What are traditional big companies building on Ethereum?

TechFlow Selected TechFlow Selected

What are traditional big companies building on Ethereum?

NFTs and RWAs are the primary application scenarios for non-crypto-native companies and institutions building within the Ethereum ecosystem.

Author: Christine Kim, Vice President at Galaxy Research

Translation: Luffy, Foresight News

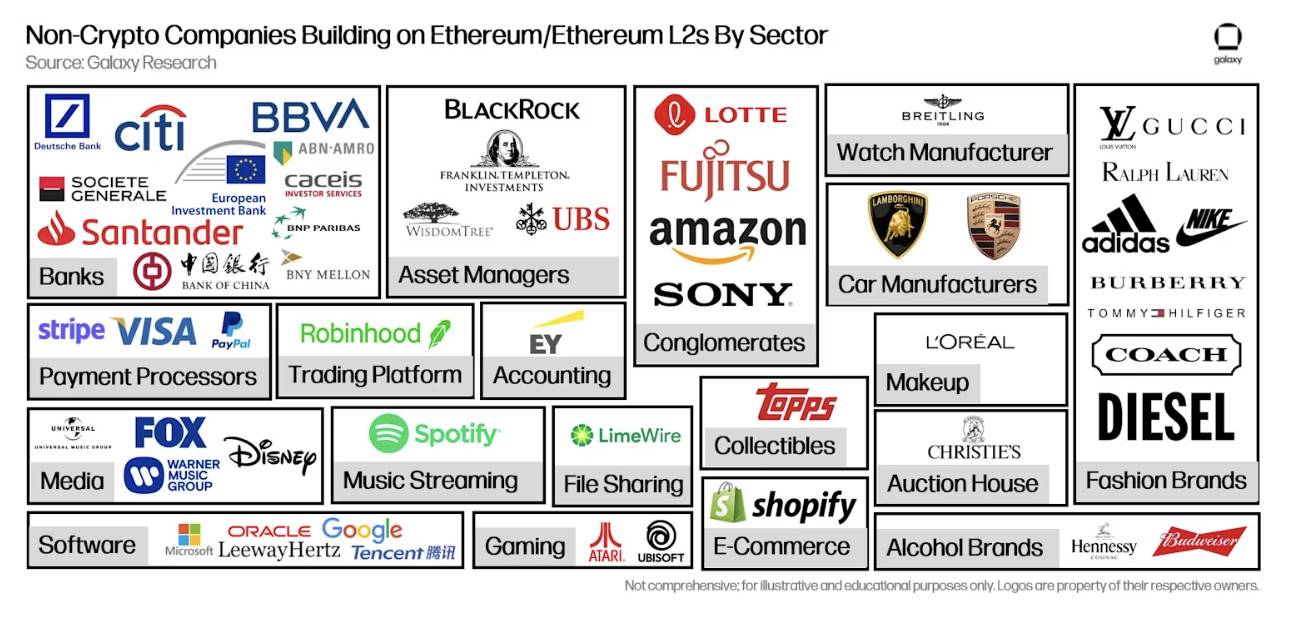

Over 50 non-crypto-native companies have already built products and services on Ethereum or Ethereum Layer-2 (L2) networks. From fashion giants like Louis Vuitton and Adidas to financial leaders such as Deutsche Bank and PayPal, these enterprises are reshaping the landscape of the crypto space. Notably, these traditional corporations' crypto initiatives are not focused on general market infrastructure like cryptocurrency trading, custody, auditing, and compliance, but rather on crypto-specific infrastructure and use cases—such as non-fungible tokens (NFTs), real-world assets (RWA), Web3 developer tools, and Layer-2 networks. Among the 20 financial institutions building crypto-specific infrastructure and applications, half are banks, most of which are actively issuing real-world assets on Ethereum. This report aims to deeply analyze the pioneering and leading use cases of Ethereum among traditional enterprises and institutions.

Introduction

In this report, the cryptocurrency industry can be broadly divided into three segments:

-

General Infrastructure: Companies offering products and services related to cryptocurrencies and blockchains that are not unique or exclusive to the crypto industry, such as general market infrastructure (e.g., exchanges, market makers, asset management) and general business support (e.g., banking, accounting, consulting, compliance).

-

Crypto-Specific Infrastructure: Companies providing products and services unique and specific to the crypto industry. For example, firms involved in mining, staking, and building on-chain oracles develop infrastructure tailored specifically for the cryptocurrency and blockchain domain.

-

Crypto Use Cases and Applications: Companies building consumer-facing applications that run fully or partially on blockchains. For instance, decentralized exchanges automatically execute cryptocurrency trades on-chain without relying on third-party intermediaries.

Today, traditional companies are no longer limited to expanding existing application suites to support crypto; they are actively innovating new products and services that can only be enabled by blockchain technology. Moreover, at least 55 of these companies are building on public blockchains such as Ethereum and Ethereum Layer-2 networks including Polygon, Arbitrum, and Base.

Below is a market map of 55 non-crypto-native companies that have built or are currently building crypto-specific infrastructure and applications on Ethereum or Ethereum Layer-2 networks.

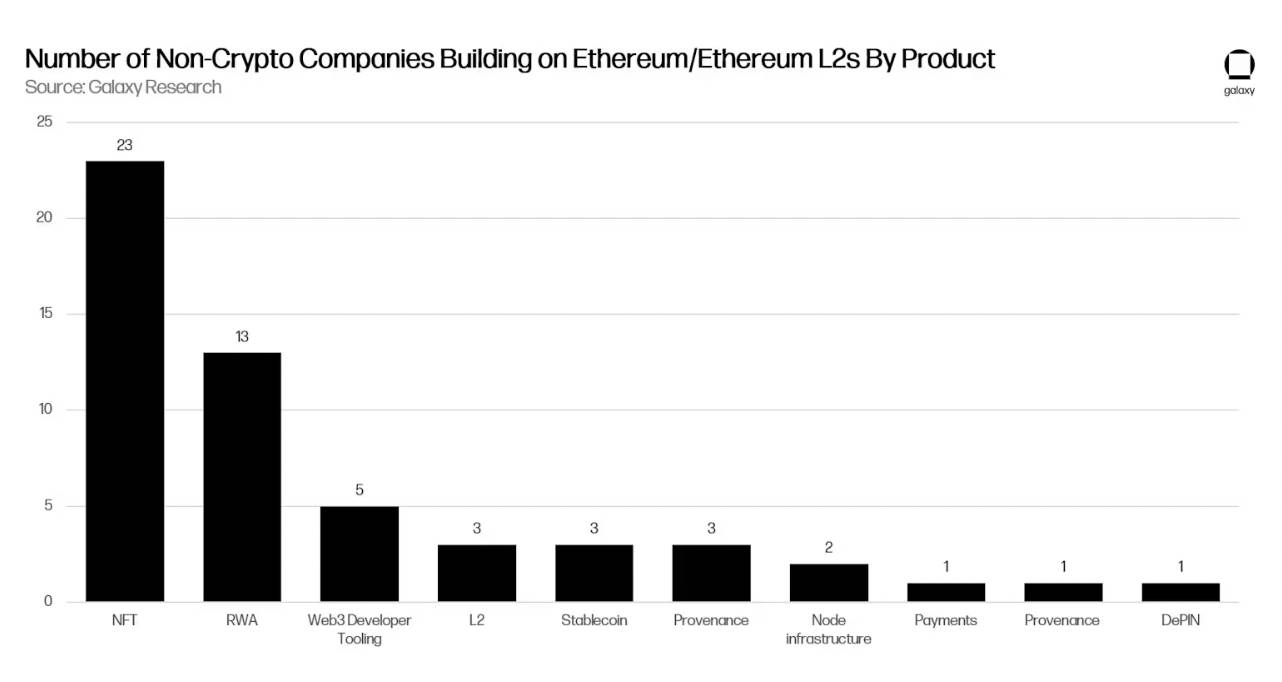

Among this list of 55 companies, at least 23 are issuing NFTs on Ethereum or Ethereum Layer-2 networks.

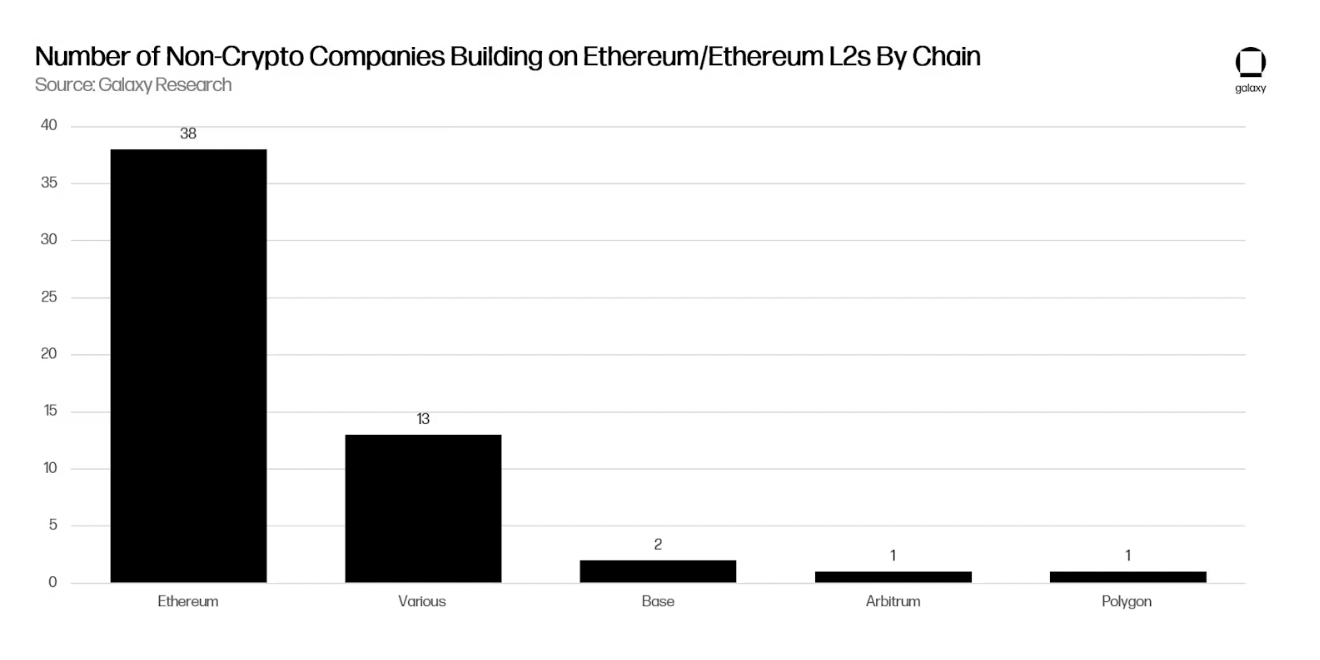

While most companies build directly on Ethereum, at least 17 have already or are exploring multiple general-purpose blockchains and L2s.

Real-World Assets (RWA) on Ethereum

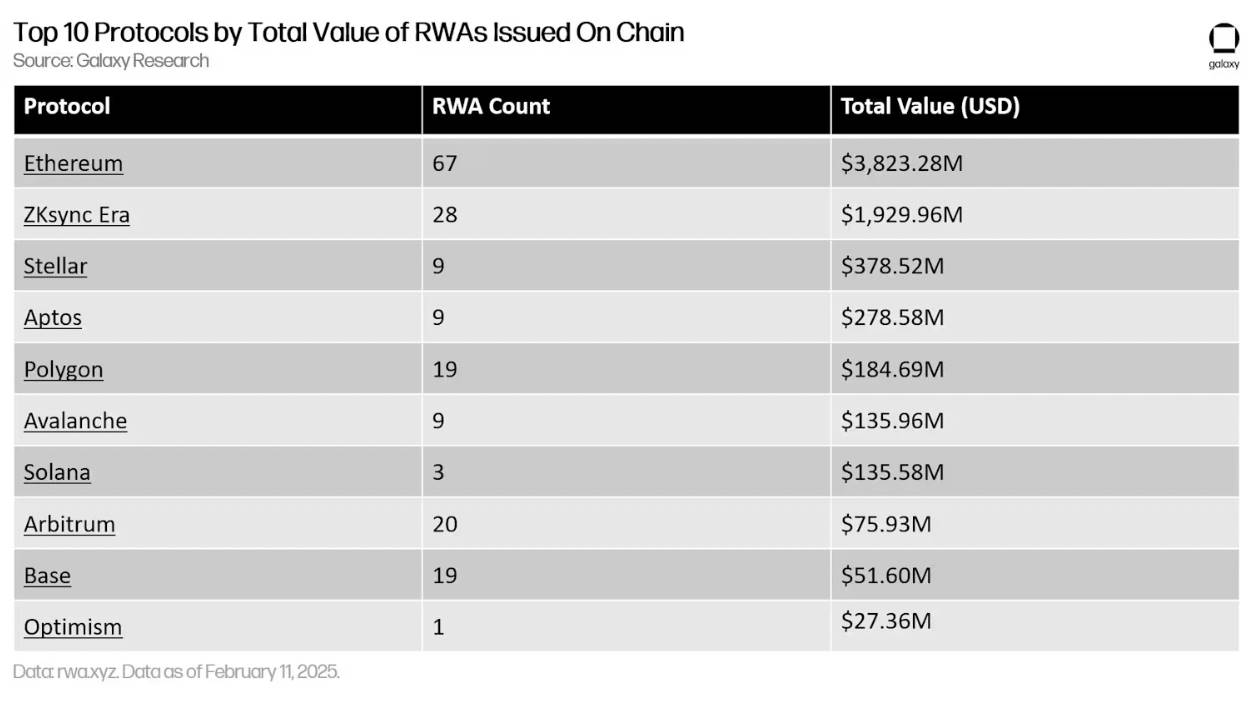

A common type of non-crypto company operating within the Ethereum ecosystem is financial institutions—banks, asset managers, payment processors, trading platforms, and accounting firms. Among the 20 financial institutions identified as building crypto-specific infrastructure and applications, 13 are issuing real-world assets on Ethereum and Ethereum L2s. The types of real-world assets issued on-chain vary widely, ranging from Franklin Templeton’s OnChain U.S. Government Money Fund to government bonds issued by entities like the European Investment Bank.

Ethereum is the preferred blockchain for tokenized assets, with the total value of its real-world assets nearly ten times that of Stellar, the second-most popular blockchain for RWAs. ZKsync, an Ethereum L2 network, has more real-world assets in terms of both number and total value than Stellar. Six of the top ten networks for issuing real-world assets are either Ethereum or Ethereum L2s.

As of February 11, 2025, the third-largest tokenized fund across all blockchains is BlackRock's USD Institutional Digital Liquidity Fund (BUIDL). Launched in March 2024, the fund offers investors U.S. dollar yields with benefits including instant and transparent settlement, and interoperability between traditional and decentralized financial markets. Robert Mitchnick, Head of Digital Assets at BlackRock, said last March: "With tokenization, we've packaged traditional finance investment exposure into a crypto-native wrapper."

BlackRock, the world’s largest asset manager, partnered with tokenization platform Securitize and U.S. financial services firm BNY Mellon to first launch BUIDL on Ethereum. Since March of last year, BlackRock has expanded the fund to five additional networks beyond Ethereum, three of which are Ethereum L2s.

The value of real-world assets issued on Ethereum has tripled over the past year. According to data from rwa.xyz, over 160 real-world assets have been issued on Ethereum, distributed across 60,000 active wallet addresses—excluding stablecoins.

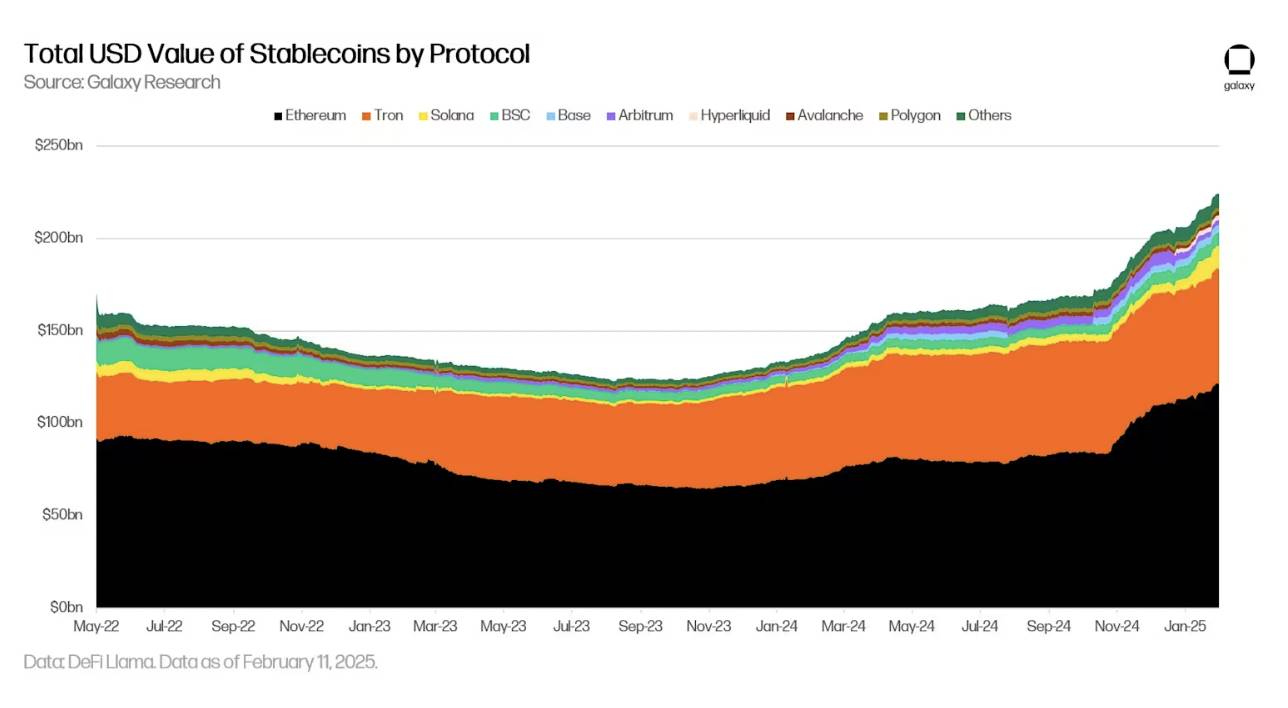

Although still limited in number, some financial institutions engaged in real-world asset and tokenization activities are also developing their own stablecoins. Payment processor PayPal first launched its U.S. dollar-pegged stablecoin PYUSD on Ethereum in August 2023. Since then, PayPal has extended PYUSD issuance to Solana. Trading platform Robinhood, in collaboration with a group of crypto-native institutions including Galaxy Digital, Kraken, Nuvei, Anchorage, Bullish, and Paxos, launched its own U.S. dollar-pegged stablecoin USDG on Ethereum in November 2024.

The total circulating supply of stablecoins on Ethereum has grown by 70% over the past year. These stablecoins differ in collateral composition and design, but the vast majority are U.S. dollar-pegged instruments backed by high-quality liquid assets. As of February 11, 2025, Ethereum accounts for over 50% of the total stablecoin market share.

According to Galaxy Research, the total supply of stablecoins is expected to double in 2025, surpassing $400 billion. A key catalyst driving traditional financial institutions to launch new stablecoins this year was Stripe’s $1 billion acquisition of stablecoin payments platform Bridge in 2024. Regarding the acquisition, Stripe CEO Patrick Collison said: "Stablecoins are the room-temperature superconductors of financial services. Thanks to stablecoins, global businesses will achieve significant improvements in speed, reach, and cost in the coming years."

In the United States, another catalyst for real-world asset and stablecoin adoption is the regulatory environment. SEC Commissioner Hester Peirce released a statement on Tuesday, February 4, 2025, outlining potential priorities and themes the SEC may address regarding the digital asset industry. Point nine emphasized modernizing traditional finance through tokenization. The statement read: "The task force also plans to explore intersections between crypto and clearing agencies and transfer agent rules. We will continue working with market participants interested in tokenizing securities or otherwise using blockchain technology to modernize traditional financial markets."

Real-world assets and stablecoins are crypto-native use cases rapidly achieving product-market fit within traditional financial institutions. As the most decentralized, widely adopted by crypto-native users, and longest-running general-purpose blockchain, Ethereum serves as the entry point for many institutions incubating and launching financial-focused crypto services and products.

Scalable Blockchain Infrastructure

Although Ethereum serves as the entry point for many financial institutions and non-crypto-native companies adopting blockchain technology, it is not a scalable protocol for new blockchain use cases. Compared to blockchains like Solana, Ethereum performs worse, with slower block times and higher transaction fees. Ethereum protocol developers are reluctant to sacrifice network resilience and security for speed, instead focusing on scaling Ethereum via Layer-2 solutions. Scaling solutions are blockchain infrastructures that inherit Ethereum’s security while enabling expansion to millions of new users.

Non-crypto-native companies are not only advancing crypto use cases like tokenization on Ethereum but are also investing in the underlying infrastructure needed to support these applications for broader audiences beyond crypto-native users. Germany’s largest bank, Deutsche Bank, is collaborating with Matter Labs—the team behind the ZKSync scaling solution—to develop a new scaling solution on Ethereum. Codenamed DAMA 2, this scaling solution is part of a broader initiative led by the Monetary Authority of Singapore (MAS) and 24 other global financial institutions to explore public blockchain applications in global finance.

Deutsche Bank’s primary motivation for developing an L2 network is to create blockchain infrastructure that is scalable, auditable, transparent, and interoperable with regulated platforms and financial services. Alex Gluchowski, co-creator of ZKSync, commented on Deutsche Bank’s motivations: "Institutions looking to build on-chain choose ZKSync because it allows them to build in Web3 without compromise. ZKSync provides institutions with customizable architecture to build tailored solutions with privacy, scalability, and interoperability with other private and public blockchains."

Financial institutions like Deutsche Bank are developing scalable, customizable, and regionally compliant blockchain infrastructure on Ethereum. However, the appeal of scalable and customizable blockchain infrastructure extends beyond financial use cases.

Japanese conglomerate Sony recently launched its own scaling solution using the OP stack on Ethereum. Their motivation for creating and operating a general-purpose scaling solution is to support a broader ecosystem of gaming, financial, and entertainment applications. Regarding Sony’s L2 network Soneium, Jun Watanabe, Chairman of Sony Blockchain Solutions Lab, said: "I believe developing comprehensive Web3 solutions based on blockchain is highly significant for the Sony Group. Sony conducts diverse business operations under the purpose of 'using creativity and technology to inspire emotions around the world.'"

Since Soneium’s launch, the protocol has faced strong backlash due to Sony’s control over on-chain activity, particularly restrictions on token transfers and address blacklisting. While this incident raised questions about how much control corporations should have when building scaling solutions atop permissionless infrastructures like Ethereum, it also highlighted one of the world’s largest corporate groups’ determination to explore answers to these issues. Sony’s investment in new digital experiences and applications via a scaling solution on Ethereum underscores the potential value of the Ethereum blockchain space and L2 networks.

Gaming on Ethereum L2 Networks

NFTs have been a major use case for traditional companies, involving luxury fashion brands like Louis Vuitton and Coach, as well as premium automakers like Porsche and Lamborghini. Most of these companies issued NFTs during the peak of the NFT boom between 2021 and 2023. Given the decline in NFT activity in recent years, many companies are no longer issuing NFTs on Ethereum or Ethereum L2 networks in 2025.

The few companies still actively issuing NFTs on Ethereum in 2025 are almost exclusively doing so in the context of game development, and almost entirely on Ethereum L2 networks rather than the Ethereum mainnet.

In July 2024, video game giant Atari deployed two of its classic arcade games, "Asteroids" and "Breakout," onto Base, an Ethereum L2 operated by Coinbase. By the end of August 2024, players could earn rewards on Base, mint exclusive Atari NFTs, and redeem physical merchandise. Several months after Atari entered on-chain gaming, in October 2024, Lamborghini announced a partnership with Web3 gaming company Animoca Brands to launch a digital collectibles platform called FastForWorld.

FastForWorld enables gamers to buy, sell, and drive Lamborghini vehicles across a suite of games developed by Animoca Brands, including "Torque Drift 2," "REVV Racing," "Motorverse Hub," and FastForWorld’s proprietary experience.

FastForWorld’s in-game assets are minted on Base. The platform’s first version launched on November 7, 2024, and remains under active development, with further expansions to the FastForWorld platform expected to be announced in 2025.

On January 7, 2025, Lotte Group—one of South Korea’s top five conglomerates—announced a deeper collaboration with the Arbitrum Foundation and Offchain Labs to build Lotte’s metaverse gaming platform "Caliverse" on the Ethereum L2 network Arbitrum. Caliverse is already live, allowing users to shop, attend virtual concerts, and play games. Kima Kim, CEO of Caliverse, said about the partnership with Arbitrum: "We are excited to partner with the most trusted blockchain, Arbitrum, as we take our first step into the blockchain world. Through Lotte Caliverse, we will leverage Lotte’s successful history in retail to deliver exceptional products and services to over 40 million people." During CES 2025 in Las Vegas, the Caliverse team announced plans to introduce virtual reality and 3D movie features on its platform in the first half of 2025.

The continued investment and development in NFTs by non-crypto-native companies like Atari, Lamborghini, and Lotte’s Caliverse is notable primarily because it occurs within the context of on-chain gaming applications. Blockchain-based games may require frequent on-chain transactions, potentially leading to high fees and network congestion. As a result, these companies build their games on Ethereum L2 networks to leverage the scalability advantages offered by Ethereum’s L2-centric architecture.

Steven Goldfeder, co-founder and CEO of Offchain Labs, said: "With Arbitrum’s industry-leading 250-millisecond block time, it can support seamless virtual worlds and gaming use cases, making it the ideal home for Caliverse."

Conclusion

NFTs and real-world assets are the primary use cases for Ethereum among non-crypto-native companies and institutions. Among companies issuing NFTs in the Ethereum ecosystem, the most active in 2025 are those issuing NFTs in the context of on-chain gaming applications built on Ethereum L2 networks. This highlights how L2 scalability helps support crypto-native use cases requiring frequent on-chain interactions, such as games developed by large retail brands and enterprises. Ethereum’s commitment to scaling its infrastructure through rollups also provides early tech adopters in traditional finance and other industries the opportunity to lead in non-speculative crypto applications by creating customizable and compliant infrastructure for these use cases. Finally, Ethereum remains the preferred blockchain for traditional financial firms issuing real-world assets and stablecoins. Key partnerships formed in 2024 are expected to drive new progress in stablecoin adoption throughout 2025.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News