Did the U.S. deliberately "want" an economic recession?

TechFlow Selected TechFlow Selected

Did the U.S. deliberately "want" an economic recession?

President Trump's statement that he "doesn't pay attention to the market" seems particularly significant.

Author: The Kobeissi Letter

Translation: TechFlow

Is the U.S. government anticipating an economic recession?

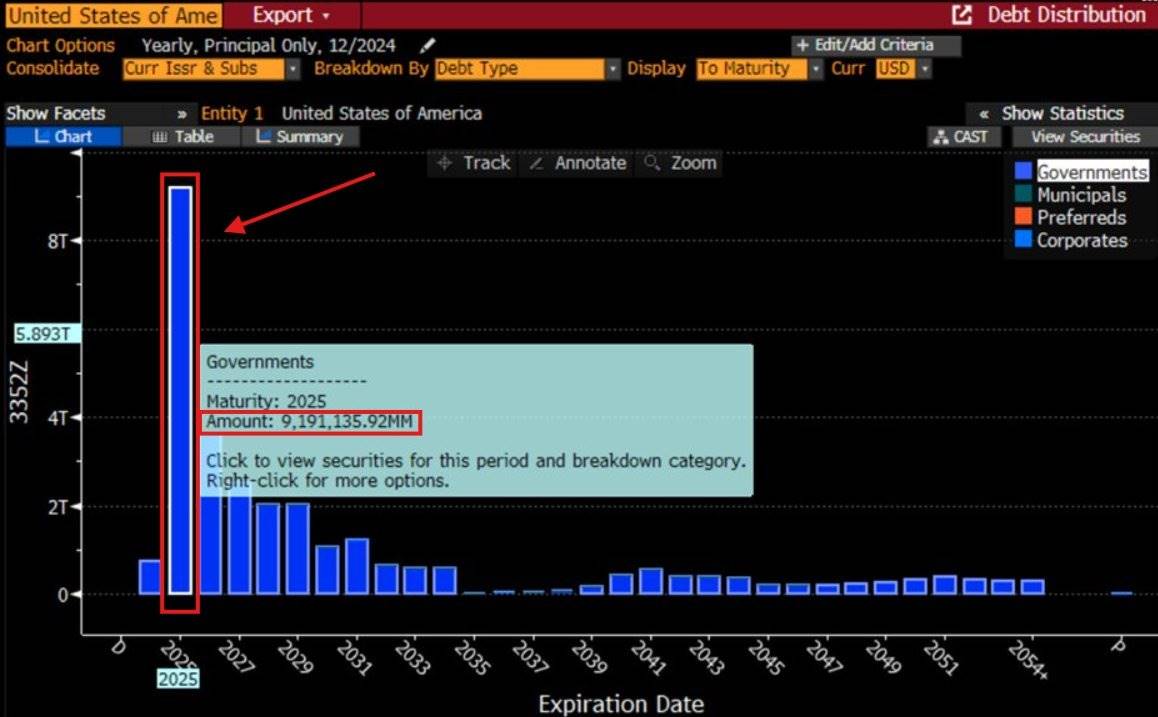

In 2025, $9.2 trillion of U.S. debt will mature or require refinancing. Facing this massive refinancing burden, the fastest way to lower interest rates might be triggering an economic recession.

But can the U.S. benefit from a market crash?

Over the past two months, the yield on 10-year Treasury bonds has dropped by about 60 basis points. Partly this reflects market expectations of reduced deficit spending by the Department of Government Efficiency. At the same time, it also relates to rising uncertainty and increasing likelihood of a U.S. economic recession.

An economic recession almost guarantees an interest rate cut.

But why does a recession imply lower interest rates?

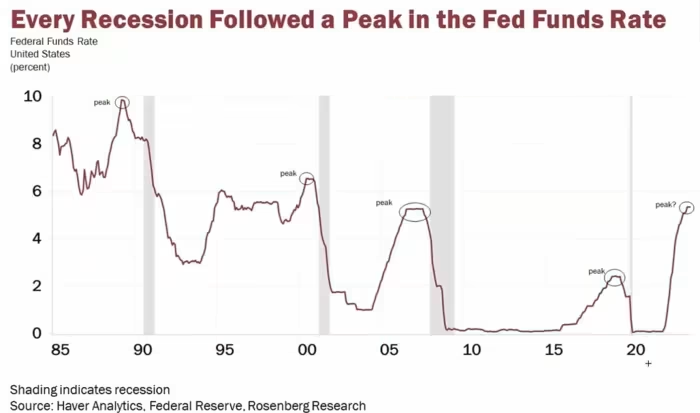

Since the 1980s, every U.S. recession has occurred after the federal funds rate reached its peak. When economic growth stalls, the Federal Reserve responds by "stimulating" the economy—meaning reducing interest rates to lower capital costs and encourage consumption.

Since the trade war began, expectations for U.S. economic growth have declined significantly. Meanwhile, oil prices have fallen to a new six-month low. More interestingly, President Trump has repeatedly stated that he wants to reduce inflationary pressure by lowering oil prices.

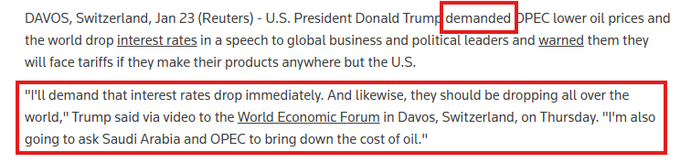

On January 25, President Trump claimed he had a solution to end the Fed's more-than-three-year battle against inflation. He urged OPEC to lower oil prices and called for global interest rate cuts.

However, the fastest way to lower oil prices is most likely through a demand-reducing economic recession.

In a recent interview with Fox News, President Trump said he would prioritize lowering interest rates.

He stated: "Interest rates are coming down... I'd also like to see energy prices go down." This comment was reported by @amitisinvesting.

Next, consider inflation data.

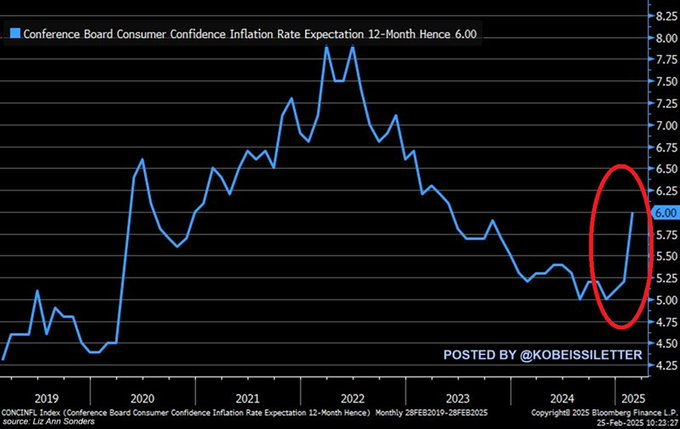

American consumers expect inflation over the next 12 months to rise to +6.0%, the highest level since May 2023. This marks the third consecutive month of rising inflation expectations.

Inflation is rising, rate cuts are being delayed, yet interest rates are falling.

The market is pricing in a recession.

In the midst of an inflation surge driven by the trade war, sharply lowering interest rates without triggering a recession seems nearly impossible. Moreover, on March 6, President Trump said he wasn't paying attention to the stock market at all. Yet in reality, as we saw during his first term, Trump consistently monitored financial markets closely.

This statement of "not watching the market" is therefore highly significant.

Given that he clearly pays close attention to markets, this serves as a signal to Wall Street—he is willing to cut interest rates and reduce the trade deficit at any cost, even if it risks triggering a recession.

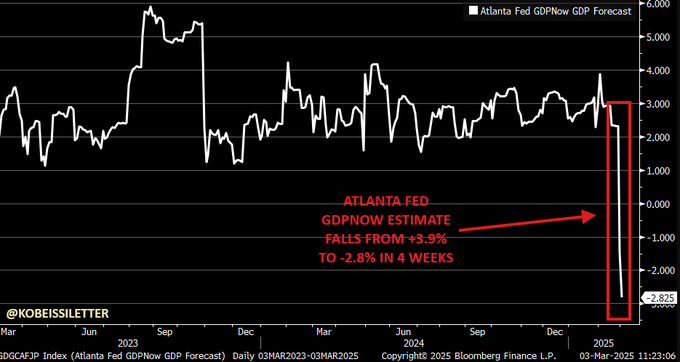

Amid the chaos of the trade war, we've seen economic growth expectations plummet. The Atlanta Fed last week revised its GDP growth forecast for Q1 2025 downward to as low as -2.8%. Consequently, market expectations for rate cuts surged sharply last week.

Was this intentional?

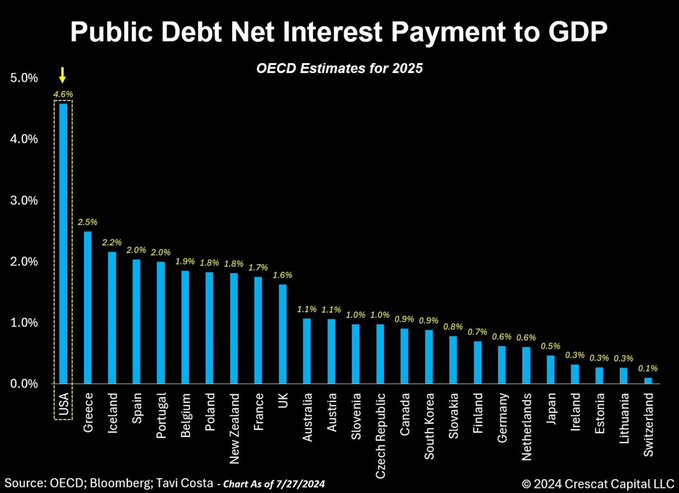

High interest rates represent the biggest challenge facing the U.S. government.

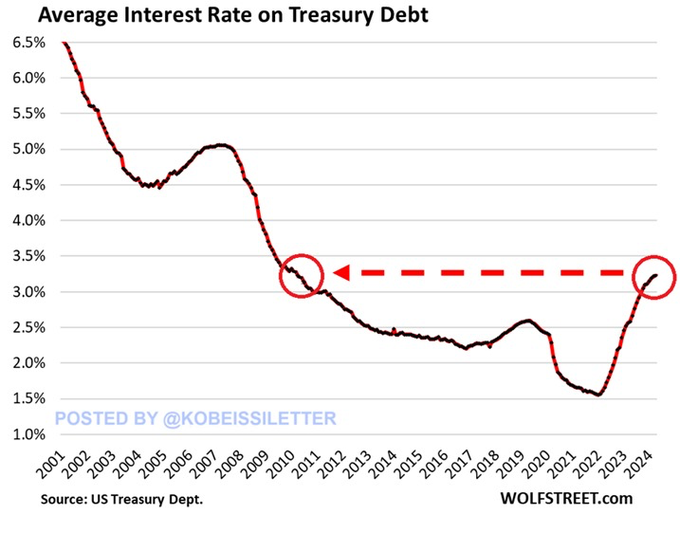

As interest rates climb, debt servicing costs increase dramatically. Currently, the average interest rate on the U.S.'s $36.2 trillion national debt stands at 3.2%, reaching its highest level since 2010. No one needs lower interest rates more than the U.S. government.

Moreover, rate cuts are becoming urgent:

$9.2 trillion of U.S. debt matures primarily in the first half of 2025, with 70% requiring refinancing between January and June 2025.

The average interest rate on this debt is expected to rise by approximately one percentage point.

In addition, efforts to reduce deficit spending won’t produce immediate results.

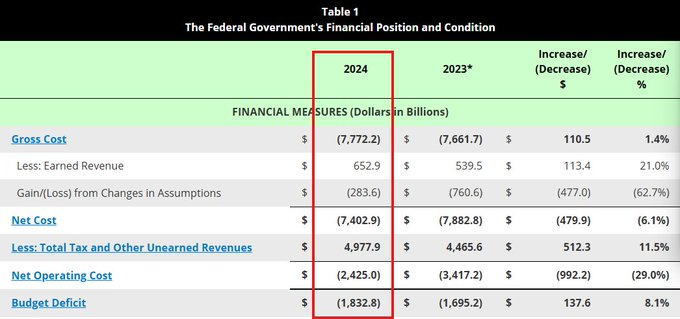

In fiscal year 2024, U.S. expenditures reached $7.8 trillion, while revenues were only around $5.0 trillion. This means that for every dollar of income, the U.S. incurs $1.56 in costs. The shadow of a debt crisis will loom over America for a long time to come.

These major shifts in the macroeconomic backdrop will have broad implications across markets, and we are actively identifying and capitalizing on opportunities within this environment.

Want to know how we trade these markets? Click the link below to subscribe to our premium analysis and alert service:

https://www.thekobeissiletter.com/pricing

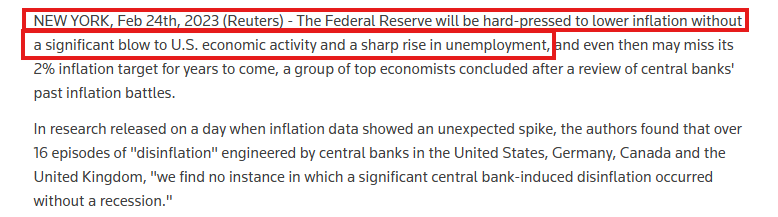

Finally, this brings us back to 2023, when the Fed nearly openly advocated using a recession to tame inflation.

In February 2023, numerous studies suggested that a recession might be the only viable solution. Later, the Fed shifted toward promoting a "soft landing" narrative, but this strategy has so far failed to meaningfully lower interest rates.

The reality is that the U.S. debt crisis is currently the most severe yet underappreciated crisis. While President Trump appears aware of this, it may already be too late. An economic recession may be the only feasible path to lower interest rates.

Follow us @KobeissiLetter for real-time analysis and updates.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News