Trump’s Son’s “Money Printer” Backfires: Mining Firm ABTC Collapses 92%, Retail Investors Lose $50 Million, While He Personally Profits $9 Million

TechFlow Selected TechFlow Selected

Trump’s Son’s “Money Printer” Backfires: Mining Firm ABTC Collapses 92%, Retail Investors Lose $50 Million, While He Personally Profits $9 Million

Insiders get filled; retail investors foot the bill.

Author: TechFlow

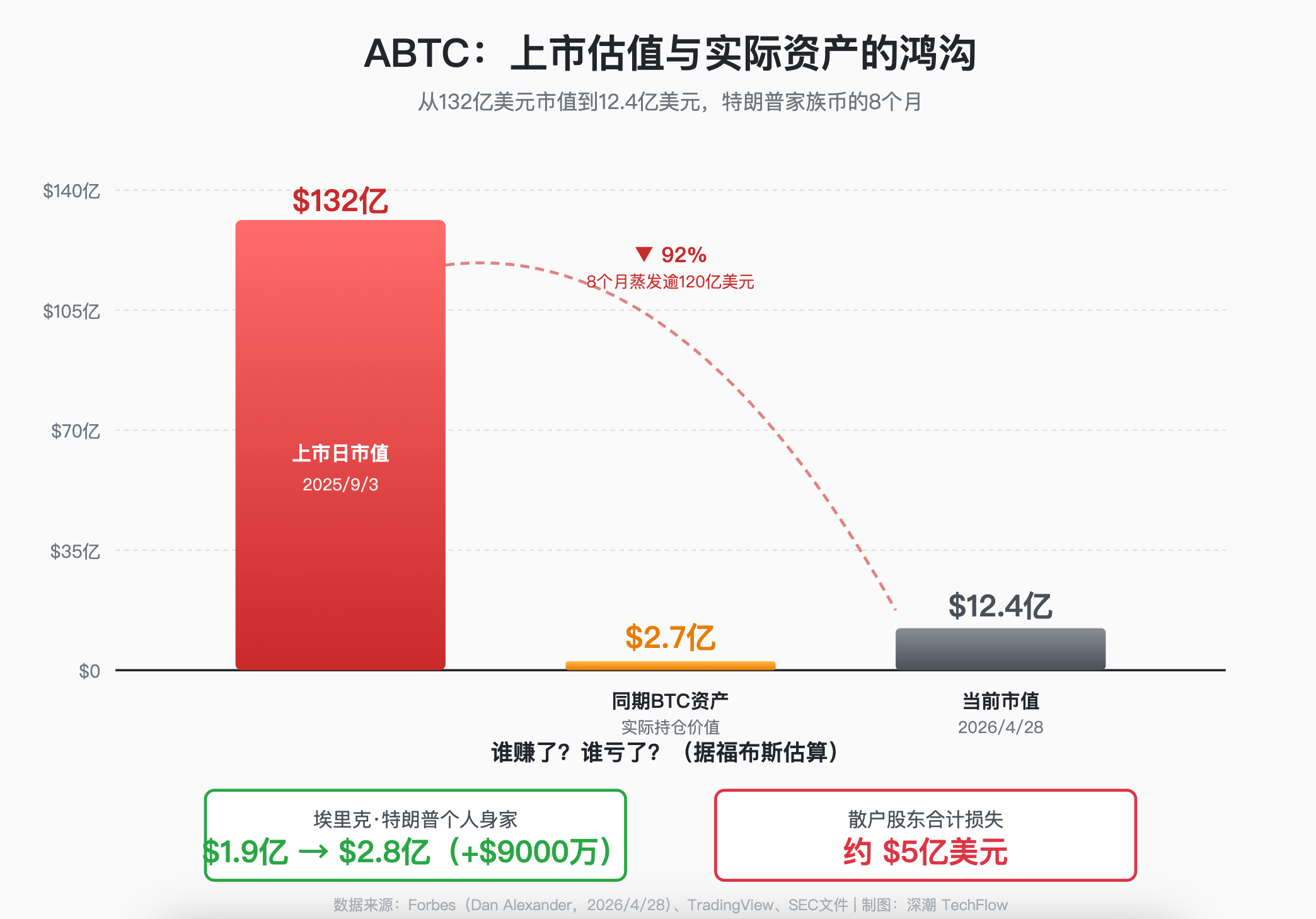

TechFlow Introduction: On April 28, Forbes published an investigative report accusing American Bitcoin (Nasdaq: ABTC), a bitcoin mining company co-founded by Eric Trump and Donald Trump Jr., of being, in essence, an “arbitrage machine.” Since its listing in September 2025, ABTC’s market capitalization has plummeted from $13.2 billion to approximately $1.24 billion, resulting in roughly $500 million in aggregate losses for retail shareholders—while Eric Trump’s personal net worth surged from $190 million to $280 million.

Forbes also revealed that roughly 70% of ABTC’s bitcoin holdings were not mined internally but instead purchased on the open market through continuous stock issuances, at an all-in cost approaching $90,000 per BTC—far exceeding the company’s claimed $57,000 per BTC. Eric Trump promptly labeled the report “Chinese propaganda” on X.

The “American Bitcoin” story crafted by the Trump family is unraveling—in an awkward fashion.

On April 28, Forbes magazine published an investigative report by veteran journalist Dan Alexander, characterizing American Bitcoin (Nasdaq: ABTC), the bitcoin mining firm co-founded by Eric Trump and Donald Trump Jr., as an “arbitrage machine” designed specifically to extract value from MAGA-aligned retail investors. The official Forbes account posted on X: “The president’s second son markets his bitcoin company as a money-printing machine. In reality, it’s an arbitrage tool feeding off MAGA investors.”

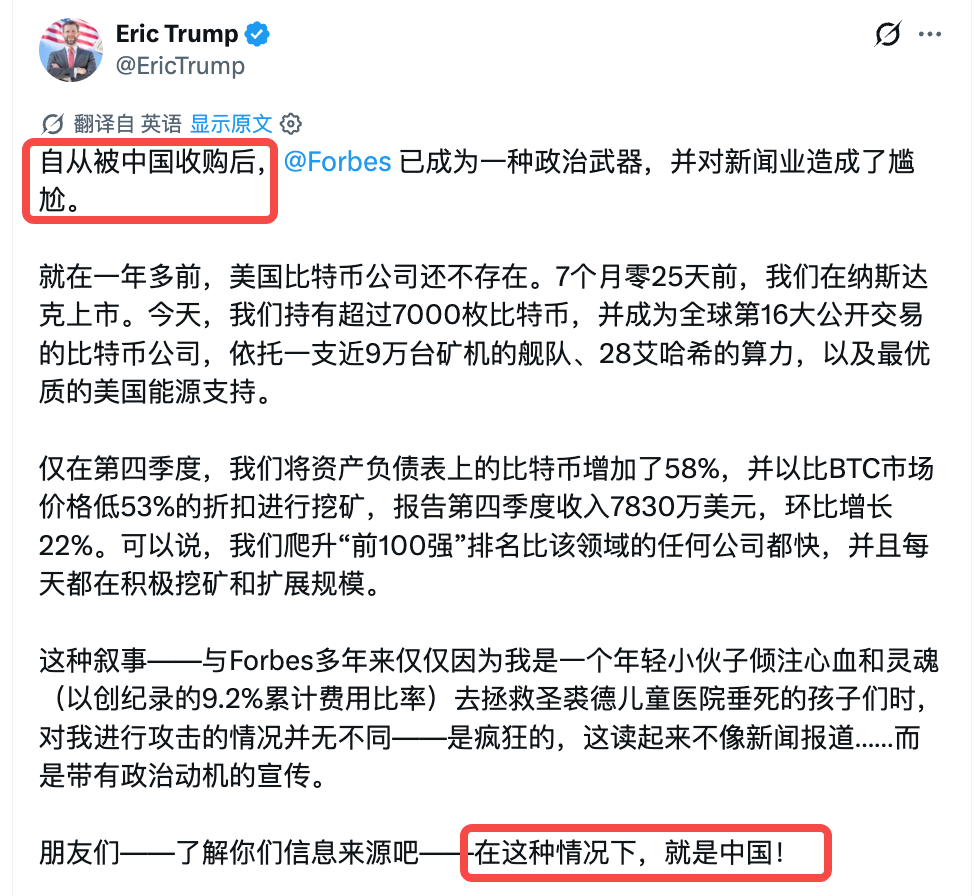

Eric Trump swiftly fired back. On X, he declared, “Forbes has become a political weapon—a disgrace to journalism,” calling the article “political-motivated propaganda,” and concluded by urging readers to “recognize the true nature of your information sources—this time, it’s China!” Multiple crypto media outlets observed that his response consisted entirely of reciting ABTC’s operational hard metrics—over 7,000 BTC in reserves, 28 EH/s of hash rate, nearly 90,000 miners, and $78.3 million in Q4 revenue—but conspicuously avoided directly addressing Forbes’ central allegation regarding retail investor losses.

Peak at Listing: $270 Million in Bitcoin Assets Supporting a $13.2 Billion Valuation

To understand Forbes’ allegations, begin with ABTC’s listing baseline.

ABTC went public on Nasdaq on September 3, 2025, via a reverse merger with listed mining firm Gryphon Digital Mining. On its first trading day, the market assigned it a staggering $13.2 billion valuation—yet the company held only about $270 million worth of bitcoin on its balance sheet. This implied investors were willing to pay nearly 50 times the value of the company’s core assets for a firm barely six months old.

The stock peaked at $14.52 that day. Eight months later, ABTC’s share price had collapsed to approximately $1.16—a 92% decline. At its current price, the company’s market cap stands at roughly $1.24 billion, representing over $12 billion in value erosion since its listing peak. Forbes estimates retail shareholders collectively lost around $500 million.

This collapse was not merely a byproduct of broader industry turbulence. Peers such as CleanSpark, IREN, and Cipher Mining also reported severe losses during the same period (CleanSpark posted a $378.7 million net loss in Q4, with some miners forced offline due to unprofitability), yet most saw share price declines within the 40–70% range—far less severe than ABTC’s 92%. ABTC’s distinctiveness lies in its inherently inflated valuation premium upon entering the secondary market—a premium widely perceived as the “Trump brand tax.” When retail investors began voting with their feet, what fell wasn’t just the mining business—it was the brand narrative itself.

The Forbes Ledger: 70% of ABTC’s Bitcoin Wasn’t Mined—It Was Bought with Newly Issued Shares

Eric Trump’s core narrative is that ABTC functions as a “money-printing machine,” capable of mining bitcoin at costs far below market price. During a February earnings call, he even stated: “We’re rapidly becoming a leader in the Bitcoin world—I truly believe we have the best brand of anyone.”

Yet Forbes’ review of the company’s SEC filings paints a radically different picture: roughly 70% of ABTC’s bitcoin reserves were not mined—but acquired on the open market via newly issued shares.

The specific sequence is as follows: Within the first 27 days post-listing, ABTC issued 11 million new shares, raising $90 million; after deducting ~$2 million in costs, it purchased approximately 725 BTC. From early October to mid-November 2025, it issued another 7 million shares, raising $44 million. At the end of November, it conducted a single issuance of 47 million shares, raising ~$106 million. Between January 1 and March 25, 2026, it issued 84 million more shares, raising $111 million and purchasing roughly 1,430 BTC.

In total, Forbes estimates ABTC raised approximately $525 million via share issuances to buy bitcoin—assets now valued at roughly $390 million at current prices, reflecting an unrealized loss of ~$135 million. While diluting existing shareholders, the company simultaneously bought bitcoin on the open market at elevated prices—even as bitcoin’s price dropped from its October 2025 high of $126,000 to near $70,000 today.

As for the portion actually mined, Forbes calculates ABTC’s all-in cost per BTC—including equipment depreciation and management expenses—at nearly $90,000. By contrast, Eric Trump repeatedly cites a figure of $57,000 in public statements. The discrepancy stems largely from whether depreciation and management expenses are included. Against the backdrop of bitcoin’s current ~$70,000 price, this difference determines whether ABTC is a “money-printing machine” or a “loss-making mine.”

Insiders Feast, Retail Pays: Eric’s Net Worth Grows by $90 Million

ABTC was never a typical mining company from day one.

The firm was jointly established in March 2025 by Hut 8 (a Canadian-listed mining company) and the Trump family: Hut 8 spun off the vast majority of its bitcoin mining operations into the new entity in exchange for an 80% equity stake; the Trump brothers and early investors received the remaining 20%. In other words, the Trump family contributed virtually no capital toward building facilities, purchasing miners, or assembling teams—their primary contributions were the “American Bitcoin” brand name and the attendant market attention.

This light-asset structure is also evident in public filings. Forbes cites an SEC document noting that, one month after ABTC’s February 2026 earnings call, the company officially employed only two full-time staff—most likely CEO Mike Ho and President Matt Prusak. Notably, Mike Ho also serves as Chief Strategy Officer at Hut 8. Day-to-day facility operations, miner management, and HR/finance functions are fully outsourced to Hut 8.

According to Forbes’ calculations, since ABTC’s launch, Eric Trump’s personal net worth has increased from ~$190 million to ~$280 million—a gain of approximately $90 million. Other insiders also reaped substantial gains during this period. In stark contrast stand retail shareholders, who collectively absorbed roughly $500 million in unrealized losses.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News