Let's dive deep into Crypto Card—what exactly is the U Card that many projects have started working on?

TechFlow Selected TechFlow Selected

Let's dive deep into Crypto Card—what exactly is the U Card that many projects have started working on?

A good channel for withdrawals.

Author: Yue Xiaoyu

Many project teams have started launching Crypto Cards (U Cards), because Crypto Cards directly solve the biggest pain point in the crypto industry: cashing out—converting cryptocurrency back into fiat currency.

Since cashing out is highly susceptible to receiving illicit funds, this process often leads to frozen cards. Cashing out is more difficult and costly than depositing, with reliable and stable cash-out channels typically charging fees around 6%.

However, the emergence of Crypto Cards has directly addressed the issue of small-scale withdrawals for crypto users. These cards can be linked directly to third-party payment platforms (such as WeChat & Alipay) for daily spending, functioning in China like a regular foreign currency card.

We can now take a closer look at how U Cards actually work.

1. What exactly is a Crypto Card?

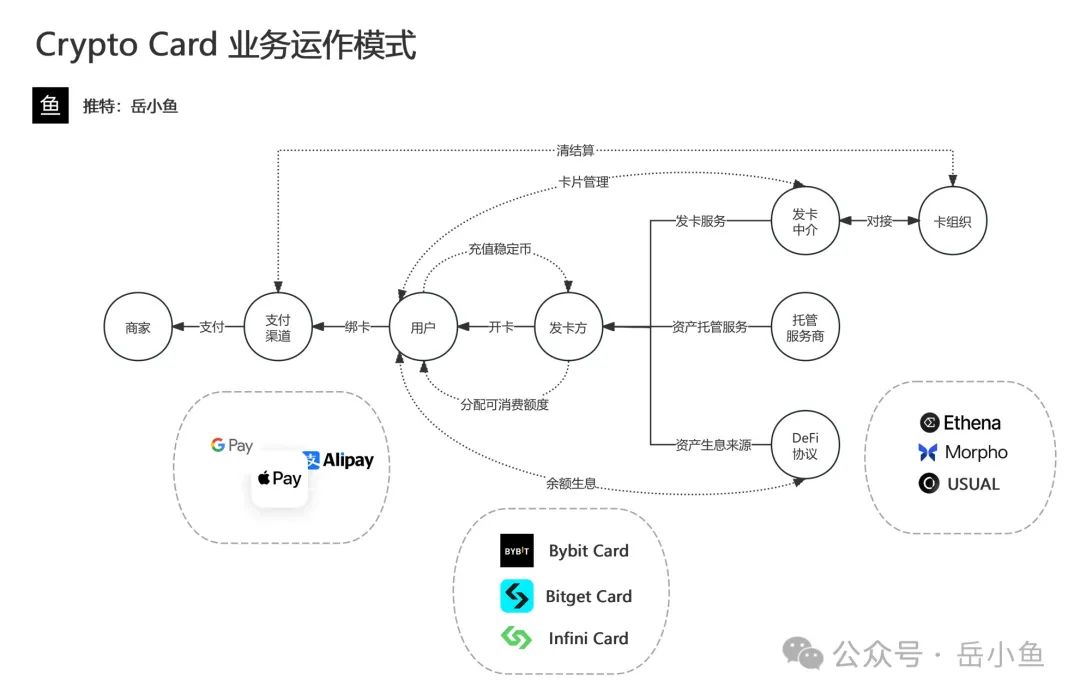

A Crypto Card is essentially a prepaid card. The issuer holds bank accounts with Visa/MasterCard. When users send stablecoins to the issuer, the issuer allocates spending limits to the user's card.

A U Card works similarly to a top-up card issued by a supermarket—usable only for payments, not for transfers—and does not actually hold any fiat balance.

The Crypto Card business operates under a centralized model: users send stablecoins to the platform, and the platform grants them card limits. When the amount of deposited funds becomes large enough, the platform has a strong incentive to abscond with the money.

Issuing cards is not particularly difficult; there are already many card-issuing intermediaries available today that enable "one-click card issuance."

The role of these intermediaries is to connect enterprises with card networks, handling all preparatory steps before card issuance so that project teams can issue cards seamlessly.

This is their key advantage: access to integration channels with card networks, which requires significant qualifications to establish.

Moreover, since issuing intermediaries control transaction data, they also manage all related risk controls, including handling frozen or suspended cards.

In fact, various Crypto Cards seen in the market are likely issued through the same card-issuing intermediaries. Their core focus lies in building brands and distribution channels, essentially converting traffic into revenue.

Revenue for issuers comes from two main sources: card issuance fees and currency conversion fees, along with income generated from capital operations.

Capital is divided into three parts: asset custody (liquid funds to meet user withdrawal demands), interest-generating assets (deployed in CeFi or DeFi to earn returns), and advance funding (sent to the issuing intermediary to secure actual fiat spending limits).

In summary, the Crypto Card market is highly homogenized. Behind the variety of cards we see may lie identical issuing intermediaries.

Therefore, choosing a Crypto Card issued by a major platform is crucial, as it significantly reduces the risk of exit scams.

2. Market Gap

The first widely popular U Card was OneKey Card.

OneKey’s primary business is hardware wallets; it later expanded into the Crypto Card space.

OneKey enjoyed a strong reputation in the industry, and its U Card offered excellent user experience, leading to rapid popularity. Almost every Chinese crypto user owned a U Card.

However, after operating the Card service for some time, OneKey first suspended KYC verification for mainland China users, effectively blocking new registrations from the region.

Later, it completely shut down its Card business—highlighting both immense compliance pressure and lackluster performance of the Card business itself.

Initially, the Card service attracted a large user base and boosted brand visibility, but eventually became a liability due to stagnating growth. The historical mission of OneKey Card had come to an end.

Still, cashing out remains the most critical and painful need in the crypto industry—otherwise, OneKey Card would never have gained such popularity.

The key issues preventing sustained operation of OneKey Card were compliance and operational costs. Projects with strong resources and backing are best suited for this business.

Project teams need substantial resources to support a Crypto Card operation.

Crypto Card is a low-margin business that requires high transaction volume and significant capital deposits to become profitable. However, as the scale grows, compliance and operational costs rise sharply. Therefore, overall, achieving scale is key.

For many Web3 companies, Crypto Card should not be the core business, but could serve as a side venture—ideally one that synergizes with their main offerings.

After OneKey Card ceased operations, a market gap emerged—one now being filled by projects such as Bitget Exchange and Infini Card.

Bitget, primarily an exchange, has strong financial backing, abundant resources, compliance capabilities, and user traffic, making it naturally suitable for launching a U Card service.

Infini Card takes a different approach by integrating DeFi features, offering users auto-compounding interest on balances, attracting many users with high annual yields.

These two projects represent typical examples in the U Card sector.

3. Business Matrix

For wallets, launching a Crypto Card service is a natural fit.

A wallet, where users store their assets, naturally leads to further needs: trading, wealth management, and depositing/withdrawing funds.

(1) Trading: Includes both on-chain trading and centralized exchange trading. While centralized exchanges still dominate, on-chain trading volumes are growing. Most wallets integrate DEXs, and trading fees are a core revenue stream.

(2) Wealth Management: Essentially involves packaging various DeFi and Staking products for users.

(3) Depositing/Withdrawing: Given the current friction in fiat-to-crypto conversion, cashing out is arguably the top immediate need in the crypto space, with naturally high profit margins.

This is usually done in partnership with OTC providers, requiring strict KYC. Crypto Cards serve as a good supplement, enabling indirect small-scale withdrawals.

Thus, for wallets, Crypto Card is a promising business direction with strong synergy.

This explains why many wallets have launched U Cards, including domestic ones like OneKey and Bitget Wallet, and international ones like MetaMask.

Wallets are critical infrastructure with high ceilings, serving as gateways to the Web3 world. With users and their assets already present, many additional services become possible.

4. Summary

U Cards operate under a centralized model: users send stablecoins to the platform, which then assigns spending limits. When accumulated funds grow large, the platform faces strong incentives to either run away with the funds or become a target for hackers.

Therefore, U Cards carry relatively high risks for users. It is advisable to keep only small amounts intended for daily spending.

Additionally, it's best to choose a Crypto Card issued by a major or well-backed platform, as this greatly reduces the risk of exit scams. In case of issues, such platforms are more likely to compensate users.

A typical example is the recent Infini Card hack, where nearly $50 million was stolen, yet the founder chose to personally reimburse users.

This highlights the importance of a project's credentials and background.

In short, Web3 is a dark forest. Only those who survive long enough can go far. Exercise caution with every move!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News