Bitcoin ETF Options Approved: Is a Surge in Bitcoin Imminent?

TechFlow Selected TechFlow Selected

Bitcoin ETF Options Approved: Is a Surge in Bitcoin Imminent?

The approval of options is a major win for Bitcoin ETFs, as it will bring deeper liquidity and attract "bigger fish."

Author: Mensh, ChainCatcher

Editor: Nianqing, ChainCatcher

On October 18, the U.S. Securities and Exchange Commission (SEC) approved applications from the New York Stock Exchange (NYSE) and the Chicago Board Options Exchange (CBOE), enabling 11 approved Bitcoin ETF providers to offer options trading. Currently, Bitcoin continues to rise, with a new high surpassing $69,000.

ETF analyst Eric Balchunas said at the Permissionless conference that Bitcoin ETF options could launch before year-end; however, since neither the CFTC nor the OCC has set a strict deadline, delays are possible, making a Q1 2025 launch more likely.

Meanwhile, the SEC has delayed its decision on Bitwise and Grayscale’s Ethereum ETF options, with market speculation suggesting this is due to weaker-than-expected capital inflows following the approval of Ethereum ETFs. The SEC aims to further assess the proposal’s impact on market stability, with a ruling expected by November 10.

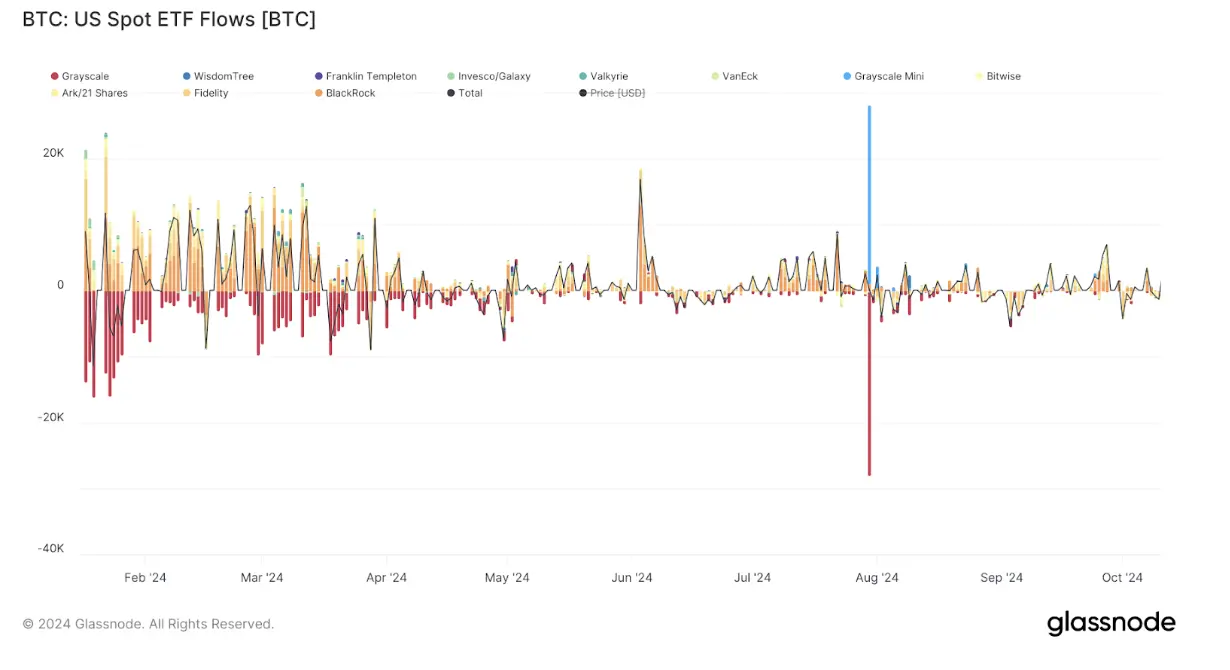

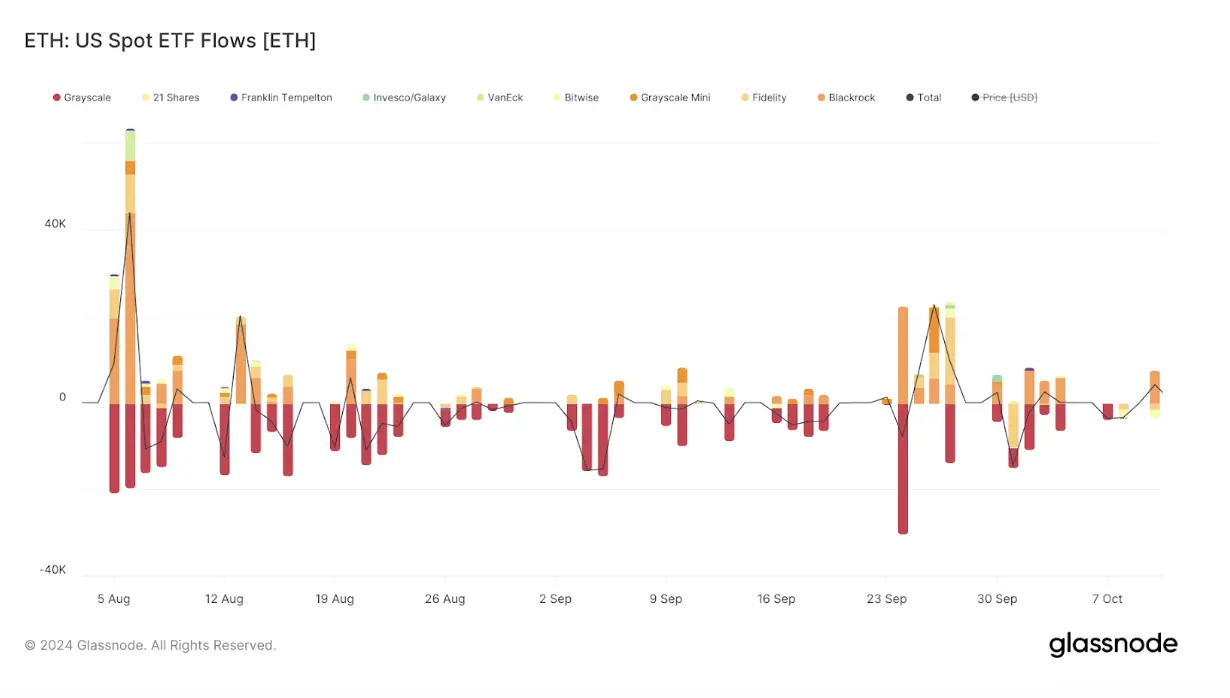

Bitcoin and Ethereum ETF Inflows/Outflows:

Why Are Bitcoin ETF Options Important?

Bitcoin options are contracts that give holders the right—but not the obligation—to buy or sell Bitcoin at a predetermined price within a specified time frame. For institutional investors, these options provide a way to hedge against price volatility or speculate on market movements without holding the underlying asset. These index-based Bitcoin options offer institutions and traders a fast, cost-effective method to increase exposure to Bitcoin, providing an alternative tool to hedge their positions in the world’s largest cryptocurrency.

Why is the approval of Bitcoin ETF options particularly significant? Although numerous crypto options products exist today, most operate without regulatory oversight, deterring institutionally compliant investors. Moreover, no product currently combines compliance with strong liquidity.

The most liquid options products are offered by Deribit, the world’s largest Bitcoin options exchange. Deribit enables 24/7/365 trading of Bitcoin and Ethereum options. Their options are European-style and settled in physical cryptocurrency. However, because only crypto assets are accepted as collateral, Deribit users cannot cross-margin between ETFs, stocks, and other traditional portfolio holdings. Additionally, Deribit is not legally recognized in many countries, including the United States. Without clearinghouse backing, counterparty risk remains unresolved.

CME's Bitcoin futures options and LedgerX—regulated by the CFTC—have very wide bid-ask spreads. Functionality is limited; for example, LedgerX lacks a margin mechanism. Every call option on LedgerX must be backed by ownership of the underlying Bitcoin, while every put option requires cash equal to the strike price, leading to high transaction costs.

Options tied to Bitcoin-related assets, such as MicroStrategy stock or BITO, suffer from large tracking errors.

The sharp rise in MSTR’s share price this year indirectly reflects existing market demand for Bitcoin hedging instruments. What Bitcoin ETF options bring to the table is exactly what’s missing: compliant, deep, and liquid options products. Bloomberg researcher Jeff Park noted: "With Bitcoin options, investors can now conduct term-based portfolio allocation, especially for long-term investments."

Increase or Reduce Volatility?

There is ongoing debate over whether the listing of Bitcoin ETF options will increase or reduce Bitcoin’s volatility.

Those who believe volatility may increase argue that once listed, retail participation in ultra-short-dated options could trigger gamma squeezes similar to those seen with meme stocks like GME and AMC. A gamma squeeze occurs when accelerating price moves force market makers—the counterparties to options—to continuously hedge their positions by buying more shares, pushing prices even higher and fueling further demand for call options.

However, Bitcoin has a fixed supply of only 21 million coins. Its absolute scarcity means that if IBIT experiences a gamma squeeze, the only potential sellers would be those already owning Bitcoin and willing to trade it for higher dollar amounts. Since everyone knows no additional Bitcoin will enter circulation to suppress prices, these holders are less likely to sell. Furthermore, no existing listed options product has exhibited gamma squeeze behavior, suggesting such concerns may be overstated.

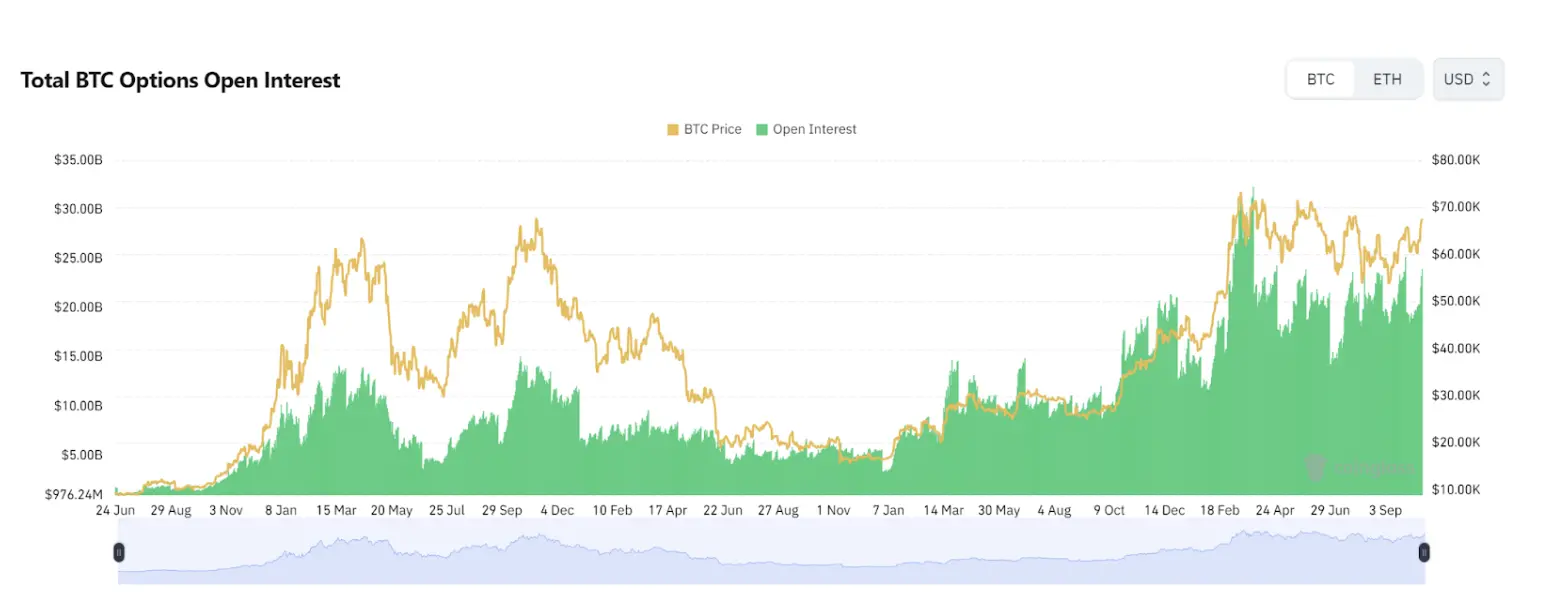

Concentrated option expirations can also cause short-term market fluctuations. Luuk Strijers, CEO of Deribit, noted that the September expiry saw the second-largest open interest in Bitcoin options in history, with approximately $58 billion in open contracts currently on Deribit. He believes over $5.8 billion worth of options could expire worthless, potentially triggering notable market volatility post-expiry.

https://www.coinglass.com/options

Historically, option expiries do affect market volatility. As expiry dates approach, traders decide whether to exercise options, let them expire, or adjust positions, often increasing trading activity as they hedge bets or exploit potential price shifts. In particular, if Bitcoin’s price is near the strike price at expiry, option holders may exercise, creating substantial buy/sell pressure. This pressure can lead to price swings immediately after expiry.

On the other hand, proponents of reduced volatility tend to take a longer-term view. Option prices reflect implied volatility—investors’ expectations of future price swings. IBIT introduces new liquidity and could spur more structured note issuances, potentially lowering realized volatility. If implied volatility rises too high, increased options issuance could naturally flatten it out.

Larger Pools Attract Bigger Fish

The introduction of options will further attract liquidity, and the resulting trading convenience will, in turn, draw even more liquidity—creating a virtuous cycle. Market consensus nearly universally agrees that options listings enhance liquidity both directly and through secondary effects.

As options market makers engage in dynamic hedging strategies, they generate additional liquidity for the underlying asset. Their continuous buying and selling provides steady trading volume, smoothing price swings and boosting overall market depth. This allows larger pools of capital to enter the market while reducing slippage.

The launch of IBIT options could also attract more institutional investors, particularly those managing large portfolios, who typically require sophisticated tools to hedge exposures. This capability lowers perceived risk barriers, enabling greater capital inflows.

Many institutional investors manage massive portfolios with precise requirements for risk management, purchasing power, and leverage. Spot ETFs alone cannot meet these needs. Options enable highly complex structured products, opening the door for significantly more institutional capital into Bitcoin.

With the approval of IBIT options, investors gain access to bet directly on Bitcoin’s volatility. Given Bitcoin’s inherently higher volatility compared to other assets, this could yield substantial returns.

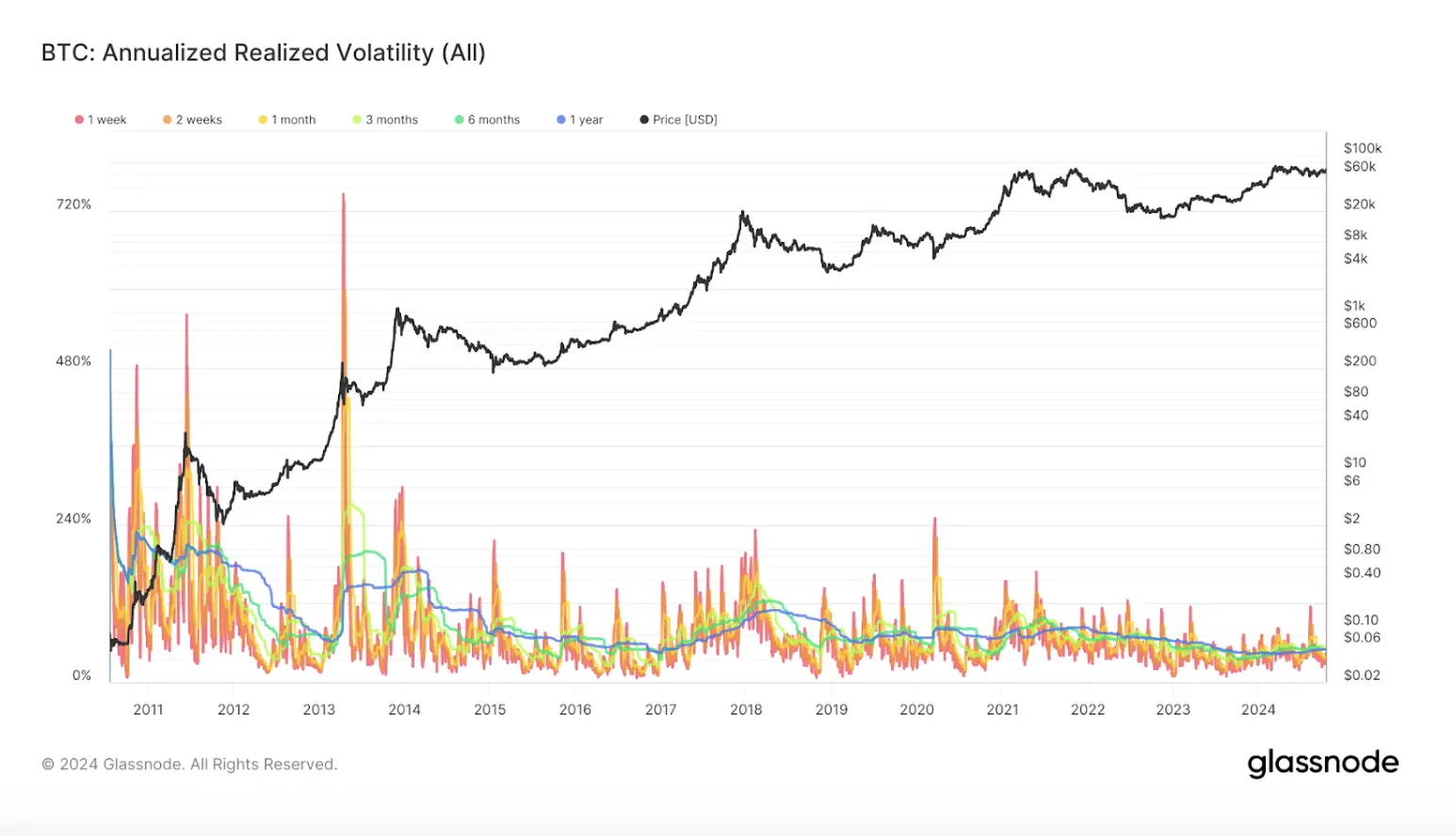

Bitcoin Annual Realized Volatility:

Bloomberg analyst Eric Balchunas pointed out that the approval of options is a major win for Bitcoin ETFs, as it brings deeper liquidity and attracts “bigger fish.”

Additionally, the approval of IBIT options marks another clear signal from regulators. Galaxy Digital CEO Mike Novogratz stated in a CNBC interview: “Unlike traditional Bitcoin futures ETFs, these options allow trading within specific time intervals, which may spark greater investor interest due to Bitcoin’s inherent volatility. The approval of ETF options could attract more investors. MicroStrategy’s trading volume reflects strong demand for Bitcoin. Regulatory clarity may pave the way for future growth in digital assets.”

For existing options markets, the approval of ETF-based options will also create positive spillovers. On Unchained’s podcast, Arbelos Markets co-founder Joshua Lim speculated that CME options would see the most noticeable liquidity gains, as both serve traditional investors. Arbitrage opportunities between the two markets would boost liquidity in both.

Altered Price Behavior

The introduction of options not only expands investors’ strategic toolkit but also leads to previously unforeseen price dynamics.

For instance, Joshua Lim observed that many traders are buying bullish options positioned after the U.S. election, indicating a hedging bet that crypto regulations may ease following November 5. Typically, some price movement clusters around such expiry dates. If many investors buy call options with a $65,000 strike price, market makers hedging their exposure tend to buy Bitcoin when the price is below $65,000 and sell when it exceeds that level, effectively pinning the price near the strike.

Trends may also be delayed until after option expiry for various reasons. Options usually expire on the last Friday of the month, which doesn’t always align with calendar-month ends—important dates for hedge fund performance evaluations and share redemptions that drive capital flows and buying pressure. Due to all these dynamics, spot markets often experience volatility post-expiry, as hedging activities by traders may unwind or diminish after settlement.

Options don’t trade over weekends. If IBIT has extremely high gamma at Friday’s close, market makers may be forced to purchase spot Bitcoin over the weekend to hedge delta exposure. Given that IBIT is cash-redeemable, transferring Bitcoin into IBIT involves certain risks. All these factors could spill over into the broader Bitcoin market, potentially widening bid-ask spreads.

Conclusion

For institutions, Bitcoin ETF options greatly expand hedging capabilities, allowing more precise control over risk and return, and enabling more diversified portfolios. For retail investors, Bitcoin ETF options offer a way to gain exposure to Bitcoin’s volatility. The versatility of options may also fuel bullish sentiment through classic market reflexivity—liquidity attracting more liquidity. However, whether these options will successfully draw sufficient capital, achieve robust liquidity, and establish a self-reinforcing cycle remains to be proven by market dynamics.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News