A comprehensive analysis of the capital flows behind stablecoins' billion-dollar growth: altcoins haven't risen, so where did the money go?

TechFlow Selected TechFlow Selected

A comprehensive analysis of the capital flows behind stablecoins' billion-dollar growth: altcoins haven't risen, so where did the money go?

Stablecoin market cap increases by $100 billion, with Ethereum and Tron still accounting for 80% of the growth.

Author: Frank, PANews

Since 2024, the global stablecoin market has grown by 80.7%, surpassing $235 billion in value, with USDT and USDC contributing 86% of this growth and continuing to dominate the market. However, puzzlingly, the tens of billions of dollars in new capital accumulated on Ethereum and Tron have not triggered a corresponding rally in altcoins as seen in previous cycles. Data shows that each additional dollar in stablecoins now drives only $1.50 in altcoin market cap growth—down 82% compared to the last bull run.

This article by PANews analyzes comprehensive stablecoin data to explore the ultimate question in crypto: Where did the money go? As exchange balances surge and DeFi protocol staking volumes climb, traditional financial institutions’ over-the-counter trading, cross-border payment adoption, and emerging markets’ demand for currency substitution are quietly reshaping the flow of capital within the cryptocurrency ecosystem.

Stablecoin Market Cap Adds $100 Billion, Ethereum and Tron Account for 80% of Growth

According to Defillama, stablecoin issuance has increased from $130 billion at the beginning of 2024 to $235 billion as of early 2025—an 80.7% overall increase. The majority of this growth continues to come from USDT and USDC.

On January 1, 2024, USDT’s supply was $91 billion; by March 31, 2025, it had reached $144.6 billion—an increase of approximately $53.6 billion, accounting for 51% of total stablecoin growth. Over the same period, USDC grew from $23.8 billion to $60.6 billion, contributing about 35% of the expansion. Together, these two stablecoins not only hold 87% of the market share but also contributed 86% of the growth.

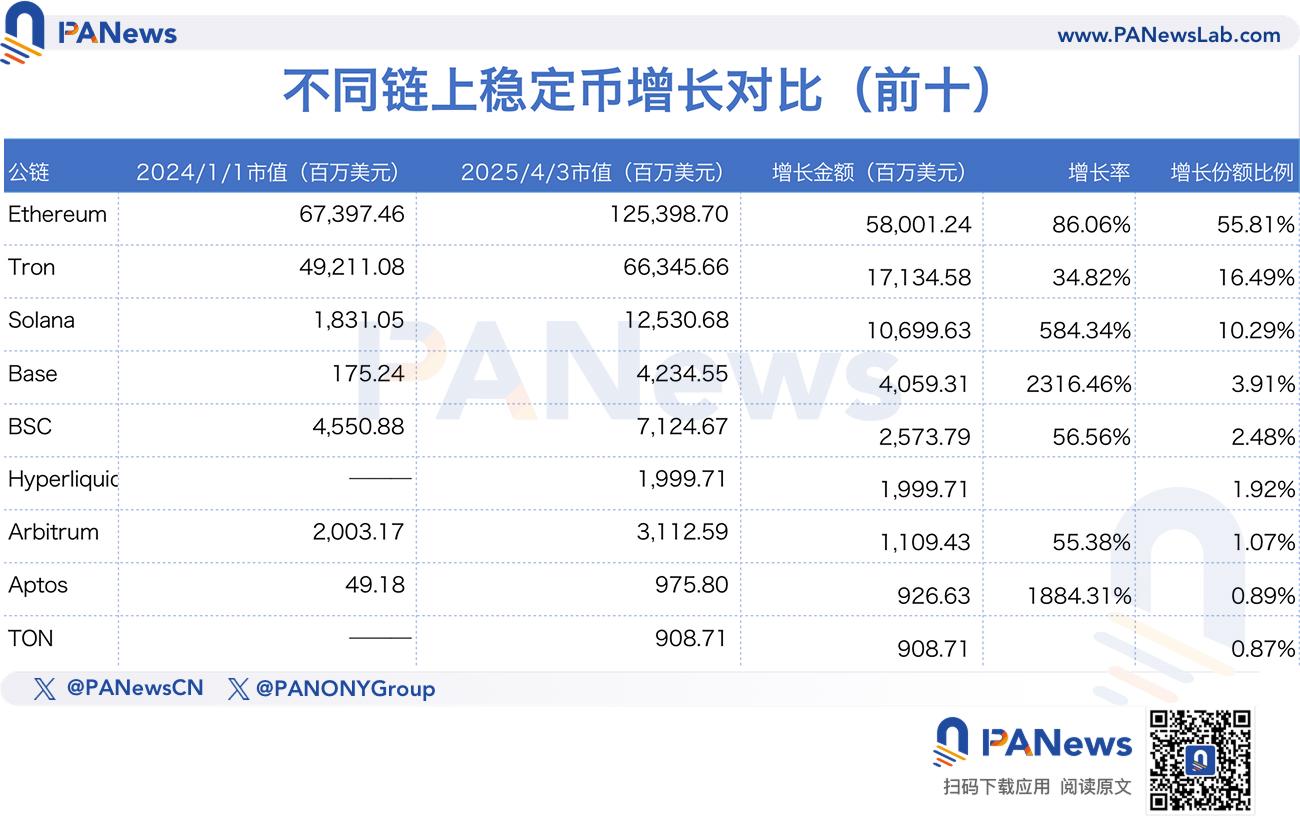

Breaking down chain-specific data, Ethereum and Tron remain the two largest public chains by stablecoin issuance. Ethereum accounts for 53.62% of stablecoin volume, while Tron holds 28.37%, combining for 81.99% of the total.

From January 1, 2024, to April 3, 2025, Ethereum saw an increase of approximately $58 billion in stablecoin issuance—a growth rate of 86%, nearly matching the issuance growth rates of USDT and USDC. Tron’s growth rate was around 34%, below the overall stablecoin average.

Solana ranks third, adding $12.5 billion in issuance during the same period with a staggering growth rate of 584.34%. Base comes fourth, increasing issuance by $4 billion—an extraordinary growth rate of 2,316.46%.

Among the top ten chains, Hyperliquid, TON, and Berachain only began issuing stablecoins within the past year. These three added approximately $3.8 billion in stablecoin supply, accounting for 3.6% of total growth. Overall, Ethereum and Tron remain the core markets for stablecoins.

Each New Dollar in Stablecoins Drives Just $1.50 in Altcoin Market Cap

Despite rapid on-chain growth in stablecoins, altcoin market cap performance has been lackluster.

For comparison, from March 2020 to May 2021, the total altcoin market cap (excluding BTC and ETH) surged from $39.8 billion to $813.5 billion—an increase of roughly 19.43x. During the same period, stablecoin supply rose from $6.14 billion to $99.2 billion, growing about 15x—nearly in sync with altcoins.

In contrast, during the current bull cycle, stablecoin market cap has grown by 80%, while the overall altcoin market cap has increased by only 38.3%, amounting to approximately $159.9 billion in value.

Looking back, during the 2020–2021 cycle, every $1 increase in stablecoin supply drove an $8.30 rise in altcoin market cap. But in the 2024–2025 cycle, each $1 in new stablecoins generates just $1.50 in altcoin market cap growth. This sharp decline suggests newly issued stablecoins are no longer being used primarily to buy altcoins.

So where did the money go? That is the key question.

Chain Landscape Reshuffled: Ethereum and Tron Hold Ground While Solana and Base Break Out

At first glance, the MEME coin frenzy on Solana has led this bull market. However, most MEME trades use SOL trading pairs, leaving little room for stablecoin involvement. Moreover, as previously analyzed, stablecoin growth remains concentrated on Ethereum.

Therefore, to trace where the new stablecoin capital flows, we must examine trends on Ethereum or major stablecoins like USDT and USDC.

Before diving into analysis, let’s outline several possible directions—common market speculations about where stablecoins might be going: increased use in payments, staking yields, or as a store of value.

First, consider stablecoin transaction patterns on Ethereum. From the chart below, we observe a heartbeat-like regularity in transaction volume fluctuations. This pattern may reveal insights into how stablecoins are actually being used.

Zooming in on shorter timeframes, the pattern reveals a clear 5+2 rhythm: two days of low activity followed by five days of high activity. Notably, troughs occur on weekends, while peaks gradually build from Monday to Wednesday and taper off Thursday and Friday. Such a distinct cyclical behavior strongly suggests institutional or corporate originators—unlikely if stablecoins were mainly used for retail spending, which would show less predictable patterns.

Additionally, daily transaction frequency data shows Ethereum’s USDT rarely exceeds 300,000 transfers per day. Both transfer frequency and average transaction amounts are significantly lower on weekends than on weekdays—further supporting the above inference.

USDT Flows into Exchanges, USDC Settles in DeFi Protocols

In terms of holding distribution, USDT’s exchange balances have surged over the past year. On January 1, 2024, exchange holdings stood at 15.2 billion tokens; by April 2, 2025, they had risen to 40.9 billion—an increase of $25.7 billion, or 169%. This far exceeds the 80.7% growth in total stablecoin supply and accounts for 48% of USDT’s issuance growth during the same period.

In other words, nearly half of all newly issued USDT over the past year flowed directly into exchanges.

However, USDC tells a different story. On January 1, 2024, USDC held on exchanges totaled approximately 2.06 billion tokens. By April 2, 2025, this figure had grown to 4.98 billion. Yet during the same period, USDC’s total issuance expanded by $36.8 billion—meaning only 7.9% of new supply entered exchanges. Exchange holdings account for just 8.5% of total USDC supply, a stark contrast to USDT’s 28.4%.

Most new USDT issuance flows into exchanges, whereas new USDC largely bypasses them.

Where, then, is the new USDC going? Answering this could shed light on broader capital flows in the market.

From a wallet perspective, top USDC holders are predominantly DeFi protocols. On Ethereum, for example, the largest holder is Sky (MakerDAO), with 4.8 billion USDC—about 11.9% of total supply. In July 2024, this address held only 20 million USDC; within a year, its holdings increased 229-fold. Sky uses USDC as collateral for its stablecoins DAI and USDS. This growth reflects DeFi protocols’ rising Total Value Locked (TVL) and their increasing demand for stablecoins.

AAVE is the fourth-largest USDC holder on Ethereum. Its holdings rose from 45 million USDC on January 1, 2024, to a peak of 1.32 billion on March 12, 2025—an increase of ~$1.275 billion, representing 7.5% of Ethereum’s new USDC issuance.

Thus, much of the new USDC on Ethereum stems from growth in staking and yield-generating products. At the start of 2024, Ethereum’s TVL was approximately $29.7 billion. Although it has since declined, it still stands at $49 billion (peaking at $76 billion). Even using the current $49 billion figure, Ethereum’s TVL has grown by 64.9%—far exceeding last year’s altcoin gains and approaching the pace of overall stablecoin growth.

However, in absolute terms, while Ethereum’s TVL grew by $19.3 billion, stablecoin issuance on the network increased by $58 billion. After accounting for exchange inflows, yield protocols have absorbed only part of the new stablecoin supply.

New Use Cases Emerge: From Cross-Border Payments to Institutional Trading

Beyond DeFi-driven demand, stablecoins are increasingly adopted in consumer payments, cross-border remittances, and institutional OTC trading.

As highlighted in multiple official reports from Circle, stablecoins are gaining traction in cross-border remittances and retail payments. According to a Rise report, about 30% of global remittances are now settled via stablecoins—especially significant in Latin America and Sub-Saharan Africa. Retail and professional stablecoin transfers in these regions grew over 40% year-on-year between July 2023 and June 2024.

Circle also reported that in 2024, Zodia Markets—Scotiabank’s institutional digital asset brokerage offering OTC and on-chain FX services—minted a net $4 billion in USDC.

Another Latin American retail payment company, Lemon, has clients holding over $137 million in USDC, primarily used for everyday retail transactions.

Beyond use-case diversification, differing ecosystem structures across blockchains create varied stablecoin demands. For instance, the MEME coin boom on Solana has driven DEX trading demand. According to incomplete statistics from PANews, the top 100 USDC trading pairs on Solana have a combined TVL of approximately $2.2 billion. Assuming USDC makes up half of those pools, this represents about $1.1 billion in locked USDC—roughly 8.8% of USDC’s total issuance on Solana.

Crypto Market Shifts from “Speculative Bubble” to “Wealth Management Product”

After dissecting stablecoin dynamics, PANews finds no single dominant driver behind their growth—making it difficult to pinpoint exactly where the money went. Instead, we arrive at a complex set of conclusions:

1. Stablecoin market caps continue to grow, but this capital is not flooding into altcoins as initial fuel for an "alt season."

2. On Ethereum, about half of new USDT ends up on exchanges—likely used to purchase BTC (given the lack of strong rallies in altcoins or even ETH) or invested in exchange-based wealth management products. The remainder appears absorbed by DeFi protocols. Overall, capital flowing into Ethereum increasingly prioritizes stable returns from staking and lending. The appeal of crypto to traditional investors may no longer lie in volatile price swings, but rather in its emergence as a novel financial product.

3. New use cases are emerging. Traditional financial institutions like Scotiabank are entering crypto, creating fresh demand for stablecoins. Additionally, users in underdeveloped regions—with poor infrastructure and unstable local currencies—are increasingly adopting stablecoins for daily transactions. However, comprehensive data on these segments remains limited, so their exact scale is unclear.

4. Different chains foster different narratives and demands for stablecoins. Solana’s growth may stem from MEME-driven trading activity, while newer chains like Hyperliquid, Berachain, and TON attract capital due to rising ecosystem momentum.

Overall, this hidden capital shift signals a paradigm change in the crypto market. Stablecoins have transcended their role as mere transactional tools and evolved into value conduits linking traditional finance and the crypto world. While altcoins have not benefited broadly from stablecoin growth, institutional investment in yield products, essential payment needs in emerging markets, and maturing on-chain financial infrastructure are positioning stablecoins as carriers of broader economic value. This may indicate that the cryptocurrency market is quietly transitioning from a “speculation-driven” era to one defined by “value accumulation.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News