Bull vs Bear: Are You Still Bullish on the Market Outlook?

TechFlow Selected TechFlow Selected

Bull vs Bear: Are You Still Bullish on the Market Outlook?

Or perhaps we are currently in a "wealth destruction" phase.

Author: Michael Nadeau

Translation: TechFlow

Hello readers, we conducted some polls last week on X and LinkedIn, and many of you expressed a desire to see more data/analysis on the current cycle.

So this week’s focus will be answering these questions: Is there still a bull market in crypto for 2025? Why do I still feel bearish despite so many positive catalysts? And how should we think dialectically about the state of the cycle?

Let’s go!

Bearish View

Before diving into on-chain data, I’d like to share some qualitative thoughts on how we view crypto cycles.

Early Bull Phase

This period spanned roughly from January 2023 to October 2023.

It was the market rebounding from the FTX collapse. This phase was very quiet—low trading volumes, near-silence on crypto Twitter. Then prices began rising again.

Bitcoin climbed from around $16,500 to $33,000.

Yet, no one called this a bull market at the time. During the "early bull" phase, most market participants remained on the sidelines.

Wealth Creation Phase

Roughly from November 2023 to March 2024.

This stage saw significant price surges and notable wealth creation. For example, SOL rose from $20 to $200. The Jito airdrop (December 2023) created massive wealth within the Solana ecosystem and repriced Solana DeFi projects (e.g., Pyth, Marinade, Raydium, Orca). The VC market also peaked during this time.

Bitcoin surged from $33,000 to $72,000. Ethereum moved from $1,500 to $3,600.

Bonk’s market cap grew from $90 million to $2.4 billion (26x). WIF’s market cap jumped from $60 million to $4.5 billion (75x). This phase also planted the seeds for the broader “Memecoin season.”

Still, this period remained relatively “quiet.” Your average friend probably wasn’t asking you about crypto yet.

Wealth Distribution Phase

Approximately from March 2024 to January 2025.

This was the peak of attention. We frequently saw “WAGMI” (We’re All Gonna Make It), rapid rotations, new fads (quickly fading), and blind investments being rewarded. Celebrities and other “crypto tourists” typically entered the market here. Headline-grabbing news such as “Tesla buying Bitcoin” or “strategic Bitcoin reserves” often emerged.

Why?

Because new investors rushed in due to such news, fearing they were “missing out on the party.”

This marked the second wave of “Memecoin season,” later evolving into “AI agent season.” During this phase, the market overlooked many clearly problematic behaviors. No one wanted to point out issues because everyone was making money.

And then we arrived at today’s situation.

Wealth Destruction Phase

We believe this phase began shortly after Trump took office.

It's the period immediately following a top, where bullish catalysts have already passed. Seemingly positive news now triggers bearish price action.

In the current environment, political moves around a “strategic Bitcoin reserve” have failed to move markets—an important signal. During this phase, market rallies often hit key resistance levels and ultimately fail (as we saw last week with Trump’s tweet on crypto reserves).

We monitor several additional signals during the “wealth destruction” phase:

-

Clearances and “panic” events that shake the market but still fail to fully awaken it—we’ve seen parallels in the DeepSeek AI panic and tariff uncertainty.

-

Investors still clinging to “fantasies.” Today, we see widespread discussion about falling USD and global M2 growth (explained in detail later in the report).

-

“Speculators” flooding the market. More people DM us to “check their project,” more ads appear, well-funded projects waste money at conferences and engage in excessive PvP. The entire industry takes on a dirtier vibe. Bad actors begin to surface during “wealth destruction.”

Hidden problems gradually emerge—often after liquidations. Last cycle, it started with Terra Luna, which led to the collapse of Three Arrows Capital, followed by BlockFi, Celsius, FTX, and eventually Genesis’ shutdown and CoinDesk’s sale.

We haven’t seen any blow-ups yet. Blow-ups in this cycle may be fewer—simply because there are fewer CeFi firms left, meaning the bottom could be higher when the market finally clears.

Where might blow-ups come from?

No one knows, but we see a few “suspects” worth watching:

-

Exchanges: Watch for hidden leverage and/or potential fraud in overseas “Tier B and C” exchanges.

-

Stablecoins: We’re monitoring Ethena/USDe—currently with nearly $5.5 billion in circulating stablecoins. It maintains its peg and earns yield via cash-and-futures basis trades (holding spot, shorting futures)—a model that was a major source of leverage last cycle (via Grayscale). Ethena’s reliance on centralized exchanges adds counterparty risk. Additionally, MakerDAO has invested part of its reserves in USDe, increasing contagion risk in DeFi.

-

Protocols: Be alert to frequent hacks and potential liquidation cascades triggered by over-collateralized loans on platforms like Aave—Aave still has over $11 billion in active loans (down from a peak of $15 billion).

-

Strategy: We believe Strategy has managed debt prudently, with most debt being long-term unsecured or convertible bonds (BTC holdings won’t trigger margin calls). They also survived a 75% BTC drawdown last cycle. That said, a sharp BTC drop could force Saylor to sell large amounts of BTC at the worst possible moment.

The best time to re-enter the market is late in the wealth destruction phase. We believe that moment has not yet arrived.

Bearish Data

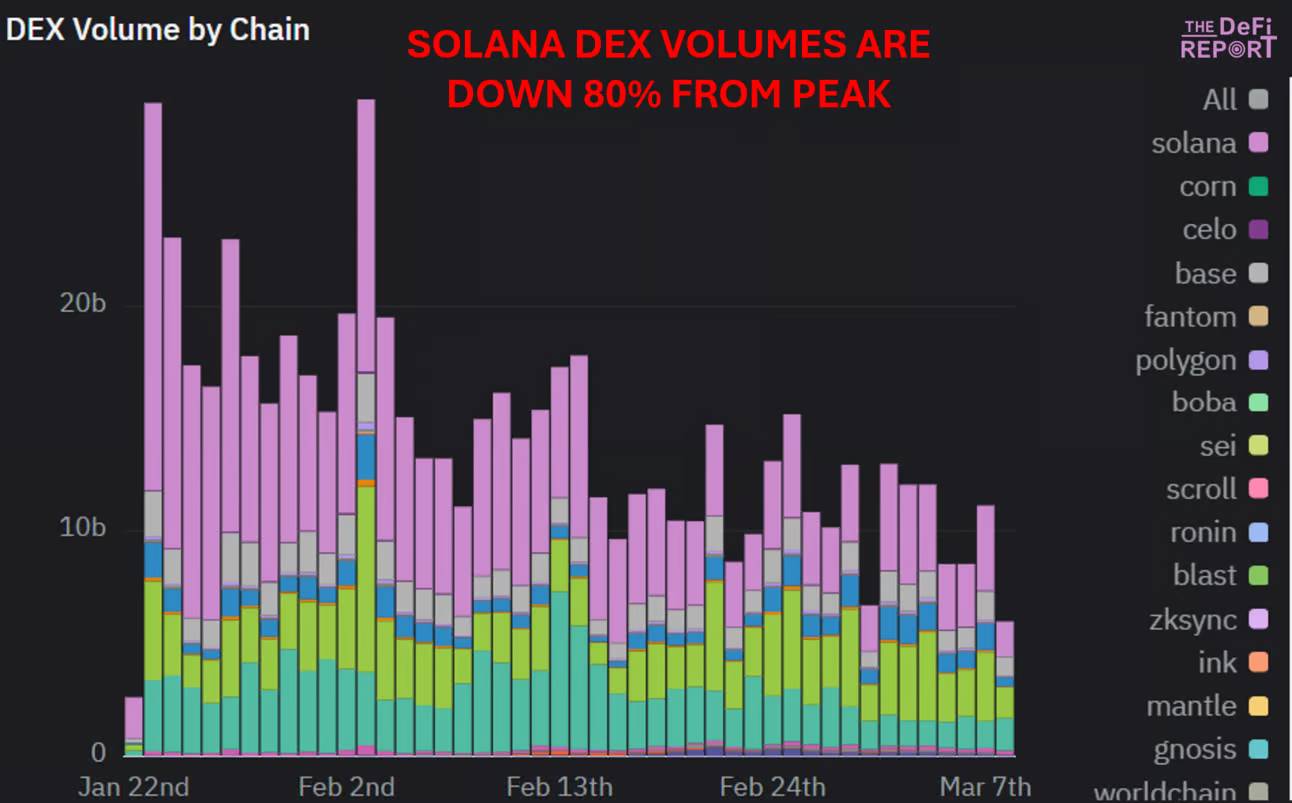

DEX Trading Volume

Solana DEX trading volume has dropped 80% from its peak following Trump’s Memecoin launch. Meanwhile, the number of active unique traders has declined by over 50%. This suggests waning speculative enthusiasm.

Data: The DeFi Report, Dune

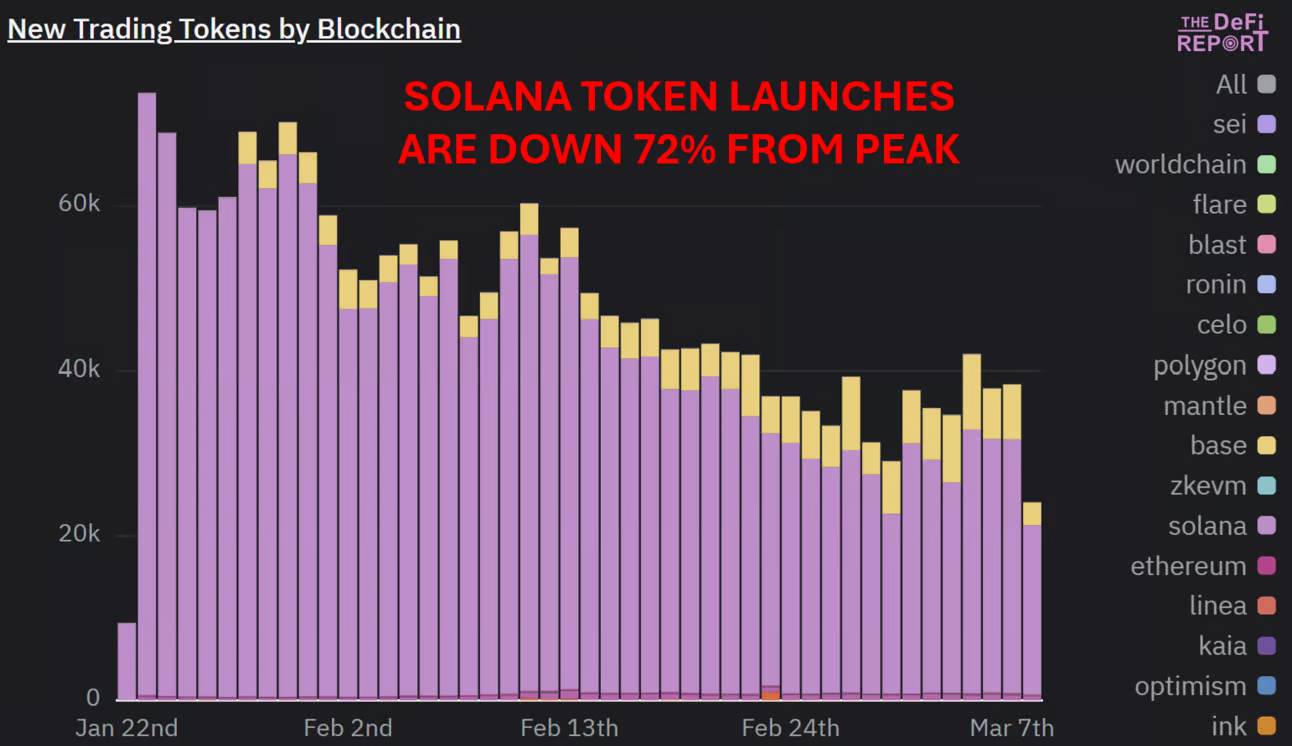

Token Issuance

Token creation on Solana has declined 72% from its peak. Nevertheless, over 20,000 tokens are still created daily on the chain.

Data: The DeFi Report, Dune

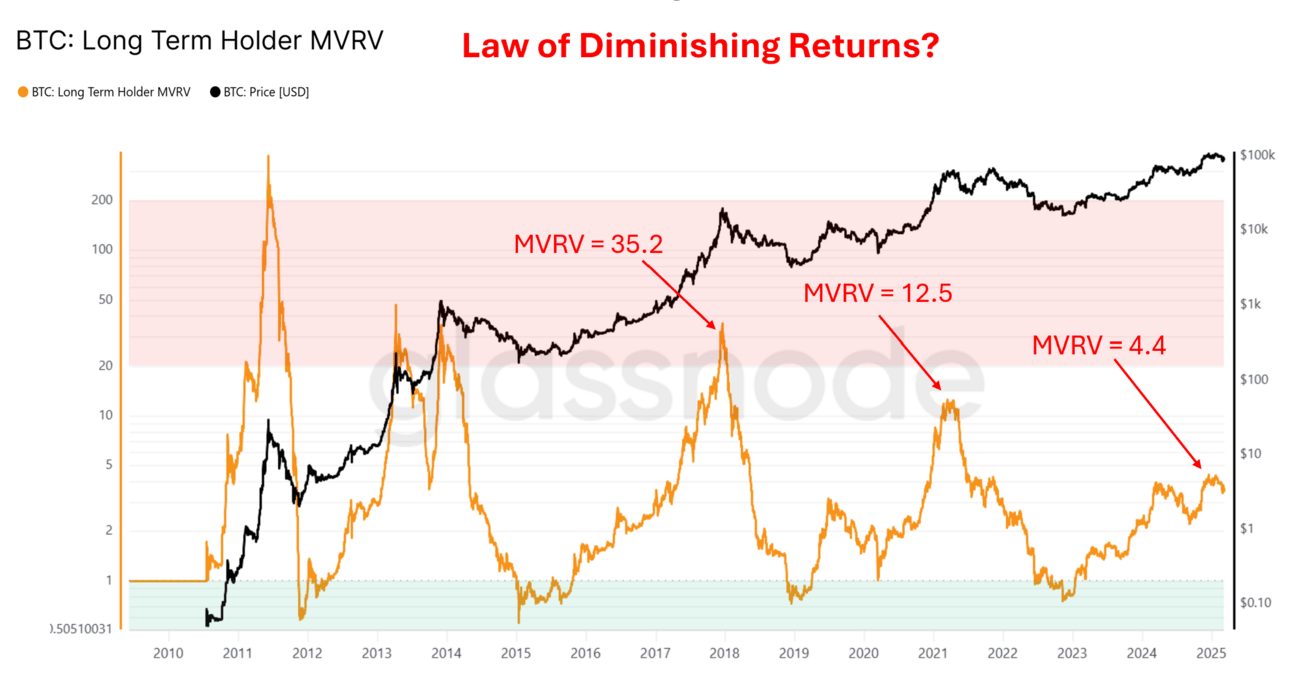

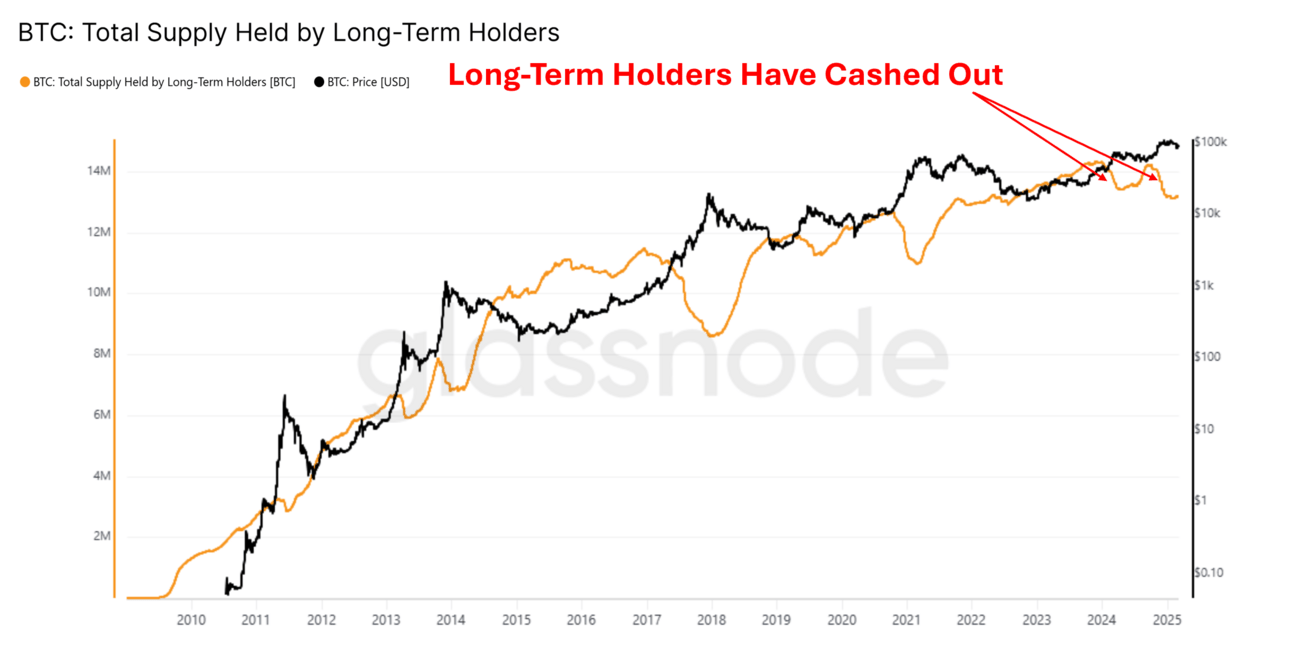

BTC Long-Term Holder MVRV Ratio

Data: Glassnode

Bitcoin’s Long-Term Holder MVRV (“smart money”) peaked at 4.4 last December. That’s only 35% of the 2021 cycle peak of 12.5, which itself was 35% of the 2017 peak.

BTC rose ~80x from low to high in 2017, ~20x in 2021, and ~6.6x in this cycle.

Bitcoin’s realized price (the average cost basis of all circulating BTC) peaked at $5,403 in the 2017 cycle—15.1x higher than the 2013 cycle peak. In 2021, it reached $24,530—4.5x higher than 2017. Today’s realized price is $43,240, 1.7x the 2021 peak.

Conclusion

-

Each data point shows symmetrical declines across cycles. This clearly indicates the law of diminishing returns is in effect.

-

Bitcoin is now a $1.7 trillion asset. No matter how bullish the news, investors shouldn’t expect sustainable parabolic growth—the capital required to push it higher is simply too large now.

-

When Bitcoin loses momentum, the rest of the market suffers heavily.

-

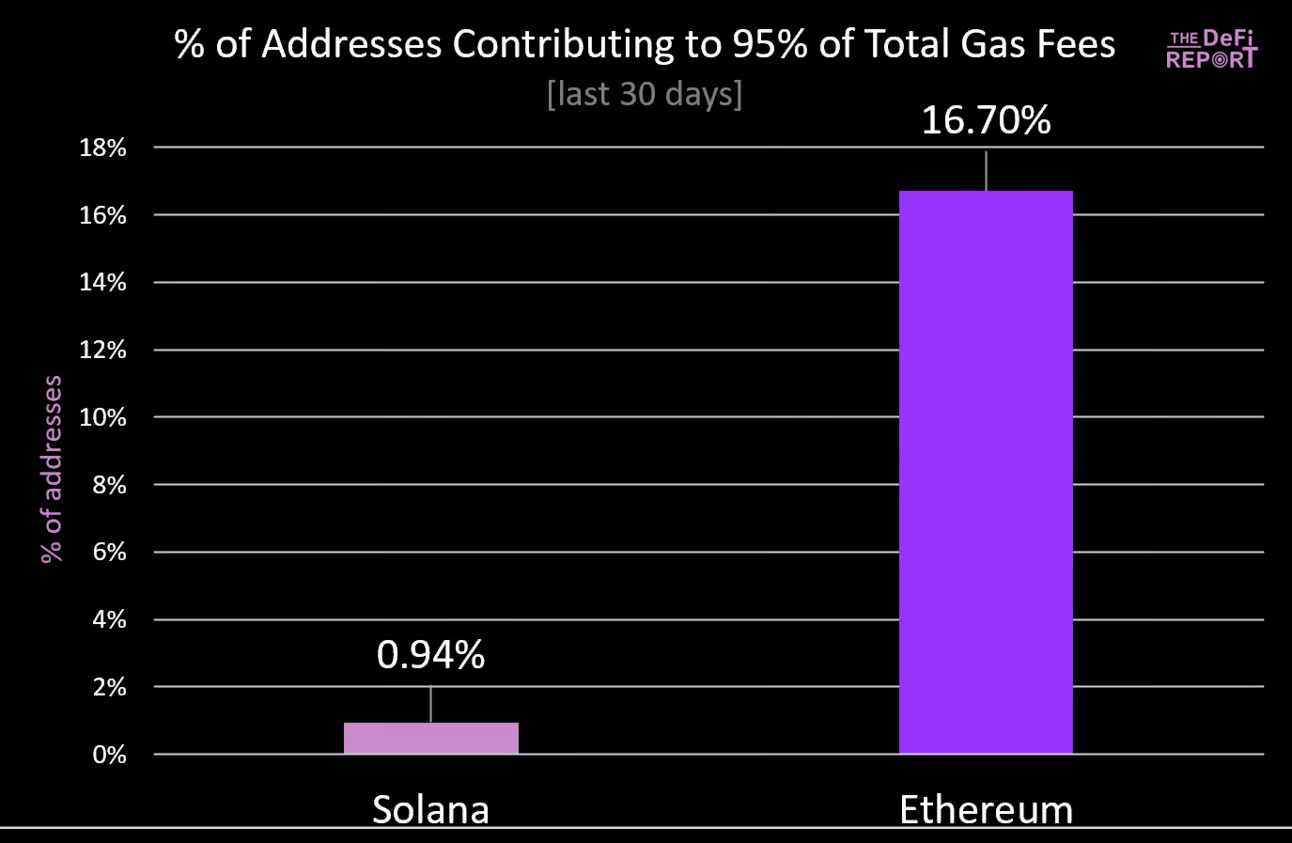

Speculative fervor on Solana is cooling. Given that 61% of DEX volume year-to-date involves memecoins, we worry Solana’s “recovery story” rests on a house of cards. Moreover, in the past 30 days, less than 1% of Solana users paid over 95% of gas fees. This is concerning—it suggests a small group of users (“whales”) are extracting value from the majority (“minnows”). If “minnows” grow tired of losing and exit (which we believe they are doing), Solana’s fundamentals could deteriorate rapidly.

Data: The DeFi Report, Dune (base + priority fees + Jito tips on Solana)

-

Bitcoin’s long-term holders have taken profits twice in the past year. Their current realized price (cost basis) is around $25,000. Short-term holders who bought near the top have an average cost basis of $92,000 and are underwater. As the market accepts that BTC’s top occurred at $109,000, we expect these short-term holders to continue selling into lower highs.

Data: Glassnode

When laid out like this, we believe it’s undeniable: the “typical” cycle has completed, and this isn’t just some “law” at work.

In our view, the best way to handle this is to accept reality and assign a probability to the possibility that the cycle has topped. We believe that probability is clearly above 50%.

After completing the fundamental analysis, we try to find holes in our argument and stress-test our views.

Let’s begin.

Bullish View

I still observe considerable resistance to bearish narratives—bulls aren’t giving up easily.

This raises a question: Do bullish arguments further prove we’re in the “wealth destruction phase”? Or are we overly bearish, overlooking another potential leg up?

In this section, we’ll review some observed “bullish” arguments.

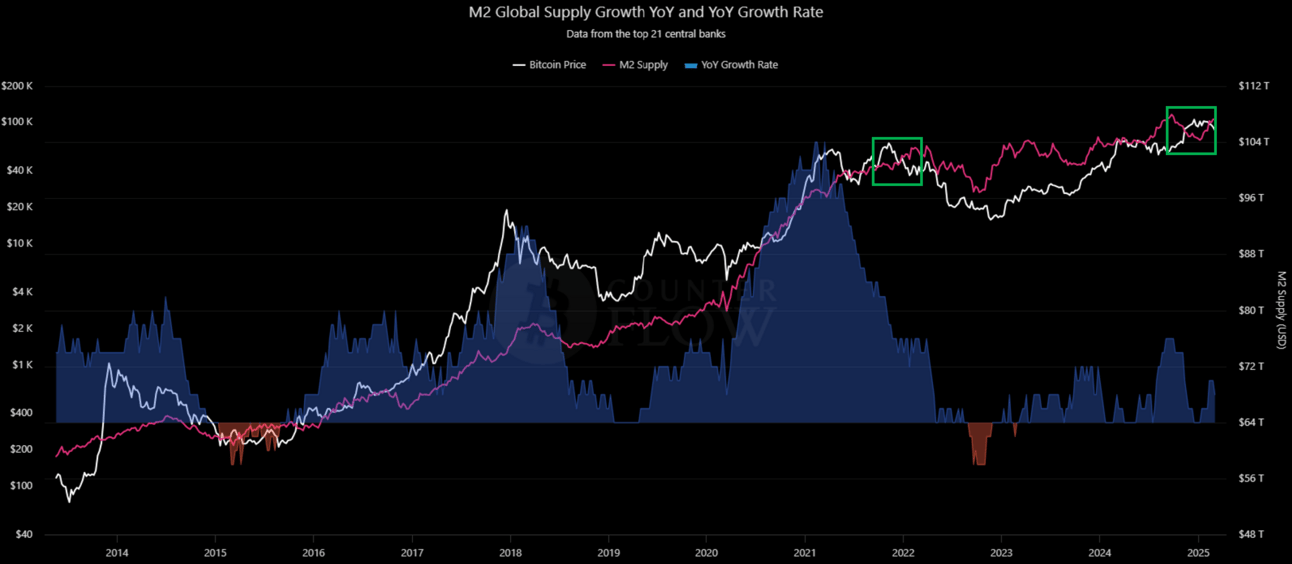

Global M2 / Liquidity

Data: Bitcoin Counter Flow

The green box on the right shows: global M2 rising while BTC falls. Some highlight this, noting BTC’s correlation with M2 and its typical 2–3 month lagged response to M2 changes.

The green box on the left shows: a similar dynamic occurred at the end of the last cycle—M2 rising while BTC fell. In fact, M2 didn’t peak until early April 2022—five months after BTC topped.

Since mid-January, global M2 has grown 1.87%, mainly due to central banks shifting from tightening to easing.

This is favorable for liquidity conditions.

However, several questions remain:

-

What’s driving M2 growth? We believe it’s primarily due to the dollar weakening (down 4% since February 28!), meaning foreign currencies priced in USD increase, boosting global M2. Additionally, the reverse repo facility has recently been drained, and China is stimulating its economy through easing.

-

Will this trend continue? We expect the dollar to keep falling as capital flows overseas, though the pace may slow in coming weeks. We anticipate China will continue easing amid a weaker dollar. However, the Fed is unlikely to ease soon, citing “ample” reserves. We also believe the Fed remains inflation-conscious.

-

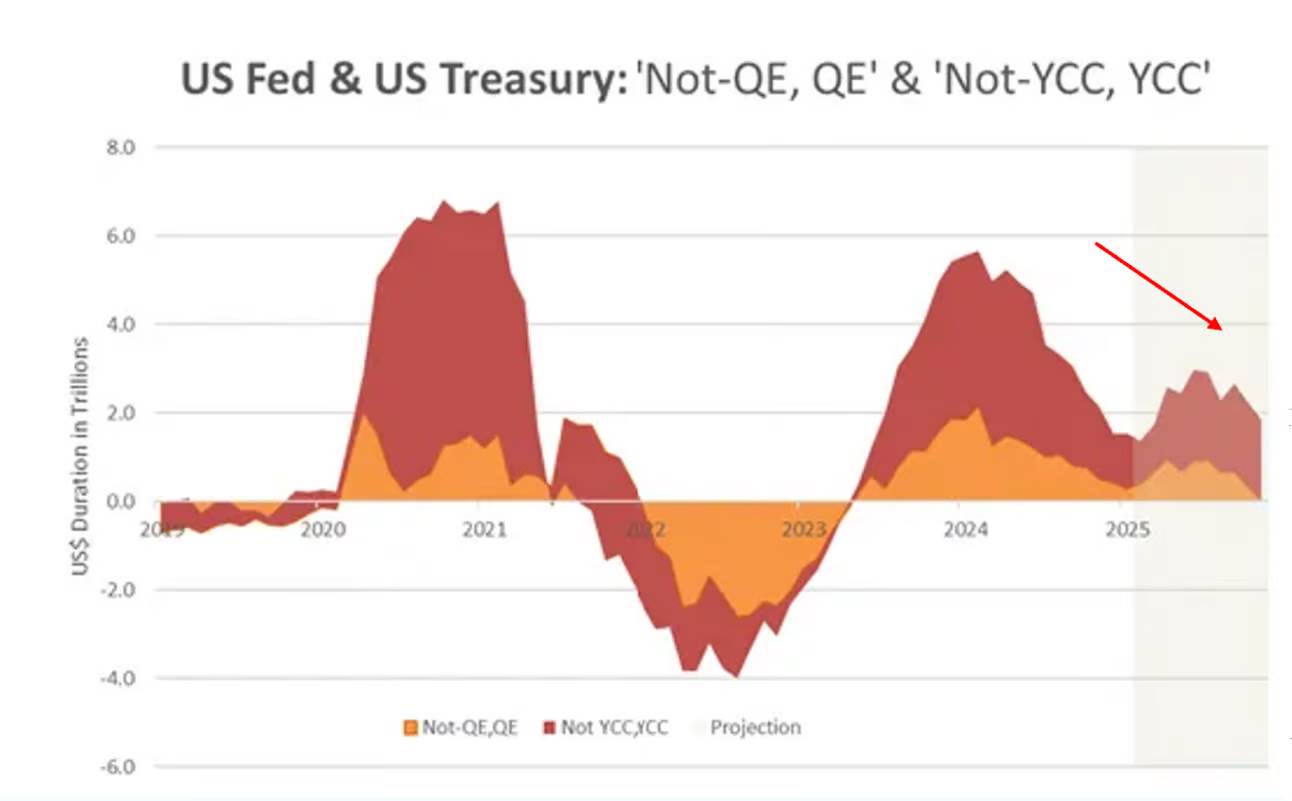

How do current liquidity conditions compare to last year? We view current liquidity as a headwind compared to last year. Remember, it’s the rate of change that matters, not just nominal growth. We strongly believe that last year, the Fed and Treasury drove markets via “shadow liquidity”—i.e., “not-QE, QE” and “not Yield Curve Control, Yield Curve Control”—to support Biden/Harris re-election. According to Cross Border Capital’s Michael Howell, the removal of these policies significantly impacted the rate of change.

Data: Cross Border Capital

These “stealth stimulus” measures reportedly injected $5.7 trillion into U.S. markets by early 2024—achieved by draining reverse repos and front-loading new bond issuance.

Finally, investors should closely watch Treasury Secretary Bessent’s recent CNBC interview: “Markets and economies are addicted. We’ve become dependent on government spending. There will need to be a withdrawal period. There will need to be a withdrawal period.”

Business Cycle / ISM

We previously noted that ISM data signaled the start of a new business cycle. We also recorded strong Capex purchases and small business confidence. We believe these figures are real, but also clearly show slowing growth. Last month’s data may have been distorted by manufacturers “pulling forward” orders ahead of expected tariffs. Since then, we’ve seen softening in services and new orders; February’s manufacturing PMI came in at 50.3, down from 50.9 in January.

Strategic Bitcoin Reserves

Until last Friday, even native crypto participants still held hope around discussions of strategic crypto/bitcoin reserves—despite repeated market indifference to such news over the past six weeks.

I think we can now agree: this was a classic “sell the news” event.

Flaws in “Cyclical Thinking”?

We should also acknowledge that the current “cycle” behaves differently from past ones. For example:

-

BTC hit an all-time high before the halving for the first time.

-

This cycle is shorter, with only a two-year bull run.

-

The “altseason” played out very differently—with Bitcoin dominance rising in steps since early 2023.

-

Bitcoin is now fully integrated into the financial system and supported by the U.S. government.

If “cyclical thinking” is flawed, perhaps we haven’t topped yet. Instead, we may just be pausing/consolidating before the next leg up—not entering a 12-month bear market with 75%-80% drawdowns like in prior cycles.

We believe cycles are evolving. Still, we expect a bear market could take 9 to 12 months to fully unfold.

Summary

To summarize our views:

-

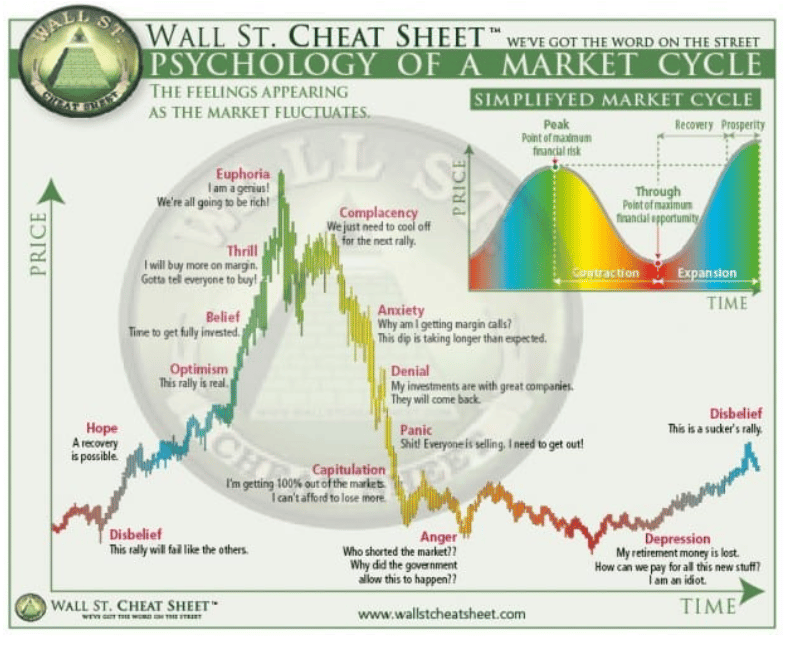

We believe we are currently in the “complacency” phase of the cycle shown above.

-

All previously identifiable bullish catalysts have already been priced in.

-

The economy may be heading toward recession. Trump administration statements are very clear—they’re telling us the economy needs a “withdrawal period.” We should believe them. This mirrors early 2022, when Powell warned of “pain” before hiking rates. Our current view: crypto is the canary in the coal mine. Traditional financial markets will slowly decline or chop sideways.

-

Given extreme bearish sentiment, we might see a short-term rally into the low $90K range for BTC. However, we believe this rally will face fierce selling pressure—likely killing any hope of restoring a bull structure.

-

As always, we remain open to being wrong. Our analysis is based on current information. We’ll update our views as new data emerges.

What would make us bullish again? We’ll watch for:

-

Reversal of fiscal tightening / DOGE (Department of Government Efficiency) efforts.

-

Significant Fed rate cuts / quantitative easing (QE).

-

Major global liquidity injections driven by the Fed (not just China).

-

Major correction or capitulation in the S&P 500 / Nasdaq.

A concern we have is that bearish views are becoming consensus. That gives us pause. But for now, we must stick with all other indicators—because signs suggest the cycle top is in, and a bear market is approaching.

Of course, in the long term, there are many compelling reasons to be bullish.

Crypto has truly entered its “inflection point.” Now is finally the time to rebuild the financial system atop public blockchains.

Not to mention, we love bear markets. When the tide goes out, the noise from past cycles becomes easier to filter, leaving only the real signals—preparing us for the next bull run.

This is when we do our best work, and when we create the most value for our readers.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News