How to leverage blockchain and Web3 to rebuild the traditional telecommunications industry?

TechFlow Selected TechFlow Selected

How to leverage blockchain and Web3 to rebuild the traditional telecommunications industry?

The transformation in the telecommunications industry is underway, potentially leading to a hybrid model of "centralized infrastructure + decentralized services" in the future.

By: Web3 Lawyer

Under the impact of global digitization and information waves, traditional business models in the telecommunications industry are facing unprecedented challenges. The rollout of next-generation 5G technology has placed immense upfront investment pressure on operators, yet their revenue models remain unchanged. Value-added services have not achieved meaningful breakthroughs, and operators are instead locked in fierce competition within saturated markets.

Data shows that while leading U.S.-listed telecom companies generate 50% higher revenues than internet giants, their profitability is only 30% of the latter's. Telecom profit margins stand at just 20% of those enjoyed by internet firms, net income hovers around 5%, and market capitalization reaches merely 30% of major tech companies. This reality reflects severe investor skepticism toward the telecom sector’s capital-intensive model and limited growth potential.

The telecom industry has been continuously evolving. For those involved in virtual operator businesses around 2015–2016, opening the telecom sector to private enterprises did not resolve core issues—whether it was competing in a saturated market or penetrating deeper into industries, this was never a fundamental transformation. We also explored international expansion back then, attempting collaboration with Lebara Mobile, Europe’s largest MVNO, but various obstacles prevented progress.

In hindsight, the eSIM global roaming scenario we envisioned would have been perfectly suited for implementation via Web3, later enabling value-added services through blockchain-based value transfer networks. However, blockchain and Web3 technologies had not yet emerged at that time—otherwise, the landscape might look entirely different today.

This article examines how blockchain technology and Web3 operational models can address current challenges in the traditional telecom industry. Through the case study of Roam, a Web3 decentralized telecom operator, we explore how blockchain and Web3 could reshape telecommunications—transforming communication networks into value exchange networks—and what such a shift may bring.

1. Challenges Facing Traditional Telecom Business Models

Traditional telecom operators center their business model on communication infrastructure, generating revenue through: 1) connectivity services, 2) value-added services, and 3) digital solutions for vertical industries. As they navigate technological evolution and market changes, their core logic follows a three-layer architecture: “connectivity + ecosystem + service.”

Basic communication services remain the primary revenue source, including mobile data, home broadband, and enterprise leased lines. For example, the adoption of 5G plans and gigabit fiber has driven growth in data traffic revenue. However, traditional voice and SMS revenues have sharply declined due to OTT apps like WeChat. To counter this trend, operators bundle offerings (e.g., “broadband + IPTV + smart home”) to increase user retention—China Mobile’s bundled package penetration exceeds 60%. Meanwhile, value-added services are becoming new growth engines across cloud computing, IoT, and fintech. In IoT alone, global operators now connect over 2 billion smart devices; China Mobile’s cloud revenue has grown 25-fold in three years, demonstrating strong digital transformation potential.

On the cost side, operators face dual pressures: 1) heavy capital expenditures and 2) the need for精细化 operations. 5G base station deployment, spectrum auctions (such as the $81 billion C-band auction in the U.S.), and data center investments drive up CAPEX, with global operators spending over $300 billion annually. To reduce costs, the industry adopts shared infrastructure (e.g., China Broadcasting Network partnering with China Mobile on 5G base stations), AI-powered energy-saving technologies (Huawei’s solution helps China Unicom save 10% power), and network virtualization (Open RAN reduces equipment costs by 30%). Yet, customer acquisition costs remain high in saturated markets, with device subsidies and channel commissions accounting for more than half of marketing expenses. This forces operators to shift toward digital direct sales—over 60% of subscriptions now occur via mobile apps.

Industry challenges stem from rapid technological shifts and cross-industry competition. Traditional service revenues are clearly declining: global voice revenue drops 7% annually, SMS revenue has shrunk by 90%, and average ARPU has fallen 40% over the past decade. Despite fast-growing 5G user numbers, return on investment takes years (estimated at 8–10). Operators must also contend with emerging competitors like Starlink satellite broadband and cloud providers’ edge computing services. For instance, SpaceX’s Starlink already serves 500,000 rural users, while AWS targets low-latency enterprise needs via Local Zones—pushing telecom operators to accelerate transformation.

(The Future of the Telecommunications Industry: A Dual Transformation)

Transformation paths for traditional telecom operators focus on technological upgrades and ecosystem restructuring. Technologically, network slicing, edge computing, and Open RAN open architectures are key innovations—for example, Deutsche Telekom offers 1ms-latency networks for autonomous driving, while AT&T provides dedicated channels for remote surgeries. On the ecosystem front, operators are shifting from being mere “data pipes” to “digital service engines”: South Korea’s SKT launched the metaverse platform Ifland, Jio integrates e-commerce and payments into a super app, and China Mobile enters content ecosystems via Migu Video. ESG strategies are also emerging as differentiators—Vodafone aims for 100% renewable energy by 2030, Verizon commits to cutting carbon emissions by 40% over ten years, reducing regulatory risks and attracting socially responsible investors.

2. Battling in Saturated Markets and Exploring Overseas Frontiers

The previous growth model—massive existing user base × basic telecom fees—is no longer sufficient to support enormous 5G CAPEX and high operating costs. The market has entered a phase where a few dominant players fight over a shrinking pie, each trying to deeply integrate into niche segments.

This is not only a crisis for telecom operators—it reflects a broader economic reality. I recall attending Luo Zhenyu’s year-end speech a few years ago (his outlook was bleak then, still relevant today)—the entire talk boiled down to two words: go global. But for telecom operators, going global is far from easy.

Telecom is an extremely sensitive sector in every country, making overseas expansion exceptionally difficult:

-

Market access restrictions: Most countries impose legal limits on foreign ownership (e.g., India caps foreign telecom investment at 50%), require local operations (e.g., Indonesia’s “data sovereignty law”), or outright ban foreign participation (e.g., North Korea, Cuba);

-

Different spectrum allocation rules: Global 5G frequency bands vary (e.g., China uses 3.5 GHz primarily, Europe favors 700 MHz), requiring customized equipment and increasing cross-border deployment costs;

-

Strict data localization requirements: Regulations like the EU’s GDPR and Russia’s Data Localization Law mandate domestic storage, restricting cross-border data flows;

-

Local monopolistic market structures: Two to three domestic operators dominate most markets (e.g., SKT, KT, LG U+ control 98% of South Korea’s market), creating strong user inertia;

-

Price wars and subsidy culture: Emerging markets (e.g., Southeast Asia) rely on low-cost plans and phone subsidies, forcing multinational entrants to bear high costs (e.g., Vodafone exited India after losses from price competition).

To overcome these barriers, strategies such as equity investments (e.g., Singapore’s Singtel gaining indirect Asian market access via stakes in India’s Airtel and Indonesia’s Telkomsel), joint ventures (e.g., China Unicom and Telefónica forming a JV to share Latin American resources), or MVNO models (e.g., UK’s Virgin Mobile entering Australia and South Africa via network leasing to minimize infrastructure investment) still lead back to the same root problems—intense competition in limited markets, massive capital outlays, and the persistent question: where is the return?

(SK Telecom accelerates AI push via alliance with more partners)

Thus, for telecom operators venturing abroad, full globalization remains unattainable. Instead, “limited globalization” can be achieved through capital partnerships, technology alliances, and vertical-specific services. Going forward, “global capability, local delivery” will define international telecom operators:

-

Core network layer: Build global backbone networks using undersea cables, satellites, and cloud services, while complying with national data sovereignty laws.

-

Technology standards layer: 6G development is already fragmenting into U.S.-China-EU “technology blocs,” forcing operators to pick sides amid standard divergence.

-

Service application layer: Highly localized, relying on joint ventures or local teams—for example, Orange launching M-Pesa mobile payments in Africa.

3. Reimagining Telecom with Web3

Clearly, limited globalization and survival in fragmented markets aren’t satisfactory outcomes. We can completely rebuild the telecom industry using blockchain technology and Web3 operational models. Web3 transformation of telecom is not simply about “adding blockchain”—it involves leveraging globalization, token economics, decentralized governance, and open protocols to elevate communication networks into foundational layers for value exchange, supporting future digital civilizations. Operators who resist change risk becoming mere “plumbers”; those embracing reinvention could become routing hubs of the next-generation value internet.

(The 「Internet of Value」: 8 Top Sectors Being Transformed by Blockchain)

At the infrastructure level, physical network resources are tokenized for distributed sharing—the Web3 decentralized telecom operator Roam has proven the feasibility of rewarding users with tokens for contributing Wi-Fi hotspots, building a decentralized communication network spanning millions of nodes and over two million users, challenging traditional operators’ cell tower monopolies. Spectrum resources can be governed via DAOs—for example, BT’s experimental “5G spectrum NFTs” allow idle bands to be auctioned on-demand via smart contracts, improving utilization and generating shared revenue. User identity management is also being redefined: Spain’s Telefónica collaborates with Evernym on a decentralized identity (DID) solution, allowing users to own SIM card data while operators act only as verification nodes, reducing privacy risks. Data sovereignty returns to users—South Korea’s SK Telecom’s blockchain data marketplace enables users to trade anonymized behavioral data for tokens, transforming operators into transaction facilitators.

Automated cross-border services and settlements offer another breakthrough. The CBSG consortium—including AT&T and Orange—uses blockchain to overhaul international roaming settlement, reducing reconciliation cycles from 30 days to real-time splits and cutting costs by 40%. DeFi principles enter pricing models: users stake stablecoins to receive discounts, while operators issue proprietary tokens (e.g., hypothetical Verizon VZW Token) to reshape payment ecosystems. In IoT, combining blockchain with edge computing creates autonomous device networks—Deutsche Telekom and Fetch.ai co-developed a车联网 protocol enabling smart cars to bid for roadside base station access, achieving ultra-low latency. Ericsson uses blockchain to trace 5G base station components, enhancing supply chain transparency.

Furthermore, economic models witness atomic-level convergence between telecom and finance: users pay for services in cryptocurrency while earning rewards by sharing bandwidth, data, or even physical activity (e.g., Telefónica’s “motion mining”), forming a “consume-produce” loop. DeFi mechanisms spawn innovative services like communication insurance and cross-chain roaming, with on-chain smart contracts automating international settlements, slashing costs by over 40%.

Case Study: Web3 Decentralized Telecom Operator Roam

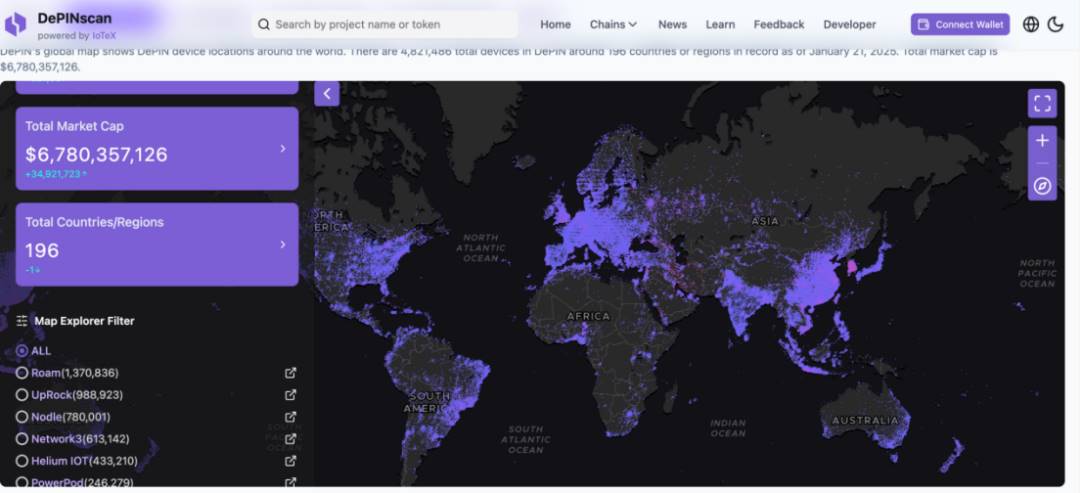

Roam aims to build a global open wireless network ensuring free, seamless, and secure connectivity for humans and intelligent devices, whether stationary or mobile. Unlike traditional telecom operators constrained by geography and homogenized offerings, Roam leverages blockchain’s inherent global advantages. By constructing a decentralized communication network based on the OpenRoaming™ Wi-Fi framework and integrating eSIM services, Roam has created a globally accessible, free wireless network.

In just over two years, Roam has deployed 1,729,536 nodes across 190 countries, serving 2,349,778 app users, conducting 500,000 daily network verifications—making it the world’s largest decentralized wireless network. Moreover, users earn free eSIM data when building or validating Wi-Fi nodes, positioning Roam as a telecom provider operating under an internet-native model.

(depinscan.io/projects/roam)

Globally, traditional Wi-Fi still carries over 70% of data traffic, yet outdated infrastructure and privacy concerns limit its potential. To address these issues, Roam partners with the Wi-Fi Alliance and Wireless Broadband Alliance (WBA), combining legacy OpenRoaming™ technology with Web3’s DID+VC frameworks to create a decentralized communication network. This approach significantly lowers initial network deployment costs while delivering cellular-like seamless login and end-to-end encryption. Users experience frictionless connectivity without repeated logins, greatly enhancing usability and connection stability.

Roam’s decentralized deployment offers an innovative path for upgrading OpenRoaming™ Wi-Fi. Leveraging Wi-Fi’s natural role as an entry point, Roam bridges Web2 and Web3 ecosystems, redefining telecom service standards in user experience and data governance through decentralization.

Roam encourages users to co-build the network via the Roam App by sharing Wi-Fi nodes or upgrading to more secure and convenient OpenRoaming™ Wi-Fi. Users enjoy seamless access across four million OpenRoaming™ hotspots worldwide, and even find Roam-built nodes in remote areas like Siberia and northern Canada, vastly expanding coverage and improving user experience.

Additionally, Roam’s eSIM is critical to its vision of a global open wireless network. Users activate data plans directly on devices without physical SIM cards, simplifying usage. Roam eSIM covers over 160 countries, offering flexible, cost-effective connectivity for travelers and business users.

Through free global access via Wi-Fi + eSIM and diverse incentive mechanisms, Roam drives rapid growth of its decentralized network. Innovative reward systems let users earn global data or Roam points by checking in, inviting friends, or engaging with Roam’s social media—creating sustainable income streams.

(weroam.xyz/)

4. Communication as a Value Exchange Network

Beyond reconstructing business models via Web3, blockchain-powered telecom networks represent a transformative leap. The essence of blockchain- and Web3-driven telecom transformation is elevating communication networks into value exchange networks—evolving from “transmitting information” to a triad of “information + value + trust,” forming the foundational layer of next-generation digital societies that integrate value transfer, data ownership, and trusted collaboration.

Web2 internet infrastructure enabled near-frictionless information flow—but value itself remained stuck. Web3’s value internet enables value to flow as freely and seamlessly as information does. At its core, payment is simply the exchange of value.

Historically, advances in communication technology have profoundly reshaped financial payment systems. Each breakthrough brought qualitative leaps in payment forms. From Morse code clicks in the 19th century to instant blockchain settlements today, communication technology has revolutionized finance by improving information transmission efficiency, expanding connectivity boundaries, and重构ing trust mechanisms.

4.1 Information Transmission Efficiency: Breaking Down Temporal and Spatial Barriers to Value Transfer

The telegraph first enabled cross-border, real-time value transfer. After the transatlantic cable launched in 1858, interbank transfers dropped from weeks to hours, shattering financial time-space barriers. SWIFT’s electronic messaging system, established in 1973, reduced traditional Telex-based cross-border payments from 3–5 days to T+1, processing 42 million payment messages daily—laying modern foundations for global payments. The internet era’s TCP/IP protocol enabled millisecond-level electronic payments. Blockchain replaces centralized financial communication with P2P networks, creating intermediary-free value transfer channels. Compared to SWIFT’s centralized message exchange, blockchain boosts communication efficiency hundreds of times over. Similarly, Web3-based telecom networks can dramatically enhance value exchange efficiency.

4.2 Expanding Connectivity Boundaries: Building the Nervous Endings of Financial Inclusion

Cellular mobile networks extend payment access to every corner of the physical world. 2G-enabled SMS payments sparked a financial inclusion revolution in Africa—Ethiotelecom’s HelloCash used USSD channels to deliver financial services in regions with less than 40% base station coverage. Likewise, the global network built by Roam can provide bank-grade financial services on the blockchain to all connected individuals—especially the 1.4 billion people currently excluded from banking—whether in the Amazon rainforest or deep in Africa, truly realizing financial inclusion and equity.

Beyond geographic reach, communication networks connect silicon-based civilizations. IoT communication creates new payment scenarios. NB-IoT-enabled smart meters in Italy’s ENEL automatically deduct electricity bills. LoRaWAN-connected vending machines at Japan’s Lawson complete over 2 million unmanned transactions monthly. 5G’s 1ms ultra-low latency and capacity for connecting millions of devices support Tesla’s V2X-enabled automatic charging payments. As AI agents proliferate, communication networks—and value transfer atop them—will be essential for interactions between AI agents and between AI and humans.

4.3 Trust Mechanism Reconstruction: In Trustless We Trust

The Bitcoin whitepaper envisioned a world without trusted intermediaries—where cryptography and code establish trust inherently. Yet, when this idealistic crypto world meets harsh reality, compromise isn’t the only option. How do we build trust mechanisms on blockchain networks?

“On-chain banks” powered by blockchain and Web3 already replicate many functions of developed-world banks: savings (self-custody), investment and yield generation (DeFi staking or RWA products), fund transfers (blockchain P2P), and consumption (stablecoin payments/receipts).

These bank-grade services require only internet access—something projects like Roam can further enable. As mechanisms evolve, more financial services built on blockchain communication networks will emerge. Future innovations may include a “global instant settlement network” or “AI-native financial entities,” blending communication and payment into new forms.

Case Study: Orange Money’s Mobile Payment Expansion in Africa

Orange Money exemplifies how telecom operators deepen localization through fintech. Though a traditional telecom play, it offers valuable lessons for Web3 telecom innovation.

Africa presents a blue ocean for mobile payments due to low traditional banking penetration (only 34% of adults south of the Sahara have bank accounts) but high mobile adoption (80%). Leveraging its 130 million African users, Orange launched Orange Money in 17 countries, reaching over 40 million users. It adopted differentiated strategies: in East Africa (e.g., Kenya), dominated by M-Pesa, it competes on lower fees and higher agent commissions; in French-speaking West Africa (e.g., Senegal), it captures over 60% market share through language alignment and village-level agent networks, while collaborating with M-Pesa on cross-border payments. Its success lies in vertical integration—partnering with agricultural cooperatives for disbursements, linking to government utility payments, and launching microloans (OKash) and low-cost remittances (fees cut by 30%)—forming a “telecom + payment + finance” ecosystem. Still, market fragmentation persists: M-Pesa dominates East Africa ($12B monthly transactions), MTN leads West Africa, and local giants battle global players like PayPal. Orange increased user ARPU by 20%, uses transaction data to improve risk control (NPL < 5%), but faces slim profits (net margin 3–5%), high cybersecurity spending (30% of IT budget), and political instability in Francophone regions. Going forward, Orange plans to integrate payments, e-commerce, and content into a super app and pilot the West African digital currency “Eco.” Its journey proves that in underserved markets, operators must deeply embed into local scenes, channels, and cultures—yet sustained growth depends on ecosystem synergy and regulatory balance.

(Orange Money: Fintech is proving a game changer in Africa)

5. Final Thoughts

The transformation of the telecom industry is underway. The future may see a hybrid model of “centralized infrastructure + decentralized services”: one type of operator maintains the role of “plumber,” controlling physical layers like fiber and spectrum, but opens network capabilities via APIs for DePIN projects—e.g., Vodafone tokenizing network slices so enterprises can purchase dedicated channels with cryptocurrency. Another type, like Roam, will leverage communication networks and blockchain to reinvent themselves as decentralized value routing hubs—not confined locally, but operating globally on communication-based ecosystems. Crucially, users must shift from passive consumers to active ecosystem co-creators to fully advance the Web3 telecom ecosystem.

The ideal of a Network State must be built upon communication networks. Projects like Roam—a Web3 decentralized telecom operator—may well become the digital foundation of that ideal society.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News