The Essence and Significance of Programmable Currency

TechFlow Selected TechFlow Selected

The Essence and Significance of Programmable Currency

Programmability is an inherent attribute of the digital age. Without true programmability, cash cannot fully transition into the digital realm.

Article Author: Nathan

Article Translation: Block unicorn

As stablecoins grow in influence and recognition, their advantages are frequently discussed—efficiency, low cost, accessibility, decentralization, and programmability.

Most of these benefits are easy to grasp, with one exception: programmable money.

Programmable money is an abstract concept, making it difficult for many to form a concrete understanding or appreciate its true significance.

The importance of programmable money lies in its potential as the only viable path to deliver essential financial services to billions of unbanked individuals. It is the only way to transform the economics of these services, enabling developers and fintech companies to innovate in areas where traditional financial systems cannot reach.

This article will explore specific examples enabled by programmable money and explain why it represents a major breakthrough in the global movement of money.

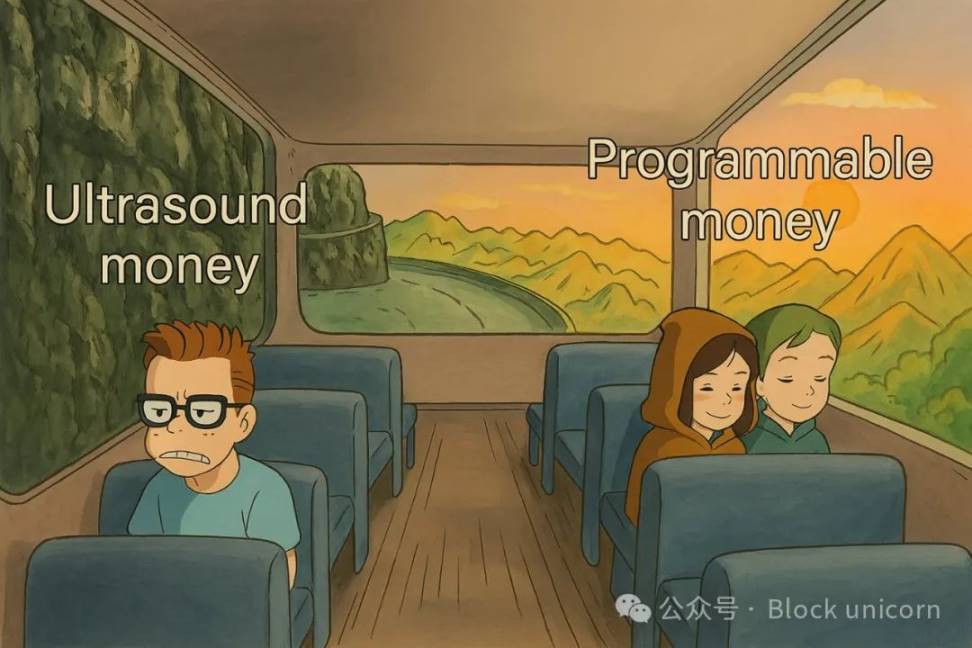

From Ultra-Sound Money to Programmable Money

Recently, I posted the following on Twitter, which I’d like to elaborate on:

Working in crypto should make us all aware of the power of memes. Whether true and meaningful or false and hollow, memes play a crucial role in spreading concepts across groups.

The previous dominant meme about money was Ethereum’s "ultra-sound money"—a guiding star concept.

For those who don’t recall, in short, Ethereum’s ultra-sound money is an evolved form of "sound money," leveraging scarcity and incentive mechanisms to ensure ETH maintains value over time and resists supply inflation. The term “ultra-sound” represents a modern framework for reliable wealth storage, around which much of the Ethereum community rallied in pursuit of this monetary policy.

However, the promise of ultra-sound money ultimately fell far short of expectations, leading to a decline in credibility.

Still, using memes to describe new forms of money remains powerful. The next meme representing monetary innovation is programmable money.

The beauty of programmable money is that its total addressable market (TAM) vastly exceeds that of ultra-sound money. This TAM is not cryptocurrency—it is money itself.

TAM Is Money, Not Cryptocurrency

I’m serious. Their goal is to take over money.

Money exists in vast quantities and various forms. Let me directly quote Bridget from her recent excellent piece on a new mental model for stablecoins.

Real Dollars and the Federal Reserve

Real dollars are entries on the Federal Reserve’s ledger. Currently, approximately 4,500 entities (banks, credit unions, certain government bodies, etc.) have access to these “real dollars” via master accounts at the Federal Reserve. None of these entities are natively tied to cryptocurrency, unless you count Lead Bank and Column Bank, which serve specific crypto clients such as Bridge. Entities with master accounts can access Fedwire—a near-zero-cost, almost instantaneous payment network that allows wire transfers nearly 23 hours a day with essentially instant settlement. Real dollars exist within M0: the sum of all balances on the Fed’s primary ledger. “Fake” dollars—created by private banks through lending—are part of M1, which is roughly six times larger than M0.

Block unicorn, WeChat Official Account: Block unicorn — Rethinking Ownership, Stablecoins, and Asset Tokenization

Here, Bridget touches on the meaning of M1 and M2 monetary categories. The only category relevant to stablecoins is M2 supply. M2 includes cash, bank deposits, and other liquid assets easily converted into cash, serving as a key metric for measuring stablecoins. The difference between M1 and M2 is that M1 is narrower, covering only cash and checking deposits, while M2 adds savings accounts and other near-cash liquid assets.

Currently, stablecoins account for more than 1.08% of the U.S. dollar M2 supply.

Again, there are many types of money—and here Bridget refers only to the U.S. dollar. There are many other currencies. Global liquidity, estimated as global M2, exceeds $90 trillion.

To reiterate: the TAM for money is enormous. And stablecoins aim to capture this market.

Programmable Money

The new meme targeting the largest possible market is programmable money.

Programmable money allows complex rules to be hard-coded directly into currency. While money serves as a store of value, another critical utility is its mobility. Stablecoins, due to their programmability, are redefining how money moves.

Stablecoins are digital cash—primarily tokenized versions of the U.S. dollar. Their programmability means software can define the conditions under which these assets transfer between wallets. Like programs or smart contracts, the rules and parameters governing how money moves operate autonomously.

By allowing financial transactions to execute and manage automatically based on preset rules, programmability dramatically improves efficiency in payments, settlements, and compliance. As a significant upgrade and breakthrough for financial systems, programmability enables cash to finally become truly digital.

Globally, the impact of programmability is profound—especially in developing regions, where stablecoins meet critical needs in remittances, microfinance, and daily transactions. Through the programmability of stablecoins, people in these areas gain access to services that enable real financial inclusion.

Examples of Programmability

To simplify the abstract concept of programmable money, here are several practical use cases.

Remittances

Imagine a system where smart contracts automatically convert the sender’s local currency into a stablecoin and transfer it to a recipient’s wallet abroad. The smart contract triggers upon meeting conditions, releasing the stablecoin and converting it into fiat, then transferring the funds. This eliminates intermediaries, reduces fees, and enables near-instant cross-border transactions.

Incorporating parameters such as payment confirmation or minimum amount thresholds highlights the application of programmability.

Global Payroll Systems

Consider a payroll solution using stablecoins to pay employees worldwide. For example, suppose you live in a developing country, work remotely for a U.S. company, but lack a U.S. bank account—and the company doesn’t use stablecoins. With a programmable payroll system, you could invoice the company in fiat, and the system would automatically convert it into stablecoins and send them to your wallet.

Similar solutions include scheduled disbursements of stablecoin payments to multiple wallets at set intervals. Stablecoins are only converted into the recipient’s local currency upon successful delivery.

Microfinance Solutions

In many developing regions, small business owners struggle to access bank loans. Decentralized lending platforms allow them to use stablecoins as collateral for microloans, with smart contracts managing collateral, disbursement, and repayment schedules. By removing barriers through programmable movement rules, access to these services becomes feasible for the first time.

Supply Chain Financing

Supply chains cover everything from raw materials to final consumers, including procurement, manufacturing, and distribution. Programmability brings a major breakthrough: smart contracts and blockchains can record data and automatically distribute stablecoins or cash based on progress along the supply chain.

Take an agricultural supply chain: farmers often supply produce to local cooperatives. Due to delays, poor communication, and overreliance on traditional finance, farmers may wait days or weeks to get paid. But by using sensors and trusted verification to track shipments, a smart contract can instantly release stablecoin payments to farmers once delivery is confirmed.

Digital Breakthrough

Programmability is the core catalyst for innovation, enabling iterative improvements and valuable lessons from experimentation.

Today, cash is inherently outdated—even its digital forms are limited in programmability. While fintech and open banking have advanced these systems, they remain constrained by the inherent limitations of traditional cash.

Programmability is a native feature of the digital age. Without true programmability, cash cannot fully transition into the digital realm. Therefore, as stablecoins now reach escape velocity, we are entering the first digital era of money.

Thank you, programmability.

In conclusion, forget ultra-sound money—programmable money has arrived.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News