PayFi New Era: Solana Leads the Future of Blockchain Payments and On-Chain Finance

TechFlow Selected TechFlow Selected

PayFi New Era: Solana Leads the Future of Blockchain Payments and On-Chain Finance

PayFi's core advantage in realizing its vision lies in leveraging Solana's high performance to break down the barriers between the real world and blockchain, while regulation and scalability remain the biggest challenges for achieving widespread adoption.

Author: YBB Capital Researcher Ac-Core

TL;DR

● The PayFi concept was introduced by Lily Liu, Chair of the Solana Foundation, during her keynote speech titled "The Emergence of PayFi: Realizing the Vision of Cryptocurrency" at the 7th EthCC conference;

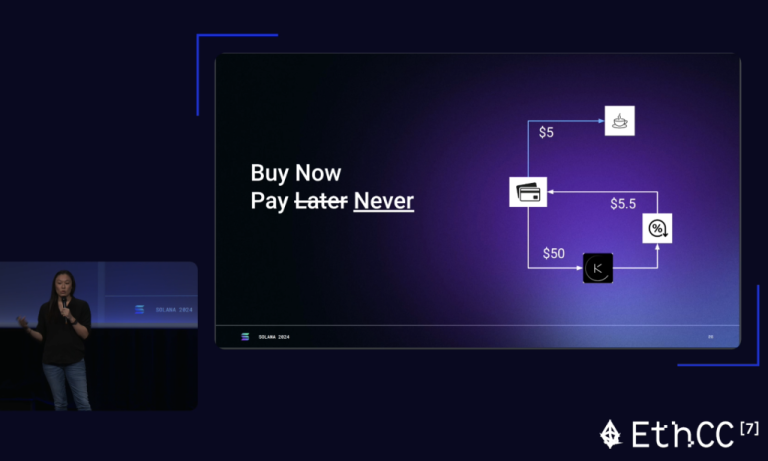

● Core ideas of PayFi: 1. Emphasizes “instant settlement,” especially valuable in speculative trading; 2. Supports a new model of “Buy Now, Pay Never,” opening new pathways for creator monetization, invoice financing, and payment risk management;

● The key advantage enabling PayFi’s vision lies in leveraging Solana’s high performance to break down barriers between the real world and blockchain, while regulation and scalability remain the biggest challenges to widespread adoption;

p>● Lily Liu offered a concise definition of PayFi: "PayFi creates new financial markets around the time value of money. On-chain finance can enable novel financial primitives and product experiences that traditional finance—and even Web2 finance—cannot achieve."1. What is PayFi?

Image source: 7th EthCC Conference

PayFi, short for Payment Finance, is an innovative paradigm combining payments and finance, proposed by Solana Foundation Chair Lily Liu at the EthCC conference in July 2024. Its core focuses on “instant transactions” to enhance efficiency in speculative trading and various financial operations. According to its founder Lily Liu, PayFi is a programmable financial structure that enables financial innovation atop the settlement layer while autonomously handling payment transactions. Based on content from Elponcho, here is a summary:

The Vision of PayFi

"To build a system of programmable money within an open financial system, empowering users with economic sovereignty and self-custody."

PayFi Use Cases

New technologies create new markets. By supporting a “Buy Now, Pay Never” model, PayFi leverages on-chain finance and instant settlement so that profits generated on-chain can immediately cover real-time consumption needs. For example, a user could deposit $50 into an on-chain yield-generating protocol, and use the instantly settled interest to purchase a “free” cup of coffee.

Additionally, PayFi enables monetization based on progress toward goals (e.g., YouTubers gradually receiving ad revenue as they approach 1 million views), supports invoice financing, manages payment processing risks, and builds a global private credit pool on the Solana blockchain. Lily Liu believes PayFi will surpass DeFi and lead the next wave of financial innovation.

Solana and PayFi

Lily Liu argues that Solana stands out among blockchains due to its high performance, consistently demonstrating fast transaction speeds and low costs, giving it advantages in capital and talent mobility. Clearly, Solana is a strong candidate for realizing the PayFi vision.

Three Key Factors for PayFi Success on Blockchain

Lily Liu identifies three critical success factors for blockchain: fast and low-cost transactions, a broad user base, and a strong developer community. She asserts that currently, Solana is the only ecosystem fully possessing all three elements.

The Future of PayFi and Solana

In closing her talk, Lily Liu outlined various financial applications possible on Solana, including supply chain finance, payday loans, credit cards, corporate lending, interbank repo markets, and insurance markets. These examples demonstrate the immense potential of combining Solana with PayFi to transform traditional financial systems.

In her article “Understanding PayFi: Solana’s Next Narrative,” Lily Liu emphasizes that PayFi centers on the time value of money, illustrated through three key cases:

● Buy Now, Pay Never: Most people are familiar with “Buy Now, Pay Later” (BNPL), but “Buy Now, Pay Never” is almost its opposite. BNPL optimizes cash flow via installment payments with interest, whereas the latter involves investing funds in DeFi products to earn interest, then using that interest to pay for consumption—sacrificing liquidity but preserving principal.

For instance, if a user buys a $5 coffee, they might lock $50 in a lending product until the accrued interest reaches $5, then use the interest to cover the cost. Afterward, the principal is unlocked and returned to the user. This process relies on automated execution via “programmable money.”

● Creator Monetization: Many creators face cash flow issues during content creation, which requires upfront time and investment while returns come later—potentially causing financial strain and slowing production. In Lily Liu’s vision, PayFi helps accelerate monetization. For example, if a video is expected to generate $10,000 in revenue one month later, the creator could receive $9,000 immediately via PayFi, sacrificing some future income for improved cash flow today.

● Accounts Receivable: A common financial relationship between businesses and customers, referring to money owed by clients. Due to receivables, companies may face cash flow shortages. To address this, firms often pledge receivables to financing companies or sell them at a discount to obtain immediate funds. PayFi aims to further streamline and optimize this process—using blockchain to accelerate settlement, improve capital turnover, lower entry barriers, and allow more businesses to access such supply chain finance tools, thereby accelerating capital flow.

2. How PayFi Integrates with DeFi: RWA as the Bridge to a New Narrative

Image source: Coincu

The origins of blockchain technology trace back to Satoshi Nakamoto’s revolutionary 2008 whitepaper, “Bitcoin: A Peer-to-Peer Electronic Cash System,” which laid the foundation for a new era of decentralized payments—creating not only a new form of currency but fundamentally transforming entrenched traditional financial payment systems. PayFi utilizes blockchain technology and smart contracts, employing digital assets and decentralized finance (DeFi) tools to manage capital flows. Its core principle is optimizing the time value of money and shortening settlement times through decentralized technology. Key operational principles include:

● Time Value of Money (TVM): PayFi emphasizes enhancing the time value of money to improve capital efficiency. For example, users can deposit funds into lending platforms and use earned interest to cover daily expenses. If buying a $5 coffee, a user could lock $50; once interest accumulates enough to cover the coffee, the principal remains untouched;

● Smart Contract Automation: Smart contracts are central to PayFi, automatically executing complex financial operations based on predefined conditions, reducing intermediaries, accelerating transactions, and lowering costs;

● Tokenization of Real-World Assets (RWA): PayFi tokenizes real-world assets like real estate and accounts receivable, facilitating cross-border payments and capital movement. This increases liquidity of physical assets and provides a new platform for global transactions.

As demand rises in the crypto ecosystem for sustainable value-bearing assets, RWA has naturally become a popular option. Over the past two years, tokenized Treasury bills yielding 4–5% became the preferred choice for on-chain capital, rapidly growing total value locked to $2 billion. With inflation and signals of central bank rate cuts, Treasury yields have declined, prompting capital to seek other high-yield, low-risk assets—creating opportunities for PayFi’s growth in the RWA space.

Typical PayFi Scenarios Include

1. Cross-Border Payment Financing: Arf transforms traditional cross-border payments by providing financial institutions with on-chain liquidity solutions, enabling 24/7 instant, transparent, and low-cost USDC-based settlements, eliminating the need for globally pre-funded accounts. Cross-border payment financing offers exceptional capital efficiency and scalability;

2. Digital Asset-Backed Corporate Cards: Rain provides Web3 teams with USDC-backed corporate card settlement liquidity. Companies stake funds in vaults set with credit limits, and at the end of each settlement cycle, assets are cleared on-chain to automatically repay the card balance, reshaping expense management;

3. Trade Finance: BSOS integrates enterprise resource planning (ERP) platforms with on-chain liquidity to create real-world assets (RWA) within supply chains, offering shorter-term financing options to meet business funding needs.

Real-World Assets (RWA) May Include

1. Instant RWA Settlement: Even highly liquid assets like Treasuries or tokenized funds typically require 2–4 days to settle, as underlying assets must be liquidated before redemption. However, on-chain liquidity pools enable 24/7 real-time subscription and redemption, ensuring fast and transparent transactions.

2. DePIN Financing: As the DePIN ecosystem rapidly expands, many projects operate on the idea of sharing large infrastructure costs and redistributing future value. For example, TLay provides critical trust infrastructure to accelerate DePIN adoption; Peaq offers a purpose-built L1 for DePIN and features enabling machines to efficiently transact with each other or with humans, supporting the machine economy.

Meanwhile, the emergence of stablecoins bridged fiat currencies and blockchain, driving the first wave of real payment use cases. Since 2014, stablecoins have experienced exponential growth, proving increasing demand for blockchain innovation in payments. Today, stablecoins support approximately $20 billion in organic annual payments—approaching Visa’s annual payment volume. Although the crypto ecosystem continues overcoming challenges like poor user experience, latency, high transaction costs, and compliance to unlock stablecoins’ full potential, there remains room for advancement. Looking back at the history of payment systems, financing mechanisms have played a crucial role in their development. For example:

● Credit Cards: Contribute $16 trillion annually to merchant payments, showing how financing drives adoption and utility;

● Trade Finance: Provides $10 trillion in annual funding for B2B payments, highlighting its critical role in global commerce;

● Cross-Border Payments: Support global remittances and settlements with $4 trillion in prepaid funds. Today, one in six households worldwide relies on remittances.

Without payment financing, global liquidity would be severely constrained. Likewise, without financing mechanisms, the utility and adoption of internet-native money would also be hindered. PayFi emerged precisely to solve these limitations. Solana Foundation Chair Lily Liu clearly articulated the vision: "PayFi is a new financial market built around the time value of money. On-chain finance can deliver new financial primitives and experiences that neither traditional finance nor even Web2 finance can offer."

3. Reflections on PayFi

Image source: Solana official website

Solana has always led in generating momentum within the crypto market, continuously fueling speculative activity with diverse narratives. The new PayFi narrative reclaims blockchain’s inherent power to disrupt traditional finance, leveraging decentralization and security to reduce fraud risks, enhance transaction integrity, eliminate intermediaries in traditional payment processing, and encode entire transaction workflows on-chain—significantly lowering barriers to financial participation. From a storytelling perspective, PayFi serves as a bridge connecting RWA and DeFi to the real world.

Despite PayFi’s potential to support mass blockchain adoption, several challenges could limit its widespread implementation. Foremost is regulation—global financial institutions still lack full understanding or legal frameworks governing blockchain operations. Legitimacy remains the first hurdle to integrating with the real world. Another obstacle is scalability: blockchain networks may experience congestion during peak periods, affecting transaction speed and cost, and block production rates across different chains are difficult to synchronize. Market acceptance remains limited—enterprises and users still exhibit hesitation toward blockchain, often reacting with skepticism when crypto is mentioned. For blockchain to truly bridge into the real world, it must continuously refine its ability to reach broader domains and break through existing circles.

References:

1: PayFi: The Frontier of Blockchain Payment Finance

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News