Stablecoin Payments: Seven Major Sectors, Who Will Emerge as the Ultimate Winner?

TechFlow Selected TechFlow Selected

Stablecoin Payments: Seven Major Sectors, Who Will Emerge as the Ultimate Winner?

Each field has its unique "moat" and different ways of capturing value.

Author: Rob Hadick >|<

Translation: TechFlow

Recently, many people have been asking me about the future direction of the stablecoin market and which part of this ecosystem might accumulate the most value. Here, I’d like to share some unfiltered personal thoughts.

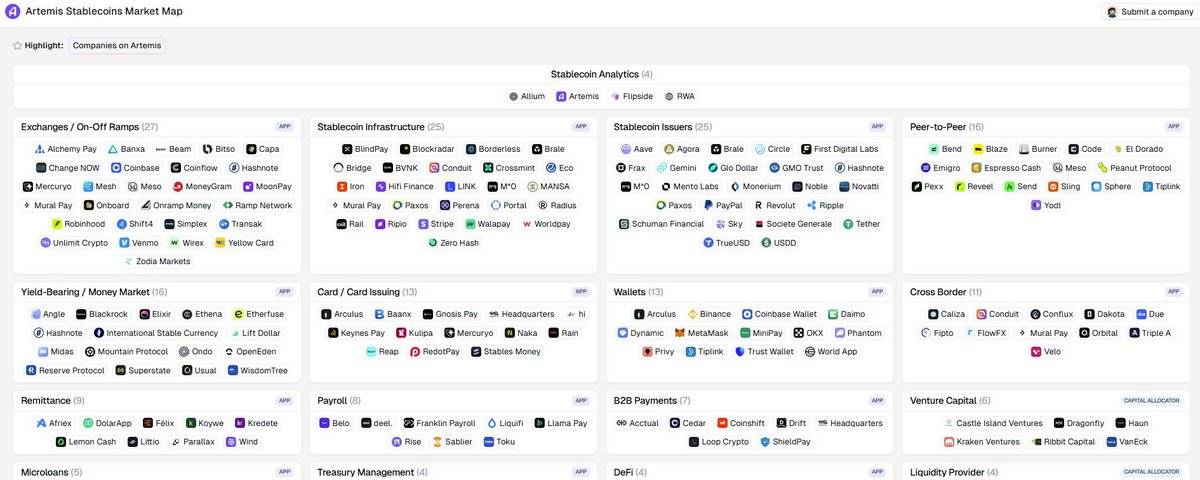

In my analysis, I divide the market into several categories—more granular than most frameworks I’ve seen (though not as comprehensive or complex as @artemis__xyz’s market map, which is truly excellent)—because payment systems are inherently intricate and nuanced. For investors, understanding each player’s role and where value accrues is especially important, as these critical details are often overlooked. I break down the stablecoin market into seven categories:

(1) Settlement Rails

(2) Stablecoin Issuers

(3) Liquidity Providers

(4) Value Transfer / Money Services

(5) Aggregated APIs / Messaging

(6) Merchant Gateways

(7) Stablecoin-Powered Applications

You might wonder: why so many categories? Especially since I’m not even discussing core infrastructure such as wallets or third-party compliance services? The reason is that each domain has its own unique "moats" and distinct ways of capturing value. While there is some overlap among service providers, deeply understanding the differences between each segment is crucial.

Below are my views on value distribution across these categories:

1. Settlement Rails:

The key competitive advantage of settlement rails lies in network effects—including deep liquidity, low transaction fees, fast settlement times, reliable uptime, and built-in compliance and privacy protections. These factors make it highly likely that this space will evolve into a winner-takes-most market. I remain skeptical that general-purpose blockchains can meet the scale and standards required by major payment networks. Although scaling solutions or Layer 2s on general-purpose chains may work in certain use cases, we ultimately need solutions purpose-built for payments. The winners in this space will be extremely valuable and will likely focus specifically on stablecoins or payments.

2. Stablecoin Issuers:

Currently, stablecoin issuers (such as @circle and @tether_to) are clear market winners, benefiting from strong network effects and the current high-interest-rate environment. However, looking ahead, their growth will hit a ceiling if they continue operating more like asset management firms than payment companies. Issuers need to invest more heavily in fast and reliable payment infrastructure, robust compliance processes, low-cost minting and redemption mechanisms, seamless integration with central and core banks, and stronger liquidity support (similar to what @withAUSD is doing). While "stablecoin-as-a-service" platforms (like @paxos) could spawn numerous competitors, I still believe neutral stablecoins issued by non-bank fintechs will emerge as the dominant players, because market competition won’t allow closed-loop systems to operate independently without credible neutral intermediaries. Stablecoin issuers have already accumulated significant value, and leading players will likely maintain their edge—but they must move beyond just issuance.

3. Liquidity Providers (LPs):

Liquidity providers today are primarily OTC desks or exchanges. They are either large, successful crypto-native firms or smaller players who underperform in broader crypto markets and pivot into stablecoin-focused operations. This space is fiercely competitive, with very little pricing power. Their moats rest mainly on access to cheap capital, operational reliability, deep liquidity, and support for multiple trading pairs. Over time, larger players are likely to dominate, while LPs focused solely on stablecoins may struggle to build durable competitive advantages.

4. Value Transfer / Money Services ("PSPs" for Stablecoins):

This category is sometimes referred to as "stablecoin orchestration" platforms—for example, @stablecoin and @conduitpay. They build defensibility through proprietary settlement rails and direct partnerships with banks (rather than relying on third-party providers). Their moats lie in deep banking relationships, flexibility in handling various payment forms, global reach, liquidity assurance, system stability, and strict compliance standards. While many companies claim these capabilities, only a few actually possess dedicated infrastructure. Winners in this space will gain some pricing power, form regional duopolies or oligopolies, and grow into sizable businesses by complementing traditional payment service providers (PSPs).

5. Aggregated APIs / Messaging Platforms:

These platforms often claim to offer services similar to PSPs, but in reality, they merely wrap or aggregate existing APIs. Unlike PSPs, they don’t directly assume compliance or operational risk; instead, they function more like marketplaces connecting PSPs and liquidity providers (LPs). Currently, they can profit from charging high fees, but over time, they may face margin compression or even displacement, as they don’t solve core challenges in payment flows or infrastructure. Some compare themselves to “Plaid for stablecoins,” but they overlook the fact that blockchain itself has already solved many of the problems Plaid addressed for legacy banking and payment systems. Unless these platforms extend closer to end users and take on more of the service stack, they’ll struggle to maintain margins and long-term competitiveness.

6. Merchant Gateways / Payment On-Ramps:

Merchant gateways help businesses and merchants accept stablecoin or cryptocurrency payments. While their functions sometimes overlap with PSPs, they typically focus more on developer-friendly tools, integrating third-party compliance and payment infrastructure into user-friendly interfaces. These platforms aim to differentiate via easy developer integration, following a path similar to Stripe. However, unlike Stripe’s early days, developer-friendly payment options are now abundant, and distribution becomes the decisive factor. Traditional payment companies can easily partner with orchestration platforms to add stablecoin support, making it difficult for crypto-only gateways to gain an edge. While companies like Moonpay and Transak previously profited from premium pricing, that advantage may not last. In B2B, certain platforms may succeed by offering unique enterprise features (e.g., large-scale treasury management), but prospects in B2C look bleak. Overall, this sector faces significant headwinds.

7. Stablecoin-Powered FinTech and Applications:

It’s easier than ever to launch a stablecoin-based “neobank” or fintech app, meaning competition in this space will be intense. Winners will be determined by distribution strength, go-to-market strategy, and differentiated product design—much like in traditional fintech. However, well-known brands like Nubank, Robinhood, and Revolut can easily integrate stablecoin functionality, making it hard for startups to stand out in developed markets. Emerging markets may offer more room for innovation (e.g., @Zarpay_app), but if your differentiation is merely offering financial services via stablecoins, you’re likely to fail in mature markets. Overall, I expect a very high failure rate in this space, with consumer-facing crypto/stablecoin startups facing immense challenges. That said, enterprise-focused business models may still find viable niches.

Of course, there are edge cases and overlaps not covered here. But this framework helps us as investors better understand opportunities in the stablecoin market. Feel free to share your thoughts. If you're interested in any of the above—or if you're a startup seeking funding—don’t hesitate to reach out.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News