IOSG: Deconstructing the Cryptocurrency Reserve Economic Model

TechFlow Selected TechFlow Selected

IOSG: Deconstructing the Cryptocurrency Reserve Economic Model

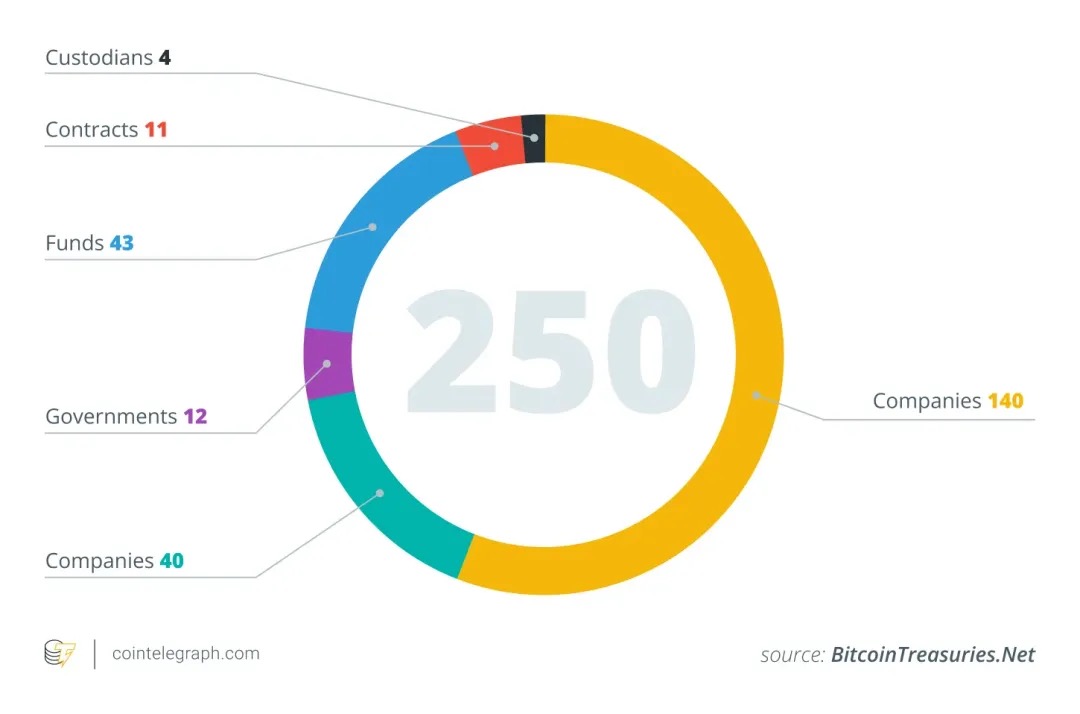

As of mid-2025, approximately 250 publicly listed companies worldwide have included Bitcoin on their balance sheets, with MicroStrategy pioneering a new corporate crypto asset allocation model by building a large-scale Bitcoin reserve through innovative financial instruments (preferred shares, zero-coupon convertible bonds).

Introduction

As of mid-2025, an increasing number of public companies have begun incorporating cryptocurrencies—especially Bitcoin—into their corporate treasury asset allocations, inspired by the success of Strategy ($MSTR). For example, according to blockchain analytics data, 26 new companies added Bitcoin to their balance sheets in June 2025 alone, bringing the global total of firms holding BTC to approximately 250.

These companies span multiple industries (technology, energy, finance, education, etc.) and regions. Many view Bitcoin’s capped supply of 21 million coins as a hedge against inflation and emphasize its low correlation with traditional financial assets. This strategy is quietly going mainstream: as of May 2025, 64 SEC-registered firms collectively held around 688,000 BTC, roughly 3–4% of Bitcoin’s total supply. Analysts estimate that over 100–200 companies globally have incorporated crypto assets into their financial statements.

Crypto Asset Reserve Models

When a public company allocates part of its balance sheet to cryptocurrency, a core question arises: how do they finance these purchases? Unlike traditional financial institutions, most companies adopting crypto treasury strategies do not rely on strong operating cash flows. The following analysis will use $MSTR (MicroStrategy) as the primary example, since most other firms are effectively replicating its model.

Operating Cash Flow

Theoretically, the “healthiest” and least dilutive method would be using free cash flow from core operations to buy crypto assets. However, in reality, this is nearly impossible. Most companies lack sufficient stable and large-scale cash flow to accumulate significant BTC, ETH, or SOL reserves without external financing.

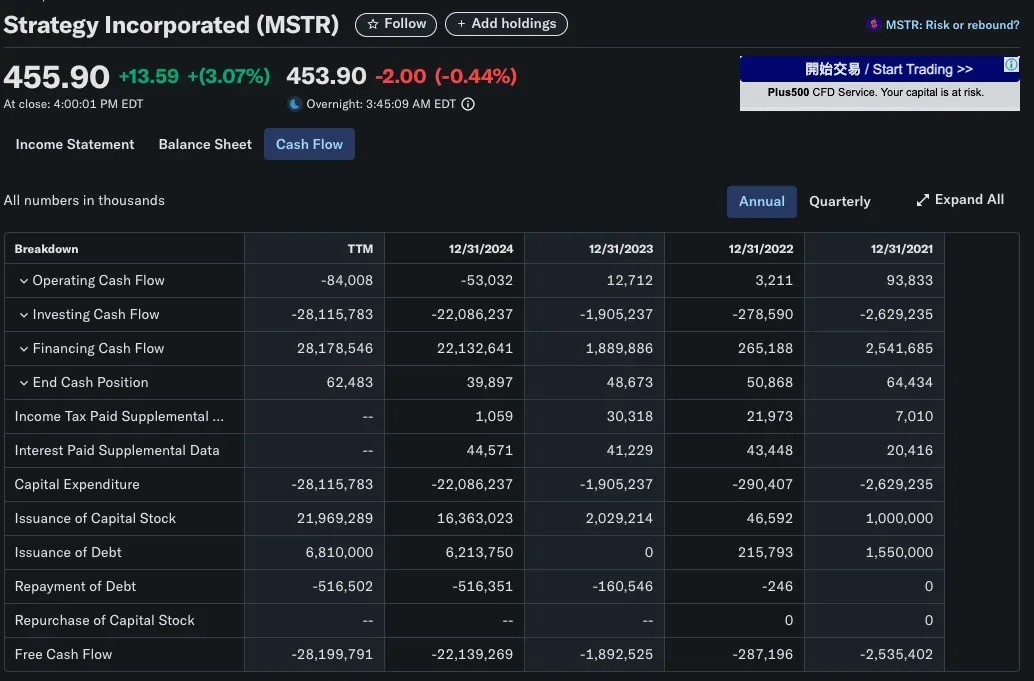

MicroStrategy (MSTR) is a classic case: founded in 1989 as a business intelligence software firm offering products like HyperIntelligence and AI analytics dashboards, it still generates only limited revenue from these businesses. In fact, MSTR has negative annual operating cash flow—far short of the tens of billions of dollars it has invested in Bitcoin. Thus, MicroStrategy’s crypto treasury strategy was never based on internal profitability but rather on external capital engineering.

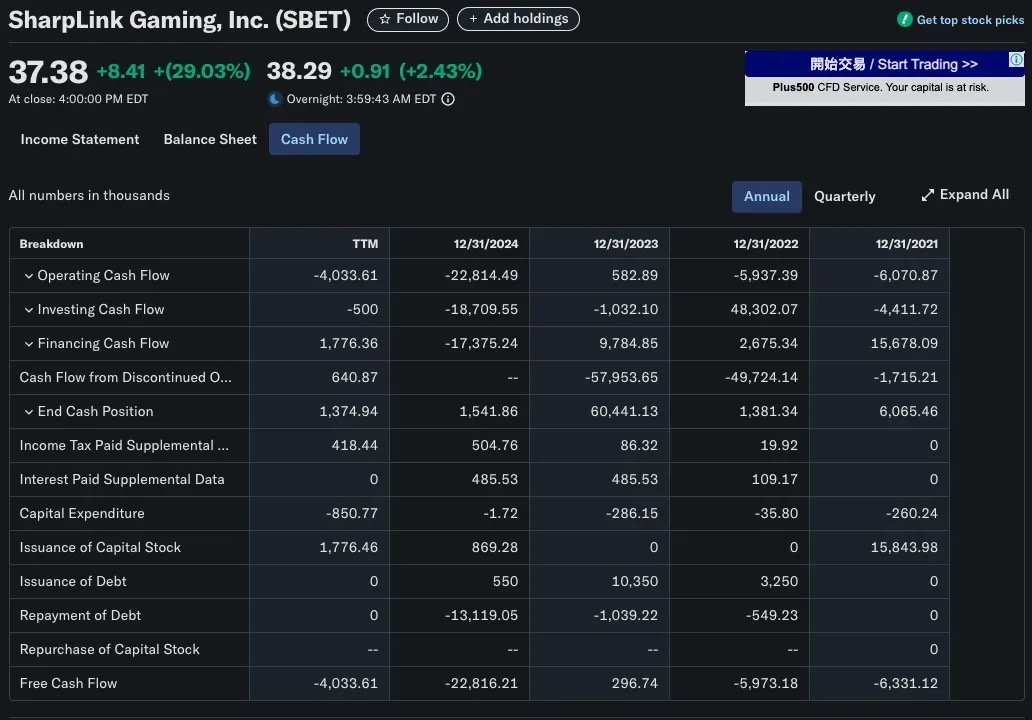

A similar situation applies to SharpLink Gaming (SBET). In 2025, SBET transformed into an Ethereum treasury vehicle, purchasing over 280,706 ETH (worth ~$840 million). Clearly, it could not have funded this through its B2B gaming business. Instead, SBET relied primarily on PIPE financing (private investment in public equity) and direct stock issuance, not operating income.

Capital Markets Financing

Among public companies pursuing crypto treasury strategies, the most common and scalable method is raising funds via public markets—issuing stocks or bonds—and using the proceeds to purchase Bitcoin or other crypto assets. This allows companies to build large crypto treasuries without tapping retained earnings, leveraging traditional financial engineering techniques.

Equity Issuance: The Traditional Dilutive Case

In most cases, issuing new shares comes at a cost. When a company raises capital through stock issuance, two things typically happen:

-

Ownership is diluted: existing shareholders’ ownership percentages decrease.

-

Earnings per share (EPS) decline: with net profit unchanged, increased shares outstanding reduce EPS.

These effects often lead to share price declines for two main reasons:

-

Valuation logic: if the price-to-earnings (P/E) ratio remains constant while EPS falls, the stock price tends to fall.

-

Market psychology: investors often interpret fundraising as a sign of financial weakness or distress, especially when proceeds fund unproven growth plans. Additionally, the supply pressure from new shares entering the market can depress prices.

An Exception: MicroStrategy’s Anti-Dilutive Equity Model

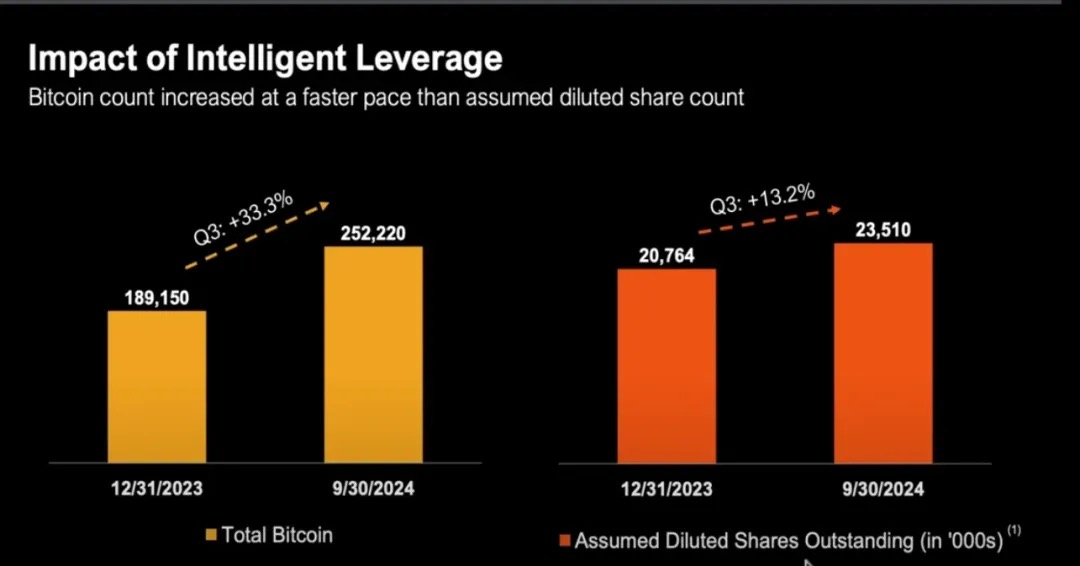

MicroStrategy (MSTR) stands as a notable exception to the conventional narrative that “equity dilution = shareholder harm.” Since 2020, MSTR has aggressively raised capital through equity financing to buy Bitcoin, increasing its total shares outstanding from under 100 million to over 224 million by the end of 2024.

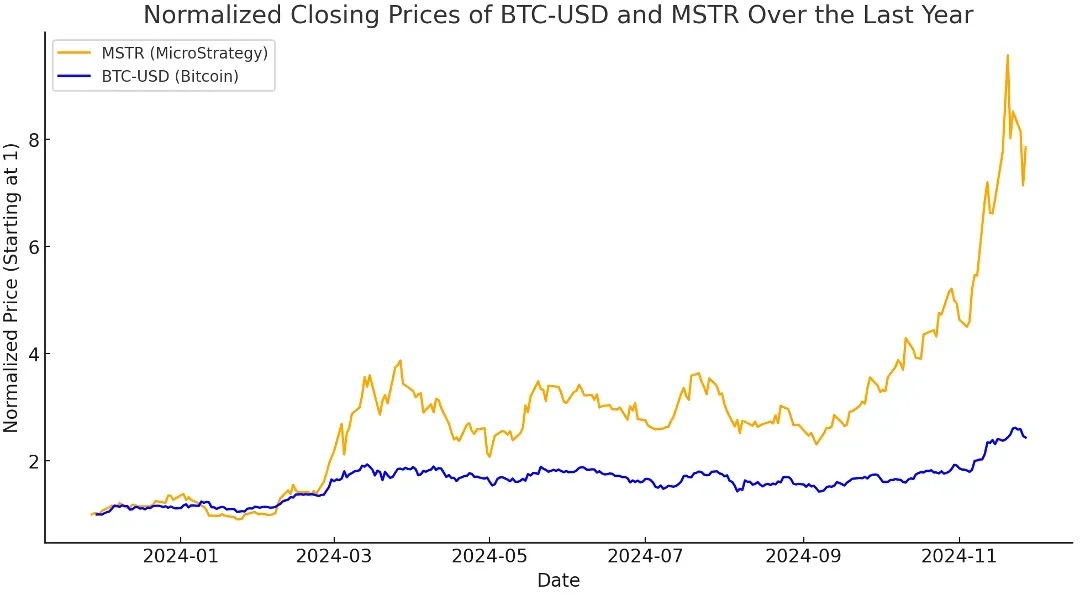

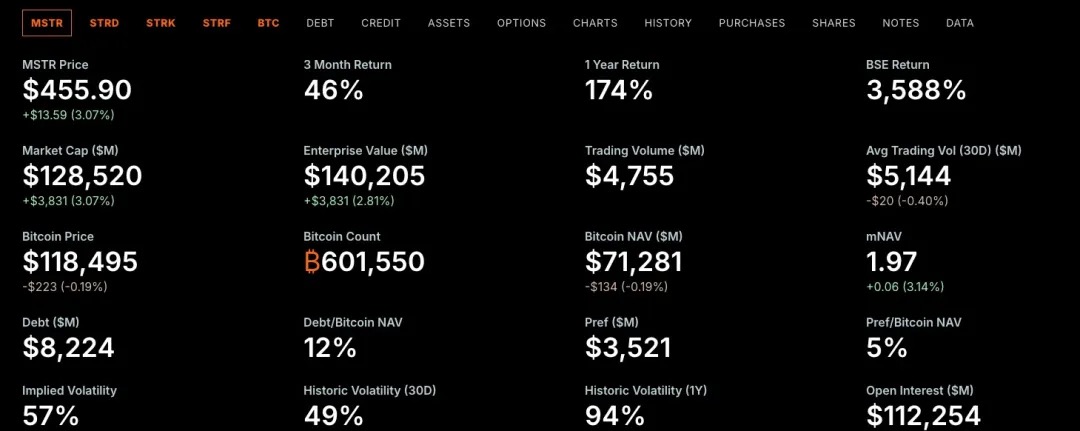

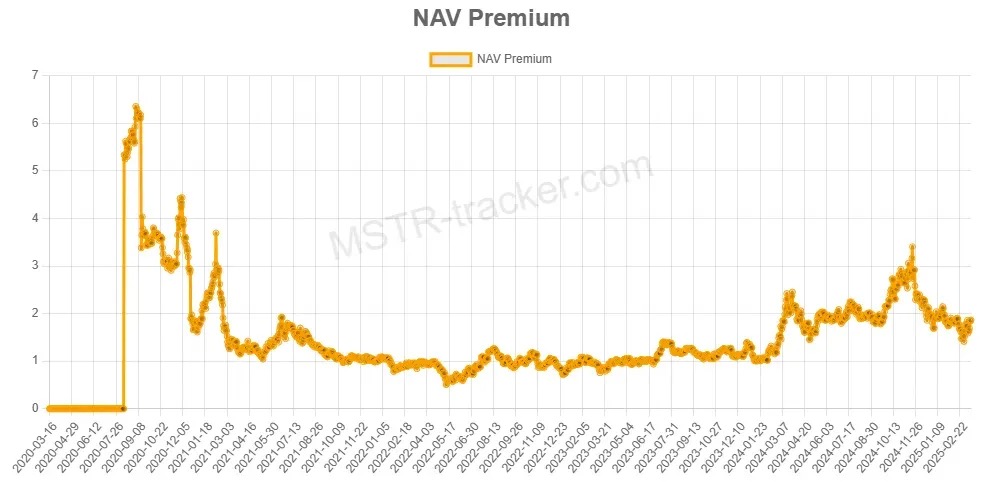

Despite share dilution, MSTR has frequently outperformed Bitcoin itself. Why? Because MicroStrategy has consistently traded at a premium to the fair market value of its Bitcoin holdings—what we refer to as mNAV > 1.

=

=

Understanding the Premium: What is mNAV?

-

When mNAV > 1, the market values MSTR above the fair market value of its Bitcoin holdings.

In other words, investors pay more per unit of exposure through MSTR than they would buying BTC directly. This premium reflects market confidence in Michael Saylor’s capital strategy and may indicate that investors see MSTR as offering leveraged, actively managed BTC exposure.

Support from Traditional Finance Logic

Although mNAV is a crypto-native valuation metric, the concept of “trading above underlying asset value” is well-established in traditional finance.

Companies often trade at premiums to book value or net asset value (NAV) for several reasons:

Discounted Cash Flow (DCF) Valuation

Investors focus on the present value of future cash flows, not just current assets.

This often leads to valuations far exceeding book value, especially when:

-

Revenue and profit margins are expected to grow

-

The company has pricing power or sustainable competitive advantages (moats)

📌 Example: Microsoft’s valuation is based not on its cash or hardware assets, but on the future value of its recurring software subscription revenues.

Profit and Revenue Multiples (EBITDA)

In high-growth sectors, companies are commonly valued using P/E ratios or revenue multiples:

-

High-growth software firms may trade at 20–30x EBITDA;

-

Early-stage companies without profits may trade at 50x revenue or higher.

📌 Example: Amazon had a P/E ratio of 1,078x in 2013.

Despite minimal profits, investors bet on its dominance in e-commerce and AWS.

MicroStrategy possesses something Bitcoin lacks: a corporate shell with access to traditional capital markets. As a U.S. public company, it can issue stocks, bonds, and even preferred equity to raise cash—and it has done so remarkably effectively.

Michael Saylor skillfully leverages this system, raising billions through zero-percent convertible bonds and innovative preferred equity products, deploying all proceeds into Bitcoin.

Investors recognize that MicroStrategy can use “other people’s money” to scale BTC purchases—a capability largely inaccessible to individual investors. The MSTR premium isn’t about short-term NAV arbitrage; it stems from deep market trust in the company’s capital-raising and allocation abilities.

How mNAV > 1 Enables Anti-Dilution

When MicroStrategy trades above the net asset value of its Bitcoin holdings (i.e., mNAV > 1), it can:

-

Issue new shares at a premium

-

Use the proceeds to buy more Bitcoin (BTC)

-

Increase total BTC holdings

-

Drive both NAV and enterprise value upward simultaneously

Even as shares outstanding increase, BTC per share may remain stable or rise—making equity issuance an anti-dilutive move.

What Happens If mNAV < 1?

When mNAV < 1, each dollar of MSTR stock represents more than one dollar of BTC market value (at least on paper).

From a traditional finance perspective, MSTR is trading at a discount to its net asset value (NAV). This creates capital allocation challenges. If the company raises equity under these conditions to buy more BTC, it’s effectively paying a premium for BTC, which:

-

Dilutes BTC per share

-

Destroys value for existing shareholders

When MicroStrategy faces mNAV < 1, it cannot sustain the “issue shares → buy BTC → increase BTC/share” flywheel effect.

So what options remain?

Buy Back Shares Instead of Buying More BTC

When mNAV < 1, repurchasing MSTR shares becomes value-accretive because:

-

You’re buying back shares below their intrinsic BTC value

-

With fewer shares outstanding, BTC per share increases

Saylor has explicitly stated: if mNAV falls below 1, the best strategy is to buy back shares rather than acquire more BTC.

Mechanism One: Issuing Preferred Stock

Preferred stock is a hybrid security, ranking between debt and common equity in the capital structure. It typically offers fixed dividends, no voting rights, and priority over common stock in dividend payments and liquidation. Unlike debt, it doesn’t require principal repayment; unlike common stock, it provides more predictable returns.

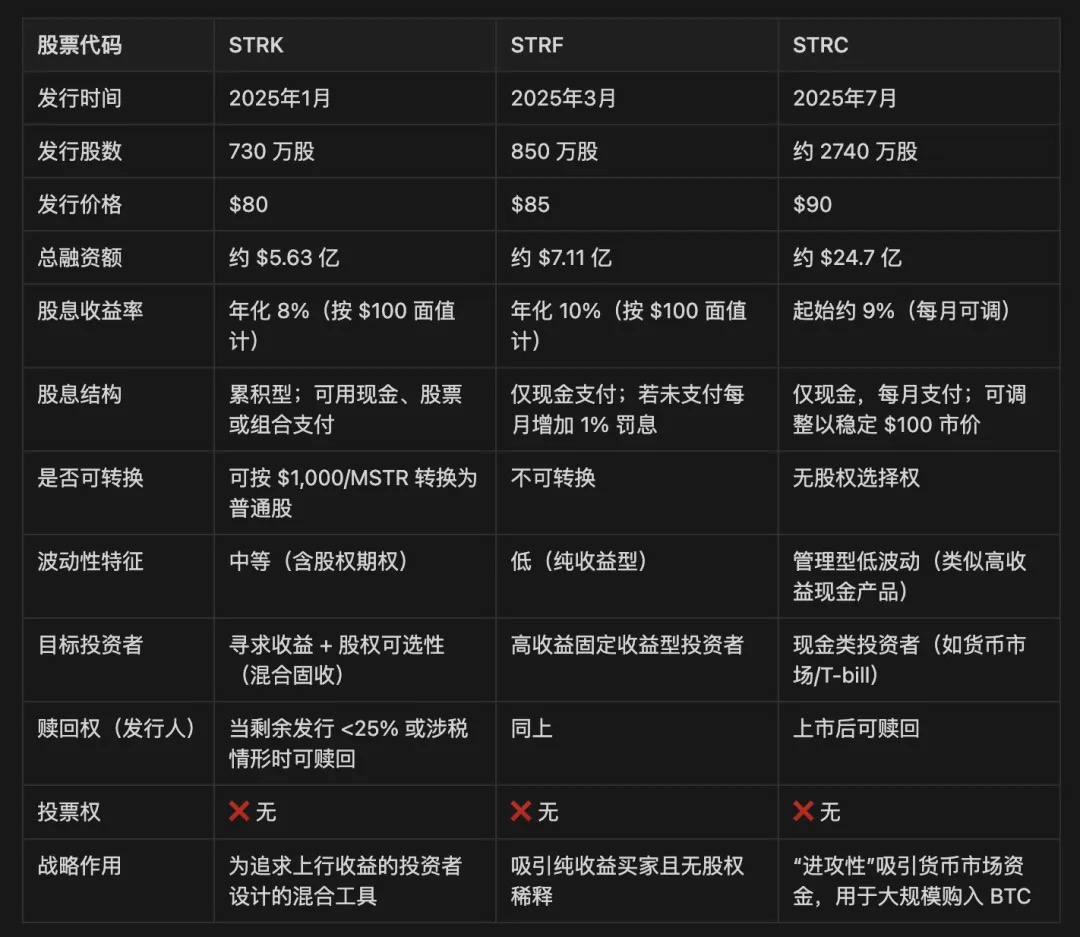

MicroStrategy has issued three classes of preferred stock: STRK, STRF, and STRC.

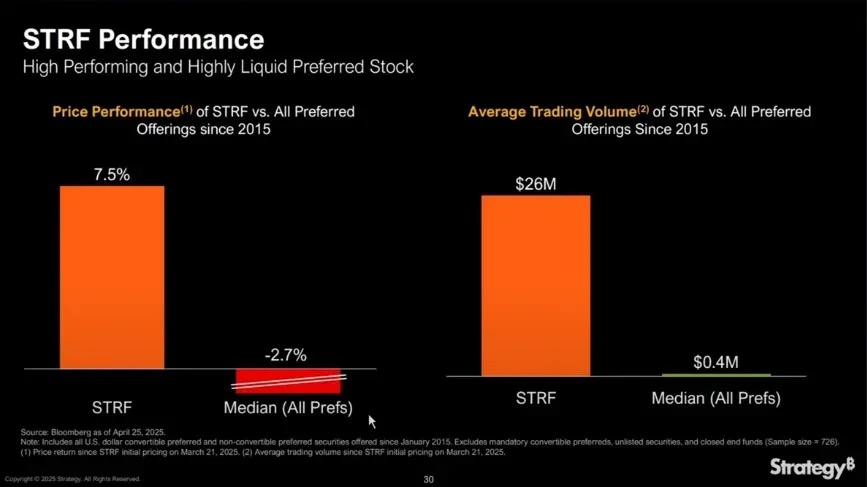

STRF is the most straightforward instrument: a non-convertible perpetual preferred stock paying a fixed 10% annual cash dividend on a $100 par value. It has no conversion option and does not participate in MSTR stock upside—only yield.

STRF’s market price fluctuates around the following dynamics:

-

If MicroStrategy needs funding, it issues more STRF, increasing supply and pushing prices down;

-

If demand for yield surges (e.g., during low-rate environments), STRF prices rise, lowering effective yields;

-

This creates a self-correcting price mechanism, with prices typically confined to a narrow range (e.g., $80–$100), driven by yield demand and supply.

Example: if the market demands a 15% yield, STRF might drop to $66.67; if 5%, it could rise to $200.

Since STRF is non-convertible and essentially non-redeemable (unless tax or capital triggers occur), it behaves like a perpetual bond. MicroStrategy can repeatedly use it to “buy the dip” on BTC without needing further financing.

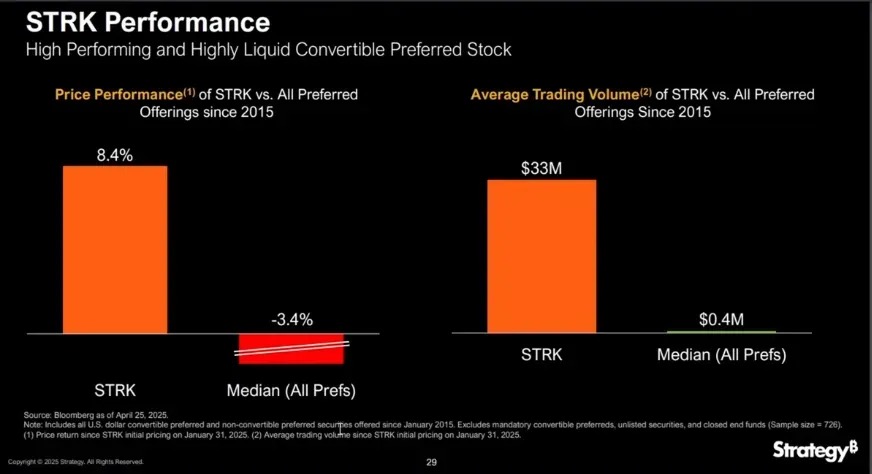

STRK is similar to STRF, with an 8% annual dividend, but includes a key feature: it can convert into common stock at a 10:1 ratio when MSTR’s share price exceeds $1,000, effectively embedding a deeply out-of-the-money call option, giving holders long-term upside potential.

STRK is highly attractive to both the company and investors due to:

Asymmetric Upside for MSTR Shareholders:

-

Each STRK sells for ~$85, so 10 shares raise $850;

-

If converted later into 1 MSTR share, the company effectively bought BTC at $850, but only dilutes if MSTR trades above $1,000;

-

Thus, it’s non-dilutive while MSTR < $1,000, and any dilution reflects prior BTC appreciation.

Yield-Stabilizing Structure:

-

STRK pays $2 quarterly, $8 annually;

-

If the price drops to $50, the yield rises to 16%, attracting buyers and supporting the price;

-

This makes STRK behave like a “bond with an embedded option”: defensive downside, participation on upside.

Investor Motivation and Conversion Incentives:

-

When MSTR breaks $1,000, holders are incentivized to convert;

-

As MSTR climbs further (e.g., to $5,000 or $10,000), the $8 dividend becomes negligible (~0.8% yield), accelerating conversion;

-

This creates a natural exit path, transforming temporary financing into permanent equity.

MicroStrategy retains the right to redeem STRK under certain conditions, such as when less than 25% of shares remain unconverted or upon tax triggers.

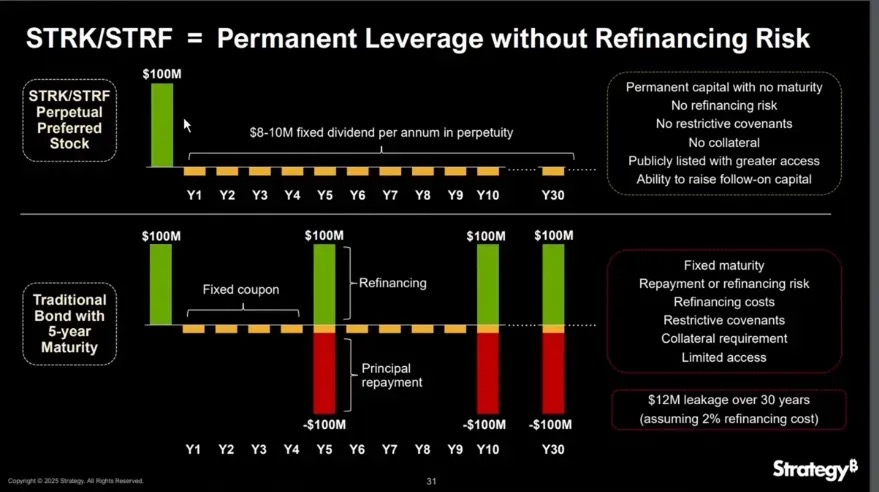

In the capital structure, STRF and STRK rank above common stock but below debt.

These instruments become crucial when mNAV < 1. Issuing common stock at a discount would dilute BTC/share and destroy value. But preferred stocks like STRF and STRK allow the company to raise capital without diluting common equity—whether to buy more BTC or repurchase shares—maintaining BTC/share stability while growing assets.

How Are Dividends Paid?

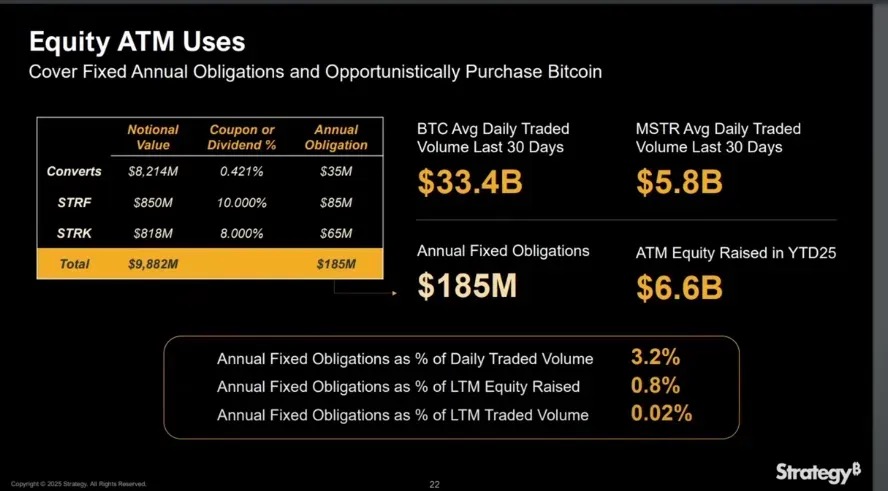

Year-to-date 2025, MicroStrategy has raised $6.6 billion via ATM (At-The-Market) stock offerings, far exceeding its annual $185 million fixed interest and dividend obligations.

When mNAV > 1, issuing equity to cover preferred dividends does not dilute BTC per share, because the incremental BTC purchased exceeds the per-share dilution.

Additionally, preferred stock is not counted as debt, allowing MicroStrategy to expand its balance sheet without worsening its net leverage ratio—an essential factor in maintaining market confidence in its capital structure.

When mNAV > 1

Convertible Bonds

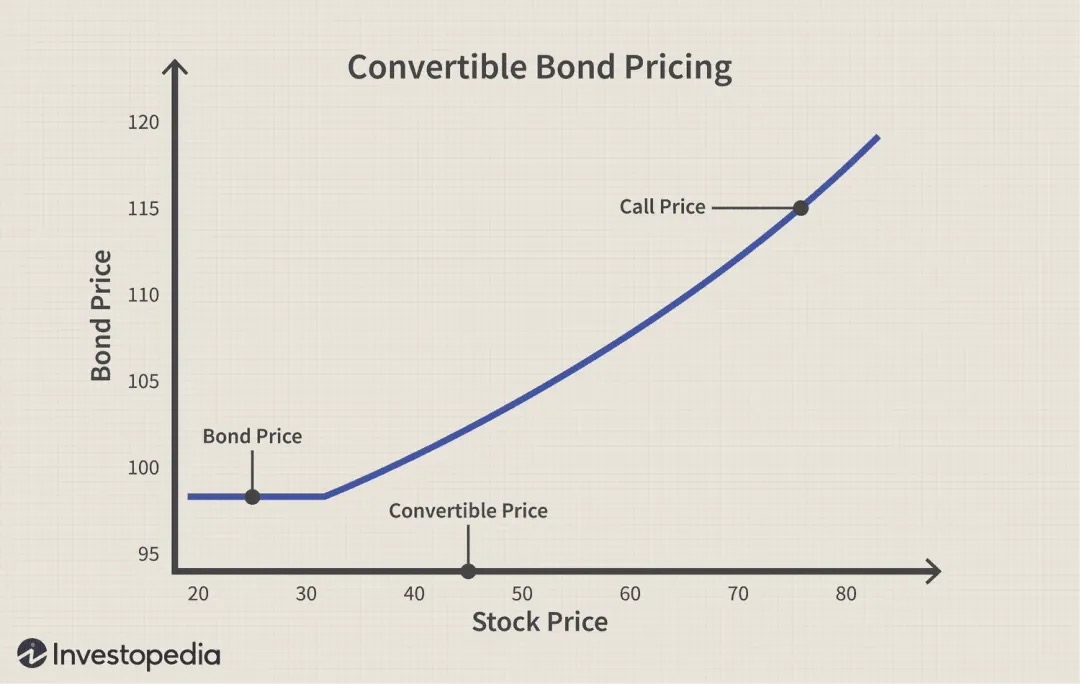

Convertible bonds are corporate debt instruments that give holders the right (but not obligation) to convert the bond into shares of the issuer at a predetermined price (conversion price). They are essentially structured as “bond + call option.” These are particularly useful when mNAV > 1, as they enable efficient BTC accumulation.

Take MicroStrategy’s 0% convertible bonds as an example:

-

No interest payments during the bond’s life;

-

Only principal repayment due at maturity (unless investors choose to convert);

-

For MSTR, this is a highly capital-efficient tool: it can raise billions to buy BTC with no immediate dilution and no interest burden. The only risk is having to repay principal if the stock underperforms.

Scenario One: Stock Price Rises Above Expectations

-

MicroStrategy issues convertible bonds to investors;

-

Company receives $3 billion immediately to buy BTC;

-

No interest paid during bond term (0% coupon);

-

If MSTR’s stock price rises above the conversion price;

-

Investors choose to convert bonds into shares or take cash;

-

MicroStrategy delivers shares instead of cash, avoiding cash outflow.

Scenario Two: Stock Price Falls Below Conversion Price

-

MicroStrategy issues convertible bonds to fund BTC purchases;

-

0% interest rate means no payments during term;

-

MSTR stock remains below conversion price;

-

Investors don’t exercise conversion, as it would result in a loss;

-

At maturity, the company must repay the full principal in cash;

-

If cash reserves are insufficient, MicroStrategy may need to refinance to repay the debt.

It’s important to emphasize: convertible bonds are fundamentally a combination of “plain bond + call option,” and this is especially clear in MicroStrategy’s case. The company keeps issuing 0% coupon convertibles, meaning investors receive no interest income during the bond’s life.

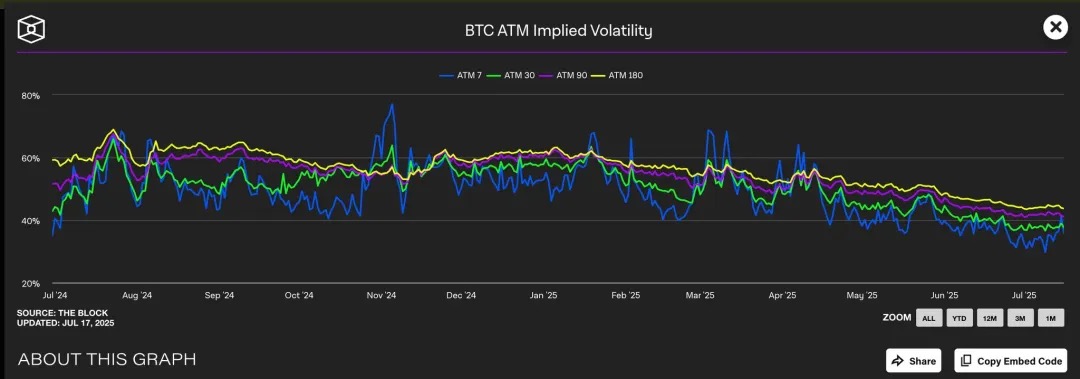

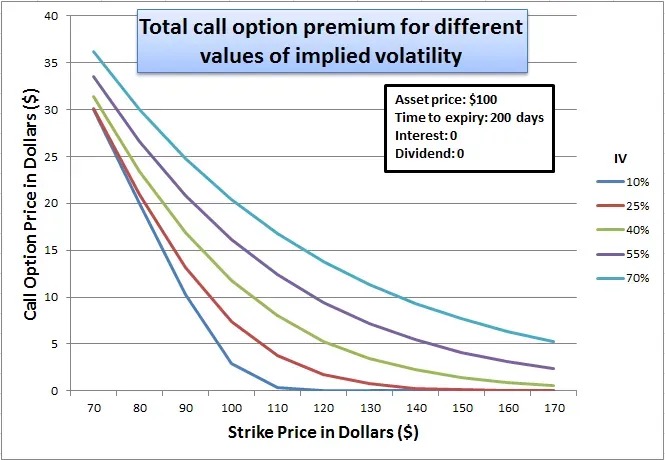

Why would sophisticated institutional investors accept such a seemingly unattractive structure? The answer lies in the embedded call option: this embedded call option becomes highly valuable when the market expects high implied volatility (IV) in MSTR’s stock. The greater the expected price swings, the higher the option’s value.

We observe that Bitcoin’s implied volatility (IV) typically ranges between 40% and 60% across different tenors. Since MicroStrategy’s stock price is highly correlated with Bitcoin, this elevated BTC IV indirectly inflates the valuation of MSTR stock options.

Currently, at-the-money call options (strike ~$455) trade at 45% IV, while put options show even higher IV, indicating strong market expectations for future volatility. This high-volatility environment significantly boosts the value of the embedded call options in MSTR’s convertibles.

In essence, MicroStrategy is effectively “selling” this call option at a premium. The higher the volatility of the underlying asset, the greater the probability the option ends up in-the-money—and thus, the more expensive it becomes.

From the investor’s perspective, this is acceptable because they are essentially making a leveraged bet on volatility: if MSTR’s stock surges, they convert and capture massive gains; if it doesn’t, they still get their principal back at maturity.

For MSTR, this is a win-win: it raises capital without paying interest or immediately diluting shareholders. And if the Bitcoin strategy succeeds, it can service or refinance the debt purely through stock appreciation. In this framework, MSTR isn’t just borrowing—it’s “monetizing volatility,” converting future upside into cheap capital today.

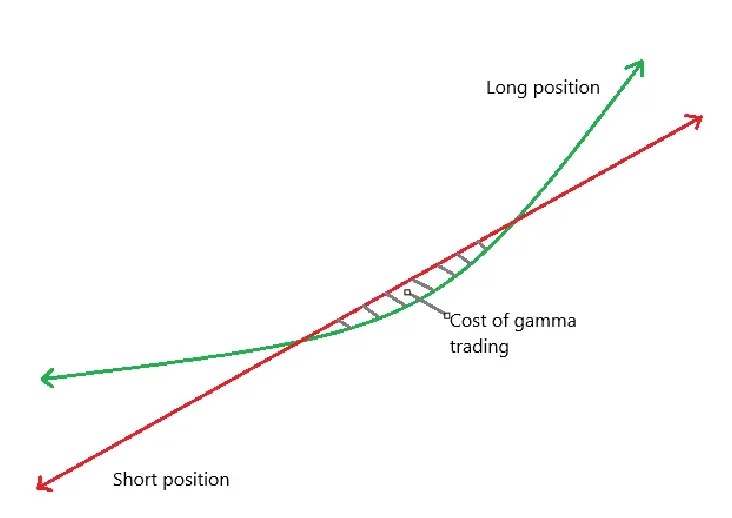

Gamma Trading

Gamma Trading is the core mechanism ensuring the sustainability of MicroStrategy’s capital structure, especially given its repeated issuance of zero-coupon convertibles. The company has issued billions in such bonds, whose appeal isn’t rooted in traditional fixed-income returns, but in the value of the embedded call option. In other words, investors aren’t buying for interest income, but for the trading and volatility arbitrage opportunities within the option component.

These bond buyers aren’t traditional long-term creditors, but hedge funds employing market-neutral strategies. These institutions engage in what’s known as Gamma Trading—their logic isn’t “buy and hold,” but continuous hedging and rebalancing to profit from volatility.

Gamma Trading Mechanism in MSTR:

Basic Trade Structure:

-

Hedge funds buy MicroStrategy’s convertible bonds (essentially bond + call option);

-

Simultaneously, they short an equivalent amount of MSTR stock to maintain delta neutrality.

Why It Works:

-

If MSTR’s stock price rises, the gain on the embedded call option outpaces the loss on the short stock;

-

If the stock price falls, the gain on the short position exceeds the bond’s loss;

-

This symmetric payoff allows hedge funds to profit from volatility, not directional moves.

Gamma and Rebalancing Mechanism:

-

As the stock price fluctuates, hedge funds must continuously adjust their short positions to stay delta neutral;

-

Initial hedge is set based on the bond’s delta—for example, if a convertible has a delta of 0.5, the fund shorts $50 worth of stock for every $100 bond;

-

But as the stock moves, the bond’s delta changes (this is gamma in action), requiring ongoing dynamic rebalancing:

-

Stock rises → delta increases (bond behaves more like stock) → add to short position;

-

Stock falls → delta decreases (bond behaves more like debt) → cover short position;

-

This constant “sell high, buy low” hedging activity is known as Gamma Trading.

-

In practice, the bond’s delta changes nonlinearly with the stock price, requiring continuous adjustment of the short hedge.

-

Green curve: return from holding the convertible;

-

Red line: return from short stock;

-

Their difference is net P&L;

-

When the stock is flat near the conversion zone, frequent hedging can actually lead to losses—this is the “cost zone” of Gamma Trading (shaded area).

Impact on MSTR’s Premium:

-

These gamma traders are not long-term holders;

-

When MSTR reaches the conversion price, delta → 1, gamma drops to near zero;

-

If volatility falls or spreads narrow, gamma trading becomes unprofitable, and these funds exit, weakening demand for convertibles.

Second-Order Effects:

-

MicroStrategy’s convertibles are typically zero-coupon with long duration → low theta (time decay);

-

When volatility is too low, gamma trading stops being profitable, and gamma PnL ≪ theta decay;

-

Convertible sales become difficult, impairing financing ability.

Short float comparisons illustrate the dominance of this strategy:

Short float refers to the percentage of shares sold short relative to total shares outstanding. We observe that MicroStrategy has a very high short float due to its extensive issuance of convertibles, as gamma traders must short MSTR stock to maintain delta-neutral hedges.

In contrast, SBET has not issued convertibles, relying instead on PIPE private placements and ATM follow-ons. It lacks the convertible+option structure that enables arbitrage, resulting in a much lower short float. SBET’s financing model resembles traditional equity issuance and fails to attract large-scale arbitrage-driven institutions.

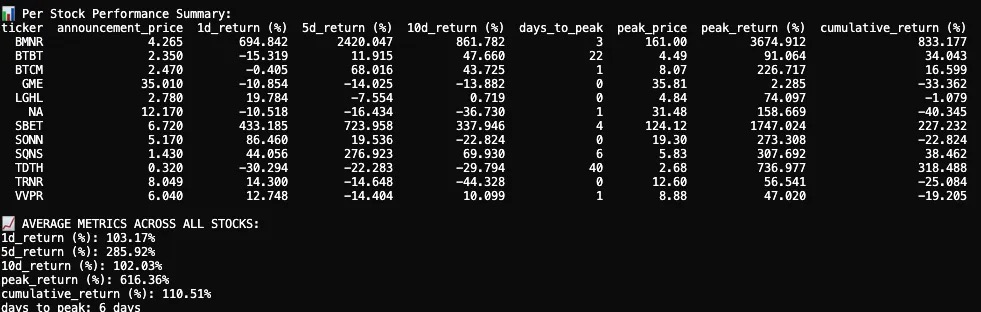

Performance

I tracked and analyzed the stock price reactions of 12 public companies after their 2025 announcements of crypto asset allocation. Our dataset includes pre- and post-announcement stock data, visual candlestick charts, and key performance metrics.

On average, the stock reaction following a first-time crypto treasury announcement in 2025 was explosive, short-lived, yet delivered positive cumulative returns.

Across the 12 firms, the average 1-day return was +103.17%, showing strong immediate investor response. The 5-day return surged further to +285.92%, peaked at day 10, then settled at +102.03%. While some companies showed muted or negative results, several experienced extreme price spikes.

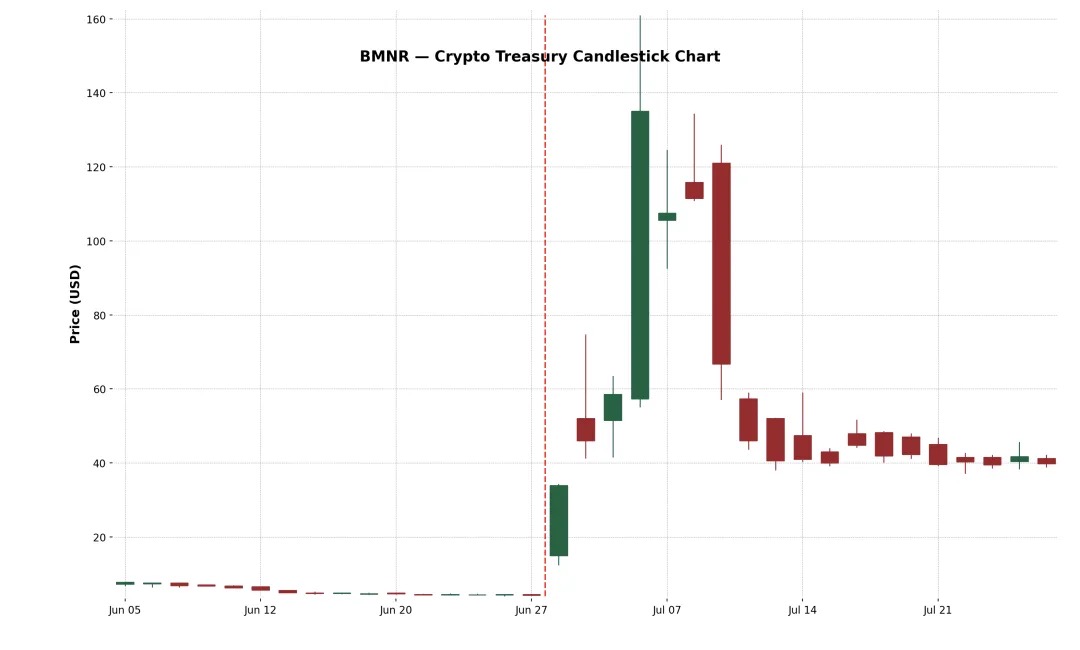

Example 1: BitMine Immersion Technologies Inc. (NYSE-American: BMNR)

A Las Vegas-based blockchain infrastructure company, BMNR operates industrial-scale Bitcoin mining farms, sells immersion cooling hardware, and provides colocation services for third-party equipment in low-cost electricity regions like Texas and Trinidad. On June 30, 2025, the company raised ~$250 million through a private placement of 55.6 million shares at $4.50 each, to expand its Ethereum treasury.

Following the announcement, BMNR’s stock surged from $4.27 to a high of $161, a 3-day gain of +3,674.9%. This historic rally was likely fueled by a thin float, retail enthusiasm, and FOMO momentum. Despite sharp corrections, the two-week cumulative gain remained +882.4%. This event highlights the market’s positive feedback toward a “MicroStrategy-style” high-conviction crypto treasury strategy.

Example 2: SharkLink Gaming Ltd. (Nasdaq: SBET)

Founded in 2019, SharpLink is a tech company focused on turning sports fans into bettors, using real-time data to deliver personalized sports betting and interactive game promotions. In 2025, the company began accumulating ETH on its balance sheet, funded through PIPE and ATM offerings.

The initial reaction was extremely strong: SBET rose +433.2% on day one, peaking at +1,747% on day four. The surge was driven by the scale of ETH acquisition and backing from prominent figures. Retail investors, crypto funds, and speculators rushed in, driving the stock above $120.

However, the rally was short-lived. On June 17, SharpLink filed an S-3 registration with the SEC, allowing PIPE investors to resell shares, causing widespread confusion. Many mistakenly believed insiders were dumping shares. Although Joseph Lubin, co-founder of Consensys and SBET chairman, later clarified “no shares have been sold,” it was too late: SBET plunged nearly 70%, erasing most of its post-announcement gains.

Despite the sharp correction, SBET’s cumulative return remained +227.2%, indicating the market still assigns significant long-term value to its ETH treasury strategy. After pulling back from highs, the stock began regaining institutional support in subsequent weeks, suggesting renewed confidence in the “Ethereum as reserve asset” model.

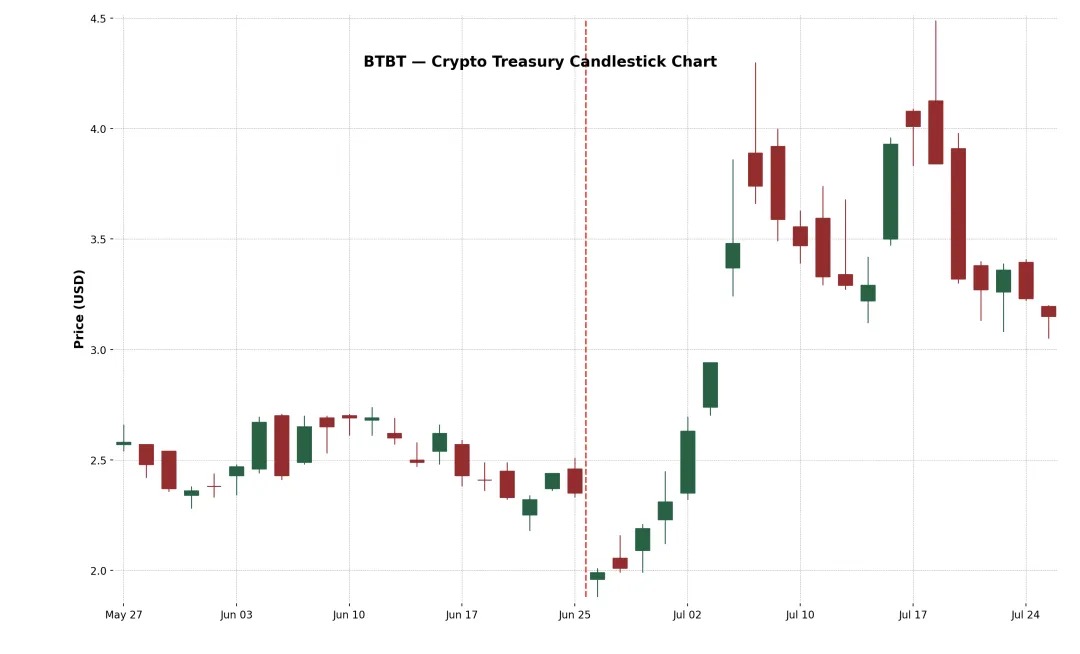

Example 3: Bit Digital Inc. (Nasdaq: BTBT)

BTBT is a New York-based digital asset platform founded in 2015, originally operating Bitcoin mining facilities in the U.S., Canada, and Iceland.

In June 2025, the company completed an underwritten offering raising ~$172 million, and used additional proceeds from selling 280 BTC to reconfigure its capital into ETH, purchasing approximately 100,603 ETH. This marked its official transition to an Ethereum staking and treasury model, with crypto veteran Sam Tabar as CEO.

The initial market reaction was weak (down –15% on day one), but the stock gradually rose over the next two weeks, ultimately gaining +91%. This muted response may reflect market familiarity with BTBT’s existing crypto-mining background. Nevertheless, a +34% cumulative return shows even established crypto firms can earn positive recognition for expanding their crypto asset allocation.

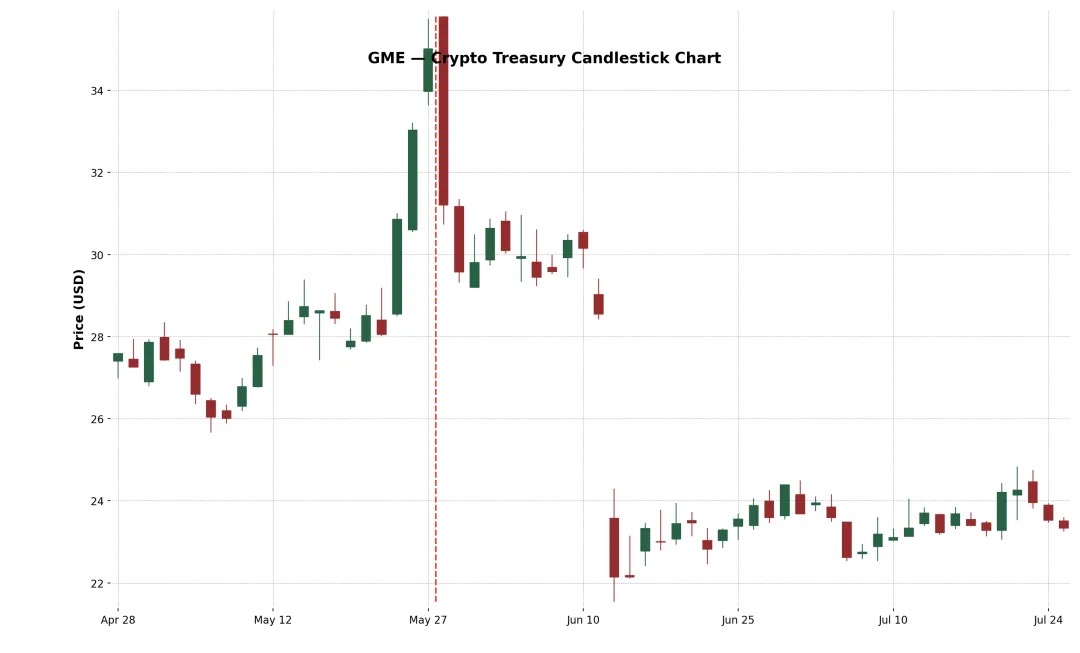

Example 4: GameStop Corp. (Nasdaq: GME)

GameStop (GME) announced its first Bitcoin purchase in May 2025, with plans to transform into a consumer-facing crypto gaming infrastructure company. Despite intense retail attention and the symbolic significance of a cultural meme stock entering crypto, GME posted negative returns on day 5 and day 10. This divergence reveals a key insight: favorable crypto news alone is insufficient to sustainably lift a stock.

GameStop’s Bitcoin initiative faced skepticism due to its declining retail business and a history of strategic pivots (stores, NFTs, metaverse). It failed to sustain momentum, reflecting doubts about its fundamentals and strategic clarity. Core revenues continue to fall, and management has offered no concrete reform beyond “buying Bitcoin.” The messaging—from stores to NFTs to metaverse to now crypto—is inconsistent, severely undermining market confidence.

Crypto Asset Allocation Trends

Beyond Bitcoin, more companies are increasingly choosing Ethereum (ETH) as a core reserve asset. There are several reasons. First, Ethereum is widely seen as the foundational infrastructure for tokenizing real-world assets (RWA), with protocols like Ondo, Backed Finance, and Centrifuge building institutional-grade financial products on Ethereum’s settlement layer. This makes ETH a strategic reserve asset for firms betting on the “on-chain traditional finance” trend.

Second, unlike Bitcoin, Ethereum is stakable and DeFi-composable, allowing holders to earn ~3–4% annual yield by securing the network. This programmable, income-generating nature makes ETH highly attractive to CFOs seeking to optimize idle cash returns.

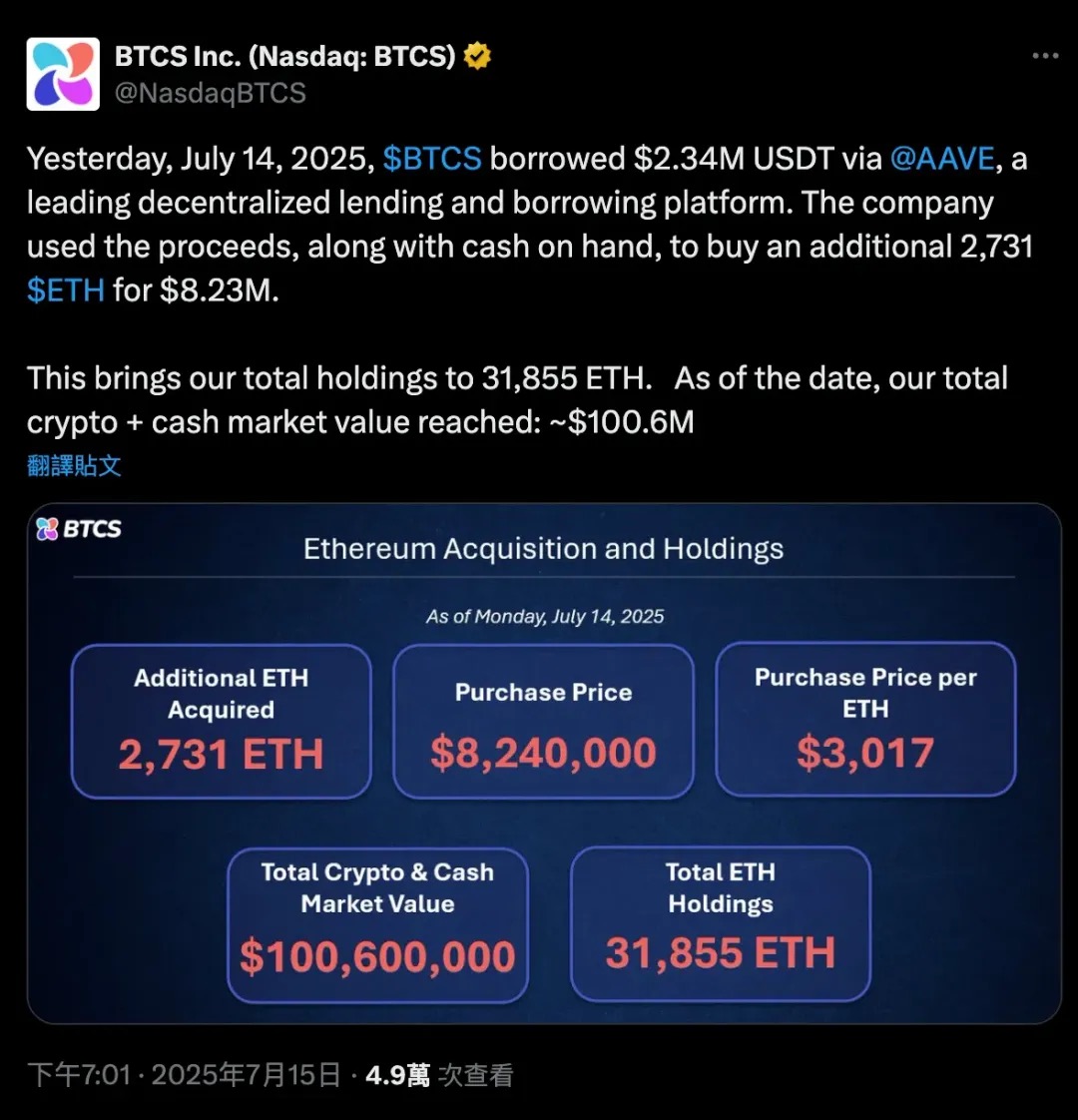

On July 14, 2025, BTCS borrowed 2.34 million USDT via Aave (a decentralized lending protocol), combined with some cash, to purchase 2,731 ETH (~$8.24 million), expanding its ETH holdings. This leveraged transaction brought BTCS’s total ETH position to 31,855 ETH, increasing its total crypto+cash market cap to $100.6 million.

This case clearly demonstrates Ethereum’s dual role in DeFi—as both collateral and productive capital. Bitcoin is largely a passive “cold wallet” asset, requiring wrapping to enter DeFi; ETH, however, is natively composable, enabling enterprises to lend, stake, or earn yield without selling their holdings.

The launch of spot Ethereum ETFs further boosted institutional confidence and liquidity in ETH, with net inflows signaling growing acceptance in mainstream finance. As a result, SharpLink (SBET), Bit Digital (BTBT), and even non-public firms are adjusting their balance sheets to increase ETH holdings—not just speculative bets, but expressions of long-term belief in “Ethereum as decentralized capital market infrastructure.”

This trend marks a major shift in corporate crypto strategy: from “Bitcoin = digital gold” to “Ethereum = digital financial infrastructure.”

Here are several examples of this diversified approach:

-

XRP as reserve asset: VivoPower International (NASDAQ: VVPR) raised $121 million in May 2025, led by a Saudi prince, becoming the first public company to adopt an XRP reserve strategy. Soon after, Singapore’s Trident Digital Holdings (TDTH) announced plans to issue up to $500 million in stock to build an XRP reserve; China’s Webus International (WETO) also filed to allocate $300 million to XRP holdings and integrate Ripple’s cross-border payment network into its operations. These moves followed Ripple’s legal compliance breakthrough in the U.S. Market reactions varied—XRP rose in mid-2025, but stock performances diverged—yet they signal that crypto treasury strategies are moving beyond the BTC-ETH duopoly.

-

Litecoin (LTC) reserves: MEI Pharma (MEIP), a small biotech firm, unexpectedly announced a transformation in July 2025, raising $100 million with participation from Litecoin founder Charlie Lee and the Litecoin Foundation, creating the first institutional-grade LTC reserve. The plan included board changes (Lee joining), viewed as an attempt to inject crypto capital into a struggling biotech sector. The stock surged on the “biotech + Litecoin” news, but volatile trading followed due to uncertainty about its ultimate business model.

-

HYPE Token reserves: A more “unconventional” case is Sonnet BioTherapeutics (SONN), which in July 2025 announced an $888 million reverse merger to form Hyperliquid Strategies Inc., planning to place $583 million in HYPE tokens on its balance sheet. Backed by top crypto VCs like Paradigm and Pantera, the goal is to create the largest publicly listed HYPE holder. SONN’s stock spiked post-announcement (as HYPE is a popular token), but analysts noted structural complexity and the token’s early stage. Similarly, Lion Group (LGHL) secured a $600 million credit line to reserve HYPE, Solana, and Sui tokens, building a multi-asset crypto treasury.

When Will Saylor Sell?

Michael Saylor has publicly declared that MicroStrategy will “HODL forever”—meaning the company has no intention of selling its BTC reserves. In fact, MicroStrategy has formally amended its policy to designate Bitcoin as its primary treasury reserve asset, signaling an extremely long-term holding strategy. However, in the real world of corporate finance, “never sell” isn’t absolute. Certain scenarios could force MicroStrategy to sell BTC. Understanding these potential triggers is critical, as they represent risks to the entire “MSTR as a proxy for Bitcoin” investment thesis.

The following are situations that could challenge MicroStrategy’s resolve and “force” BTC sales:

-

Major debt maturity during tight credit conditions: MicroStrategy currently has several debts outstanding, including convertible bonds maturing in 2028 and 2030 (it previously refinanced 2025 and 2027 bonds via equity issuance), and possibly other loans. Typically, the company refinances old debt—issuing new bonds or shares. In early 2025, MicroStrategy successfully retired its 2027 convertible bonds with stock, avoiding cash outlays. But imagine a scenario: in 2028, Bitcoin enters a deep bear market, MSTR’s stock crashes, and interest rates are high (making new financing prohibitively expensive). If $5–10 billion in debt comes due, the company could face a cash crunch.

-

In such a scenario, traditional capital markets might “close the door,” especially if implied volatility (IV) is too low, making investors unwilling to buy convertibles with embedded options—MicroStrategy’s favorite financing tool would fail.

-

Facing such a credit crunch, the company might have to sell some BTC to repay debt—akin to a “forced liquidation.” Though MicroStrategy holds a massive BTC stash (worth over $70 billion as of 2025), any sale would shake market confidence. Such a move would likely be a last resort, only after all other financing avenues fail.

-

Heavy interest burden or preferred dividend pressure: While flexible, MicroStrategy’s capital structure isn’t cost-free. In 2025, the company faces fixed obligations including:

-

STRK: 8% annual dividend (payable in cash or stock)

-

STRF: 10% annual cash dividend (must be paid in cash; default incurs penalties)

-

STRC: 9–10% monthly interest (cash payment, adjustable by board)

-

Convertible bond coupons (e.g., 0.625% for 2030 bonds)

Total fixed liabilities exceed $185 million annually and could rise with future issuances.

-

If MSTR’s stock is weak, issuing new shares would cause severe dilution.

-

If crypto winter hits, MicroStrategy could burn cash maintaining STRF and STRC cash payouts. If BTC remains depressed long-term, its leveraged structure becomes risky. The board might decide to sell some BTC to “buy time,” covering one to two years of interest/dividends. This contradicts the original intent, but is preferable to default or triggering STRF’s cumulative penalty clauses.

-

What if interest rates keep rising? Then all future financing becomes more expensive:

New preferred stock must offer higher yields (>10%) to attract investors;

Convertibles must come with higher implied volatility to be marketable (hard to achieve in a bear market);

If MSTR’s stock is weak, equity issuance causes severe dilution.

In short: rising capital costs, stagnant income, and low BTC prices.

Summary: MicroStrategy would only sell BTC under extreme financial stress or strategic shifts. These scenarios relate to refinancing difficulties, high capital costs, or market discounts to NAV. Under normal conditions, Saylor’s strategy is to keep buying or holding, not selling. Indeed, the company has already demonstrated this resolve: during the 2022–2023 crypto crash, unlike Tesla, MicroStrategy did not sell BTC. Instead, it quietly repurchased some convertibles in secondary markets—achieving “discounted debt repayment”—always choosing alternatives over selling Bitcoin, because selling would collapse the entire “Bitcoin treasury” narrative and shatter market faith.

Conclusion

MicroStrategy (MSTR) has pioneered a new corporate finance model, transforming a public operating company into a leveraged Bitcoin holding vehicle. By aggressively leveraging capital markets—especially zero-coupon convertibles—MSTR has monetized its stock volatility to accumulate over 600,000 BTC, independent of operating cash flow.

Its core mechanism is simple yet powerful: when the company’s stock trades at a premium to its BTC net asset value (mNAV > 1), it issues stock or convertibles (like the “21/21” or “42/42” programs), uses the proceeds to buy BTC. Because MSTR’s stock has long traded above its BTC market value, this cycle sustains itself, allowing the company to increase BTC per share while raising capital.

At the heart of this model, convertibles play a crucial role: they combine bond-like downside protection (“bond floor”) with equity-like upside (embedded call option). In high-volatility environments (like 2025), investors accept 0% interest because the option value is high. Effectively, MSTR isn’t just borrowing—it’s “selling volatility” at a premium. The market pays upfront for future growth potential, enabling endless rounds of interest-free, non-dilutive financing to buy BTC.

But this model has limits: if implied volatility contracts (due to market maturity or BTC stagnation), the embedded option loses value, making future convertible issuance far less attractive. The company may then rely on traditional financing or face cash repayment at maturity. Moreover, the “gamma traders” and volatility arbitrageurs sustaining MSTR’s financing ecosystem are opportunistic. If volatility drops or sentiment shifts, demand for its securities could vanish overnight. This isn’t “delta risk” (everyone

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News