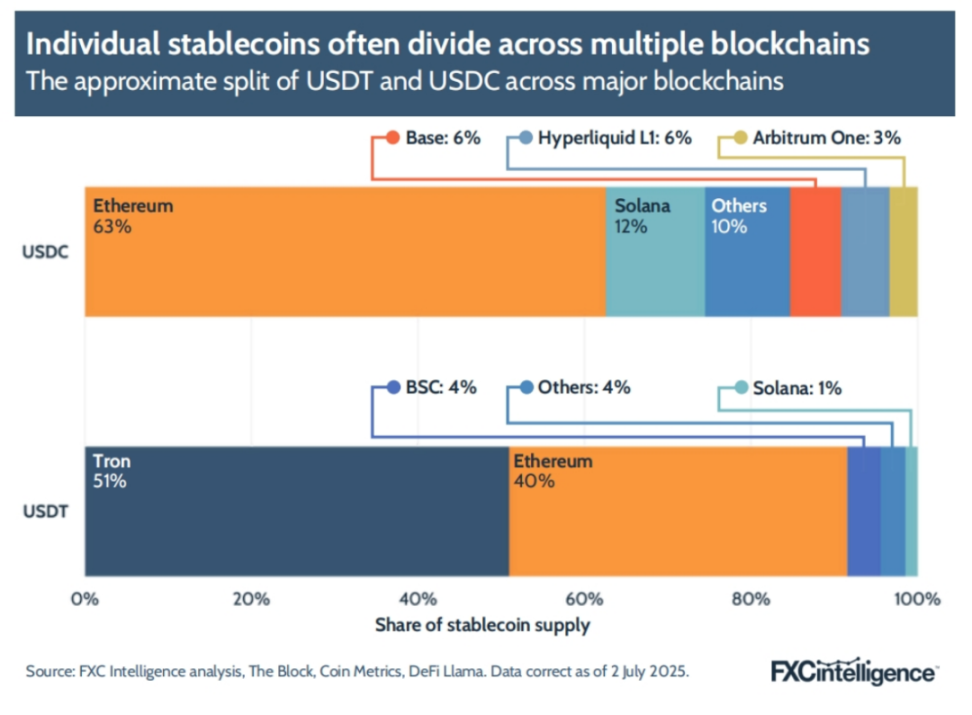

For Circle, USDC serves multiple purposes beyond cross-border payments, so the company actively promotes native issuance across as many chains as possible—currently spanning 23 chains. "We’ve built robust infrastructure to issue stablecoins on these chains and manage liquidity across them," said Circle’s Chandhok. Yet despite broad coverage, USDC circulation concentrates on a few chains: Ethereum accounts for 63%, followed by Solana at 12%.

USDT similarly favors Ethereum, with about 40% of its supply on that chain; although the proportion is lower than USDC’s, the larger total issuance means more actual USDT exists on Ethereum. However, USDT’s largest share is on TRON, at about 51%. Circle previously issued stablecoins on TRON but decided to exit in early 2024 due to regulatory and compliance concerns.

Although companies using specific stablecoins for cross-border payments aren’t automatically confined to a single blockchain, they often choose a limited number. Each blockchain requires separate integration into internal systems and operates under different technical standards; transferring stablecoins across multiple chains can introduce friction.

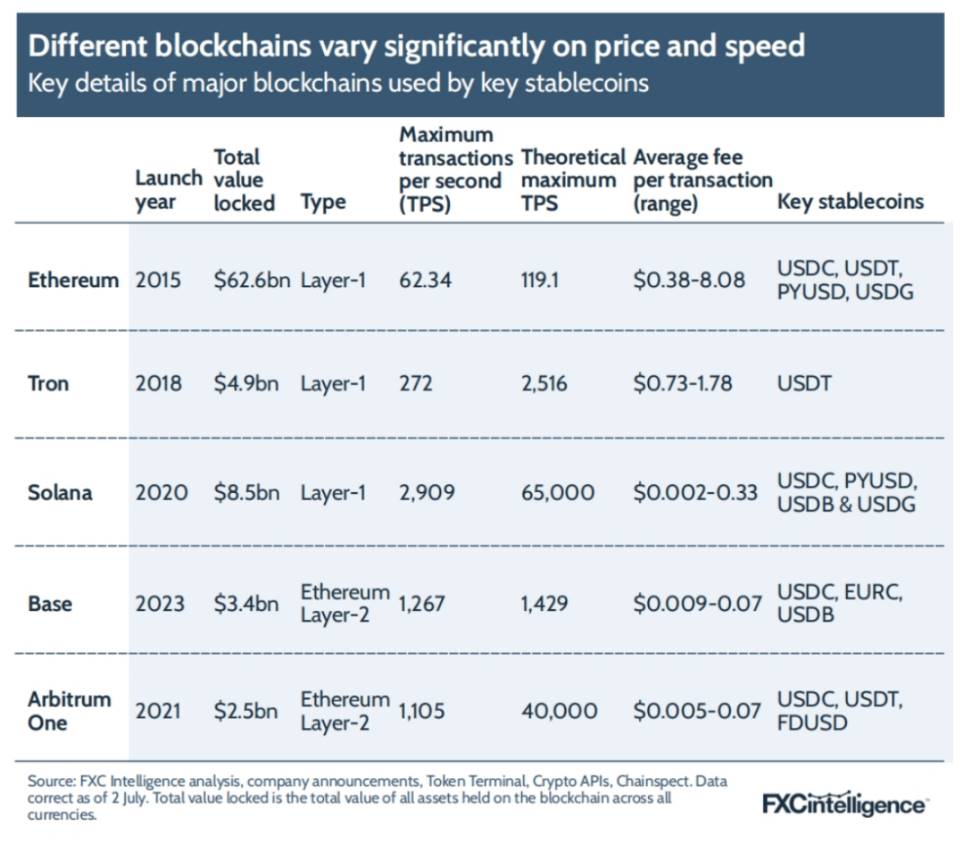

Among blockchains favored by major cross-border payment stablecoins, two broad categories emerge: Layer-1 and Layer-2. Layer-1 refers to base chains, while Layer-2s are built atop Layer-1s, typically to enhance speed and reduce costs.

In terms of "Total Value Locked" (TVL)—the aggregate value of all cryptocurrencies (including stablecoins and other assets) on a given chain—Ethereum leads by far, followed by Solana. However, the two chains differ significantly in transaction throughput and per-transaction cost.

Ethereum’s transaction speed is relatively slow: peak values reported at around 62 transactions per second (TPS), with theoretical maximums estimated at about 119 TPS (a rough figure rarely achieved in practice due to network congestion). In contrast, Solana has achieved peak TPS of about 2,900, with theoretical limits believed to reach around 65,000. For comparison, Visa averaged about 9,600 TPS in fiscal year 2024.

The difference in transfer costs is even more pronounced. Average transaction fees fluctuate significantly over time and by date, directly impacting baseline business costs. Data from Token Terminal shows that over the past year, Ethereum’s average transaction fee ("gas fee") ranged from slightly below $0.4 to over $8; Solana’s peak was just above $0.03, with lows under one cent.

Despite Ethereum’s relative expense and lower transaction ceiling, its token standards enjoy widespread support, meaning there’s still demand to move funds on derivatives of Ethereum even without direct Layer-1 use. Thus, multiple Layer-2 chains have emerged, such as Base and Arbitrum-One. These not only offer higher maximum TPS and lower average fees but also provide various payment-friendly features highly attractive to certain service providers.

4.3 How Key Stablecoin Usage Patterns Are Evolving

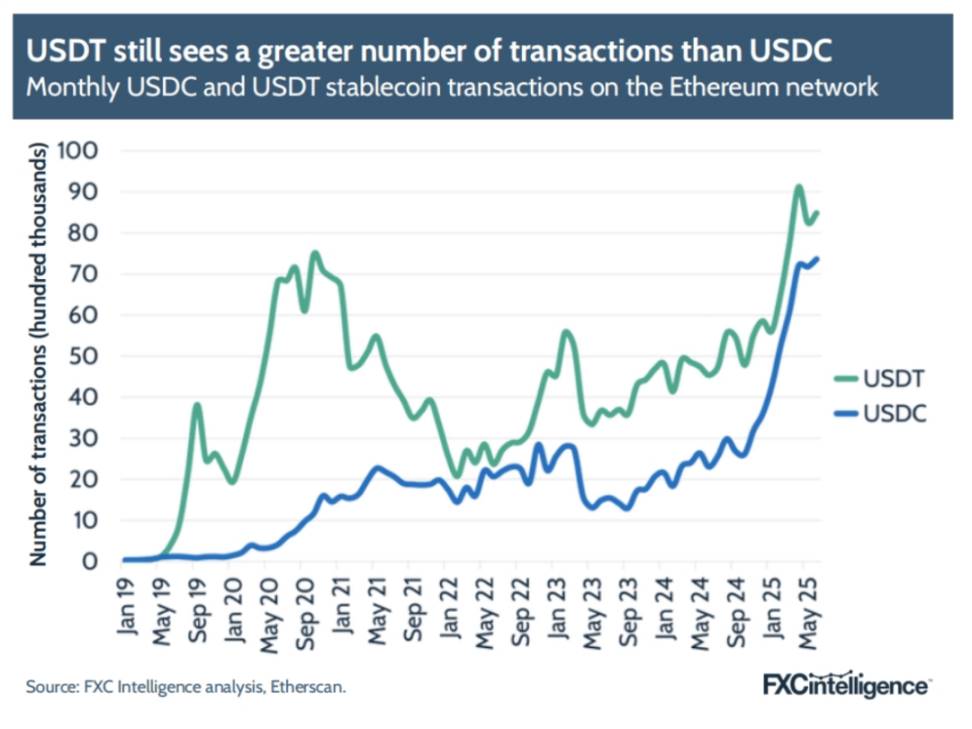

Although USDT has greater issuance volume than USDC, transaction data from the Ethereum blockchain reveals usage differences.

Despite USDT’s circulation on Ethereum exceeding USDC’s by over 60%, their transaction counts are much closer; since late 2024, USDC’s transaction volume has trailed USDT’s only slightly.

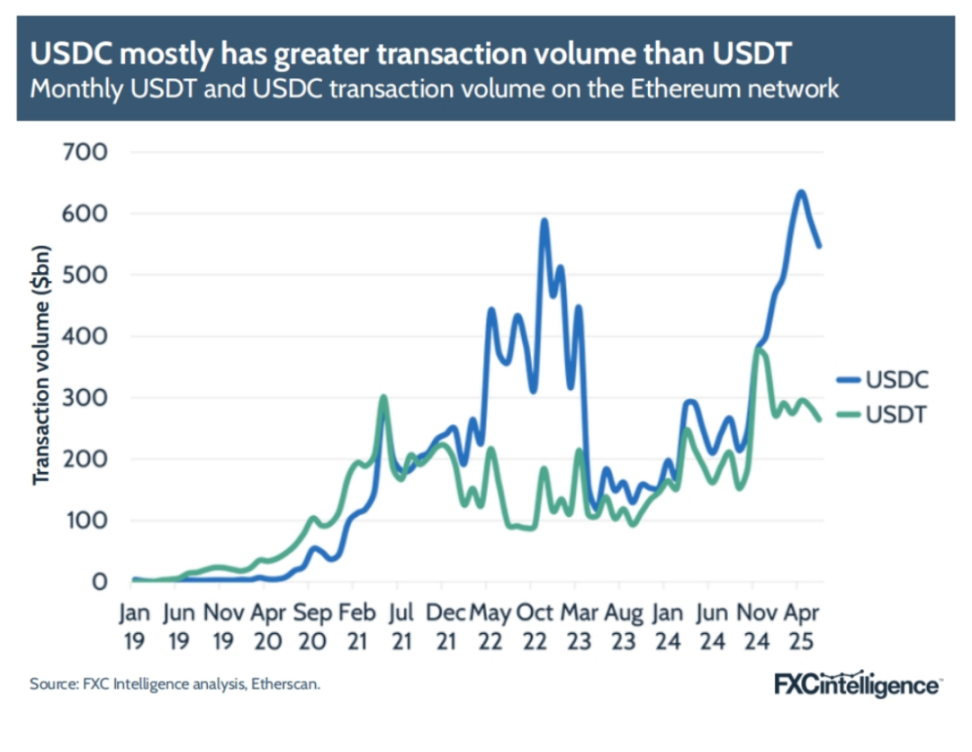

Meanwhile, since November 2024, USDC’s total transaction value on blockchain (i.e., the actual value transferred via the stablecoin) has surpassed USDT’s, and this gap has widened significantly in the first half of this year.

The exact drivers behind this trend remain unclear, likely involving multiple factors. However, the growing interest in stablecoins from the payments industry—where many participants clearly prefer USDC—may at least partially explain this shift.

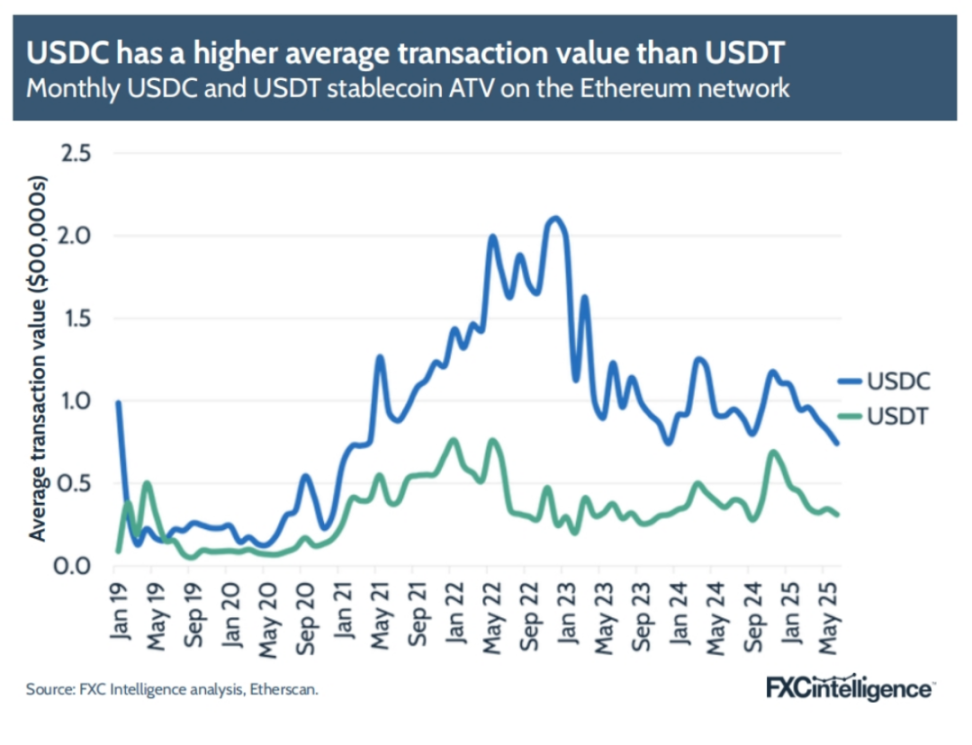

Notably, since 2020, USDC’s average transaction size has consistently exceeded USDT’s, suggesting that—at least on the Ethereum blockchain—USDC is more frequently used for transferring large sums. This doesn’t mean USDT isn’t used for high-value transfers—both coins average transaction sizes in the tens of thousands of dollars—but it does reflect differences in typical use cases.

5. Key Players in Stablecoin Cross-Border Payments

Mapping the core players in the stablecoin cross-border payments landscape is a complex task: the sector hosts numerous companies, with new small firms emerging regularly; simultaneously, more "traditional finance" (TradFi) institutions are incorporating this technology into their operations. We attempt to visualize the current market landscape below. This map doesn’t exhaustively list all stablecoin-involved enterprises but focuses on key active players of various scales.

Although companies like BVNK, Fireblocks, and Bridge operate across multiple aspects of stablecoin cross-border payments, the industry can be divided into several key segments:

1. Stablecoin Issuance & White-Label Issuance Services: Includes both firms issuing their own stablecoins and those providing white-label issuance solutions to others.

2. White-Label Payment Infrastructure (B2B2X): An increasing number of service providers offer white-label payment capabilities to other industry participants. Their models range from turnkey full networks to enhancing existing networks of major payment institutions; these solutions don’t target end-users directly but "empower" other payment service providers.

3. B2B Payments for Enterprises: Numerous companies directly offer B2B payment services using stablecoins, serving clients of varying sizes.

4. Payroll & Contractor Payments: Includes payroll processing, contractor payment services, and companies supporting freelancers receiving such payments.

5. Consumer Remittances: Inevitably, there are also service providers focused on personal consumer remittance scenarios.

6. Stablecoin Acquiring: Includes organizations helping merchants accept stablecoin payments, as well as a few companies offering issuance solutions for stablecoin prepaid cards and digital wallets.

6. Key Opportunities and Use Cases

While emerging markets remain the central focus of stablecoin cross-border payment opportunities, the wide variety of participants reflects increasingly diverse use cases—some spawning others and mutually reinforcing.

6.1 Instant Settlement

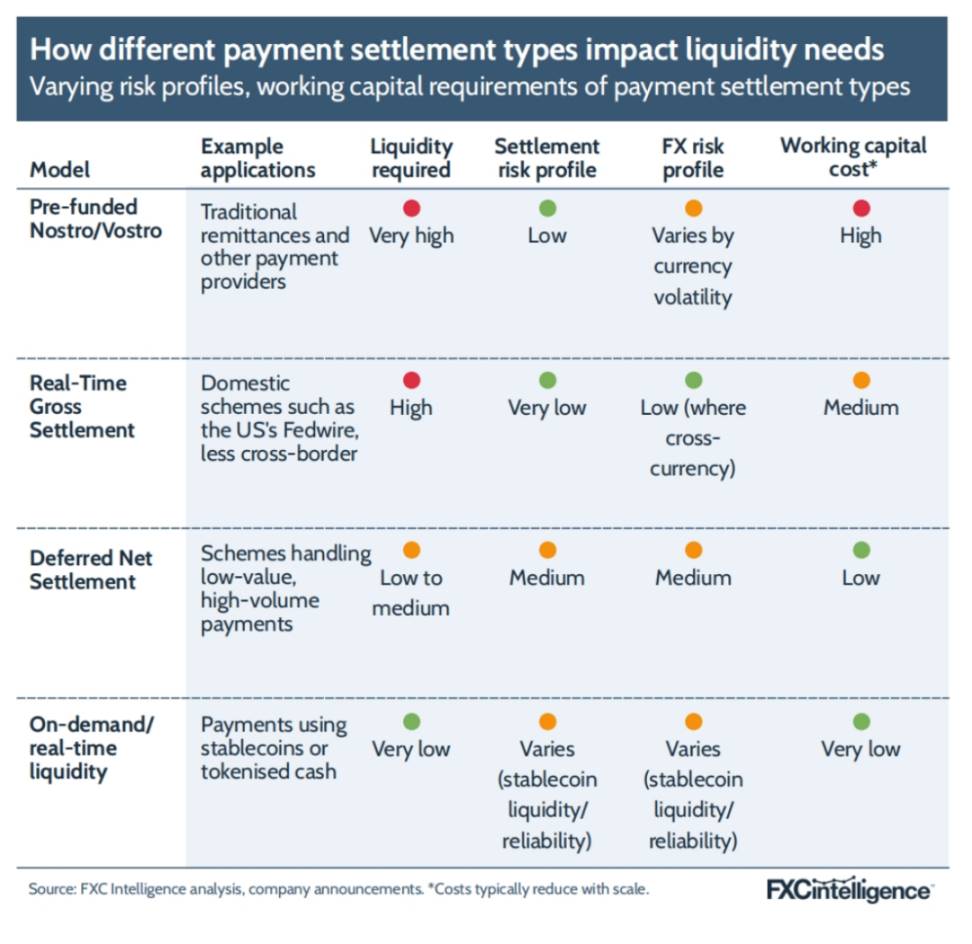

Among the advantages brought by stablecoins, "instant settlement" was repeatedly mentioned by interviewees in this report, primarily due to its stark contrast with prevailing settlement methods in current cross-border payments.

Conduit’s Gertman explained: "Existing institutions achieve 'instant payments' today because they pre-fund liquidity at both ends. If you send money from Brazil to Europe today, as a customer you might feel the funds arrive instantly. But beneath the surface, euro funds were already sitting in a European account waiting for distribution—or the European bank provided an overdraft facility."

This common practice among traditional cross-border payment providers relies on pre-funded nostro and vostro accounts—foreign currency accounts opened by domestic banks at overseas correspondent banks, called nostro from the domestic bank’s perspective and vostro from the correspondent bank’s view.

People often compare stablecoins to "digital nostro accounts." When you use stablecoins, you no longer need to worry about pre-funding. — Nikhil Chandhok, Chief Product & Technology Officer

This settlement model is "netting": consolidating clearing of multiple transactions so companies only need to cover the net difference between payables and receivables. This significantly reduces working capital requirements, while stablecoins go further by enabling instant settlement for every transaction.

You don’t need to estimate counterparty liquidity or forecast demand—just initiate the transaction, because Party A in Country A and Party B in Country B share the same ledger. — Chandhok, Circle

For industry participants, this means dramatically reduced working capital needs. Higlobe’s Farman-Farmaian gave an example: "With instant settlement, I no longer need to freeze $1 million—I can get by with $10,000 because Mastercard knows they can instantly pull funds from my account—we currently have zero working capital tied up."

Farman-Farmaian believes the ripple effects will deepen as more institutions adopt this model. "Currently, trillions of dollars globally are locked in pre-funded accounts—this capital will be released over the next five years," he said. "I don’t know exactly where this money will go, but if market efficiency improves exponentially, genuine financial innovation will follow." BVNK’s Harmse stated bluntly: "Pre-funding is a problem in payments that hasn’t been effectively solved in 25 years." He defines it as a "technical disease."

However, instant settlement also carries potential downsides: no delay means no opportunity to reverse transactions mid-process. Fireblocks’ Shaulov noted: "When SWIFT was hacked, 80% of the funds were recovered because settlement took three days, giving Deutsche Bank analysts time to roll back; but once a stablecoin wallet is compromised or sent to the wrong address, settlement is immediate and irreversible, making recovery extremely difficult."

Meanwhile, the ability to operate without reserving capital has attracted some enterprises to incorporate stablecoins into treasury management—MoneyGram is one such example. Not everyone is convinced yet: Wise is currently observing the technology but hasn’t adopted it for treasury operations.

6.2 Access to Dollars

While "instant settlement" isn’t limited to any specific market, one of the most compelling use cases for stablecoins—and a major driver of mass adoption—is that stablecoins like USDC or USDT are essentially digital forms of the US dollar. Because they aren’t actual physical dollars, people worldwide facing volatile local currencies find it easier to hold them.

Mason of Orbital explained using Argentina as an example: "If you’re in Argentina, you don’t want to hold pesos; due to local regulations, you might not be able to directly hold dollars, but you want dollar exposure—so you hold stablecoins instead."

Turkey is another frequently cited case. Chainalysis research in 2024 showed Turkey had the world’s highest per-capita stablecoin ownership, with local purchases equivalent to 4% of GDP. "Turkey suffers from high inflation—people want to convert wages to dollars immediately," said Paxos’s Kendall. "Exchanging via banks is expensive and cumbersome, so they use Tether. But they don’t know it’s Tether—they just treat it as cheaper dollars stored in crypto wallets rather than bank accounts."

We may be underestimating the extent to which stablecoins provide dollar exposure to global users. Demand for dollars via stablecoins is like a faucet we’ve just turned on. — Luke Tuttle, Chief Product & Technology Officer, MoneyGram

He described stablecoins as "democratizing nearly infinite demand for dollars," a view shared by Circle’s Chandhok, who calls access to dollar banking services a "superpower."

"Westerners don’t understand this," he added. "For many businesses, especially those operating cross-border, obtaining a dollar bank account is extremely difficult, as is accessing competitive foreign exchange rates. Global crypto infrastructure for dollar stablecoin exchange and on/off-ramp services solves these problems without relying on traditional banks."

Another accelerator of this demand is the rise of "remote service professionals"—a market that surged during the pandemic.

Higlobe’s Farman-Farmaian said: "A new group has emerged—highly paid individuals living abroad—not Western expats traveling the world, but highly educated locals working remotely for Western companies, earning salaries between local and US levels, far exceeding local norms."

His company provides dollar-receiving accounts in emerging markets for contractors and businesses, but the key is: funds remain in stablecoin form until the user needs to spend, then instantly convert and disburse via local payment networks (like Brazil’s PIX). "It’s like having an ATM in the sky—she can withdraw anytime, instantly," he explained. This on-demand liquidity, rather than monthly bulk conversion to local currency, fundamentally transforms users’ "relationship with money."

It’s not just individuals who want to hold funds in stablecoins. For emerging market enterprises frequently conducting cross-border transactions, retaining received funds partially or fully in stablecoins is equally appealing. Mason of Orbital explained: "Some companies just want to operate in the world of USDT or USDC. They don’t want Mexican pesos—they’d rather hold stablecoins because they’ll need to pay others later; or they’ll convert only part of it to pay salaries."

6.3 B2C Payments and Stablecoin Disbursements (Pay-outs)

The flip side of surging demand to "hold stablecoins denominated in dollars" is the ability to "make cross-border payments using stablecoins." Fireblocks’ Shaulov pointed out this has become a common use case: suppose you have an IT contractor in Colombia working for a European or American company—they often prefer receiving stablecoins over local bank wire transfers.

An increasing number of marketplace platforms and payment service providers have incorporated stablecoin payments into their product stacks. Worldpay, one of the world’s largest payment processors, recently added this feature. "It’s merchant demand pushing PSPs to ask, 'Hey, what else can we add to our payment stack?'" said BVNK’s Harmse, adding that rising stablecoin adoption in emerging markets is a key driver of this interest.

"Now you have a new payment technology, and users in emerging markets are demanding it—whether gig economy platforms want to receive payments or marketplaces need to pay users or sellers." While payment scenarios vary, Triple-A’s Barbier believes paying content creators via stablecoins holds particular promise. "The beauty of stablecoins is that even tiny amounts can be economically feasible to deliver," he said. "For example, a gamer or content creator earning just one dollar can actually receive it—because stablecoin transfers cost almost nothing."

6.4 B2B Payments and Trade Finance

Although B2C payments attract attention and offer great potential for many participants, in terms of transaction volume, they still pale in comparison to B2B payments. "B2C may get a disproportionate amount of airtime, but the real heavy flows happen on the B2B side," said BVNK’s Harmse.

Adoption here

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News