After "Female Buffett" CRCL made $100 million and exited her position, can we short Circle now?

TechFlow Selected TechFlow Selected

After "Female Buffett" CRCL made $100 million and exited her position, can we short Circle now?

Fundamentals and short-term movements are two different things.

By shushu, BlockBeats

Since its IPO on June 5, Circle has become the most frenzied stock in the crypto equity space, surging over 500%.

On June 18, CRCL hit a record high, reaching a market capitalization of $48.4 billion. According to Yahoo Finance, Circle currently has approximately 36.34 million shares in circulation, representing 17.94% of its total outstanding shares (202.55 million). Based on the closing price of $199.59 on the 18th, the corresponding free-float market cap is about $7.253 billion.

Circle's surge has also lifted Coinbase’s stock, marking the first time COIN has rallied independently of cryptocurrency prices and trading volume since its IPO.

As CRCL hits new highs, institutions have begun gradually taking profits.

ARK Made $96 Million—And That Was Just Profit

Reports indicate that Circle planned to issue 24 million shares to raise $624 million, targeting a valuation of $6.7 billion. ARK Invest subscribed for $150 million, while BlackRock, led by Larry Fink, invested $60 million—accounting for roughly 35% of this funding round combined.

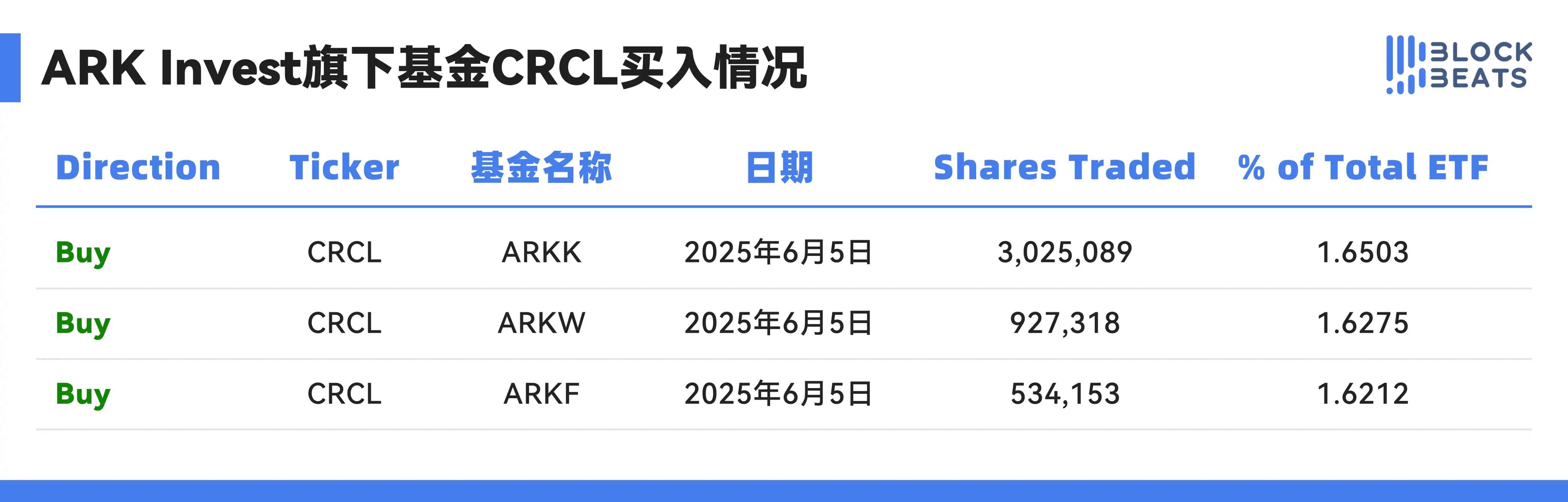

On June 5, ARK Invest purchased nearly 4.5 million CRCL shares on Circle’s first trading day. At the closing price, the total value was approximately $373 million.

On June 16, as CRCL surpassed $160 to reach an all-time high, ARK Invest sold a total of 342,658 shares of Circle Internet Group Inc. through three of its ETFs: ARK Innovation ETF (ARKK) reduced its position by 196,367 shares, ARK Next Generation Internet ETF (ARKW) by 92,310 shares, and ARK Fintech Innovation ETF (ARKF) by 53,981 shares—totaling around $51.7 million in proceeds.

On June 17, with CRCL rebounding past $160 again, ARK’s three ETFs offloaded over 300,000 additional shares, generating $44.76 million in revenue.

Despite selling more than 600,000 shares, ARK still holds nearly 4 million shares of Circle, valued at approximately $371 million, representing 6.13% of its ETF portfolios. In other words, based on current prices, ARK’s two recent sales only realized the profit portion of its existing CRCL holdings.

Related reading: "Crypto Bull Market Is All in U.S. Stocks: Circle’s Rise from $31 to $165 in Ten Days"

FOMO, Sold Too Early—Can Crypto Traders Short Circle Now?

"Circle's market cap has already reached $40 billion, yet USDC’s supply is only $60 billion," lamented a veteran trader on social media, capturing the conflicted sentiment among crypto natives toward CRCL’s rally. The stock’s meteoric rise since listing not only reflects collective market psychology but also highlights divergent perceptions and strategic gaps between different investor groups.

Insiders familiar with USDC’s operations should have been early beneficiaries, yet during this IPO run-up, they displayed unusual division—one group “bought reluctantly,” while another “understood the thesis but thought it too expensive,” ultimately missing the move. Meanwhile, many traditional investors, driven by narrative appeal and low information barriers, rushed into CRCL, fueling bullish momentum that sent prices soaring.

"Not going all-in on CRCL might be a regret that lasts a long time," wrote crypto trader yuyue. "Until USDT completes a legitimate U.S. IPO—which is almost impossible—or USD1 overtakes USDC and goes public—unlikely in the short term—Circle will firmly occupy the leading narrative position."

"My winning streak in U.S. stocks ended because of this crypto-linked stock!" joked Twitter user 'Tianli,' mocking herself. "Ever since Circle listed, my usual stock-trading logic no longer applies. Now I need crypto-style thinking instead. Other stocks don’t make sense anymore—everything feels chaotic when they move together. For me, U.S. equities now feel like a drunkard beating up an experienced driver." To Tianli, Circle’s fundamentals don’t justify the surge, and the short-term movement defies conventional models.

Some traders point to the less-than-18% free float as an explanation for the explosive rally, drawing parallels to WLD’s ultra-thin float dynamics—an old lesson relearned: “Fundamentals and short-term price action are two different things.”

Others bet on beta spillover effects. Before Circle’s listing, crypto KOL Taiki wrote: “Companies like CRCL are essentially pricing anchors for stablecoins. If it’s worth $10 billion, then ENA and MKR must be revalued too.” Taiki increased exposure to DeFi blue chips to capture potential overflow gains. Yet today, as CRCL rockets toward a $40 billion valuation, ENA and MKR have clearly underperformed.

Another group stayed away for simpler reasons—they know too much. Lin from Deribit openly advised her family against touching CRCL, arguing that “Circle’s revenue model is overly concentrated and operates in a saturated market. BlackRock’s BUIDL and Trump’s USD1 will both eat into their share.” Her view isn't emotional but grounded in deep understanding of the stablecoin ecosystem. Still, she admits: “In crypto, knowing too much can sometimes become a burden.”

Unlike crypto traders who endlessly debate valuations and fundamentals, Wall Street investors prefer compelling stories. As crypto KOL Kay noted on X, U.S. equity buyers see CRCL as “part of a national strategy, replacing VISA, charging aggressively toward a $2 trillion target.” Meanwhile, actual crypto users see “high compliance costs eroding profits, easy losses in rate-cut cycles, issuance fueled by heavy subsidies, and a fair valuation of $3–5 billion.”

Jack Zhang, co-founder and CEO of Airwallex—who previously sparked debate on X about stablecoins’ real-world utility—recently posted: “It’s time to short Circle.”

But Is It Really Time?

The CRCL narrative wasn’t built for crypto natives. Chris, a Coinbase x Circle maxi, argues that finding Circle expensive reflects crypto insularity: “You thought crypto would revolutionize finance, but instead, finance joined crypto—and ended up revolutionizing it.”

Some see Circle’s listing as a potential bull-market top signal, similar to how Coinbase’s IPO day coincided with Bitcoin’s peak in the last cycle. Others disagree: “This bubble is nowhere near 2021 levels. Altcoins have been thoroughly shaken out, and BTC dominance remains high.”

More importantly, CRCL underwent a traditional IPO with a 180-day lock-up period, limiting immediate sell-side pressure—unlike $COIN, which saw immediate insider dumping. Many hedge funds were unable to get in on day one and are now forced to buy at elevated prices in the secondary market. Some short sellers are paying steep annualized borrowing fees (over 5%), making sustained bearish positioning difficult.

As Arthur Hayes put it: “Should you short Circle? Absolutely not. You can choose not to buy—but never short. Sentiment premium is the most terrifying accelerant.”

Perhaps Circle’s market cap isn’t justified yet. But what it represents—a stablecoin platform backed by BlackRock, Fidelity, Visa, and Coinbase—has already crossed the regulatory threshold and entered mainstream U.S. markets. Its valuation doesn’t stem from crypto consensus, but from the stock market’s re-pricing of a “compliant fintech infrastructure” player.

Hayes believes Circle is severely overvalued—but expects prices to keep rising, as this IPO marks the beginning of the current stablecoin mania, not its end.

With traditional payment giants yet to enter en masse, USDT unlikely to go public, and USD1 still in policy limbo, Circle may be the sole vehicle for this narrative. “There is no real future—because distribution channels for new entrants are closed. Drill that into your thick skull. Trade this pile like a hot potato. But don’t short it—these new stocks will bankrupt every single short seller.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News