Polymarket and Kalshi Challenge Hyperliquid: What Are Their Chances?

TechFlow Selected TechFlow Selected

Polymarket and Kalshi Challenge Hyperliquid: What Are Their Chances?

Entering the prediction market with perpetual contracts is significantly more difficult than perpetual contract platforms entering the prediction market.

By Prathik Desai

Translated by Luffy, Foresight News

Perpetual futures have already emerged as an indispensable force in the industry. They enable participants to price and trade ahead of events, offering advantages such as high leverage, 24/7 availability, and deep liquidity—features traditional exchanges cannot match due to their fixed trading hours.

A team of just 11 people seized upon the pain point of 24/7 trading to build Hyperliquid—the fastest-growing cryptocurrency exchange, generating nearly $1 billion in annualized revenue.

In 2025, daily perpetual futures trading volume reached seven times that of spot trading—a clear signal that this is a mature, sustainable business line. Industry-wide entry has thus become inevitable.

Just last week, Polymarket and Kalshi—the two largest prediction market platforms globally—announced, within hours of each other, the launch of perpetual futures and cryptocurrency trading. Just months earlier, Hyperliquid had announced its own event contracts.

The convergence of perpetual futures and prediction markets is now an irreversible trend. Platforms across the board aim to become full-service, all-in-one exchanges—aggregating traffic, capital, and leveraged trading demand under one roof.

Saurabh recently stated on X that Hyperliquid’s foray into prediction markets could help it dominate the entire financial trading landscape. But does the reverse logic hold? Can Polymarket and Kalshi replicate similar success by entering perpetual futures?

Why Are Perpetual Futures Important for Prediction Markets?

Prediction markets suffer from low user retention and highly cyclical activity: trading volume spikes only around major events—such as U.S. elections, the Super Bowl, or Federal Reserve rate decisions.

During the 2024 U.S. election, Polymarket’s monthly active users (MAUs) peaked at 321,500; just three weeks later, MAUs plunged 25%, falling to 245,000.

MAUs fluctuate wildly due to seasonal events: they surged to 500,000 in January 2025, then dropped below 200,000 by September that year—highlighting Polymarket’s weak user retention.

Dune data shows that, since 2024, only 8%–11% of monthly users remain active a year later; roughly 75% churn within 90 days. Users return only for major events—and form no lasting loyalty to the platform.

This is only part of the problem.

Another key pain point: funds remain locked until event resolution. Perpetual futures are fundamentally different—underlying prices change every second, sustaining user attention and continuous trading activity. From a commercial standpoint, perpetual futures generate significantly higher trading volumes and fee income.

In 2025, global nominal perpetual futures trading volume exceeded $60 trillion, compared to just $28 billion for prediction markets.

Thus, expanding into perpetual futures is a natural evolution for prediction markets. Any platform capable of hosting one type of speculative activity tends to expand into adjacent categories—either by building in-house capabilities or acquiring specialized firms. Examples abound: Robinhood expanded from equities to options and crypto, then entered prediction markets; Coinbase acquired Deribit for $2.9 billion to enter derivatives; Binance launched from spot trading into futures and then built its own public chain ecosystem.

Traditional finance follows the same logic. By broadening service offerings, firms cross-sell new products to existing customers—delivering two core benefits: increased revenue per user and diversified income streams to hedge against sectoral cycles.

In the early 1970s, as commodity futures revenue at the Chicago Board of Trade (CBOT) declined, it leveraged a 4,000-square-foot lounge space owned by its parent company to launch the Chicago Board Options Exchange (now Cboe). The two product lines synergized through shared infrastructure: risk management, clearing and settlement systems, and a network of professionals skilled in derivatives pricing.

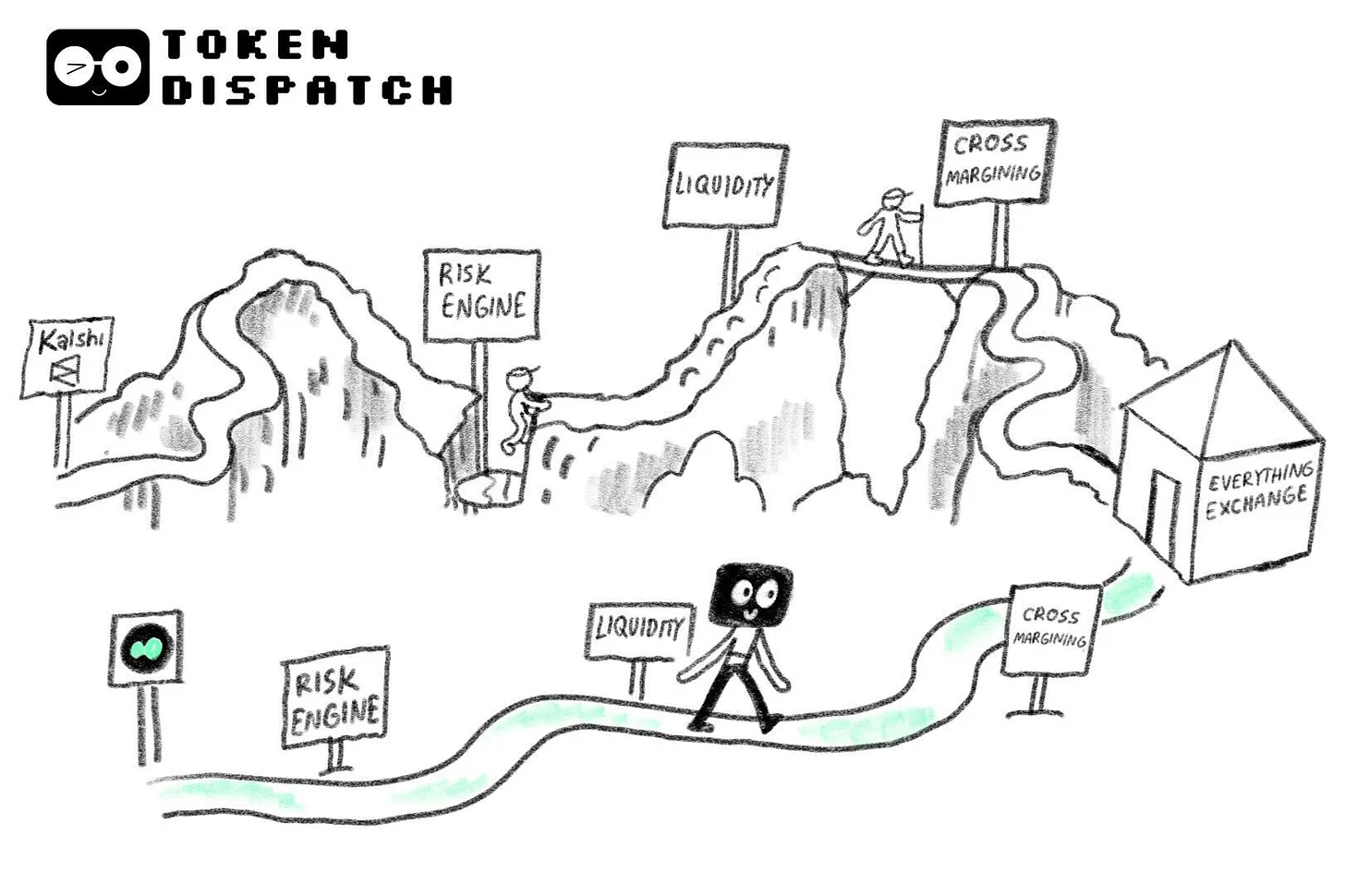

Yet building a perpetual futures platform—and operating it successfully—are two very different propositions.

Infrastructure Barriers to Entry for Perpetual Futures

Operating a perpetual futures exchange involves extremely complex system components—starting with liquidity.

Hyperliquid’s fully on-chain order book processes over 200,000 orders per second. Its two-way market-making mechanism clears $6–7 billion daily. Poor liquidity triggers extreme price volatility, wide bid-ask spreads, high slippage, and susceptibility to whale manipulation.

Second is the risk engine—the core lifeline of any derivatives platform. It tracks all positions in real time and validates margin rules on every order. During the October 2025 crypto market crash—when $19 billion in market value was liquidated overnight—Hyperliquid smoothly processed billions of dollars in liquidations without downtime.

Third is the funding rate mechanism, which anchors perpetual contract prices to underlying spot prices. The system automatically settles small funding payments between long and short positions every few hours to maintain fair pricing.

Building this full infrastructure stack isn’t the biggest hurdle for prediction market platforms—they likely possess the technical capacity to implement it. The real barrier lies in stress testing and real-world validation.

After completing its infrastructure, Hyperliquid underwent rigorous live stress tests—including the October 10 crypto liquidation wave and the Israel-Hamas conflict—before launching event contracts via HIP-4.

Kalshi and Polymarket, by contrast, follow the opposite path: they originally operated prediction markets, requiring none of this complex perpetual infrastructure. Now they must compete head-on with the battle-tested Hyperliquid—while their own systems have never endured the high-frequency trading or extreme market conditions inherent to perpetual futures.

Beyond this, multiple additional disadvantages make it far harder for prediction markets to enter perpetual futures than vice versa.

Hedging and Synergistic Effects

On Hyperliquid, the risk engine unifies visibility across all user positions—perpetuals, spot, and soon-to-launch event contracts—as Saurabh detailed when explaining HIP-4.

The system calculates positions holistically—not by category. The final liquidation threshold depends on the user’s aggregate leverage and cross-product margin sharing ratio. All positions—spot, perpetuals, prediction markets—are consolidated to determine required margin.

One might ask: Don’t general-purpose blockchains like Ethereum and Solana offer composability too? Yes—but each app runs its own isolated risk engine within its smart contracts, unable to atomically share position states. Kamino can’t see Pacifica’s positions; Aave can’t sync Lighter’s risk data. Without massive, coordinated upgrades across apps, building a unified, cross-platform risk engine remains prohibitively difficult.

Hyperliquid’s unified risk engine delivers a critical advantage: the same capital can be flexibly reused across multiple trades—optimizing capital efficiency.

For example: A trader goes long ETH at 5x leverage, while simultaneously buying an “Fed holds rates steady” event contract for $0.65, concerned about next week’s Fed decision. Thanks to the unified margin account, both positions share the same margin pool. If the Fed unexpectedly cuts rates, ETH surges—generating profit on the perpetual, while the event contract loses only its principal. If the Fed holds rates steady, the event contract profits and partially offsets drawdowns on the perpetual.

This implies prediction markets and perpetuals cannot function merely as add-on features. This native hedging capability is precisely the core insight behind Hyperliquid’s HIP-4 proposal—ordinary traders will treat prediction market positions as insurance against perpetual portfolio risk.

By contrast, Polymarket and Kalshi currently lock user funds until event settlement. Unless both platforms implement cross-product margin sharing, they forfeit a crucial competitive edge for retaining traders—neither has yet announced such functionality.

Moreover, structural and demographic mismatches raise further concerns about prediction markets entering perpetuals.

Over 80% of Kalshi’s monthly volume comes from sports betting; Polymarket’s sports segment accounted for over 40% of its 2025 volume. Sports events struggle to support the continuous pricing mechanics essential to perpetuals—meaning much of their existing user base doesn’t overlap with the target perpetual audience.

Additionally, Kalshi’s typical user is a retail investor unfamiliar with crypto, funding accounts via bank ACH transfers. Even if cross-margin functionality launches, such users lack the expertise to use perpetuals for hedging prediction positions.

Breakout Opportunities for Prediction Market Platforms

Only one scenario offers a viable path forward: if Kalshi and Polymarket officially launch cross-product margin sharing—and partner with top-tier brokers and clearinghouses—they could attract high-net-worth capital and high-frequency traders to both event contracts and perpetuals.

Institutional trading desks could integrate prediction markets into their broader risk management toolkits.

Both platforms already enjoy strong institutional partnerships: Kalshi collaborates with FIS and Tradeweb on data; Polymarket partners with Intercontinental Exchange (ICE). These relationships help retain institutional clients who prioritize “hedging and capital optimization on a single platform.”

Yet this breakout path remains highly uncertain—dependent on multiple conditions aligning: deploying infrastructure validated under extreme market stress, deepening institutional collaboration, and proving tangible value in capital efficiency and risk management.

In today’s hyper-competitive landscape, these are survival essentials. Hyperliquid has firmly captured first-mover advantage and user traction—leaving Kalshi and Polymarket no choice but to fight for differentiation elsewhere.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News