2025 H1 Crypto Funding Insights: $37B Total Funding Signals Recovery, Top VCs Still Hold Significant Influence

TechFlow Selected TechFlow Selected

2025 H1 Crypto Funding Insights: $37B Total Funding Signals Recovery, Top VCs Still Hold Significant Influence

Cryptocurrency venture capital investment surged to $37 billion in the first half of 2025.

Author: Marco Manoppo

Translation: TechFlow

The first half of 2025 marked a turning point for cryptocurrency venture capital. After two years of capital constraints and investor caution, funding surged dramatically. By June 30, disclosed crypto financing had exceeded $37 billion across more than 150 tracked deals, spanning seed, Series A–C, strategic rounds, and IPOs. Despite regulatory uncertainty and persistent token price volatility, institutional and venture capital confidence in the sector has strongly returned.

Key Takeaways:

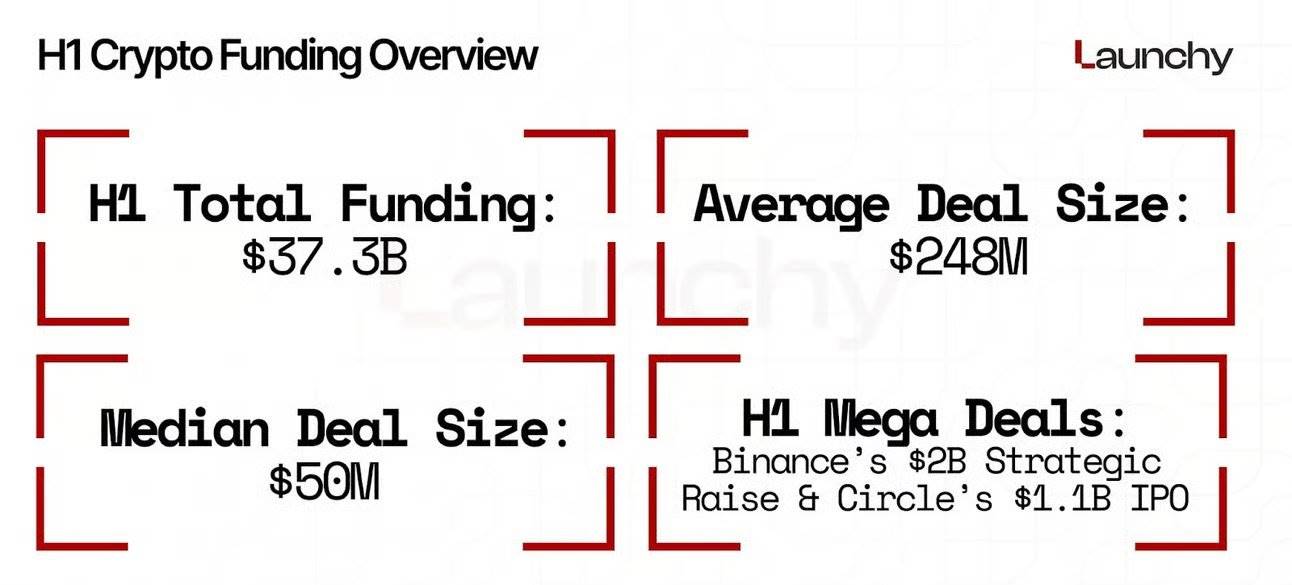

• In the first half of 2025, disclosed crypto funding surpassed $37 billion—the most active period since the 2021 bull run—with over 150 tracked deals.

• Large-scale financings such as Binance’s $2 billion strategic round and Circle’s $1.1 billion IPO pushed the average deal size to $248 million, signaling renewed market confidence in mature platforms.

• Capital shifted away from consumer-facing applications and speculative projects, flowing instead into scaling solutions, compliant infrastructure, and cross-chain protocols.

• Approximately $700 million was invested in AI-related crypto projects, indicating that investors view this intersection as the next major innovation frontier.

• Top investors including a16z crypto, Paradigm, Pantera, Galaxy Digital, and Sequoia accounted for about 40% of the highest-valued rounds, underscoring the continued influence of major funds on the direction of the crypto industry.

Overall Funding Overview

From January to June 2025, crypto and blockchain startups raised approximately $37.3 billion in disclosed funding.

The average deal size was around $248 million—significantly higher than previous years. This average is skewed by several mega-rounds and IPOs, such as Binance’s $2 billion strategic financing and Circle’s $1.1 billion IPO. The median deal size was closer to $50 million, reflecting that most fundraising rounds remain within the mid-market range.

This funding volume makes the first half of 2025 one of the most active periods since the 2021 bull market. Notably, substantial capital flowed into infrastructure and scaling solutions, not just consumer-facing applications.

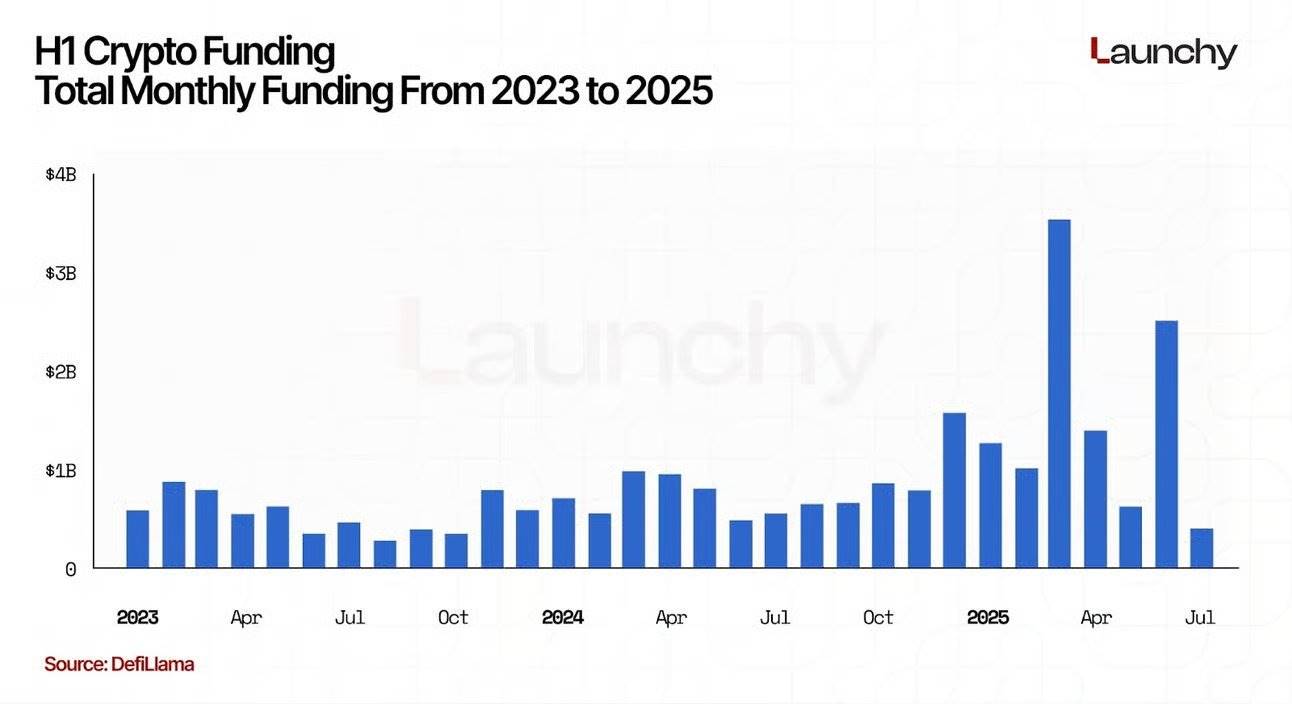

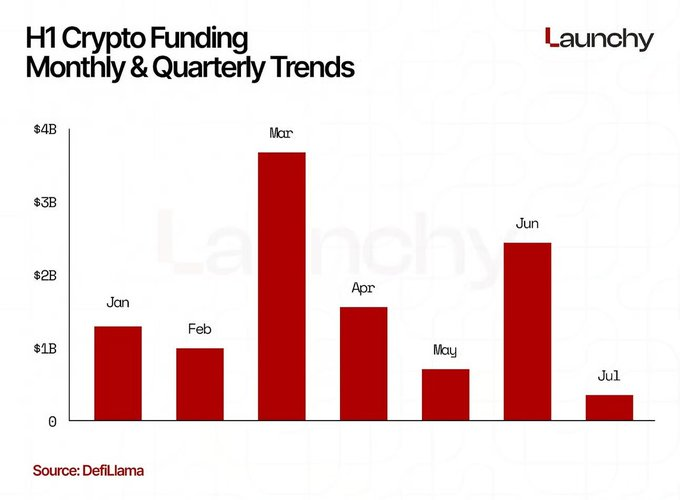

Monthly and Quarterly Trends

Funding amounts varied month by month, with March being the strongest. In March alone, companies raised an estimated $8 billion, driven by large strategic rounds and pre-IPO funding.

January and February combined saw around $9.4 billion in funding, while April slowed slightly to about $4.5 billion.

Fundraising rebounded in May and June, both months exceeding $5 billion, primarily fueled by late-stage deals and Circle’s IPO.

Quarterly, Q1 raised nearly $17.4 billion, while Q2 added another $15.9 billion. While Q1 was boosted by early momentum and Binance’s financing, Q2 saw broader distribution, with large rounds going to scaling infrastructure, custody solutions, and DeFi.

This pattern suggests investors made funding decisions early in the year, possibly aiming to lock in valuations before further token price increases.

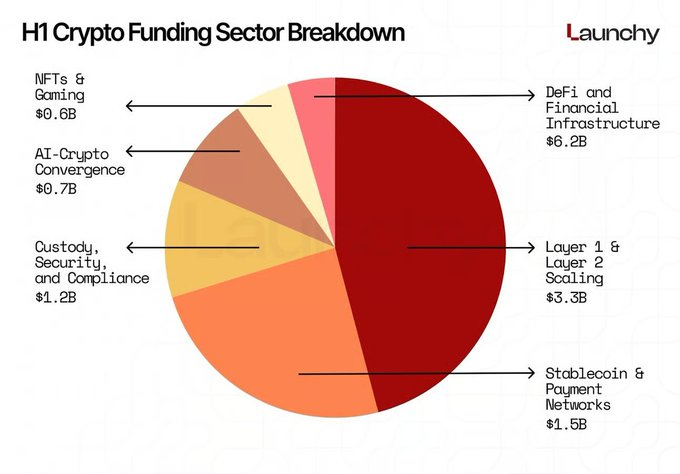

Sector Breakdown and Analysis

An analysis of capital allocation reveals which sectors investors believe hold long-term value:

• DeFi and financial infrastructure attracted the largest share, raising over $6.2 billion. Institutional DeFi protocols focused on compliant lending, derivatives, and liquidity provision were particularly popular.

• Layer 1 and Layer 2 scaling solutions raised approximately $3.3 billion. Projects like EigenLayer, LayerZero, and other protocol-centric initiatives were top beneficiaries, reflecting investor belief that Ethereum scaling and cross-chain interoperability remain unresolved opportunities.

• Custody, security, and compliance solutions attracted over $1.2 billion, highlighting the growing importance of trusted infrastructure amid tightening regulatory requirements.

• Stablecoins and payment networks raised about $1.5 billion, showing sustained capital support for projects bridging fiat and on-chain liquidity.

• AI-Crypto convergence emerged as a fast-growing theme, with roughly $700 million invested in projects combining large language models, decentralized computing, and token incentives.

• Compared to 2021–2022, NFT and gaming remained subdued, totaling around $600 million—underscoring a market shift from speculative collectibles toward more utility-driven applications. In short, capital has decisively moved from pure consumer hype cycles toward infrastructure, compliance tracks, and scalable ecosystems.

Notable Funding Rounds

Several large financings dominated headlines and capital flows. Binance’s $2 billion strategic round in January immediately set the tone for the year’s fundraising market, demonstrating that even established exchanges still command significant investor confidence. Circle’s $1.1 billion IPO became the largest public exit of the first half and validated the stablecoin model as a viable, revenue-generating business. Together, Binance and Circle’s rounds rank as the second- and third-largest in crypto history.

Other standout rounds include TON’s $400 million strategic raise, Phantom’s $150 million Series C, and LayerZero’s $150 million investment. These alone accounted for a quarter of total funding in the first half.

A key trend: nearly all major rounds included participation from top-tier investors such as a16z crypto, Paradigm, Sequoia, and Pantera Capital—indicating that mainstream venture funds continue to concentrate equity in leading industry players.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News