The evolution and transformation of the global financial system

TechFlow Selected TechFlow Selected

The evolution and transformation of the global financial system

In the next wave of traditional finance migration to the blockchain, RWA tokenization will become mainstream, with substantial physical assets—from real estate and U.S. equities to private equity—being fractionalized into on-chain tokens.

Author: Andy, epochChain

Evolution and Transition of the Global Financial System

Background Introduction

The Age of Exploration: The Birth of Finance (15th–17th Centuries)

The Age of Exploration laid the foundation for financial system development. To meet the massive capital demands of long-distance maritime trade, the Dutch East India Company innovatively issued stocks, pricing and dividing "trade revenue rights" into tradable units—achieving asset tokenization. This allowed ordinary people to invest in overseas trade and share profits. At the same time, marine insurance emerged, enabling shipowners to transfer transportation risks by paying premiums. These pooled premiums formed a risk-sharing fund—the early model of risk diversification and pricing. In international trade, gold and silver, due to their scarcity and universally recognized value, became core settlement instruments, solving trust issues across different currency systems. At this stage, the financial system initially acquired three core functions: profit generation (stock investment), risk hedging (marine insurance), and value settlement (precious metals). These functions supported each other, serving trade expansion and forming the prototype of a modern financial system.

Silver-Based Monetary System and Hegemonic Shifts (19th Century)

In the 19th century, Qing China, leveraging its strong competitiveness in tea, silk, and other goods, played a major role in global trade. Massive exports attracted global silver inflows, creating a cycle of “Chinese goods – global silver,” where silver became the core settlement currency in world trade—an arrangement effectively anchored by Chinese goods. As cross-border trade expanded, stock trading spread from Europe globally, and insurance extended from shipping to commodity transport, but the core logic remained focused on “pricing assets and underwriting risks.” However, the Opium Wars disrupted this order. Britain plundered Chinese silver through war, weakened China’s monetary base, and leveraged its gold reserves to promote the gold standard, redefining global settlement rules—demonstrating how national power determines the status of settlement media.

Bretton Woods System and the Dollar Era (20th Century)

The 1944 Bretton Woods Agreement established a system where “the dollar was pegged to gold, and other currencies to the dollar,” shifting the global settlement system from precious metals to national credit. The U.S. dollar became the central nervous system of global finance. During this period, stock markets became increasingly interconnected globally, with exchanges like New York and London emerging as key centers. The insurance industry adopted sophisticated actuarial models, while derivatives were used to hedge commodity prices. Financial markets evolved around more precise asset pricing and efficient risk hedging. In this system, the dollar dominated settlements, stock markets enabled asset trading, and insurance and derivatives managed risk hedging—these three functions worked more cohesively, driving the post-war economic recovery and global financial operations.

Later, after the collapse of the Bretton Woods system, the U.S. quickly reached agreements with oil-rich nations like Saudi Arabia, anchoring the dollar to oil—ushering in the petrodollar era and extending dollar hegemony. However, by 2024, Saudi Arabia announced that oil would no longer be settled exclusively in dollars, marking the end of the petrodollar era and signaling a reshaping of the global monetary landscape.

Modern Finance: Complexity and Return to Essence (21st Century)

Entering the 21st century, financial innovation reached new heights with the emergence of derivatives, commodity futures, structured products, and other complex instruments. Financial transaction structures and product designs grew increasingly intricate. While these innovations improved market efficiency and met diverse needs, the core of finance remained centered on “returns, risk, and settlement.” Complex tools represent an extension and evolution of traditional financial functions in new environments—the “technique” evolving—while the three core functions embody the enduring “principle,” reflecting finance’s fundamental purpose: serving the real economy and optimizing resource allocation.

Rise of Emerging Financial Models: The Birth of DeFi and CeFi

DeFi: Blockchain-Powered Decentralized Financial Systems

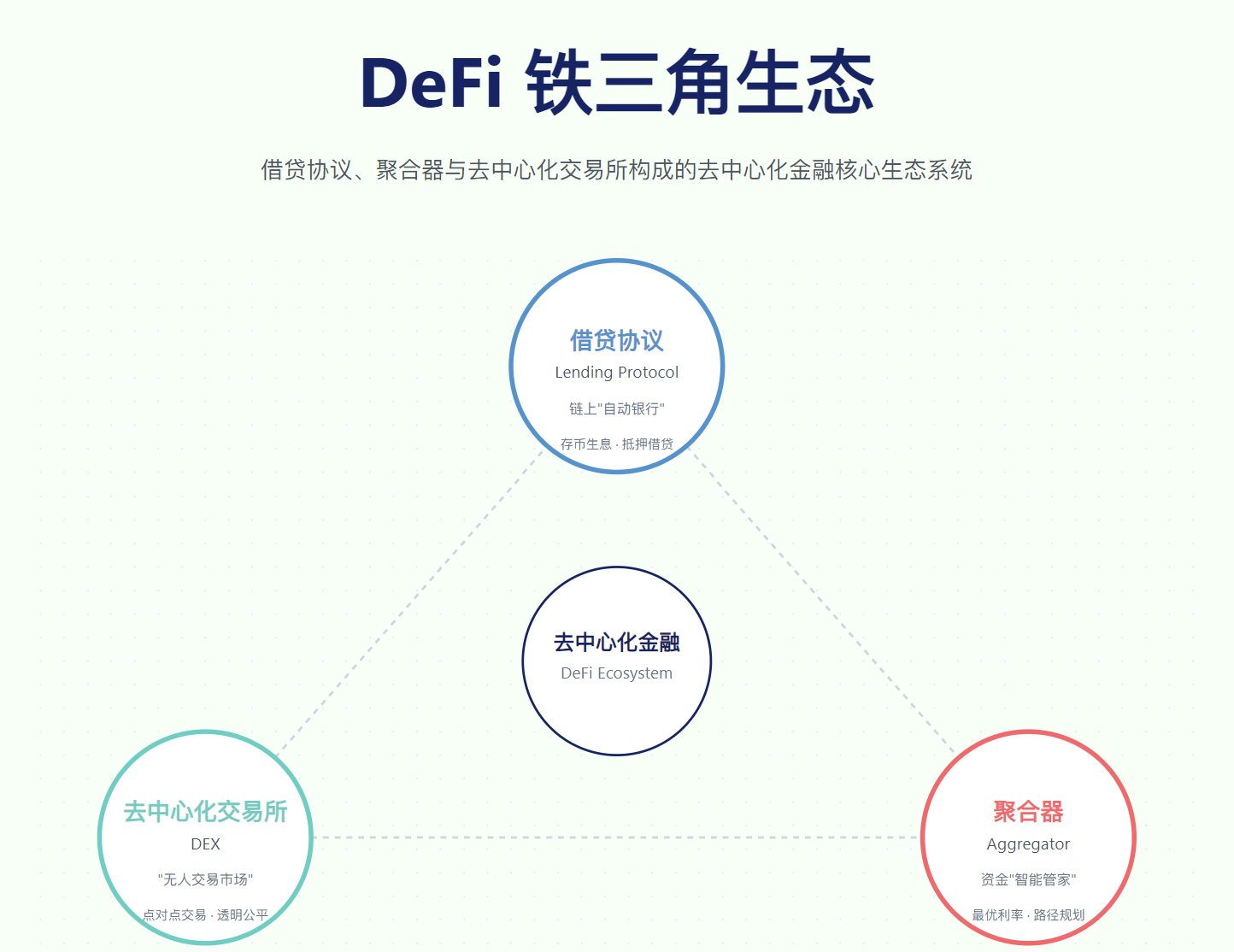

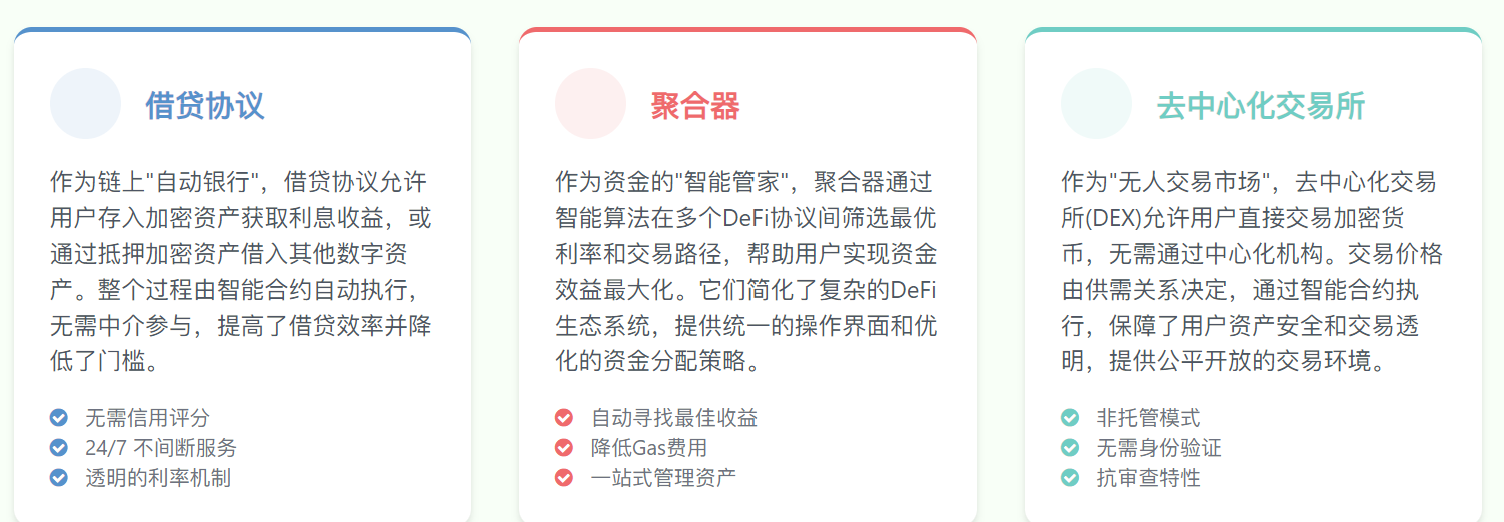

The breakthrough of Ethereum smart contract technology in 2015 provided the technical foundation for DeFi's rise. Smart contracts enable financial rules to execute automatically via code, eliminating the need for traditional intermediaries and transforming financial transactions. Within the DeFi ecosystem, the “DeFi Trinity” plays a crucial role. Fundamentally, DeFi replicates the core functions of traditional finance, using blockchain technology to achieve “no intermediaries, fully open, automated” operations—injecting new vitality into the financial system.

CeFi: The Centralized Bridge Connecting Traditional and Decentralized Finance

Despite its innovative advantages, DeFi faces challenges such as high technical barriers and regulatory uncertainty. CeFi emerged as a bridge between traditional finance and DeFi, acting as a “converter.”

Its main role is simple: helping users convert fiat currencies (like RMB or USD) into cryptocurrencies (like Bitcoin or Ethereum) and vice versa, making it easier to move money between traditional finance and DeFi; simplifying DeFi operations with user-friendly interfaces to lower participation barriers; securely safeguarding user assets; and, within compliance boundaries, fulfilling traditional institutions’ (such as banks and securities firms) demand for blockchain-based services, helping them explore on-chain business and promoting better integration between traditional finance and DeFi.

Integration of Traditional and Emerging Finance

Role Positioning and Challenges of the Three Systems

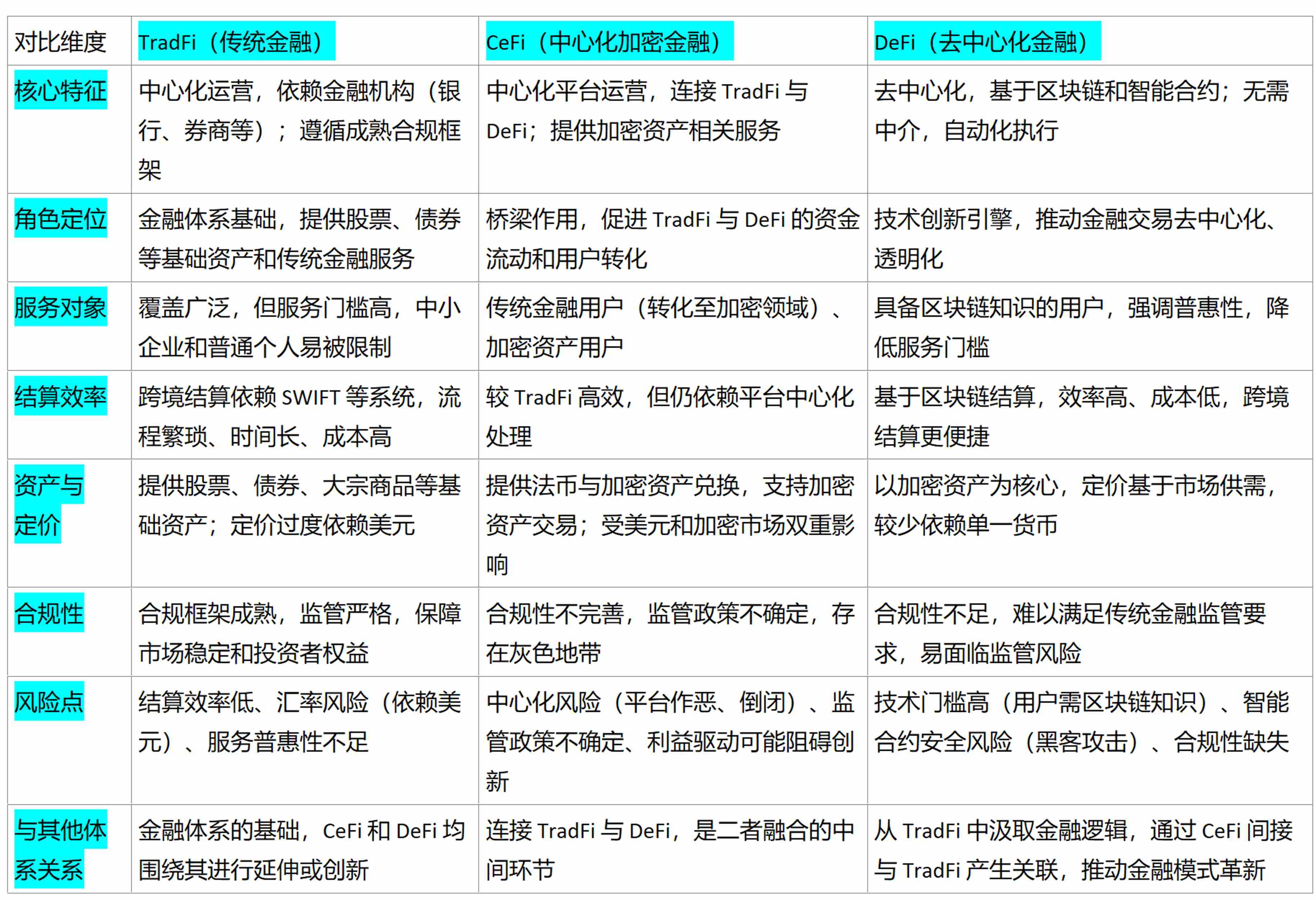

TradFi

TradFi refers to the traditional financial systems we interact with daily—like depositing money at banks, transferring funds, buying stocks or funds through brokers, or investing in gold and bonds.

For example: If you want to send $10,000 to a friend abroad but can’t do it directly, you must rely on a bank with cross-border services. The bank converts your RMB into the recipient’s local currency, charges fees and exchange rate spreads, then routes the transaction via the SWIFT system. This process requires filling out multiple forms, passing several reviews, and often takes days to settle—with hundreds of dollars potentially lost in fees. The bank manages the entire flow and assumes responsibility if something goes wrong.

This is the TradFi model—whether for cross-border transfers, stock purchases, or loans—intermediaries like banks and brokers set procedures, charge fees, and bear liability. Users cannot bypass them, leading to inefficiencies and high costs in cross-border settlements. Moreover, many economies depend heavily on dollar-denominated trade, making them vulnerable to fluctuations in the dollar exchange rate.

CeFi

CeFi refers to centralized crypto-financial platforms—essentially “bridges” between traditional finance and the cryptocurrency world. They provide conversion channels, simplify processes for non-technical users, and help traditional institutions (like banks and brokers) conduct compliant crypto-related businesses, promoting integration. However, they have flaws: regulation has not fully caught up, and platforms operate with significant autonomy. Sometimes, platforms may misuse user assets for profit.

For example: If you want to use your salary to buy Ethereum for crypto investments but find direct operation too complex, you can use a well-known crypto exchange’s CeFi platform. Simply deposit RMB via bank card, instantly convert it to Ethereum, and use the platform’s simplified earning features to generate returns. You don’t need to understand complex tech—the platform handles everything—but you must trust that the platform won’t run off with your funds.

DeFi

DeFi is “decentralized finance” built on blockchain technology—operating without banks or brokers, relying solely on self-executing smart contracts. Transactions are transparent and visible to all. It enables faster, cheaper transfers and lending, and anyone, regardless of wealth or location, can access its services if they understand blockchain operations. However, it comes with challenges: average users must first learn about wallets, private keys, and other technical concepts—a high barrier to entry. Also, if the code has vulnerabilities, hackers may exploit them to steal funds.

For example: If you hold Bitcoin and want to exchange it for Ethereum, you don’t need an exchange. On a DeFi platform, connect your wallet, select the exchange rate, and the smart contract automatically swaps your Bitcoin for Ethereum, sending it directly to your wallet. There’s no intermediary, fees are lower than on exchanges, and settlement is fast—but you must securely manage your wallet key, or you’ll lose your funds permanently.

Foundations of the 'Trifi' Ecosystem

Here, we introduce a new concept—the “Trifi” model (the fusion of TradFi + CeFi + DeFi). The on-chain migration of traditional finance is essentially the convergence of traditional finance (TradFi), centralized finance (CeFi), and decentralized finance (DeFi). Through gradual penetration and synergy, this process gives rise to “Trifi”—a new financial paradigm. This path reflects the deep evolutionary logic of finance—from fragmentation to interconnection, from competition to symbiosis—and “Trifi” represents the ultimate form and core outcome of this evolution.

Core Logic of Complementary Advantages: Value Coexistence in the Trifi Ecosystem

The reason TradFi, CeFi, and DeFi can integrate into a Trifi ecosystem lies in their complementary strengths. Through synergistic effects, they address pain points in both traditional and single-chain financial models, building a more resilient financial system.

For example: A traditional real estate company (a TradFi institution) owns commercial property worth $10 million. To improve liquidity, it legally tokenizes the property into “Token A” (each representing a fractional ownership), completes regulatory registration, and transforms physical assets into on-chain digital assets. Then, the company partners with a crypto exchange (a CeFi platform). Users deposit USD from their bank accounts through the platform’s compliant channel, converting it into stablecoins. Meanwhile, the company deposits Token A into the platform’s custodial account. After verification, the trading pair is listed. Investors can buy Token A using stablecoins, either holding it on the platform or withdrawing it to personal blockchain wallets. The platform connects fiat and crypto, provides a compliant trading environment for Token A, and paves the way for users to enter DeFi—acting as a cross-system bridge. Holders of Token A can then transfer it to a DeFi lending protocol. The protocol’s smart contract automatically reads on-chain data to assess Token A’s value, allowing users to borrow stablecoins using Token A as collateral. The entire lending and liquidation process is executed by code—no human intervention needed. DeFi provides decentralized financial tools, enabling real-world real estate assets to be used for on-chain lending—greatly enhancing capital efficiency. Together, the three systems complete the full-cycle migration of traditional assets from offline to on-chain.

In summary, TradFi provides capital, CeFi acts as the conduit, and DeFi offers technological infrastructure. Their integration allows the Trifi ecosystem to absorb massive traditional capital while unlocking the innovative potential of on-chain finance.

Building the Future Financial System: Trends and Development

The Core of Circulation: Evolution of Payment and Settlement

Transformation in Cross-Border Trade

In cross-border trade, blockchain technology is profoundly reshaping the international settlement system.

Take the Lightning Network as an example—it functions like a “fast lane” built on top of Bitcoin. Previously, small cross-border payments were slow and costly. Now, with Lightning, transactions settle in seconds with minimal fees. This accelerates cash flow and reduces costs for small businesses and individuals, encouraging greater participation in global micro-trade.

Regarding commodity trading—for instance, oil—Layer2 technology enhances transaction efficiency and lowers costs. It can also tokenize commodities, turning oil into digital tokens. Buyers and sellers no longer need cumbersome processes like letters of credit or manual shipping document exchanges. Instead, they trade these digital tokens via smart contracts, enabling instant settlement and significantly boosting transaction efficiency.

Innovation in Social and Inclusive Finance

Integrating payment functions into decentralized social platforms is becoming a trend.

New approaches are bringing financial services closer to everyday life—such as “on-chain red packets” and “peer-to-peer micro-transfers.” Previously, sending small amounts often incurred high fees or was restricted to specific platforms with complicated procedures. Now, on decentralized social platforms, transferring small sums via cryptocurrency is much easier—low fees, no convoluted steps. This is especially beneficial for unbanked or low-income populations in remote areas who previously had limited access to formal financial services. These innovations lower the barrier to entry, enabling broader participation.

Changing Role of Nations in Payment and Settlement

Nations will continue to play a dominant role in large-scale, high-risk cross-border settlements for the foreseeable future. Governments ensure stability and security through monetary policy, financial regulation, and international cooperation. For strategic resources like oil and minerals, countries strictly control settlement currencies and methods to safeguard economic security and national interests.

However, as blockchain technology matures, smaller and medium-sized cross-border settlements will gradually migrate onto blockchains. Governments can respond by introducing policies and regulations to guide and supervise blockchain use in these areas—supporting fintech innovation while maintaining oversight. This balanced approach strengthens national competitiveness in global financial markets.

Pricing Power and the Battle for Stablecoin Anchors

Challenges to Dollar Dominance

The U.S. dollar’s hegemony in global finance faces disruption in the digital currency era. The U.S. attempts to maintain its on-chain pricing power through regulations like the GENIUS Act. Most mainstream stablecoins (e.g., USDT, USDC) are currently pegged to the dollar. U.S. regulators oversee stablecoin issuers’ reserve assets and operational models to ensure tight dollar linkage, reinforcing the dollar’s central position. However, with the global economy becoming multipolar, other countries and regions are actively exploring regional settlement solutions to reduce reliance on the dollar.

Development of a Multipolar Stablecoin System

China is advancing research and pilot programs for its digital yuan, which features controllable anonymity and dual offline payment capabilities. Domestic pilots already cover retail, transportation, and government services. In the future, it could play a larger role in trade settlements along the Belt and Road Initiative, accelerating RMB internationalization. The European Union is also developing its own digital currency to strengthen Europe’s voice in global finance and mitigate the impact of dollar volatility. These regional initiatives challenge the dollar’s dominance in the stablecoin space, pushing the global financial system toward a multipolar structure—“dollar-led, multi-currency coexistence”—and fostering greater financial diversity.

New Opportunities: On-Chain Migration of Traditional Finance and DeFi 2.0

Trends in RWA Tokenization

RWA (Real World Asset) tokenization is a key direction for future financial development. Traditional assets like stocks, private equity, and real estate are being issued as tokens on-chain and integrated into DeFi ecosystems, serving as new collateral and trading instruments. For example, tokenized U.S. stocks allow investors to trade or lend stock tokens on DeFi platforms—expanding investment avenues and offering companies new financing options. Tokenizing private equity improves liquidity, while fractionalizing real estate lowers investment thresholds, enabling broader participation and profit-sharing. This tightly integrates traditional finance with DeFi, injecting new vitality into financial markets.

Core Goals and Development of DeFi 2.0

DeFi 2.0 aims to replicate complex traditional financial scenarios—building a “Wall Street on-chain.” Leveraging RWA such as tokenized stocks, it enables advanced financial activities like stock token lending and derivatives trading. Using smart contracts and blockchain, it brings complex financial products and strategies on-chain. Investors can pledge tokenized stocks to borrow capital for investment or purchase futures and options based on these tokens for risk management and speculation. This enriches DeFi’s product offerings, improving market efficiency and transparency.

Role of Traditional Financial Institutions

As regulations mature, traditional financial institutions are increasingly accepting crypto assets. Banks and asset managers are entering the crypto space through investments and partnerships, contributing to DeFi ecosystem development. They bring substantial capital, professional talent, and proven risk management expertise—helping elevate crypto assets to mainstream investment status. By leveraging brand recognition and customer bases, they promote crypto investment products, enhancing market credibility and liquidity. Their compliant operations encourage market standardization, creating favorable conditions for deeper integration between traditional and emerging finance.

Conclusion

In the next wave of traditional finance migrating on-chain, RWA (real-world asset) tokenization will become mainstream. From real estate and U.S. stocks to private equity, vast physical assets will be split into on-chain tokens—becoming “new meme coins backed by real assets”—ushering in a “meme season.” The Ethereum ecosystem, with its mature DeFi infrastructure and growing compliance support, will serve as the core platform for RWA tokenization. Through smart contracts, it will enable cross-chain asset flows, lending, and other functions—with the key breakthrough lying in the deep integration of RWA and DeFi.

Key focus areas include RWA tokenization, DeFi innovation within the Ethereum ecosystem, and compliant on-chain exchanges (such as Nasdaq’s blockchain platform). Unlisted companies can tokenize private equity through compliant processes and raise funds on-chain without traditional IPOs—lowering listing barriers. Meanwhile, TradFi provides assets and regulatory frameworks, while DeFi offers on-chain tools enabling “stacking” (e.g., using RWA as collateral to mint stablecoins, then reinvesting those stablecoins into other tokenized assets). Together, they drive a market shift from speculation to “financialization of on-chain real assets.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News