The opening act of the "Trump Rally" is officially over: How the market prices in a "debt crisis" as term premium rises

TechFlow Selected TechFlow Selected

The opening act of the "Trump Rally" is officially over: How the market prices in a "debt crisis" as term premium rises

Currently, many high-growth risk assets, including the crypto market, will continue to face downward price pressure in the short term.

Author: @Web3_Mario

Summary: The cryptocurrency market experienced significant volatility this week, with price movements forming an "M top" pattern. This indicates that as Trump's January 20 inauguration draws closer, capital markets have quietly begun pricing in the opportunities and risks associated with his presidency. Thus, the three-month-long, sentiment-driven "Trump rally" has officially come to an end. What we now need is to distill the core focus of short-term market speculation from the overwhelming noise, enabling more rational judgments about market trends. In this article, I will share my analytical framework from the perspective of a non-finance professional enthusiast, hoping it may provide some value. Overall, I believe that many high-growth risk assets—including crypto—will continue facing downward price pressure in the near term. The key reason lies in rising medium-to-long-term U.S. Treasury yields driven by expanding term premiums, which negatively impacts these assets. This phenomenon stems from the market pricing in concerns over a potential U.S. debt crisis.

Macroeconomic indicators remain strong; inflation expectations have not significantly increased, thus having limited impact on current price trends

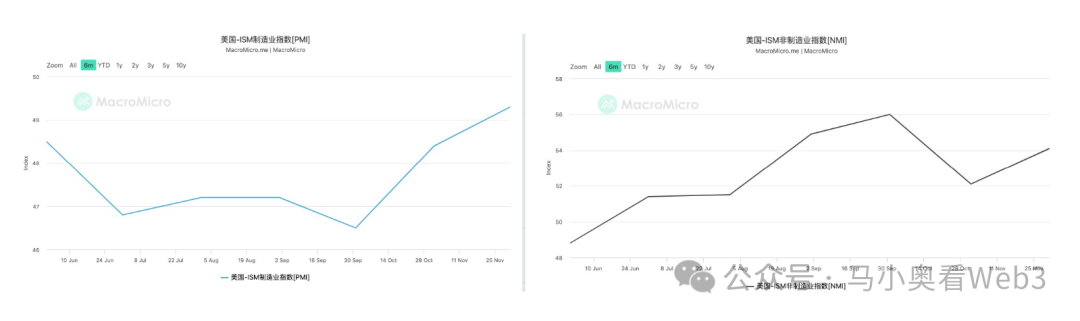

First, let’s examine the factors behind recent price weakness. Last week saw the release of several important macroeconomic data points. Let's analyze them one by one, starting with U.S. economic growth metrics. Both the ISM Manufacturing and Non-Manufacturing Purchasing Managers’ Index (PMI) continued to rise. Since PMIs are typically leading indicators of economic growth, this suggests a relatively positive short-term outlook for the U.S. economy.

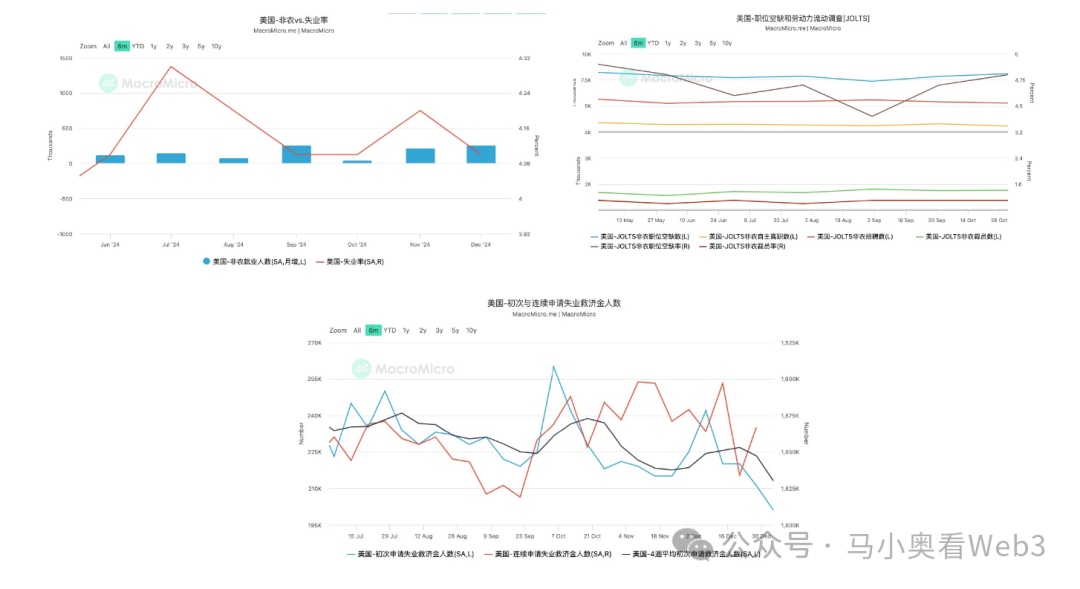

Next, we turn to the labor market. We’ll review four key indicators: nonfarm payrolls, job openings (JOLTS), unemployment rate, and initial jobless claims. Nonfarm payrolls rose from 212,000 last month to 256,000—well above expectations—while the unemployment rate declined from 4.2% to 4.1%. Meanwhile, JOLTS job openings surged significantly to 809,000. Furthermore, initial jobless claims continue to trend downward, indicating optimism regarding January’s labor market performance. Together, these figures confirm that the U.S. labor market remains robust, making a soft landing increasingly certain.

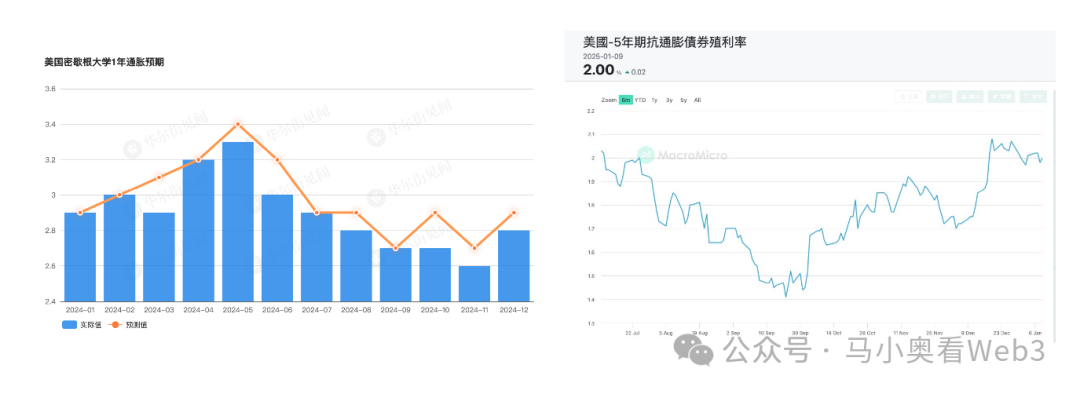

Finally, let’s assess inflation. Since the December CPI will be released next week, we use the University of Michigan’s one-year inflation expectation as a forward-looking gauge. Compared to November, this metric edged up slightly to 2.8%, below expectations. However, this level still falls within the 2–3% range deemed acceptable by Powell. That said, future developments warrant close attention. Nevertheless, judging from changes in TIPS (Treasury Inflation-Protected Securities) yields—an indicator of inflation hedging demand—the market does not appear to be panicking about rising inflation.

In summary, from a macroeconomic standpoint, there are currently no evident signs of economic distress in the U.S. Therefore, we must now identify the root cause behind the recent decline in valuations of high-growth companies.

Rising medium-to-long-term U.S. Treasury yields amid a bearish steepening yield curve, with widening term premiums reflecting market pricing of a U.S. debt crisis

Let’s revisit the movement in U.S. Treasury yields. The yield curve shows that over the past week, long-end rates have continued climbing—particularly the 10-year Treasury yield, which jumped nearly 20 basis points. This further intensifies the bear steepening dynamic in the U.S. bond market. We know that rising long-term Treasury yields exert greater downward pressure on high-growth equities than on blue-chip or value stocks. The core reasons are:

1. Impact on high-growth enterprises (typically tech firms or emerging industries):

Higher financing costs: High-growth companies rely heavily on external funding (equity or debt) to support expansion. Rising long-term interest rates increase borrowing costs, while higher discount rates make equity financing harder due to reduced present value of future cash flows.

Valuation pressure: Growth company valuations depend heavily on projected future cash flows (FCF). Higher long-term rates mean higher discount rates, reducing the present value of those future cash flows and thereby lowering enterprise valuations.

Shift in investor preference: Investors may rotate out of higher-risk growth stocks into safer, dividend-paying value stocks, putting downward pressure on growth stock prices.

Constrained capital expenditures: Elevated financing costs may force companies to cut back on R&D and expansion plans, impairing long-term growth potential.

2. Impact on stable enterprises (consumer staples, utilities, healthcare, etc.):

Milder effects: These firms generally enjoy strong profitability and stable cash flows, with lower reliance on external financing, so they’re less affected operationally by rising rates.

Increased debt servicing costs: If leverage is high, rising rates could raise financial expenses. However, such firms usually possess stronger debt management capabilities.

Reduced dividend appeal: As Treasury yields rise, fixed-income instruments become more attractive relative to dividend yields, potentially pressuring stable stock valuations.

Inflation pass-through capacity: If rising rates accompany inflation, cost pressures may emerge. Yet stable firms often have stronger pricing power to offset input cost increases.

Therefore, it’s clear that rising long-end Treasury yields significantly weigh on the market caps of crypto and other tech-related assets. The key question now becomes: against a backdrop of anticipated rate cuts, what is driving the increase in long-term Treasury yields?

To understand this, recall the nominal Treasury yield formula:

I = r + π + RP

Where I is the nominal Treasury yield, r is the real interest rate, π represents inflation expectations, and RP denotes the term premium. Let’s clarify each component: the real interest rate reflects the true return on bonds, independent of risk preferences or compensation, directly representing time value and economic growth potential. π refers to average societal inflation expectations, commonly gauged via CPI or TIPS yields. RP, or term premium, reflects investors’ required compensation for interest rate risk—when uncertainty about future economic conditions rises, investors demand higher compensation.

In our earlier analysis, we established that the U.S. economy remains fundamentally sound in the short term, and TIPS yields suggest no notable surge in inflation expectations. Hence, neither real rates nor inflation expectations are the primary drivers of the recent rise in nominal yields. The culprit, therefore, must lie in the **term premium**.

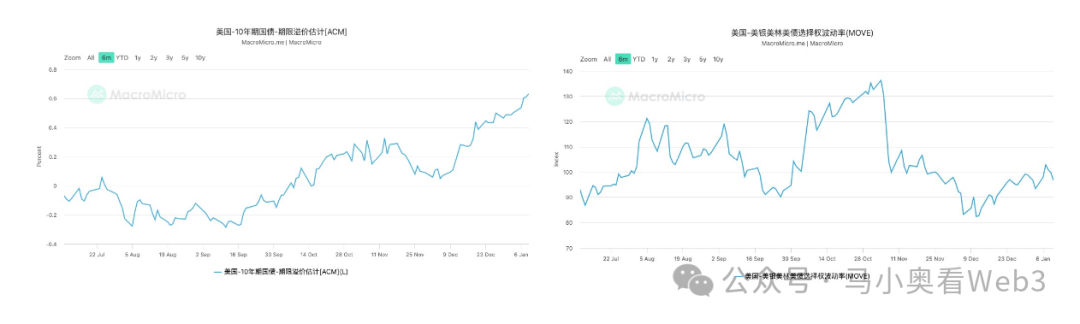

To track term premium shifts, we examine two indicators. First is the ACM model estimate of U.S. Treasury term premium levels. As shown, the 10-year Treasury term premium has risen sharply in recent months, clearly serving as the dominant factor behind increasing Treasury yields. Second is the Merrill Lynch Option Volatility Estimate (MOVE) index, which measures implied volatility in the U.S. Treasuries options market. Recently, MOVE has remained relatively stable. Typically, MOVE is more sensitive to short-end rate volatility due to its weighting structure. This stability implies that markets are not currently pricing in significant uncertainty around short-term rate fluctuations—short-term rates being primarily controlled by the Fed. Therefore, fears related to potential changes in the Fed’s 2025 policy trajectory are not the direct driver. Instead, the sustained rise in term premiums signals growing market concern over medium- to long-term U.S. economic prospects. Given current economic discourse, this concern centers squarely on worries about America’s fiscal deficit.

Thus, it is clear that markets are now pricing in risks surrounding a potential U.S. debt crisis under a Trump administration. In the coming weeks, when evaluating political developments and stakeholder statements, we should assess whether they alleviate or exacerbate fiscal risks—this will better inform our understanding of risk asset market direction. For example, last week Trump mentioned considering declaring a national economic emergency. Under such a declaration, the International Emergency Economic Powers Act (IEEPA) could be invoked to unilaterally impose new tariff policies, significantly reducing constraints and opposition to tariff adjustments. While this reignites concerns over renewed trade tensions, the direct fiscal impact—increased tariff revenue—is actually positive for government finances. Therefore, I believe the overall effect would not be severe. By contrast, progress on his proposed tax cuts and plans for reducing government spending will be the true focal points of the fiscal debate. I will continue monitoring these closely.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News