Interview with Fundstrat’s Head of Research: Bitcoin’s $115,000 target remains unchanged after accurately predicting the crash; Hyperliquid targets $100

TechFlow Selected TechFlow Selected

Interview with Fundstrat’s Head of Research: Bitcoin’s $115,000 target remains unchanged after accurately predicting the crash; Hyperliquid targets $100

“I’m waiting for a ‘surrender-style liquidation.’ If the price breaks above the key moving average again and CME open interest increases, I’ll be more confident about scaling up my position.”

Compiled & Translated by TechFlow

Guest: Sean Farrell, Head of Crypto Research at Fundstrat

Host: Zack Guzman

Podcast Source: Coinage

Original Title: Why The Analyst Who Called Crypto's Crash Is Still Cautious

Air Date: March 18, 2026

Key Takeaways

Although many investors believe Bitcoin and other cryptocurrencies have already hit bottom, market turbulence—and ongoing uncertainty surrounding the Iran conflict—has led some analysts to remain skeptical of this optimism.

Sean Farrell, a Fundstrat analyst who accurately predicted February’s market crash, shared his views on Bitcoin and crypto-market risks in an interview with Coinage. He delved into Bitcoin’s potential future trajectory, factors that could impact risk assets, and why his cautious stance toward the crypto market remains unchanged. He also analyzed Hyperliquid’s cross-asset growth potential, calling it one of the most compelling protocols in crypto today.

Highlights of Key Insights

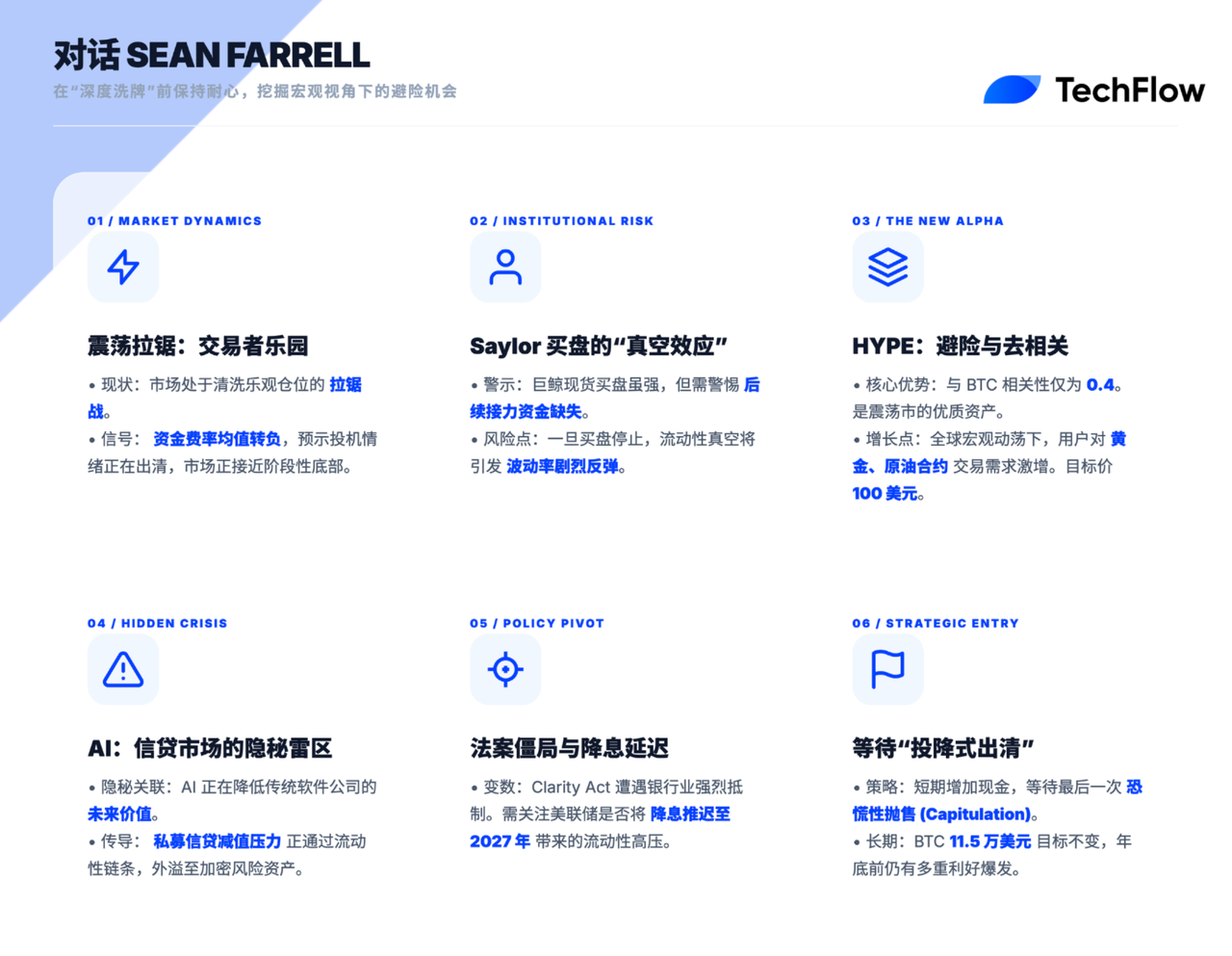

Market Timing & Positioning: A “Tug-of-War” for Traders

- At the start of the year, markets exhibited extreme positioning—low volatility but unusually active trading in risk assets. Coupled with miners selling Bitcoin indiscriminately, I concluded there was little attractive risk-reward in the first half of the year.

- Markets are not currently in a clear trend-driven regime—they remain a classic trader’s market. Holding some dry powder during rallies is a more prudent strategy.

- The 30-day moving average of funding rates has turned negative—a typical signal that markets may be approaching a more stable bottom. However, I expect a difficult adjustment phase before a meaningful turnaround later this year.

Institutional Dynamics: The “Secondary Buying” Vacuum Behind Saylor’s Purchases

- While large institutional buying injects liquidity, the concern lies in what happens when spot demand dries up—markets may lack sufficient secondary buying to absorb supply, increasing near-term volatility risk.

- Many alternative asset managers’ stock prices have already been hammered. If credit spreads begin rising broadly, the impact on risk assets like crypto will be delayed—but devastating.

Top Alpha Opportunity: Hyperliquid (HYPE) as a Paradigm Shift

- Hyperliquid is our portfolio’s most compelling opportunity. In the first 15 days of March alone, its HIP-3 market traded $28 billion—driven by global macro turbulence and surging user demand for gold and oil perpetuals.

- HYPE’s 90-day correlation with Bitcoin is only ~0.4 (vs. ~1 for most crypto assets), making it a valuable diversifier within crypto portfolios.

- Our price target for HYPE is ~$100—still substantial upside from current levels (~$40).

Macro Risk Deep Dive: Private Credit & AI’s Negative Feedback Loop

- My biggest concern is mounting stress in private credit markets. Many funds face forced redemptions and valuation markdowns. Credit spreads are widening—if we wait until they surge fully before acting, it’ll be too late.

- A significant portion of private credit exposure targets software companies. Rapid AI advancement may erode their terminal value—and thus credit quality—creating spillover pressure on crypto markets.

Regulation & the Fed: Uncertain Catalysts

- Strong opposition from banking lobby groups—and persistent controversy over stablecoin yield—have dimmed prospects for the Clarity Act. This battle is proving far more protracted than expected.

- Investors should closely monitor whether the Fed pushes rate-cut expectations into 2027. If so, it would amplify the current war-risk premium and weigh on asset prices.

- I’m waiting for a “capitulation-style washout.” If price breaks above key moving averages *and* CME open interest rises, I’ll gain greater conviction to scale in.

Long-Term Vision: Target Price Unchanged

- Despite short-term caution, I have no plans to revise my year-end $115,000 Bitcoin target—the favorable catalysts may converge in H2.

Sean Farrell on “Calling the Crypto Crash”

Zack Guzman: Welcome back to a new episode of Coinage. We’re thrilled to welcome Sean Farrell, Head of Digital Asset Strategy at Fundstrat.

You joined us earlier this year and correctly called the market downturn. Now, after a rebound, Bitcoin remains volatile. I noticed you recently issued another cautionary report—especially regarding certain crypto sectors. Could you share your view on current market volatility and how it impacts crypto?

Sean Farrell:

Let me first revisit early-year conditions—I held an extremely cautious stance. Markets showed extreme positioning: low volatility but unusually active risk-asset trading, alongside ambiguous liquidity. Many investment products traded near—or even below—their net asset value (NAV). Bitcoin miners, pressured by market conditions, sold indiscriminately—further accelerating the downtrend. Taken together, these signals suggested little attractive risk-reward in crypto during the first half of the year—and heightened volatility ahead. That assessment proved accurate.

We saw a pullback on February 5. But I viewed that decline less as a long-term buy signal and more as a short-term trading opportunity. While markets rebounded afterward, crypto’s spillover effects and volatility remain critical concerns.

Recently, however, some positive signals have emerged. Fear sentiment has eased somewhat, while equity and bond market volatility have risen—indicating investors are reassessing risk. In crypto, we’ve seen signs of emotional cleansing—for example, the 30-day moving average of funding rates has turned negative. Historically, this often suggests markets are nearing a more stable bottom. Additionally, MicroStrategy recently resumed large-scale Bitcoin purchases, injecting liquidity.

Nonetheless, I remain cautious on overall market positioning. Current conditions still carry high uncertainty—especially given historically low cash allocations in January and February. Equity indices and broader markets still price in excessive optimism, suggesting markets haven’t yet undergone a full capitulation.

That said, I remain bullish on Bitcoin’s long-term outlook. I believe a clear upward inflection point may arrive before year-end—but crypto likely faces a challenging adjustment phase first.

Investors must closely monitor global macro conditions—especially Fed policy, geopolitical risk, and emerging stress in private credit markets. These factors affect traditional finance directly—and spill over meaningfully into crypto. Still, I believe Bitcoin’s fundamentals remain robust, and its long-term value appreciation potential endures.

Will these risks inevitably materialize? Not necessarily—but they persist, amplified by latent uncertainties. Geopolitical risk remains a key concern. Oil prices hover near $100/barrel, while credit markets show early signs of deterioration. Though not all driven solely by geopolitics, these are undeniable headwinds.

Additionally, the Fed meets tomorrow. Market pricing has nearly erased 2026 rate cuts from the yield curve. While I believe Fed policy shifts could benefit markets in H2, internal divisions and policy ambiguity make it difficult to foresee near-term dovish action supporting markets.

MicroStrategy’s Persistent Buying, Bitcoin Flows & Market Risk

Zack Guzman: You warned of sharp volatility early this year—and were proven right, as Bitcoin plunged rapidly to ~$60,000 and lingered there. Remarkably, you flagged this *before* the Iran conflict escalated. That prompts a question: Should similar geopolitical events be systematically integrated into market-risk frameworks?

Also, per CoinShares data, digital-asset investment products have seen inflows for three consecutive weeks. You cited Michael Saylor and MicroStrategy’s aggressive buying. Had markets moved differently, Saylor’s activity might not have drawn such attention. But combined, these developments reveal noteworthy trends. Could this create a “crowding-out effect,” dampening enthusiasm among other market participants?

TechFlow Note: Crowding-Out Effect is an economics and finance term describing how excessive concentration of capital or resources in one area squeezes out participation or investment elsewhere. In crypto, it typically refers to large investors (“whales”) buying heavily into an asset (e.g., Bitcoin), lifting prices and drawing attention—potentially diverting capital and enthusiasm away from other assets.

Sean Farrell:

I’m not sure I’d label it fully as a “crowding-out effect,” but it certainly qualifies as part of market risk. We’ve seen this repeatedly before: crypto briefly outperforms equities—and that outperformance is frequently driven by large institutional players or whales like MicroStrategy.

The issue arises once those spot purchases cease. Overall market support may then appear insufficient. If demand for MicroStrategy’s common stock weakens in any given week, the withdrawal of such large-scale buying could leave markets without adequate “secondary buying” to absorb supply—likely triggering further volatility and elevating near-term risk.

Why Crypto Remains a Trader’s Playground

Zack Guzman: You noted early this year that many fund managers held almost no cash. Does today’s risk-reward landscape imply limited available buying power—and that if investors need to sell, Bitcoin and other cryptos could bear the brunt? What worries you most right now?

Sean Farrell:

I agree—and I do lean more tactical than some peers. Our current view is that markets are close to a bottom, but still some distance from a top. My role is helping investors manage risk—and outperform Bitcoin across the cycle. Frankly, markets aren’t in a clear trend-driven regime—we’re squarely in a trader’s market.

For investors seeking advantage, forming clear—but flexible—tactical views in the near term is essential. Recall early February’s drop—yet markets have since rallied significantly: Bitcoin is up ~20–25%, and alts even more.

Given this risk calculus, holding some dry powder during rallies is likely the wiser choice.

Sean Farrell’s Continued Bullishness on Hyperliquid

Zack Guzman: Arthur Hayes set a >$100 price target for HYPE. When analyzing real-world drivers behind HYPE’s performance—like heavy gold, silver, and oil perpetual trading on Hyperliquid—do you share Hayes’ optimism? If so, what’s your HYPE target? Also, you’ve discussed DATs (Digital Asset Treasuries)—what’s your view on HYPE’s longer-term trajectory?

Sean Farrell:

Last year, we set a $100 target for HYPE—still considerable upside from current levels (~$40.55 at recording).

Fundamentally, Hyperliquid is one of the most compelling opportunities in our portfolio. This includes both the HYPE token and Hyperliquid Strategies—the digital asset treasury firm—which has performed exceptionally well.

Hyperliquid recently launched its HIP-3 market: a permissionless market where anyone can create their own venue. These venues trade primarily perpetual futures tied to commodities and equities.

I shared a chart showing HIP-3 volume reached $28 billion in the first 15 days of March—driven by cross-asset price swings and global macro turbulence. We’ve observed heavy weekend oil-perpetual trading—and previously, precious metals were hotspots.

This activity boosts Hyperliquid’s revenue—and critically, much of that revenue stems from *external* assets outside the crypto ecosystem. That’s why HYPE’s correlation with Bitcoin has dropped sharply. Traditionally, crypto assets correlate near 1. Yet this year (through last week), HYPE’s 90-day correlation with Bitcoin stands at ~0.4—making it a vital diversifier in crypto portfolios.

HYPE’s recent price surge has been impressive—perhaps requiring short-term consolidation. But long term, I remain highly confident in the Hyperliquid protocol.

Crypto Regulation, the Clarity Act & Market Structure

Zack Guzman: Beyond passage of the Clarity Act, what else would clear current fear? Or what final catalyst would shift you—as Tom and other crypto bulls have—to re-embrace crypto’s resurgence?

Sean Farrell:

Let me start with regulation. Early this year, I was relatively optimistic about the Clarity Act’s prospects—believing it could pass. That optimism rested on two factors: first, this is a midterm election year, and Republicans hold a tenuous majority in Congress; second, organizations like Fairshake recently raised nearly $200 million in a “war chest” to support legislative efforts—so the risk-reward balance initially favored passage.

But over time, things grew more complex. From industry sources, I learned banking lobbyists are strongly opposing the bill—and controversy around stablecoin yield has dragged on far longer than expected. This “battle” is proving far more protracted than many anticipated. Meanwhile, Congress faces numerous higher-priority items—further clouding the Clarity Act’s path.

Still, I believe markets underestimate one fact: the SEC and CFTC will advance rulemaking regardless. So I expect some positive structural changes in H2—though I still hope the Clarity Act ultimately passes as a major milestone.

Regarding your question about “realigning” or changing my view—I’d require broad risk-market capitulation to boost confidence in buying at lower levels.

Another scenario: geopolitical risk premiums recede, rate expectations stabilize, and credit markets normalize. And crucially, if markets enter a clear trend regime—with unambiguous directional momentum—I’ll be more willing to act.

Specifically, if price breaks above key moving averages, institutional flows resume, CME open interest rises, and basis widens—I’ll gain stronger conviction to scale in.

Private Credit Stress & Broader Market Risk

Zack Guzman: How much of your market view hinges on macroeconomic risk? Zooming out, what’s your read on broader market risk—especially credit-market stress? Yet professional experience tells me true market drawdowns often stem from *unanticipated* risks—not widely debated ones. Could private credit stress add extra pressure on crypto?

Sean Farrell:

I believe it will exert some influence—and people sometimes forget quickly. Everyone’s focused on geopolitical events like the Iran conflict and commodity-price impacts, which matter. But even before those events unfolded, we saw serious issues across broader markets—and deteriorating private credit was a primary driver.

Recently, many private-credit funds faced forced redemptions and marked down valuations. I don’t claim full visibility into the overall credit quality of these assets—given wide variation—but repeated negative headlines warrant vigilance.

Market-wise, many alternative asset managers’ stocks have been severely punished. Simultaneously, credit spreads—an indicator of corporate borrowing costs—are widening, aligning with those stock declines. Though absolute spread levels remain low, the *pace* of widening is concerning. If we wait until spreads surge fully before acting, it’ll be too late.

This situation may indeed impact markets—but I don’t see it escalating to systemic risk. Some issues tie to AI-affected tech firms. For instance, many private-credit exposures target software companies—whose market share may fragment amid rapid AI adoption. Further, AI could depress their terminal value—eroding valuations.

So yes—this is a key focus area. I’m still working through how and when it might erupt—but it’s unquestionably worth watching.

Why His Bitcoin Target Remains Unchanged

Zack Guzman: Each time you join us, we discuss your long-term price forecasts. I recall your $115,000 Bitcoin target at year-start. Looking back at those January projections—do you feel compelled to adjust them? Or as we approach end-2026, will you reassess?

Sean Farrell:

It’s only mid-March—adjusting long-term forecasts now would be premature. I still believe we’ll benefit from favorable catalysts we highlighted earlier—and those may crystallize in H2. So I have no plans to revise my year-end target.

My priority remains managing near-term volatility—and scaling in decisively once markets show clearer trend directionality.

Fed Meeting: What Crypto Investors Should Watch

Zack Guzman: What will you watch most closely at Wednesday’s Fed meeting? How will you interpret the statement—and what should crypto investors prioritize?

I recall your recent report noting markets seem to be pre-pricing some “dovish” expectations—that Chair Powell might signal easing. But as you noted, it’s a tug-of-war: soft labor data fuels concerns—especially AI-driven job displacement—while inflation risks appear resurgent.

Sean Farrell:

I agree. Most expect Powell to strike a relatively “neutral” tone—he lacks strong justification to turn overtly hawkish.

Investors should zero in on the Fed’s dot plot and Summary of Economic Projections (SEP). These tools reveal the Fed’s latest forecasts for inflation, growth, unemployment—and potentially, clues about its rate-cut path.

If the dot plot pushes rate-cut expectations into 2027, it could negatively impact asset prices. Such a shift could refocus market attention on other risks—and possibly amplify existing war-risk premiums. Of course, final market reactions depend on the specifics released.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News