Looking back at the evolution of UNI's versions, how has UNI influenced blockchain?

TechFlow Selected TechFlow Selected

Looking back at the evolution of UNI's versions, how has UNI influenced blockchain?

From V1 to V4, from UNI X to UNI Chain, how far is UNI from the ultimate answer for a DEX?

Author: Zeke, Researcher at YBB Capital

Introduction

For Web3, I believe there are three pivotal historical moments: Bitcoin pioneering decentralized blockchain systems; Ethereum’s smart contracts expanding blockchains beyond payments; and UNI democratizing financial privileges, heralding the golden age of blockchain. From V1 to V4, from UNI X to UNI Chain, how far is UNI from becoming the ultimate answer for decentralized exchanges (Dex)?

UNI V1: Prelude to the Golden Age

Prior to UNI, on-chain exchanges already existed—but only after UNI did they truly become known as decentralized exchanges (Dex). Many articles attribute UNI's success to simplicity, security, privacy, and being a pioneer of Automated Market Makers (AMM). In my view, however, aside from simplicity, most of these factors had little actual impact. Contrary to popular belief today, UNI was not the first on-chain exchange to adopt the AMM model. Before UNI, there was Bancor—the second-largest ICO in blockchain history—and order book-based on-chain exchanges had also long existed. UNI was neither the pioneer nor the only platform capable of offering secure and private on-chain trading. So why did UNI succeed where others didn’t? Let's examine Bancor, which predated UNI and once stood as a top-tier on-chain exchange. Bancor provided the algorithmic foundation for early phenomena like EOS RAM and IBO (the "B" stands for Bancor Protocol), and pioneered the Constant Product Market Maker (CPMM) model now widely used. As for why Bancor ultimately lost ground to UNI, theories abound: U.S. regulatory issues, inferior user experience compared to UNI, or deeper technical flaws in its algorithm and protocol design. While we won't delve into all those here, in my view, UNI’s rise boils down to one simple reason: it was the first Dex project that truly fulfilled the definition of DeFi.

The AMM model was the only way at the time to democratize market making and token issuance. Order-book models—whether fully on-chain or hybrid on-chain/off-chain—could never allow users to freely list tokens. Nor could ordinary users participate in liquidity provision to earn returns. This led to chronic problems such as limited trading pairs and slow trade execution. Even though Bancor used the same AMM model, it failed due to rigid liquidity mechanisms and centralized control: new token listings required approval from the Bancor team and payment of listing fees. At its core, Bancor still operated around the interests of a central entity, failing to truly return “privileges” to users.

In truth, UNI’s initial version wasn’t particularly user-friendly. It suffered from extreme short-term price volatility—one inherent flaw of CPMM—where large transactions could temporarily manipulate token prices. Swaps between ERC20 tokens couldn’t happen directly, leading to slippage. Gas costs were high, there was no slippage protection, and advanced features were missing. While AMM solved the liquidity shortage and slow matching issues plaguing order-book DEXs at the time, it still couldn’t compete with centralized exchanges (Cex). Early adoption of V1 was limited, yet its significance was historic: it marked the first real manifestation of financial democratization within a Dex—a platform with no listing barriers, where liquidity came from the people. Thanks to UNI, meme tokens can flourish today, and projects without elite teams can thrive on-chain. Privileges once reserved for major financial institutions now exist across the blockchain ecosystem.

UNI V2: DeFi Summer

UNI V2 launched in May 2020. At the time, despite what it would later become—a "DeFi giant"—its TVL was under $40 million. V2 focused on addressing key weaknesses of V1, including short-term price manipulation and the need to route trades through ETH. It also introduced flash swaps to enhance usability. The most notable innovation in V2 was its approach to mitigating price manipulation. UNI implemented an end-of-block pricing mechanism, using the last traded price in each block as the official price. For an attacker to manipulate this, they’d have to execute a trade at the end of one block and complete arbitrage in the next—requiring selfish mining (withholding blocks from the network) and successfully mining two consecutive blocks. Otherwise, other arbitrageurs would correct the price. This made attacks extremely difficult and costly in practice.

Another major addition was Time-Weighted Average Price (TWAP). Unlike a simple average of recent block prices, TWAP weights each price by how long it persisted. For example:

● Block 1: Price 10, duration 15 seconds

● Block 2: Price 12, duration 17 seconds

● Block 3: Price 11, duration 16 seconds

The cumulative value at the end of Block 3 would be: 10 × 15 + 12 × 17 + 11 × 16 = 488. The TWAP over these three blocks is then 488 / (15 + 17 + 16) ≈ 11.11. By weighting based on duration, brief price spikes have minimal impact on the final TWAP. Attackers must sustain manipulated prices over longer periods, significantly increasing cost and difficulty.

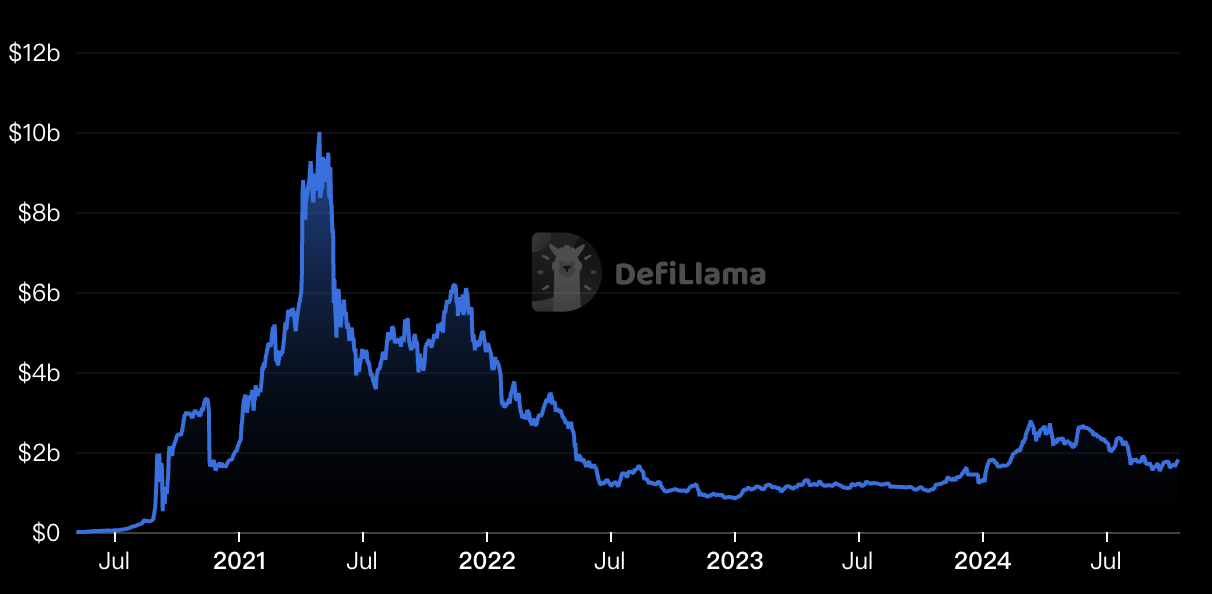

This approach served as an early and effective defense against MEV (Maximal Extractable Value), enhancing AMM safety and reliability. Gradually, UNI became the dominant choice among on-chain Dex platforms. Beyond internal improvements, external factors also played a role in UNI’s rise—some luck involved. A pivotal event in June 2020 sparked what we now call “DeFi Summer,” officially launching blockchain’s golden era. It began when lending platform Compound Finance started distributing COMP tokens to both lenders and borrowers. Other projects followed suit, creating layered investment opportunities known as “yield farming” or “liquidity mining” (today’s “Points” are essentially a rogue variant of liquidity mining). As a low-barrier-to-entry Dex where anyone could add liquidity, UNI naturally became the go-to platform for launching altcoin mining initiatives. The rush resembled the California Gold Rush of the mid-19th century—“gold miners” flooded in, pouring massive liquidity into UNI and cementing its position at the top of DeFi (UNI V2 reached a TVL peak exceeding $10 billion on April 29, 2021). From then on, DeFi gained widespread recognition, and blockchain entered the mainstream.

UNI V3: The Long Road Toward Challenging Cex

By the time of V2, UNI had already become the standard-bearer for AMM-based Dex platforms. Nearly 99% of similar projects during that era mirrored UNI’s core architecture. By then, UNI’s true rival may no longer have been other Dexs, but rather centralized exchanges (Cex). Compared to the efficiency of Cex, AMMs suffer from low capital efficiency. For average users, providing liquidity to non-stablecoin pairs carries significant impermanent loss risk. During the 2020–2021 DeFi Summer, many chased yield farming rewards only to lose their entire principal. To profit safely from liquidity provision (LP), the best option was stablecoin pairs like DAI-USDC, meaning much of the TVL represented capital with limited utility. Moreover, V2 distributed liquidity uniformly across the entire 0 to ∞ price range—even over ranges where no trading occurred—resulting in inefficient capital use.

To address this, V3 introduced Concentrated Liquidity. Unlike V2’s uniform distribution, V3 allows LPs to allocate funds within custom price ranges. Liquidity is only active within these specified bounds, enabling LPs to achieve the same depth with less capital—or greater depth with the same amount. This proved especially beneficial for stablecoin pairs trading within narrow bands.

However, real-world results fell short of expectations. Most LPs tend to concentrate liquidity in anticipated high-volatility zones, causing capital congestion in certain ranges while leaving others undercapitalized. Although individual LPs saw improved capital efficiency, overall distribution remained uneven—meaning systemic inefficiencies from V2 weren’t substantially resolved. In terms of liquidity efficiency, solutions like Trader Joe’s price bins outperformed UNI V3; for stablecoin trading optimization, Curve remained superior. Meanwhile, with Layer2 rollups emerging, order-book-based Dexs were poised to reclaim dominance. At this point, UNI hadn’t achieved its dream of surpassing Cex—it instead faced an awkward “midlife crisis.”

UNI V4: The Era of Hooks

UNI V4 arrived two years after V3—an update analyzed in greater detail in our previous reports. Here, I’ll summarize briefly. Compared to V3, V4 emphasizes customization and efficiency. While V3 improved capital utilization via concentrated liquidity, it required LPs to precisely define price ranges—a limitation that could lead to insufficient liquidity during extreme market moves. Solutions like Curve and Trader Joe offered better alternatives.

V4 strikes a balance between customization and efficiency, aiming to surpass prior models in precision and capital use. Its most important feature is the introduction of Hooks (essentially smart contracts), granting developers unprecedented flexibility. They can insert custom logic at critical points in a pool’s lifecycle—before/after trades, or during deposit/withdrawal events. This enables highly customized pools supporting features like Time-Weighted Average Market Makers (TWAMM), dynamic fees, on-chain limit orders, and integration with lending protocols.

Additionally, V4 replaced the long-standing Factory-Pool architecture with a Singleton structure, consolidating all liquidity pools into a single contract. This drastically reduces gas costs for creating pools and cross-pool trading—by up to 99%—and introduces a “Flash Accounting” system for further gas optimization. Launched near the end of the 2023 bear market, V4 helped UNI regain competitive footing amid growing challenges in the AMM space. However, V4’s high degree of customization brings trade-offs. Developers need stronger technical expertise to leverage Hooks effectively, and poor implementation risks introducing security vulnerabilities. Furthermore, highly fragmented, customized pools could exacerbate market fragmentation and reduce aggregate liquidity. Overall, V4 represents a crucial direction for DeFi evolution: highly customizable, efficient automated market-making services.

UNI Chain: Striving for Peak Efficiency

UNI Chain is a recently announced major upgrade, signaling a potential future where Dexs evolve into full-fledged blockchains (though curiously, UNI Chain is not an appchain). Built on Optimism’s OP Stack, its primary goal is to boost transaction speed and security, ultimately capturing protocol value to benefit UNI token holders. Its innovations center on three pillars:

Verifiable Block Building: Leveraging Rollup-Boost technology developed with Flashbots, combined with Trusted Execution Environments (TEE) and Flashblocks, enabling fast, secure, and verifiable block construction—reducing MEV risks, accelerating transactions, and offering rollback protection;

UNIchain Validation Network (UVN): Incentivizes validators to stake UNI tokens for block verification, mitigating centralization risks associated with single sequencers and enhancing network security;

Intent-Centric Interaction Model (ERC-7683): Simplifies user experience by automatically selecting optimal cross-chain routes, solving liquidity fragmentation and complex inter-chain interactions, while remaining compatible with both OP Stack and non-OP Stack chains;

In short: MEV resistance, decentralized sequencing, and intent-driven UX. UNI joining the ranks of superchains will undoubtedly strengthen the OP alliance. Yet in the short term, this poses a challenge for Ethereum—especially as a core protocol (accounting for 50% of Ethereum’s transaction fees) begins to drift away, further fragmenting an already divided ecosystem. Long-term, however, this could serve as a crucial test of Ethereum’s rent-seeking economic model.

Conclusion

Today, as infrastructure increasingly exceeds the performance needs of DeFi applications, more and more Dexs are shifting toward order-book models. No matter how simple AMM becomes, it cannot match the raw performance of order books. And in terms of capital efficiency, AMM will never surpass them. Will AMM eventually disappear? Some argue AMM is merely a product of a specific era. But I believe AMM has become a totem of Web3. As long as memes exist, AMM will persist. As long as bottom-up demand remains, AMM will endure. One day, we might see UNI surpassed—or even adopt an order-book model itself—but I believe this totem will remain forever preserved.

On another note, UNI itself is increasingly trending toward centralization—governance dominated by a16z wielding veto power, and front-end fee collection implemented without community notice. We must acknowledge that Web3’s development path often conflicts with human nature and reality. How should we coexist with these suddenly massive entities? That is a question we all must confront.

References

2.Re-examining the Bancor Algorithm: Why cw Is a Flawed Design

4.Uniswap: From Zero to Infinity

5.YBB Capital: Moving Beyond Fork Swaps – Is Uniswap V4 Entering the 'Era of Hooks'?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News