Quick Overview of Neutrl: You Deposit Stablecoins, We Help You Short VC-Backed Tokens

TechFlow Selected TechFlow Selected

Quick Overview of Neutrl: You Deposit Stablecoins, We Help You Short VC-Backed Tokens

Neutrl buys locked VC coins at a discount via OTC, then hedges with short positions. Behind the concept that "everything can be a stablecoin," is the risk already excessive?

By Alex Liu, Foresight News

Neutrl, a Stablecoin Protocol

On April 17, synthetic dollar-pegged stablecoin project Neutrl announced a $5 million seed round led by digital asset private market STIX and venture capital firm Accomplice. Amber Group, SCB Limited, Figment Capital, Nascent, as well as angel investors including Ethena founder Guy Young and Joshua Lim, a derivatives trader at Arbelos Markets (recently acquired by FalconX), also participated in the funding.

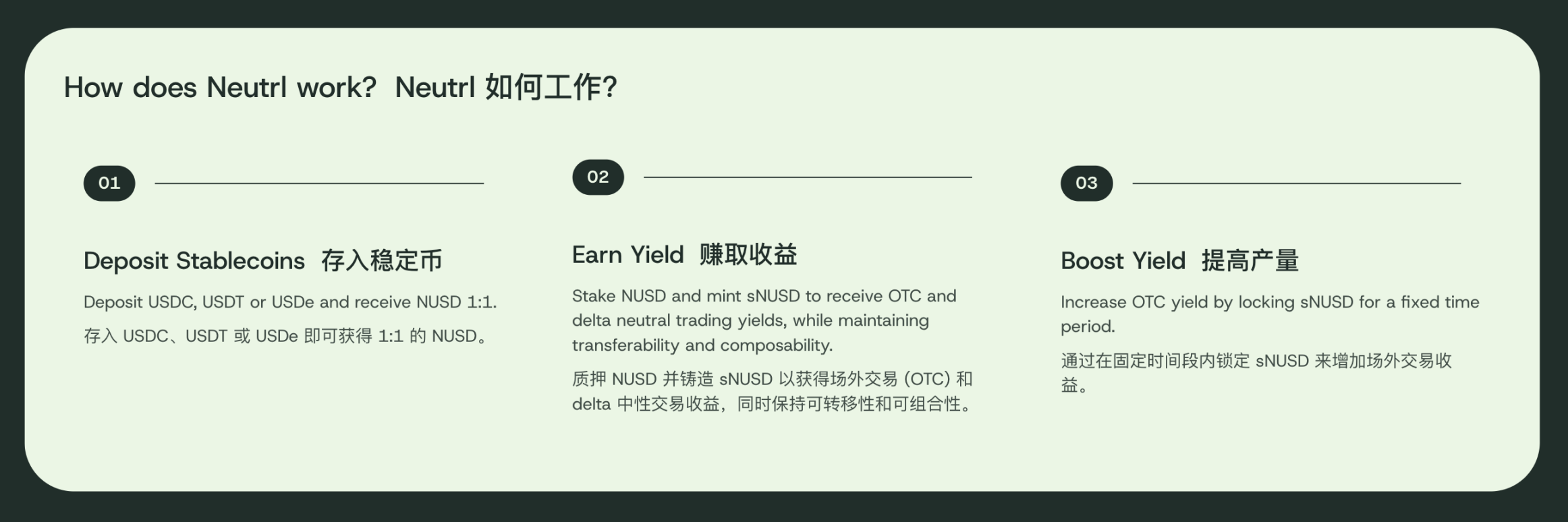

Neutrl’s product model resembles that of category leader Ethena, featuring a dollar-pegged synthetic stablecoin NUSD and an interest-bearing asset sNUSD—corresponding to USDe and sUSDe respectively. The key difference lies in their yield sources: while Ethena generates returns through funding rate arbitrage in crypto perpetual futures markets, Neutrl takes a more aggressive approach: discount arbitrage on OTC tokens.

Yield Source: OTC Discount Arbitrage

Institutional investors such as VCs can acquire project tokens at discounted valuations inaccessible to retail users, though these tokens typically come with stricter unlocking conditions. Generally, tokens are subject to lock-up periods ranging from six months to one year, followed by linear vesting schedules spanning two to four years.

Facing cash flow constraints but holding locked tokens? Worried about significant value depreciation upon unlocking? Or simply eager to cash out early for a yacht-and-villa lifestyle? OTC (Over-The-Counter) trading offers a solution: selling unlocked tokens at a discount before they officially release. The discount level depends on the project quality and unlock terms, but is usually substantial—for instance, discounts exceeding 50% for tokens unlocking one year later.

Neutrl uses user deposits to purchase these discounted, locked VC tokens, while simultaneously shorting an equivalent amount of the same token via futures contracts to hedge price exposure, achieving delta-neutral risk (i.e., profits are independent of token price fluctuations).

For example: purchasing OM tokens from the Mantra project at a 60% discount one year prior to unlocking, assuming a $400,000 investment. At the same time, short $1 million worth of OM futures. Ignoring funding fees and other complexities, this effectively locks in $600,000 of profit one year later.

If OM crashes overnight by 90%, the OTC-purchased $400,000 stake becomes nearly worthless, but the short position gains $900,000—locking in profits earlier than expected upon closing. Conversely, if OM doesn't crash and instead rises 50% after one year, the short loses $500,000, but the unlocked tokens are now worth $1.5 million—still securing the originally targeted $600,000 gain.

Potential Risk: Is It Really a "Stablecoin"?

This strategy may appear flawless, but there are caveats. Why don’t VCs simply hedge their positions via shorting instead of selling at a discount?

First, while some VCs might indeed do so, in practice, VCs are often required to disclose their portfolio holdings and fund usage to LPs and investors. Shorting their own investments could damage reputation. Second, certain VCs may hold over 10% of a project’s tokens, a volume too large for the futures market to absorb through shorting alone, leaving discount sales as the only viable exit.

Moreover, this strategy faces two major risks: abnormal funding rates and sharp token price increases.

Regarding funding rates: when too many participants go short, the short side must continuously pay funding fees to longs. In extreme cases with fully negative funding, daily rates could reach up to 10% of principal. Over OTC lock-up durations that span a year or even four years, cumulative funding payments could exceed the yield generated from the OTC discount. That said, in a bull market context, positive funding rates could provide additional gains.

If the token price surges more than double, “infinite margin” would be needed to maintain the short until the OTC tokens unlock. Otherwise, premature liquidation of the short position means locking in actual losses. If the price subsequently drops, the investor still bears the loss. Not everyone can perfectly short smooth downward moves like "W" or "MOVE"—shorting "TIA" and getting liquidated midway would result in net losses.

Conclusion

Underlying Neutrl is a high-risk arbitrage strategy. While its risk management may be more sophisticated than that of average retail traders, the potential risks remain significant and cannot be ignored.

Marketing this high-risk arbitrage fund under the label of a “stablecoin” seems questionable and warrants stronger risk disclosures. Yet Ethena is fundamentally also an arbitrage fund wrapped in a stablecoin facade. Without Ethena or Neutrl, retail investors would have little to no access to the underlying strategy yields, making them innovative developments within the CeDeFi space that expand yield opportunities for users.

Neutrl has not yet launched publicly. Interested users can currently sign up via the official website for waitlist access to early testing.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News