Opportunities and Challenges Under Uniswap's Innovation: Where is DEX Heading?

TechFlow Selected TechFlow Selected

Opportunities and Challenges Under Uniswap's Innovation: Where is DEX Heading?

AMM will focus on the long-tail market in the future, but we also need to continuously optimize the landscape where PMM gradually dominates.

Author: IOSG Ventures

Introduction

Uniswap has recently been driving three main initiatives: Uniswap X, Uniswap V4, and Unichain.

Uniswap introduced the intent-based trading network Uniswap X last year, which now captures 10%-20% of trading volume. During the same period, 1Inch, 0x, and Cowswap also adopted similar intent-based trading experiences.

Over the past few months, the DEX landscape has shifted toward intent-based protocols that unify on-chain and off-chain liquidity, enabling traders to enjoy better user experience and lower prices. These protocols have introduced market makers, searchers, solvers, and other roles who obtain quotes from DEX front-ends and access any liquidity source including CEXs. After Uniswap launched UniswapX and enabled it by default in its front-end, Uniswap became a key player in demonstrating how intent protocols impact AMM liquidity.

Uniswap completed contract audits in September and is about to launch V4. Key features in V4 include Hooks, a single-contract design, gas fee optimization, and flash contracts. The single-contract design in Uniswap V4 consolidates all liquidity pools into one smart contract instead of creating separate contracts for each trading pair as in V3. This significantly reduces transaction costs—especially for multi-pool swaps and complex trade paths—and allows for more concentrated liquidity and improved trading efficiency. Due to this unified architecture and the new Hook system, Uniswap V4 achieves lower gas fees when executing complex trades.

Hooks build various DeFi services on top of AMMs through a plugin model, allowing developers to insert custom logic during transactions—such as dynamic fees, liquidity management strategies, or independent control over specific trading pairs. Hooks offer unprecedented flexibility to AMMs, enabling developers to create more sophisticated liquidity strategies and dynamically adjust trading parameters under different market conditions.

Unichain primarily serves as a liquidity hub within the OP Superchain ecosystem and helps improve experiences for traders and LPs. We will not discuss Unichain in depth here; further research on Unichain will be published later.

Besides Uniswap, many other protocols are innovating along similar lines, particularly in the area of Hooks—including Balancer and Ekubo on Starknet. Others achieve Hook-like functionality through modular DEX designs like Valantis. Around the Hook paradigm, existing protocols focused on solving AMM limitations—especially liquidity management protocols—now have better entry points. On the intent side, Cowswap, 1inch Fusion, and even long-tail DEXs are building their own intent networks, reflecting an ongoing competition between PMM and AMM—PMM's continuous encroachment on on-chain liquidity markets versus on-chain protocols' efforts to retain more on-chain liquidity.

In light of these evolving dynamics in the DEX space, this article explores three key perspectives on future trends we believe will shape the DEX landscape:

1. AMMs will resolve current structural issues and expand their scope by leveraging plug-in/modular capabilities to migrate into broader DeFi use cases such as liquidity management, asset issuance, personalized financial services, and trading strategies.

2. In intent-centric DEX designs, front-ends lose strategic importance while LPs face vertical competition across the trading supply chain.

3. AMMs will increasingly focus on long-tail markets, but we must continuously optimize the growing dominance of PMM models.

1. AMM Resolving Current Structural Issues and Expansion

The expansion of AMM’s role aims to address several core pain points and capture previously unreachable market segments.

This transformation is largely driven by Hooks—the central innovation in Uniswap V4—which allow developers to inject custom logic into the trading process, such as setting dynamic fees, implementing liquidity management strategies, or exerting independent control over specific trading pairs. Hooks grant AMMs exceptional flexibility, expanding their operational scope. Developers can now build more complex liquidity strategies and adapt them to varying market conditions.

1.1 Addressing LP Management Challenges in AMM

-

Impermanent Loss (IL)

Impermanent loss remains the biggest challenge for LPs. When LPs deposit assets into liquidity pools, the AMM algorithm automatically rebalances holdings to maintain asset parity. During price volatility, LPs may suffer disproportionate losses, causing their portfolio value to fall below what it would have been had they simply held the assets.

Impermanent loss stems from the "negative gamma" characteristic of AMMs. In finance, gamma measures the rate of change of delta—the sensitivity of a portfolio's value to changes in the underlying asset price. In AMMs, price fluctuations alter asset ratios, leading LPs to accumulate underperforming assets.

For example, when the price of one asset in a pool rises, the AMM sells the appreciating asset and buys the depreciating one to rebalance. As a result, LPs fail to benefit from upward price moves and instead end up holding more of the losing asset. This negative gamma effect is especially pronounced in AMMs like Uniswap v2, where LP positions grow proportionally to the square root of price changes. Uniswap v3’s concentrated liquidity mechanism further amplifies this nonlinearity, making impermanent loss a critical risk for LPs.

-

Strategies to Mitigate Impermanent Loss

To counter impermanent loss, LPs employ various hedging strategies to reduce volatility risk and secure more stable returns. Some effective approaches include:

-

Perpetual contracts for gamma hedging: LPs can hedge impermanent loss risks using perpetual futures or options. For instance, a straddle strategy—buying both call and put options—can mitigate risks from bidirectional price swings. Perpetual contracts provide continuous hedging without expiration dates, making them ideal for highly volatile environments.

-

Selling options (LP as option writer): Since LP income resembles that of an option seller, protocols like Panoptic allow LPs to sell their positions as tradable options, effectively selling volatility—particularly effective in low-volatility markets. Panoptic’s model transforms LP positions into tradeable financial instruments, enabling LPs to earn premiums.

-

Liquidity management protocols: active position management and rebalancing

Beyond hedging, LPs can actively manage their liquidity positions to reduce impermanent loss and increase profitability.

-

Rebalancing based on market indicators: LPs can use technical indicators such as MACD, TWAP, and Bollinger Bands to trigger rebalancing actions. Monitoring these metrics enables LPs to adjust liquidity ranges and exposure, reducing downside risk during high volatility.

-

Inventory management strategies: LPs can apply inventory management techniques to dynamically adjust asset holdings. Protocols like Charm Finance and ICHI help LPs manage liquidity dynamically, ensuring positions adapt to volatility or price shifts to avoid excessive losses.

In addition, some liquidity management protocols, such as Bunniswap, build tools on top of Uniswap V4 Hooks to help users optimize liquidity management and unlock additional incentives.

-

Latency Vulnerability Risk (LVR)

AMMs operate on-chain, and due to block propagation delays and simultaneous transaction submissions, price updates typically lag behind CEXs. Arbitrageurs exploit these price discrepancies, forcing LPs to sell assets at unfavorable prices and incur losses.

According to a16z researcher Tim Roughgarden, LVR causes ETH-USDC LPs to lose 11% of principal annually. Reducing LVR risk by 50% could translate into a 5.5% annual yield gain for LPs.

To mitigate LVR, several innovative solutions have emerged:

-

Pre-confirmation protocols: MEV-boost and PBS allow block builders to pre-confirm execution prices, reducing arbitrageurs’ ability to manipulate prices. This solution is particularly emphasized in Unichain.

-

Oracle-based pricing: By incorporating real-time CEX price data, protocols like Ajna Finance ensure AMMs reflect accurate market prices, minimizing losses from lag.

-

Intent-based AMMs: Intent-driven AMMs let LPs set execution conditions, only trading at optimal prices, using RFQ (request-for-quote) mechanisms to reduce latency-driven arbitrage.

-

Enhancing LP Returns Through Active Management

Many liquidity management protocols maximize LP returns by better estimating implied volatility and adjusting asset allocations accordingly—extracting implied volatility data from trading volume and liquidity patterns, assessing potential risks, and adjusting positions. By comparing potential LP fee income with hedging costs, LPs can make informed decisions on when to hedge or hold. For example, Gamma Strategy uses a MACD-based hedging approach to instantly hedge LP risk as a financial product, increasing overall returns.

-

RFQ for MEV Avoidance/Capture and Dynamic Fee Structures

MEV capture mechanisms redistribute MEV gains by auctioning off MEV rights, ensuring LPs benefit not only from trading fees but also from arbitrage opportunities.

Pioneers like CoW Swap protect traders and LPs by batching trades via its CoW AMM and having solvers bid in batch auctions, settling all trades at a uniform price point—eliminating MEV created by LVR. Angstrom from Sorella Labs builds an off-chain auction system using Uniswap V4 Hooks to prevent arbitrage entirely.

App-chains like Unichain reduce MEV exposure for traders and LPs by providing TEE-secured block-building environments and pre-confirmation capabilities.

Through Hooks, Uniswap V4 enables dynamic fee structures. Unlike fixed fees, dynamic fees can adjust according to market conditions and LP preferences. For example, fees may rise during high volatility to compensate LPs for increased risk, and decrease during calm periods. This flexible fee model enhances LP returns while offering better prices to traders.

Arrakis’s HOT AMM introduces a dynamic fee model that identifies arbitrage trades and applies higher fees to mitigate latency risk, helping LPs capture more value from high-frequency and arbitrage trading.

1.2 Personalized Business Logic

Different users have subjective preferences regarding risk and return. A lack of differentiation fails to explain user behavior and misses opportunities to enhance stickiness, incentivize positive actions, and optimize capital utilization.

V4’s liquidity pools support more flexible configurations, allowing developers to use hooks and custom logic to create diverse pool types. For example, specialized pools can be built for hedging market risk or executing specific arbitrage strategies. Cork Protocol is currently building an AMM via Hooks to trade de-peg risk tokens for LRT ETH. This opens up new innovation opportunities and direct integration possibilities within AMMs, transforming Uniswap from a mere trading platform into an open platform for liquidity and trading strategies. Verifiable off-chain computation will become increasingly important—for instance, ZK coprocessors like Brevis, combined with advances in verifiable computing, can bring external data to enhance AMM personalization. Meanwhile, in intent networks, this also helps reduce trust assumptions around solvers.

1.3 Asset Issuance

One of the most exciting expansions for AMMs lies in asset issuance. Capabilities previously unavailable on Uniswap—like Liquidity Bootstrapping Pools (LBPs)—can now be implemented via Hooks, as Doppler is doing. Further innovations could enable Uniswap to develop asset issuance capabilities surpassing even those of pump.fun, directly capturing value from token launches.

2. Intent-Centric DEX Design: Declining Front-End Importance and Vertical Competition Facing LPs

2.1 Reduced Front-End Relevance and Increased Vertical Competition

The relevance of front-ends will decline because efficient solver markets eliminate advantages gained from protocol-specific front-end execution. The diversity of pools brought by V4, along with the potential for toxic traffic associated with certain Hooks, means Hook-controlled pools cannot be directly routed by Uniswap. This reflects the future state of modularized AMMs—most pools will operate behind the scenes, routed directly by intermediaries (i.e., solvers), rather than interacting with users via front-ends.

An intent-centric future will profoundly impact our understanding of value capture in the trading supply chain, affecting LPs, bridge protocols, and overall user experience. In this scenario, the role of front-ends will diminish. Protocols will compete on efficiency rather than user acquisition via front-ends. This trend began with DEX aggregators, as some DEXs gained significant volume through aggregators despite minimal user traffic on their native front-ends.

We’re already seeing DEXs like Ekubo on StarkNet that do not provide a swap front-end at all, relying entirely on DEX aggregators. In future solutions, their liquidity routes swaps directly, accounting for approximately 75% of all transactions on StarkNet.

2.2 Current Limitations of RFQ Systems

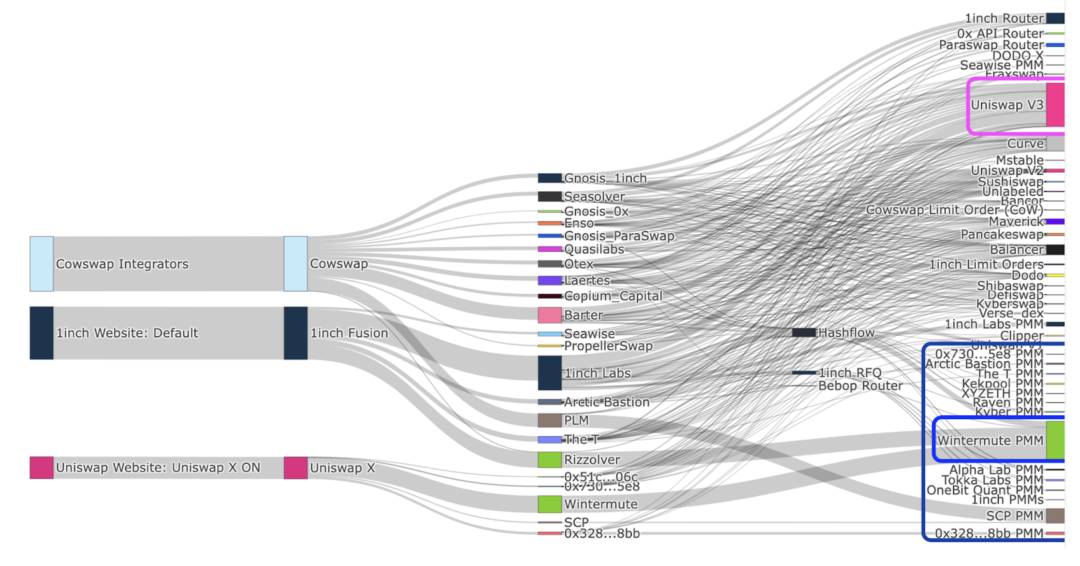

Most intent protocols on Ethereum remain isolated, primitive intent systems where users express protocol-specific intents, primarily around trading. Major examples include CoW Swap, 1inch Fusion, and UniswapX.

One of the biggest current issues with RFQ systems is the lack of composability of intents. This limitation calls for universal intent networks and architectures. Teams like Essential are working on open, universal intent standards such as ERC-7521 to establish common frameworks that improve user and solver experiences.

For solvers specifically, serving multiple protocols across stacks requires building efficient on-chain routing, maintaining off-chain liquidity sources, managing private order flow, and handling inter-protocol latency. Beyond protocol unification, vertical integration of roles across the trading supply chain becomes crucial. For pools and liquidity providers, the best way to capture traffic in intent networks is often to become a solver themselves. To better protect all parties’ interests amid the various risks outlined above, collaboration with block builders becomes essential. This leads to vertical integration among RFQ participants—solver providers offering their own liquidity via off-chain/AMM pools and collaborating directly with builders. However, this raises potential centralization concerns, as reduced competition in solver auctions may undermine the price efficiency originally envisioned.

3. AMMs Will Focus on Long-Tail Markets; Optimizing the Growing Dominance of PMM

The long-tail effect in crypto assets is pronounced: blue-chip pools are increasingly captured by off-chain liquidity. High-liquidity, large-cap tokens are ultimately filled by off-chain resources—especially PMMs—while long-tail, low-market-cap tokens are routed to AMMs. This is already partially reality.

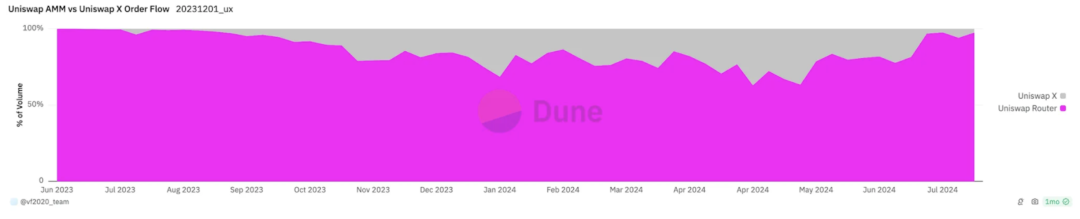

About 60–80% of total weekly trading volume on Uniswap Labs’ front-end is filled by AMMs. Yet, looking at individual trades, intent-based systems currently account for about 30% of all DeFi volume—a figure that has remained steady since early 2022. PMMs dominate intent-driven order flow, with Wintermute leading the pack, consistently capturing at least 50% of PMM-facilitated intent flows since September 2023.

As intent adoption grows, PMMs are receiving increasing volumes of non-toxic flow. But AMMs serve more than just long-tail liquidity: in ETH/USDC trades routed through UniswapX and the Uniswap front-end, only 30% of volume goes to AMMs. The advantage of PMMs (private market makers) lies in their ability to provide liquidity and capture non-toxic flow efficiently.

3.1 Disadvantages of AMMs

-

From the perspective of LP price lag

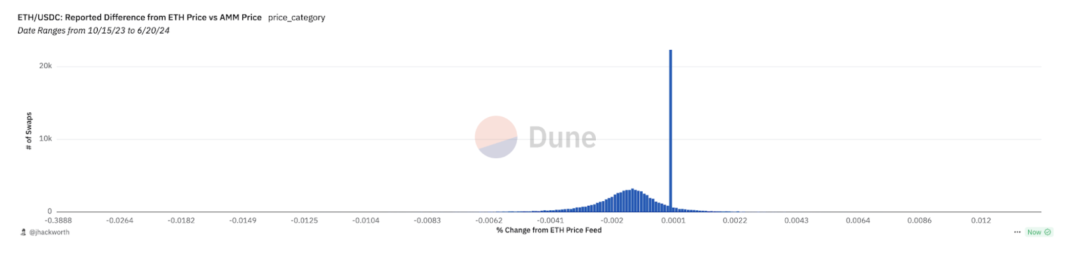

Due to delayed price updates, AMMs may quote stale prices that appear better than current market prices—typically set by CEXs. This helps explain why some traffic still flows to AMMs.

This phenomenon was observed by Variant in its analysis of Uniswap X. The chart below shows the difference between DEX quotes and estimated market prices derived from CEX APIs for trades routed to AMMs via the Uniswap front-end. On average, AMM liquidity is priced below market levels, indicating that traffic flows to AMMs because LPs offer seemingly better—but outdated—prices.

-

From the perspective of intent economics

For long-tail assets, the cost for off-chain liquidity fillers as a percentage of trading volume decreases with larger trade sizes, whereas AMM costs decline more slowly. This indicates weaker economies of scale for AMMs—making off-chain liquidity filling cheaper as trade size increases. Fillers’ only costs come from relatively inefficient gas usage and hedging expenses.

-

From the perspective of AMM incentives

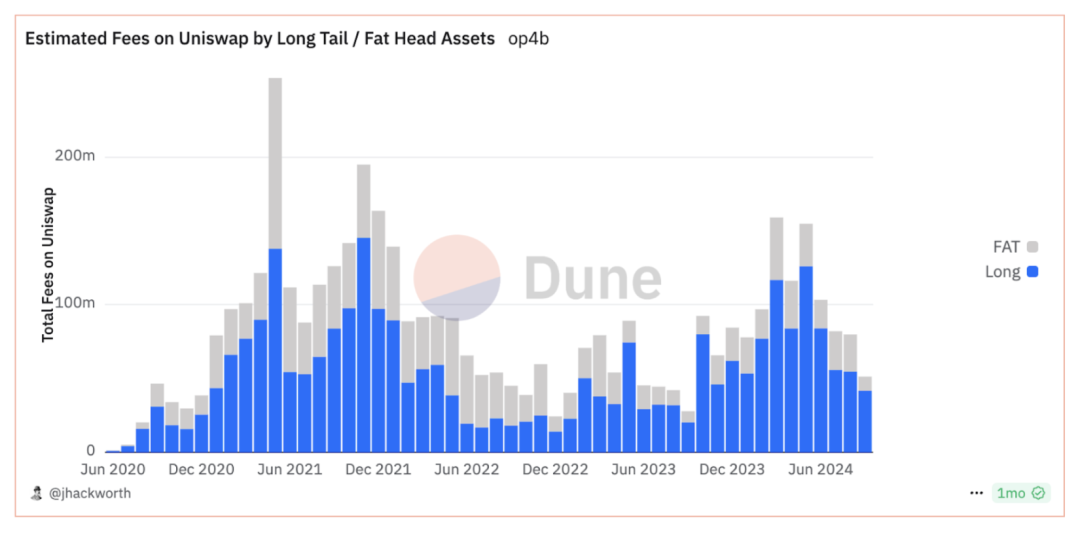

Uniswap’s trading volume is increasingly concentrated in top-tier assets, but fee generation trends are exactly the opposite. Most fees each month come from long-tail trading pairs. This is because Uniswap V3 introduced lower fee tiers, intensifying competition among top-tier liquidity. Long-tail liquidity is more valuable—it is less fee-sensitive, scarcer, and for these assets, price discovery often matters more than price efficiency.

3.2 Advantages and Potential Issues of PMM

As PMMs attract more traffic through intent-based systems, AMM LPs face a higher proportion of toxic, arbitrage-driven traffic. LPs suffer greater losses in this environment because they rely on fees from non-toxic flow to offset losses from toxic flow. New AMM designs aiming to capture non-toxic flow must now compete directly with PMMs.

The entities behind these PMMs are traditional market makers such as Jump, Jane Street, GSR, Alameda, and Wintermute.

These market makers achieve higher profit margins by vertically integrating every layer of the MEV supply chain. In today’s environment, they outperform pure on-chain liquidity providers by collaborating closely with builders and other MEV participants to execute MEV strategies and produce blocks.

However, for long-tail assets, on-chain AMM LPs still hold an edge. This is because CVMMs (centralized vol-controlled market makers) face inventory risk when providing liquidity, requiring corresponding hedging strategies—which remain difficult to implement effectively for long-tail assets.

Ultimately, this is a battle between on-chain liquidity and off-chain market makers. As off-chain market makers erode on-chain liquidity, if price discovery gradually shifts off-chain, on-chain DEX liquidity may shrink. Our ultimate goal should be to shift liquidity *onto* the chain—not merely make accessing off-chain liquidity easier.

Arrakis is vertically integrating into the MEV supply chain through its next-generation AMM called HOT. This solution aims to reclaim MEV for LPs and build healthier, fairer on-chain markets. With HOT AMM at its core, Arrakis takes the first step in addressing DeFi’s CVMM problem by protecting on-chain LPs. HOT is a liquidity module powered by modular capabilities provided by Valantis.

4. Conclusion

With the development of DEX RFQ networks like Uniswap X and Arrakis, and modular DEX architectures such as Uniswap V4 and Valantis, the DEX landscape is entering a new phase.

First, many structural issues within AMMs will be resolved, and their operational scope will greatly expand. The most urgent issue is that of LPs, which can be broken down into two types of losses: IL and LVR. These can be addressed through various liquidity management protocols, derivatives (which can be integrated as modular components into AMMs), and RFQ systems—thereby raising the ceiling for on-chain liquidity provision. Additionally, personalized business logic, cross-chain trading, and asset issuance capabilities will enable AMMs to capture more financial value and expand into broader use cases. We are particularly bullish on any protocol innovation that effectively broadens the AMM application landscape.

Second, under the current intent-driven paradigm, many challenges related to RFQ systems remain unresolved. The entire trading supply chain has undergone significant transformation—similar to what we’ve seen in block production—where vertically integrated service providers now hold greater advantages.

Finally, AMMs will increasingly focus on long-tail markets while striving to optimize the growing dominance of PMM models. As intent networks evolve, centralized market makers with vertically integrated trading pipelines will gain absolute advantages in liquidity for most blue-chip assets. This results in increased toxic flow and declining yields for on-chain native liquidity providers. To strengthen the decentralized on-chain trading ecosystem, exploring ways to enhance AMM competitiveness—especially in long-tail asset markets—remains a key area of focus for us going forward.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News