New highs in spot seat auction prices—could Hyperliquid become the new choice for token listings?

TechFlow Selected TechFlow Selected

New highs in spot seat auction prices—could Hyperliquid become the new choice for token listings?

Many projects have already turned their listing ambitions toward Hyperliquid.

By Nancy, PANews

Listing fees have long been a focal point of market controversy, with exorbitant costs often seen as a major barrier to innovation. As a result, an increasing number of emerging projects are choosing DEXs (decentralized exchanges) as their launchpad—yet this shift also brings significantly higher Rug risks.

Recently, derivative DEX Hyperliquid has not only delivered a textbook-perfect airdrop but also achieved impressive performance across multiple metrics, while setting new highs in spot listing auction prices—further strengthening its market position. Amid these strong results, PANews has learned that numerous projects are now turning their attention toward listing on Hyperliquid.

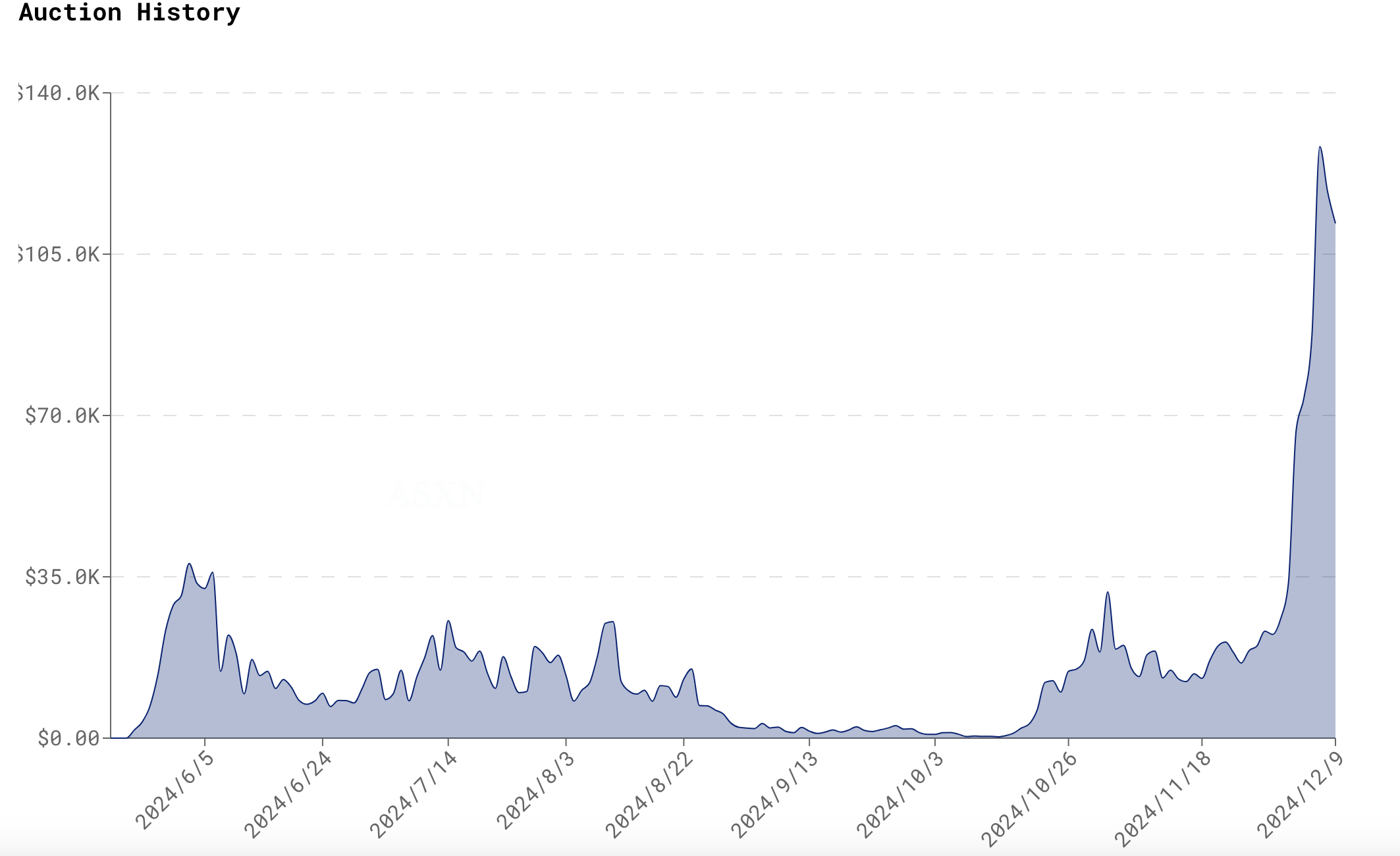

Auction Prices Surge Post-Airdrop; Spot Liquidity Concentrated in HYPE

On December 6, a token ticket named "SOLV" set a new auction record on Hyperliquid at approximately $128,000, drawing significant investor attention and speculated to be linked to Solv Protocol, which recently announced plans for an upcoming TGE (Token Generation Event).

According to official documentation, for a project to be listed on Hyperliquid, it must obtain HIP-1 native token deployment rights. HIP-1 is the protocol’s standard for native tokens in spot trading, enabling on-chain order books similar to ERC20 on Ethereum. To gain permission for issuing a new token, projects typically need to participate in Dutch auctions held every 31 hours—meaning a maximum of 282 tokens can be deployed annually.

This auction fee can be viewed as a deployment gas cost, currently paid in USDC. During each 31-hour auction period, the gas price starts high and gradually decreases, with a floor of $10,000 USDC. If the previous auction was completed, the starting price for the next one is double the final gas price from the prior round; otherwise, it resets to $10,000. This mechanism helps prevent excessive speculation and irrational price surges while dynamically adjusting the pace of new token listings based on demand. It ensures that only high-quality projects are prioritized and limits the total number of tokens available on Hyperliquid.

Historical auction data shows that since May, Hyperliquid has conducted over 150 auctions, according to ASXN. Prior to the airdrop in December, most auction prices remained below $25,000, with many successful bids coming from meme coins such as PEPE, TRUMP, FUN, LADY, and WAGMI. However, auction prices surged this month: besides SOLV, SHEEP sold for about $112,000, BUBZ for $118,000, and GENES for $87,000. This indicates a clear increase in market demand and interest following the airdrop hype.

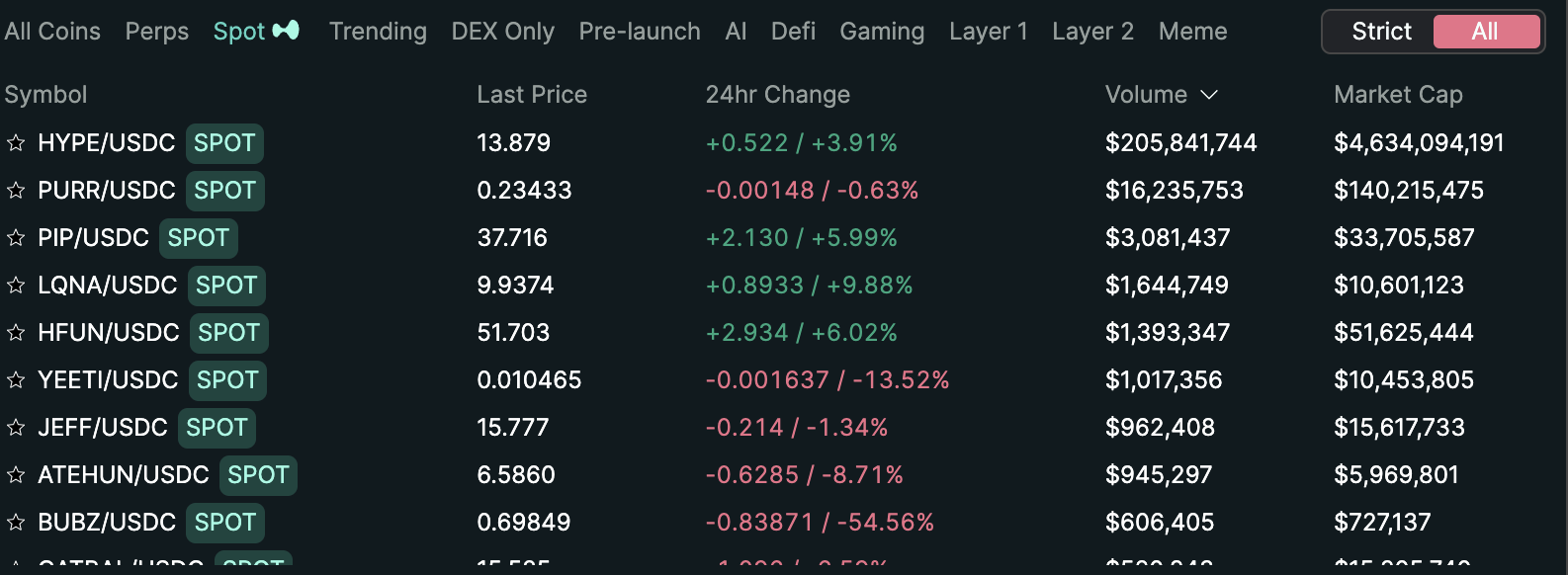

Despite hundreds of HIP-1 tokens being listed, liquidity remains highly concentrated among a few top assets. Data from Hyperliquid shows that as of December 10, over 100 HIP-1 tokens were live on the platform, with total 24-hour trading volume reaching around $240 million. Notably, Hyperliquid's own token HYPE accounted for 85.9% of all spot trading volume, followed by its flagship meme coin PURR at over 6.7%. All other projects combined represent just 7.4% of liquidity. This concentration reflects Hyperliquid’s primary focus on derivatives trading, with its spot market gaining traction more recently alongside the rise of meme coins.

"Compared to CEXs, there are very few tradable spot assets on Hyperliquid right now. If a major project wins a spot listing through auction, it would be a powerful combination. On-chain exchanges welcome more high-quality projects launching via auction—the existing USDC liquidity could then concentrate more effectively on newly listed assets," analyzed blockchain researcher @defioasis from Wu Shuo Blockchain.

Strong Post-Airdrop Metrics—Could Hyperliquid Become a Top Contender for Listings?

With strong market performance and an innovative listing strategy, Hyperliquid may emerge as a key contender among platforms vying for new project listings.

On one hand, Hyperliquid’s wealth-generating airdrop and sustained token momentum have served as powerful marketing tools, boosting both visibility and key performance indicators.

In terms of token performance, unlike many projects whose tokens drop sharply after a high initial airdrop price, Hyperliquid’s token HYPE has seen its FDV (Fully Diluted Valuation) climb steadily. CoinGecko data shows HYPE’s circulating market cap briefly touched $4.96 billion and has since slightly pulled back, while its current FDV stands at $13.21 billion, peaking at $14.85 billion.

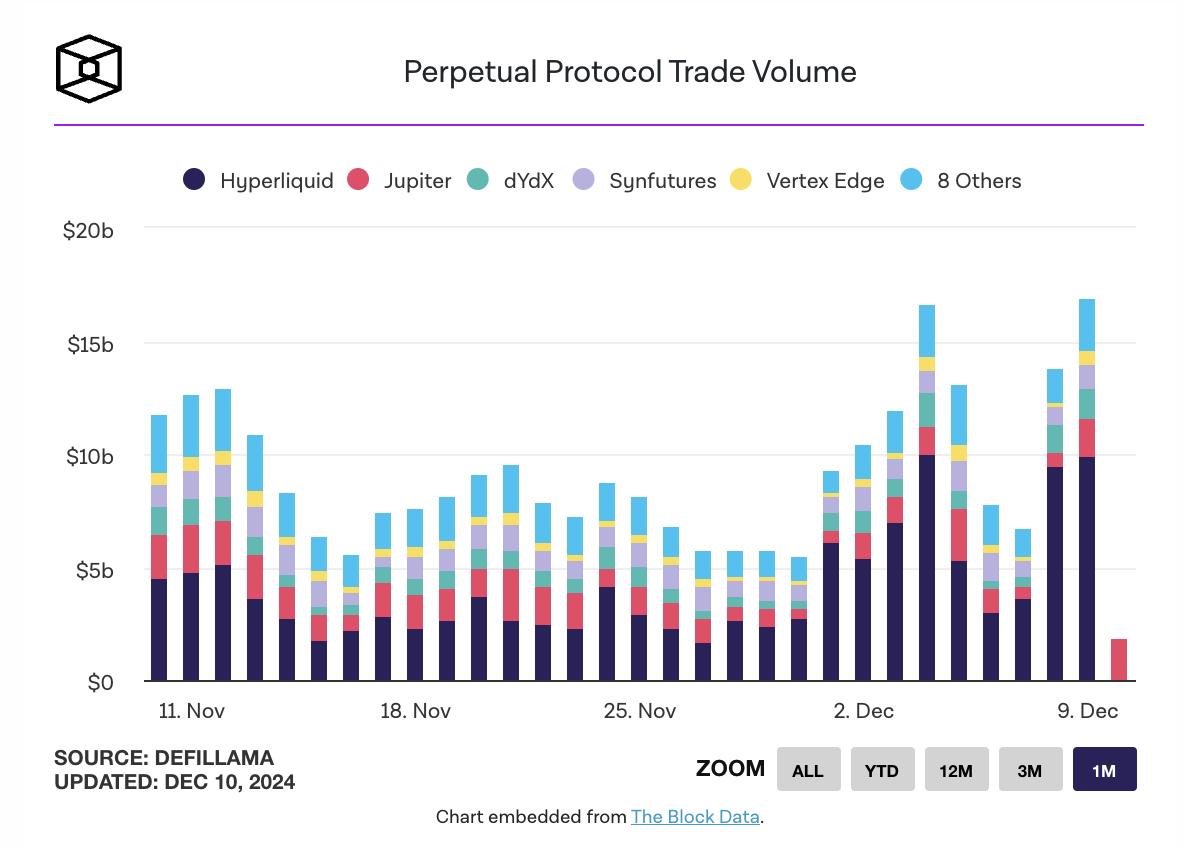

Hyperliquid also holds a dominant position in the derivatives DEX space. According to The Block’s data for December 9, Hyperliquid recorded $9.89 billion in daily trading volume, capturing 58.4% of the entire sector’s volume (~$16.92 billion).

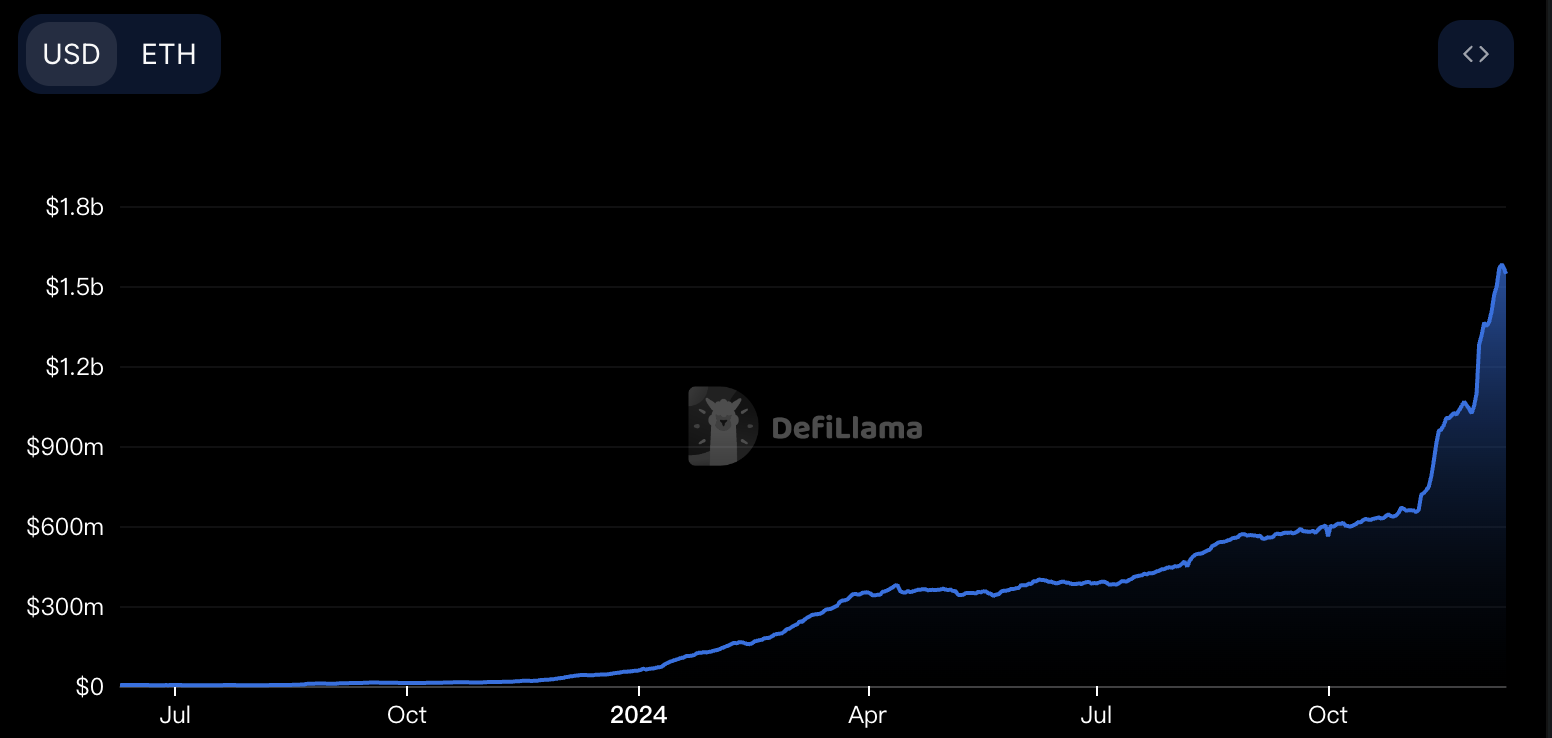

Additionally, Hyperliquid has accumulated substantial asset deposits. DeFiLlama数据显示,截至12月10日,Hyperliquid Bridge的TVL达到15.4亿美元。在平台拥有如此庞大的 asset pool 的情况下, adding more high-quality projects could unlock further trading potential.

Moreover, Hyperliquid demonstrates exceptional revenue-generating capability. As analyzed by @stevenyuntcap from Yunt Capital, the platform earns income from immediate listing auction fees, profits and losses from HLP market makers, and platform fees. While the first two sources are publicly visible, the team recently clarified details about the third. Based on this, estimated year-to-date revenue reaches $44 million. When HYPE launched, the team used an Assistance Fund wallet to buy back HYPE in the open market; assuming no multiple USDC AF wallets exist, the USDC AF wallet has generated a year-to-date P&L of $52 million. Adding the HLP’s $44 million and USDC AF’s $52 million yields a total year-to-date revenue of approximately $96 million—surpassing Lido and ranking Hyperliquid as the 9th most profitable crypto project of 2024.

These figures highlight Hyperliquid’s growing appeal and competitiveness in the market.

On the other hand, Hyperliquid offers greater transparency and fairness in its listing mechanism. Listing fees have long sparked debate, especially after recent controversies involving Binance and Coinbase, where differing views emerged over whether such fees are justified.

Critics argue that soaring listing fees impose heavy financial burdens on early-stage projects, forcing them to sacrifice long-term development and ultimately harming ecosystem health. Arthur Hayes once revealed that top-tier CEXs like Binance may charge up to 8% of a project’s total token supply as a listing fee, while most others charge between $250,000 and $500,000 in stablecoins. He acknowledged that charging listing fees isn’t inherently wrong—exchanges invest heavily in user acquisition and need to recoup costs. However, allocating tokens to exchanges instead of users harms future project potential and negatively impacts token prices.

Proponents counter that listing fees are essential for exchange operations and serve as an effective tool for filtering project quality. By requiring payment, exchanges ensure sustainable operations and confirm that listed projects possess sufficient economic strength and market validation, reducing low-quality listings and promoting healthy market order.

In response, IOSG partner Jocy suggested several improvements: exchanges should enhance transparency, strictly penalize problematic projects, enforce departmental separation to avoid conflicts of interest, and conduct rigorous due diligence with diverse decision-making processes to reject any form of project fraud.

Beyond exchanges, projects themselves should not rely solely on CEX listings but instead focus on user engagement and organic market recognition. For example, Binance founder CZ recently stated, “We should work to reduce these ‘quote attacks’ in the industry. Bitcoin never paid any listing fees. Focus on building great projects, not on getting listed.” Arthur Hayes added that the biggest issue in current token issuance is excessively high initial prices, making successful launches nearly impossible regardless of which CEX gets first listing rights. Meanwhile, for projects obsessed with CEX listings, selling tokens to exchanges offers only one-time gains, whereas fostering user participation creates a lasting flywheel effect. Crypto researcher 0xLoki also emphasized: “Quality speaks for itself—truly strong projects will get listed anywhere. If a project requires extremely unfavorable terms to get listed, it should question its own fundamentals: Is the project really good enough? What is the real goal of listing? And who ultimately bears the cost?”

At its core, the debate over listing fees centers on transparency, fairness, and a project’s long-term viability. Compared to the opaque processes and high costs associated with CEX listings, Hyperliquid’s auction-based model reduces listing expenses and enhances market fairness, ensuring higher-value, more promising assets on its platform. Furthermore, by recycling listing fees back into the community, Hyperliquid incentivizes broader user participation in trading.

In summary, in today’s market environment, balancing listing costs with sustainable project growth has become a critical challenge the industry must urgently address.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News