Can BNB's treasury, managed by the richest Chinese person, keep rising after surging 600%?

TechFlow Selected TechFlow Selected

Can BNB's treasury, managed by the richest Chinese person, keep rising after surging 600%?

1.25 billion USD, where can it take BNB?

Author: Lin Wanwan, BlockBeats

On July 28, the long-rumored "main force" behind the BNB treasury ultimately landed on a small nicotine e-cigarette company named VAPE—this previously sub-$10 million market cap micro-cap unexpectedly became the chosen one personally selected by China’s richest individual.

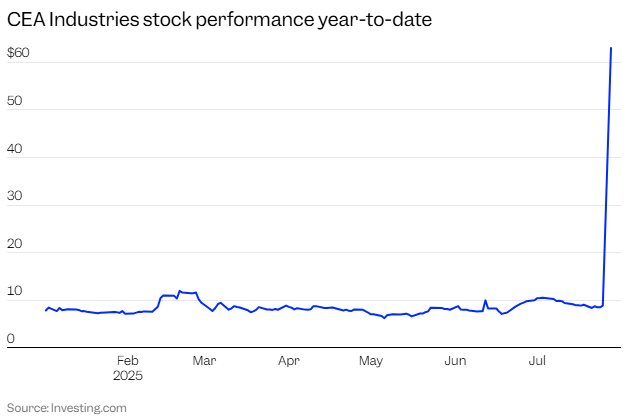

News leaked early, causing the stock to surge over 1800% pre-market. After opening, the share price jumped from Friday’s closing price of $8.88 to an intraday high of $82.88.

An insider told BlockBeats that Binance-related investment teams had already initiated shell acquisition and private placement fundraising preparations for the BNB treasury project before early July. Another source indicated that to prevent front-running risks prior to finalization, the team simultaneously acquired stakes in multiple small U.S.-listed shell companies, only settling on VAPE as the final target at the last moment.

Behind this sharp price movement lies a PIPE (Private Investment in Public Equity) agreement—valued at up to $500 million, co-led by 10X Capital and YZi Labs—with the ambition of turning VAPE into the world's largest publicly listed BNB treasury company.

This is not retail-driven frenzy but a precisely structured capital experiment—a novel arbitrage pathway combining “compliant BNB holding + public company valuation premium,” and potentially a breakout narrative within the Binance ecosystem.

VAPE, once an obscure entity, is now being remembered across broader capital markets as a key variable in the “BNB treasury” story.

Deconstructing the BNB Treasury Playbook: From Shell Acquisition to Valuation Leverage

On July 28, VAPE (formerly CEA Industries) officially announced a PIPE financing led by 10X Capital and YZi Labs, with initial funding reaching $500 million—including $400 million in cash and $100 million in crypto asset subscriptions. If all attached warrants are exercised, total funding could expand to $1.25 billion.

This financing isn't just massive in scale—it has a clear mission: VAPE aims to become the world’s largest publicly traded BNB treasury company, bringing BNB into traditional capital markets and attracting compliant capital into the BNB Chain ecosystem through asset allocation models.

This means VAPE is no longer merely a hardware or retail supplier but is transforming into a financial platform focused on BNB, integrating BNB's value and yield mechanisms into its corporate capital structure.

After the PIPE closes, VAPE will be led by a core team with institutional and digital asset expertise: David Namdar (co-founder of Galaxy Digital, now senior executive at 10X Capital) will serve as CEO; Russell Read (former CIO of CalPERS, current CIO at 10X Capital) will take the CIO role; Saad Naja (seasoned operator from Kraken and Exinity) joins the executive team.

Meanwhile, 10X Capital itself will act as the asset manager for the BNB treasury, responsible for structural design, capital operations, and strategy execution, while YZi Labs provides strategic support to ensure smooth PIPE distribution. Over 140 institutions and crypto funds (including Pantera Capital, Blockchain.com, GSR, Arrington, etc.) have participated, forming strong institutional backing.

BlockBeats analyzed the VAPE announcement: proceeds will fund a centralized, long-term BNB treasury strategy. Within the next 12–24 months, VAPE will build an initial BNB position and scale up via ATM (At-The-Market) issuance; it may also participate in BNB staking, lending, DeFi protocol yields, and other income-generating mechanisms under a conservative risk framework.

This operational model mirrors MicroStrategy’s BTC treasury approach—but focuses on BNB, which has stronger utility within its ecosystem. By layering yield strategies atop holding appreciation, it introduces cash flow potential and valuation upside.

Once the PIPE concludes, VAPE will become one of the largest publicly traded companies offering exposure to a single Layer-1 blockchain.

In simple terms, this round equips the company with a $1.25 billion “crypto arsenal” to buy BNB. In comparison, SharpLink (SBET), the earliest firm to bet on an ETH treasury concept, raised only $525 million in total.

After the Deal: Where Will the Stock Go?

Following the PIPE signing, VAPE announced the transaction is expected to close by July 31, 2025. At that point, funds will be disbursed and the updated capital management strategy will go live. According to the announcement, common shares will continue trading on Nasdaq under the ticker “VAPE.”

The essence of PIPE financing is a discounted private placement—essentially selling shares at a discount to specific investors in exchange for large-scale capital. For VAPE, the primary raise is $500 million ($400M cash, $100M in BNB assets), plus warrant mechanisms that can bring total funding up to $1.25 billion. In short, the company will issue substantial new shares and warrants to PIPE investors.

This leads directly to two structural outcomes: existing shareholders face equity dilution. Under full-dilution calculations, legacy shareholders’ voting rights and profit participation will significantly decline; the capital structure becomes more complex. With warrants, lock-up clauses, and staged exercise mechanisms, valuation will lean more toward structural modeling than fundamental analysis.

As the PIPE allocation completes, VAPE’s equity structure shifts from “controlled” to “liquid,” especially after warrants are exercised—free float will increase exponentially.

This is particularly evident in VAPE’s PIPE terms: the deal includes a large warrant component allowing investors to purchase new shares at prices below market rate, creating a classic warrant + subscription arbitrage structure.

Image source: crypto-economy

Specifically, such warrants typically exhibit several features—extremely low strike prices far below public market levels, creating arbitrage potential; phased unlocking, where some warrants vest immediately while others are subject to price triggers or time-based rolling releases; possible dynamic execution tied to market prices—when the stock exceeds certain thresholds (e.g., 2–3x PIPE price), forced exercise or accelerated conversion clauses may activate.

Under this structure, VAPE’s stock behavior will be driven less by fundamentals and more by actions of PIPE investors. Once valuations diverge from underlying asset values, these structures create strong profit-taking incentives, potentially becoming sources of liquidity shocks.

So what happens to the stock price—will it rise or fall?

By analyzing existing PIPE cases, we can break down VAPE’s likely trajectory into three phases:

Phase One: Expectation-Driven (Already Occurred)

After the PIPE announcement on July 28, VAPE’s stock surged 800% pre-market, jumping from $8.88 to around $80, triggering multiple circuit breakers. At this stage, the market ignored fundamentals, pricing purely based on narrative expectations, fueling intense speculation.

With funding not yet received and warrants unexercised, the market was in a state of “low float, high sentiment, no supply,” making the stock extremely sensitive to expectations.

Phase Two: Structural Release (Post-Closing)

Expected post-July 31, once the deal closes, capital flows in and some PIPE investors receive initial shares and transferable warrants.

The market enters a delicate phase: if the stock remains elevated, warrant holders may quickly exercise and sell, pressuring prices; if confidence in the treasury model wanes, early arbitrageurs exit immediately; any failure to disclose timely BNB accumulation would weaken the “on-chain NAV anchoring” expectation.

During this phase, volatility spikes sharply, and pricing shifts from “value anchoring” to “capital behavior.”

Phase Three: Valuation Reversion or Second Narrative Launch

If BNB performs strongly and the company publishes on-chain yield details, the market might refocus on the “Crypto NAV+” model, driving a second wave of valuation growth; if sentiment cools or PIPE participants keep selling, the stock may revert to asset value levels—or enter a liquidity vacuum.

This is the critical divergence point for most PIPE projects—some evolve into sustainable secondary market plays, others become one-off stories followed by capital flight.

Rises often stem from structural scarcity; falls usually begin with liquidity collapse. Both paths have been repeatedly observed in past PIPE cases. Therefore, the direction isn’t about intrinsic value judgment—it’s a race between valuation buildup and liquidity release speed.

Why VAPE? What Made This Shell Suitable?

Looking back at VAPE’s origins reveals a very different starting point.

VAPE was formerly CEA Industries, an engineering equipment firm focused on indoor agriculture and climate control systems for cannabis cultivation. Its subsidiary Surna provided LED lighting, air circulation, hydroponic systems—primarily serving North American cannabis growers. The company long operated in a “triple-low” state: low growth, low profitability, low market cap.

According to StockAnalysis and TipRanks, annual revenue in 2024 was under $6 million, with market cap persistently below $10 million and minimal free float on U.S. markets.

In 2024, the company attempted its first strategic pivot: acquiring Canadian vape chain Fat Panda for CAD 18 million. Fat Panda operated 33 stores, generated over CAD 38 million in annual revenue, and achieved nearly 21% EBITDA margin. This marked a shift from “hardware vendor” to “retail operator,” signaling VAPE’s move toward consumer branding.

But this alone wasn’t enough to justify revaluation.

Thus, VAPE was never compelling—and could even be described as a “market sleeper.” Yet these very flaws made it ideal as a shell: small size, clean capital structure, untapped market cap potential, and narrative emptiness in crypto circles (no prior BNB exposure).

Whether VAPE can become the “MicroStrategy of BNB” remains unproven. But one thing is certain: it’s no longer just an e-cigarette company. It has become a programmable shell embedded in a capital game—its exterior a U.S. public company, its core a structured financial instrument, its soul the ability to manipulate narrative and sentiment.

Control and Core Team: Who Is Running This Deal?

Behind this “asset-for-valuation” transformation experiment, VAPE functions not as an operating business but as a financial vehicle. The real drivers are a capital-structure-focused team—a hybrid of finance and crypto experts whose goal isn’t just fundraising but building a self-sustaining valuation loop: from primary placement, to on-chain asset accumulation, to secondary market narrative rollout.

After the PIPE closes, actual control shifts. The original management team, rooted in industrial and retail operations, lacks the capability to manage an on-chain treasury or structured assets. Real control gradually transfers to the financing architects—10X Capital and YZi Labs.

10X Capital: the lead institution in this PIPE, specializing in SPAC mergers, cross-border arbitrage, and structured trades—a classic “leveraged capital engineer.” Since 2023, the team has tried extending the MSTR model to ETH, SOL, and even LSD sectors. Betting on BNB now clearly aims to replicate MicroStrategy’s treasury + compounding valuation formula.

YZi Labs: strategic advisor on this deal, widely believed to have direct ties to CZ’s family fund, acting as the key behind-the-scenes force pushing BNB treasury adoption and public listing pathways. Their involvement is seen as an open signal of Binance-affiliated support. In the VAPE project, they helped select the shell, coordinate media timing, and collaborate with investors and market makers to craft a “accumulate-expose-value” narrative strategy.

The defining feature of this capital arrangement is that VAPE is no longer a creator of value but a designed intermediary for value extraction. 10X Capital provides structure and timing, YZi Labs delivers narrative and access, and BNB serves as the embedded base asset. Together, they complete an end-to-end loop from asset layer to market layer.

Whether the story holds depends on whether on-chain positions materialize and market confidence sustains. For most retail investors and observers, VAPE’s emergence isn’t an endpoint—it’s more like a prelude to the accelerating era of structural arbitrage.

Image source: bankless

Epilogue

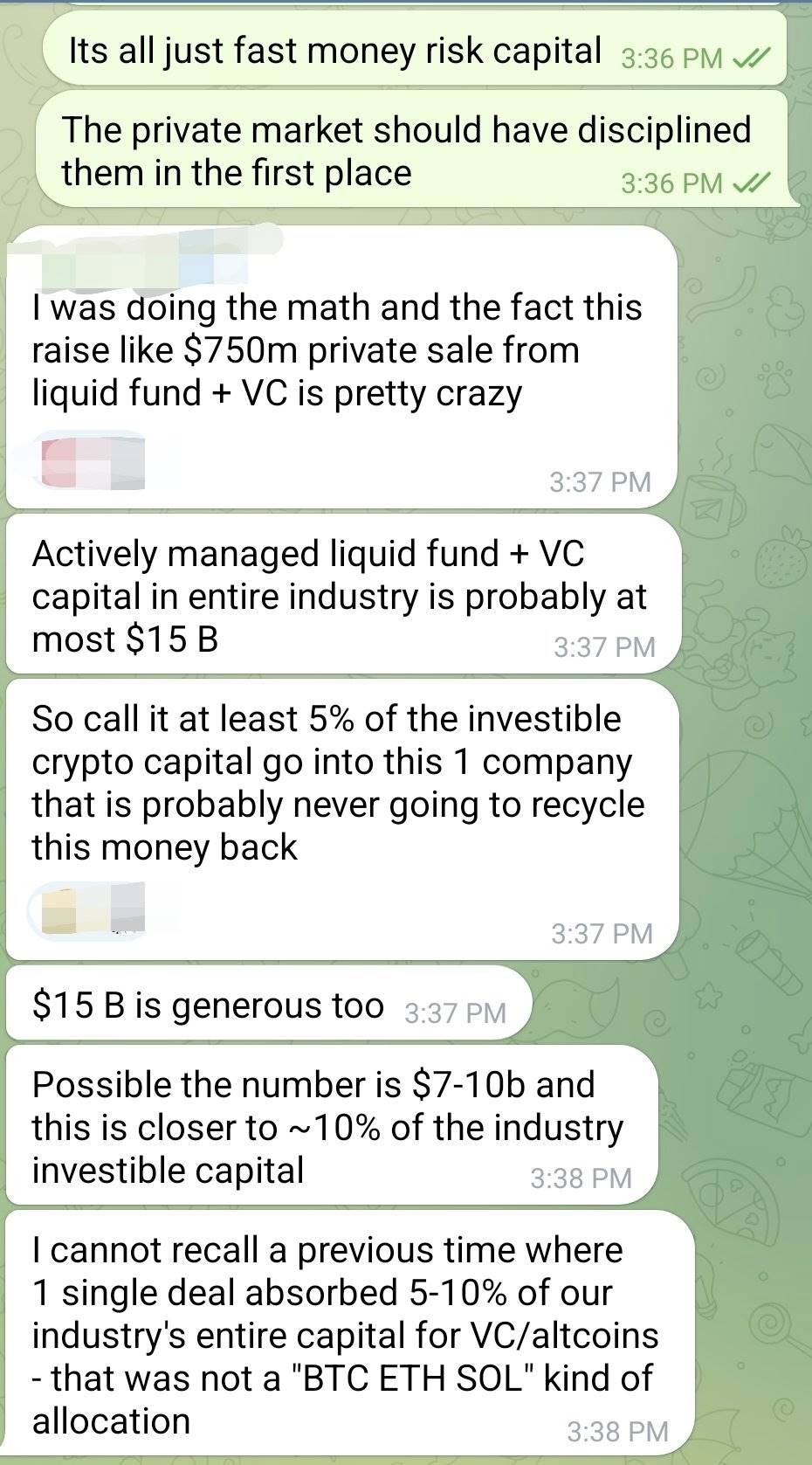

In a Telegram conversation among investors, someone did the math: active capital available for VC and liquidity funds across the entire crypto industry may only amount to $7–15 billion. VAPE’s PIPE, targeting up to $1.25 billion, could absorb 5–10% of the sector’s investable capital under extreme scenarios.

“I’ve never seen a non-BTC/ETH/SOL project pull in so much capital in a single deal,” he said. “And this company likely won’t recycle those funds back into the industry.”

This isn’t just a concentration risk—it signals that the crypto industry’s already tight liquidity is being siphoned off by an unproven model.

During bull markets, liquidity should fuel diverse innovation, supporting early-stage projects in DeFi, payments, infrastructure. Now, instead, capital is funneled into a “story shell” built on PIPE structures and shell speculation. If VAPE succeeds, it may spawn more crypto versions of MicroStrategy; if it fails, it could become a textbook case of industry-wide resource misallocation.

Capital writes narratives—and creates bubbles. At the intersection of crypto and finance, everything looks like a victory of structural arbitrage—until liquidity dries up completely, revealing whether there was any real “blood-making” capacity beneath.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News