The Rise of U.S. Crypto Enterprises: M&A, IPOs, and the Tokenization Boom

TechFlow Selected TechFlow Selected

The Rise of U.S. Crypto Enterprises: M&A, IPOs, and the Tokenization Boom

What are crypto giants building?

Author: Nianqing, ChainCatcher

Recently, the U.S. Securities and Exchange Commission (SEC) has dropped a series of lawsuits against cryptocurrency firms in what appears to be a sweeping reset—cases against Kraken, Consensys, Cumberland, Ripple, Robinhood, and Nova Labs have all been dismissed. The SEC’s new chair, Paul Atkins, has officially taken office and declared establishing a digital asset regulatory framework as his “top priority,” signaling a decisive shift away from the previous era of closed-off, high-pressure regulation. Meanwhile, the U.S. Department of Justice has clarified that crypto developers bear no responsibility for how their code is misused by criminals and should not be held liable.

Clearly, regulatory clarity and deregulation are propelling crypto companies into a period of rapid acceleration.

At present, U.S. crypto enterprises are experiencing a surge in IPOs and mergers and acquisitions (M&A). Over ten American crypto firms are actively seizing this window to go public. Additionally, an increasing number of projects are exiting via acquisition. Since November 2024, there have been more than 10 M&A deals per month for five consecutive months, with large-scale transactions frequently occurring and deal values continuously setting new all-time highs in the crypto industry. The crypto market is entering a phase of consolidation and institutionalization, giving rise to one-stop, integrated platform-style crypto giants.

What are these crypto giants building toward? And what does this mean for the future of the crypto market?

IPO Boom: Seizing the Window

2021 was a peak year for the crypto industry. Fueled by surging Bitcoin prices, a low-interest-rate environment, and the SPAC boom, multiple crypto firms planned to raise capital and boost market influence through IPOs or SPAC listings. On April 14, 2021, Coinbase’s successful Nasdaq listing marked a milestone in the mainstreaming of the crypto industry. However, other crypto companies were not as fortunate—Circle, Kraken, Ripple, BlockFi, and eToro had all announced IPO or SPAC plans in 2021, but many were ultimately shelved due to regulatory uncertainty and market volatility.

In the second half of 2024, Donald Trump’s election reopened the IPO window for U.S. crypto companies. Several crypto firms have already gone public in the U.S. Japanese cryptocurrency exchange Coincheck completed a merger-based listing on December 11, 2024; Fold Holdings successfully listed on Nasdaq via SPAC on February 19; Amber PremiumAmber, the digital wealth management platform under Amber Group, completed its merger-based listing in March.

Companies like Circle, eToro, and Kraken, which previously attempted IPOs, are now moving quickly to advance their plans. Currently, Circle, eToro, Bgin Blockchain, Chia Network, Gemini, and Ionic Digital have already filed S-1/F-1 forms, making a Q2 2025上市 highly likely. BitGo, Kraken, Bullish Global, Consensys, Figure, Chainalysis, and Blockchain.com have indicated IPO intentions or are in advisor discussions, positioning them well for potential listings between 2025 and 2026.

Their current progress is shown in the chart below:

M&A Heats Up: Crypto Market Enters Consolidation and Institutionalization Phase

Recently, M&A activity in the crypto market has intensified. Amid a broader downturn in primary investment markets, more projects are opting for exits via acquisition, while leading players are increasingly willing to optimize their industrial footprint and expand influence through strategic acquisitions at reasonable valuations.

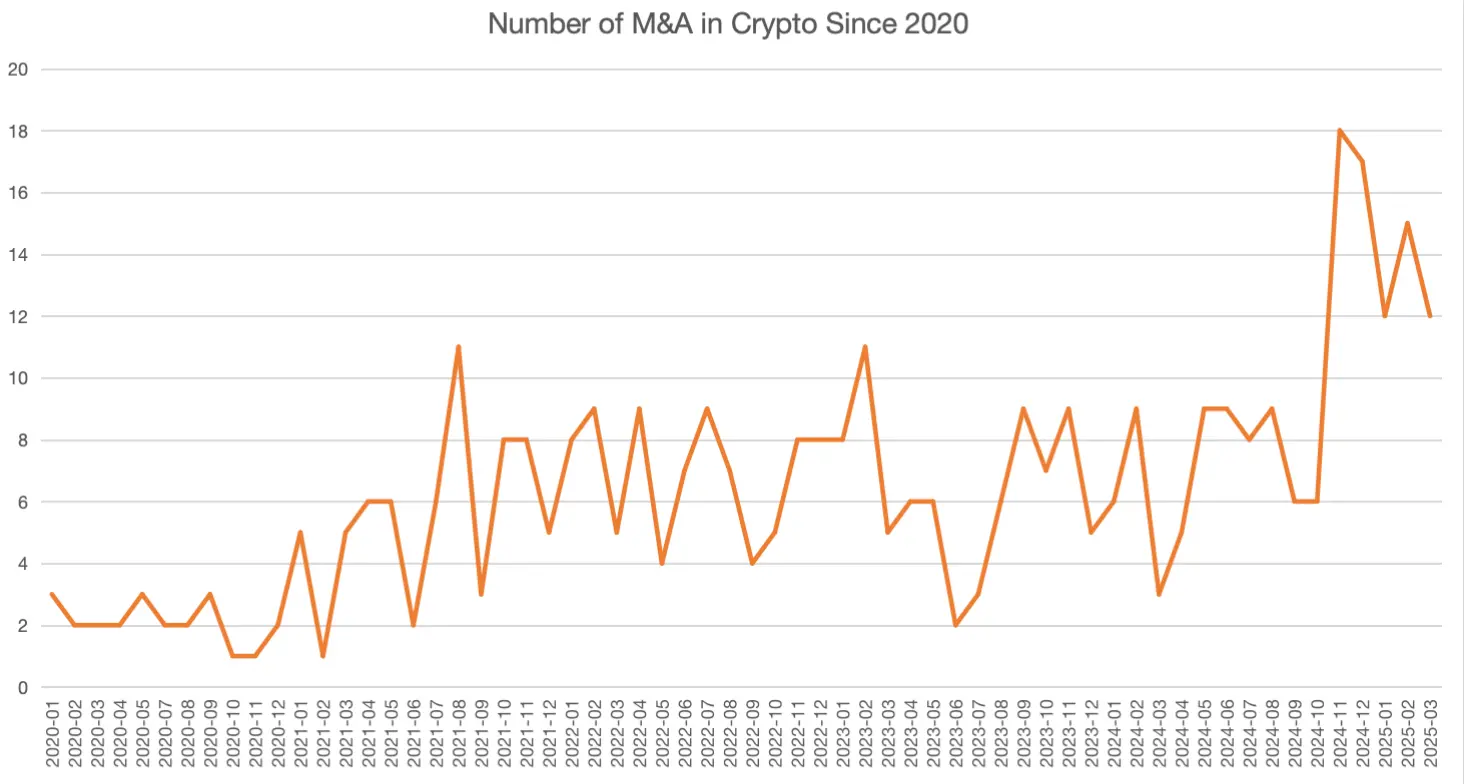

According to RootData, over the past three months, there have been more than 40 M&A events, most led by U.S.-based crypto firms. Since November 2024, the number of monthly M&A deals has exceeded 10 for five consecutive months. Large-value acquisitions are becoming frequent, pushing transaction volumes to record highs in the crypto space.

Crypto M&A Trends since 2020, Data Source: RootData

In the past six months, every acquisition exceeding $1 billion occurred in the U.S.:

-

In December 2024, traditional payments giant Stripe acquired stablecoin platform Bridge for $1.1 billion

-

In March 2025, Kraken acquired U.S. futures trading platform NinjaTrader for $1.5 billion

-

In April 2025, Ripple acquired crypto-friendly broker Hidden Road for $1.25 billion

In addition, Coinbase is engaged in advanced talks to acquire Deribit, valued at approximately $4–5 billion. Arthur Hayes’ crypto derivatives platform BitMEX is also exploring a sale. If either deal closes, it would set a new record for M&A value in the sector.

Bernstein analysts note that as exchanges and broker/dealer models begin to converge, the crypto industry is evolving toward more integrated, “one-stop” multi-asset investment platforms. For example, Kraken's acquisition of NinjaTrader, Robinhood’s integration of Bitstamp, and Coinbase’s ongoing negotiations to acquire Deribit all reflect this trend. Deribit accounts for around 70% of the global BTC and ETH options market, with monthly options trading volume exceeding $100 billion and monthly crypto futures volume reaching about $45 billion. A Coinbase acquisition of Deribit would allow it to expand into derivatives, particularly options, and directly compete with Binance in the international crypto derivatives market.

Beyond options and derivatives, crypto exchanges are even expanding into traditional assets. On April 14, Kraken launched stock and ETF trading in the U.S. for the first time. On April 12, several SEC commissioners expressed support during a second digital asset roundtable for creating a regulatory sandbox that would allow crypto exchanges like Coinbase to experiment freely in new areas—including offering tokenized securities trading. In the future, crypto exchanges will offer spot cryptocurrencies, crypto derivatives, tokenized stocks, and even equities and equity derivatives. At the same time, brokerage platforms like Robinhood will further expand their crypto and crypto futures offerings.

As traditional assets become tokenized, the line between crypto tokens and stocks is blurring. The roles of digital asset securities, tokenization, and intermediaries will become clearer, and overlap between crypto exchanges and brokers will grow. Traditional financial institutions and crypto firms will merge further. U.S. crypto companies will resemble FinTech firms more than pure crypto entities.

Crypto Firms Pivot Toward Institutional Services

Trump administration policies favorable to crypto have lowered barriers for institutional entry. The U.S. Office of the Comptroller of the Currency (OCC) has approved blockchain-native lending licenses (e.g., for Figure Technologies), encouraging traditional banks to participate. Starting in 2024, institutional services—including digital asset custody, tokenization, payment settlement, derivatives trading, and compliance solutions—have become the main drivers of revenue growth in the crypto industry.

Meanwhile, with the broader crypto market lacking new narratives to attract users, customer acquisition costs for retail-facing platforms like crypto exchanges have risen. As a result, compliant, regulation-abiding crypto firms are shifting focus toward institutional business.

Coinbase began pivoting early to reduce reliance on retail trading. Its transaction revenue—especially retail trading fees—has declined steadily: 70%, 65%, and 52.7% of total revenue in 2022, 2023, and 2024, respectively. In contrast, subscription and services revenue (targeted at institutions) has grown annually—from 17.8% in 2022 to 22.6% in 2023 and 34.8% in 2024.

As of 2024, Coinbase’s custodied assets reached $220 billion, doubling year-on-year, primarily serving institutional clients such as hedge funds and ETF issuers. Over the past year, Coinbase became the primary custodian for spot Bitcoin ETFs.

If Coinbase completes the acquisition of Deribit, it would not only expand its presence in the global crypto derivatives market but also strengthen its institutional offerings. In 2024, Deribit’s trading volume nearly doubled, driven by soaring demand from institutional investors (e.g., hedge funds, asset managers) for sophisticated financial instruments. Deribit’s institutional client base and professional tools (like options and futures) would enhance the appeal of Coinbase Prime. Recently, Coinbase Prime provided $200 million in credit support to CleanSpark, a Nasdaq-listed mining company, whose digital asset management team has officially launched an institutional-grade Bitcoin fund management platform.

Kraken, Gemini, and other crypto exchanges have made similar strategic moves. Kraken’s high-stakes acquisition of U.S. retail futures platform NinjaTrader aims to boost competitiveness in derivatives and expand institutional capabilities. In April, Kraken also announced a partnership with Beeks Exchange Cloud to launch custody services later this year. Gemini has recently expanded its institutional services to Europe and Canada through U.S. dollar payment support.

Ripple’s recent $1.25 billion acquisition of crypto-friendly broker Hidden Road is also fundamentally aimed at expanding services for institutional investors. Hidden Road is a one-stop provider helping large institutional players—such as Jump Trading, market makers, and hedge funds—connect to exchanges, move funds, borrow money, and clear trades.

Ripple’s core business lies in cross-border payments, but its ecosystem relies heavily on self-built networks and alliances, exposing clear bottlenecks in its payment operations. Additionally, in June last year, Ripple acquired New York-based crypto trust company Standard Custody & Trust Company, enabling it to offer crypto custody and settlement services.

Building Into Tokenization

Beneath the shift toward institutional services lies the explosive growth of the tokenization market.

Recently, Ripple partnered with Boston Consulting Group (BCG) to publish a report titled *Approaching the Tokenization Tipping Point*. It makes a key prediction: the tokenized asset (tokenization) market will grow from $600 billion in 2025 to $18.9 trillion by 2033, representing a compound annual growth rate (CAGR) of 53%.

Tokenization refers to using blockchain to record ownership and transfer real-world assets—such as securities, commodities, and real estate. Key use cases include trade finance, collateral and liquidity management, investment-grade bonds, private credit, and carbon markets.

Notably, unlike in Chinese-speaking regions where stablecoins and RWA are often treated separately, this report classifies stablecoins within the broader category of asset tokenization—a space now central to U.S. crypto firms' strategic ambitions. Kraken’s co-CEO recently stated he expects tokenized stocks to surpass stablecoins in scale.

Three crypto firms featured in Forbes’ 2025 Fintech 50—Figure, Fireblocks, and Securitize—are all deeply involved in tokenization, covering real estate, bonds, and equity.

Figure Technologies leverages its proprietary Provenance blockchain to offer home equity lines of credit (HELOC), payment solutions, and asset tokenization. It has also launched its own tokenized assets. On February 20, the SEC approved Figure Markets (a subsidiary of Figure Technologies) to issue YLDS, the first “yield-bearing stablecoin.” Pegged 1:1 to the U.S. dollar, YLDS is registered with the SEC as a public security, offers yield, and currently yields around 3.85% annually—placing it in the same financial category as stocks or bonds.

Fireblocks focuses on secure storage, transfer, and issuance of digital assets for financial institutions, exchanges, payment platforms, and Web3 companies. In September last year, Fireblocks acquired tokenization firm BlockFold for $13.6 million to enhance its ability to help major banks and financial institutions move assets onto blockchains. Since 2024, Fireblocks has rapidly expanded globally, launching operations in Germany, France, Singapore, Japan, and South Korea.

Securitize gained public attention through its collaboration with BlackRock on the tokenized asset BUIDL. It offers end-to-end services including fund management, token issuance, brokerage, transfer agency, and alternative trading systems. On April 15, Securitize announced the acquisition of MG Stover’s fund management business, making its subsidiary Securitize Fund Services (SFS) the world’s largest digital asset fund management platform. This acquisition “solidifies Securitize’s position as a comprehensive, institution-grade platform for tokenization and fund management.”

Beyond IPO preparations, Circle is also targeting the broader tokenization market.

Circle’s IPO S-1 filing reveals that 95% of its revenue comes from short-term U.S. Treasury yields, while its native business lines—such as trading fees, cross-chain bridges, and wallets—generate negligible income. Beyond risks tied to interest rate dependency, high compliance and distribution costs consume much of its revenue.

Recently, Circle acquired Hashnote and its USYC tokenized money market fund. Hashnote is a regulated, institution-grade investment management platform incubated by Cumberland Labs (DRW’s blockchain arm), offering institutional investors tokenized money market funds (USYC), customized investment strategies, on-chain asset management, and custody services.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News