What is PayFi, and why Solana for PayFi?

TechFlow Selected TechFlow Selected

What is PayFi, and why Solana for PayFi?

PayFi, a new innovation that integrates Web3 payments, RWA, and DeFi, can help us move toward the stars and oceans.

By: Will Awang

Elon Musk's ambition reaches for the stars and seas of space. Similarly, for the $2 trillion crypto market aiming toward mass adoption, the traditional financial market—valued at $400 to $600 trillion—is its own vast ocean of opportunity.

We can already see certain pathways emerging, such as the rise of tokenization. However, the current early-stage migration of real-world assets (RWA 1.0) onto blockchains lacks sufficient liquidity and is not sustainable in the long run. Even though DePIN could revive the IoT sector, it still fails to address the core challenges.

This is why we're turning to Web3 payments—a key driver for stablecoin mass adoption, especially in non-trading contexts. According to Visa’s stablecoin report: the total supply of stablecoins stands at approximately $170 billion, settling trillions of dollars in assets annually. Around 20 million blockchain addresses conduct stablecoin transactions each month, and over 120 million addresses hold non-zero stablecoin balances.

Web3 payments offer traditional financial networks advantages like instant settlement, 24/7 availability, and low transaction costs. But that's not enough. We should instead focus on PayFi—an innovative application that unlocks an entirely new financial market. PayFi, integrating Web3 payments, RWA, and DeFi, can help us navigate this vast new frontier.

Therefore, this article will first define PayFi and explore its relationship with Web3 payments, DeFi, and RWA. Then, we’ll examine how Solana—the chain that introduced PayFi—is progressively building its PayFi ecosystem.

1. What is PayFi?

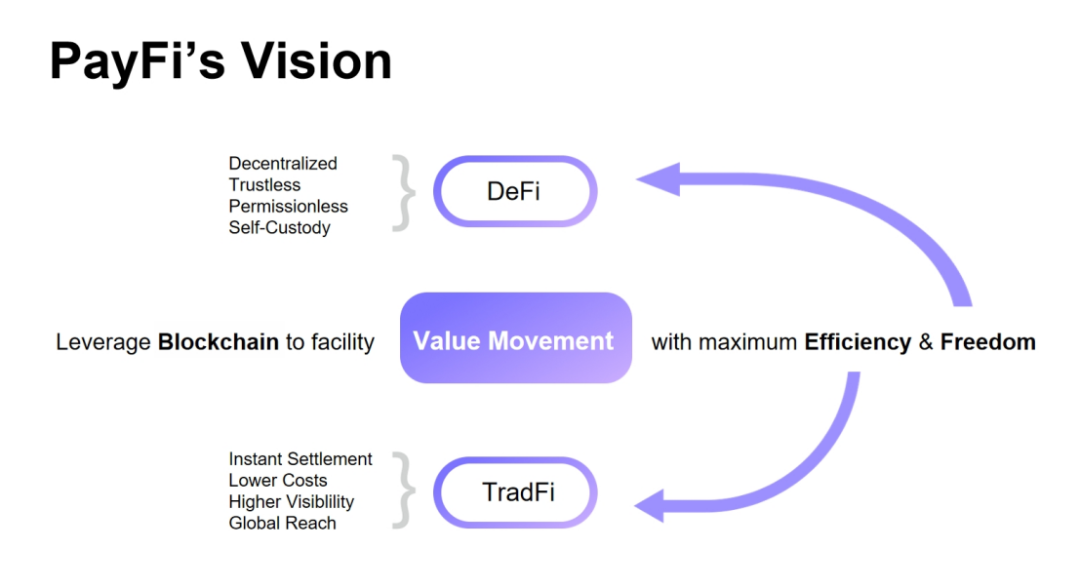

PayFi, or Payment Finance, refers to an innovative application model that combines payment functionality with financial services using blockchain and smart contract technologies. At its core, PayFi leverages blockchain as a settlement layer, merging the strengths of Web3 payments and decentralized finance (DeFi) to enable efficient and unrestricted value movement.

The goal of PayFi is to realize the vision outlined in the Bitcoin whitepaper: creating a peer-to-peer electronic cash system without trusted third parties, while fully harnessing the benefits of DeFi to form a new financial market. This includes delivering novel financial experiences, enabling complex financial products and use cases, and ultimately forming an integrated value chain.

PayFi was first proposed by Lily Liu, President of the Solana Foundation, during the 2024 Hong Kong Web3 Festival. In her view, PayFi builds a new financial market centered around the time value of money (TVM)—something difficult or impossible to achieve in traditional finance.

In this emerging PayFi market, Web3 payments surpass traditional finance not only in efficiency—offering instant settlement, reduced costs, transparency, and global reach—but also leverage DeFi to ensure decentralization, permissionless access, user-controlled assets, and personal sovereignty across a global network.

2. The Relationship Between PayFi, Web3 Payments, DeFi, and RWA

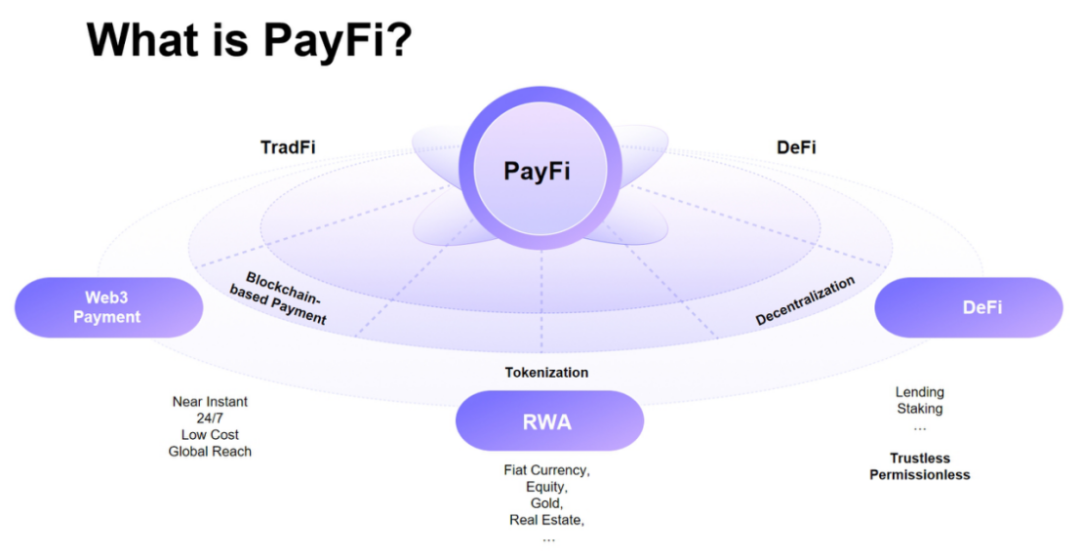

PayFi is not synonymous with Web3 payments. While Web3 payments improve upon traditional finance through blockchain technology, PayFi goes further—it builds, expands, and deepens Web3 payments by incorporating DeFi to create a new financial market.

PayFi is also not equivalent to DeFi. At its essence, payment involves real-world value exchange—goods or services traded for money. Thus, PayFi primarily revolves around the sending, receiving, and settlement of digital assets rather than the trading-centric activities dominant in DeFi. Only by seamlessly connecting Web3 payments and DeFi via blockchain and smart contracts can we develop payment-linked financial derivatives such as lending and wealth management.

PayFi is also distinct from RWA. Here, RWA has two meanings. First, asset tokenization—only when assets are tokenized and moved on-chain can seamless value transfer occur, allowing smart contracts to manage trading and settlement processes (e.g., USD-backed stablecoins).

Second, RWA fundraising—providing liquidity support for financing needs within PayFi scenarios. As Lily Liu stated: “PayFi creates a new financial market centered on the time value of money. This on-chain financial market enables new financial paradigms and product experiences unattainable in traditional finance.”

Thus, PayFi is not an isolated innovation but an integrative application combining Web3 payments, DeFi, and RWA. It encompasses not just digital asset payments and transactions, but also financial activities like lending, investment, and wealth management. Through blockchain and smart contracts, PayFi makes global financial payments faster and cheaper, significantly reducing friction and costs inherent in traditional financial services.

3. The Significance and Value of PayFi

On the surface, PayFi may seem no different from concepts like GameFi or SocialFi. However, its true significance lies in promoting the practical application of digital assets in real-world scenarios.

From a forward-looking perspective, PayFi allows Web2 entities—such as traditional financial payment companies—to adopt blockchain technology to capture larger market share and avoid missing out on this transformative wave.

Conversely, Web3 communities can use payments as a vehicle to solve pain points in traditional finance, leveraging blockchain to deliver new financial models and user experiences previously impossible.

Currently, Web3 payments remain in an early, foundational state—mostly limited to using cryptocurrencies as transactional mediums in cross-border remittances, OTC trades, or payment cards. These semi-centralized approaches struggle to integrate with the broader DeFi ecosystem and suffer from narrow use cases.

However, as PayFi evolves, this blockchain- and smart-contract-driven model of value transfer will accelerate the integration of Web3 payments and DeFi services, making digital assets more practical and efficient in both daily transactions and complex financial environments.

PayFi helps prevent the scenario where "we lived like this for thirty years until the building collapsed"—a fate threatening both traditional and crypto finance. In the future global financial landscape, PayFi will be a crucial catalyst for crypto’s mass adoption.

Raymond, co-founder of PolyFlow, offers deeper insight into PayFi: “PayFi doesn’t solve the obvious problems Web3 payments aim to fix—like cross-border transfers or lack of financial inclusion. Instead, it tackles the most fundamental issue: effectively separating transaction information flow from fund flow, establishing consensus on fund movements within a unified blockchain ledger. Only then can we boost the entire Web3 industry’s efficiency and drive true mass adoption.”

4. Why Solana for PayFi?

Lily Liu answers this question clearly: “Solana possesses three key advantages—high-performance public infrastructure, capital liquidity, and talent mobility.” These strengths form barriers competitors cannot easily overcome today.

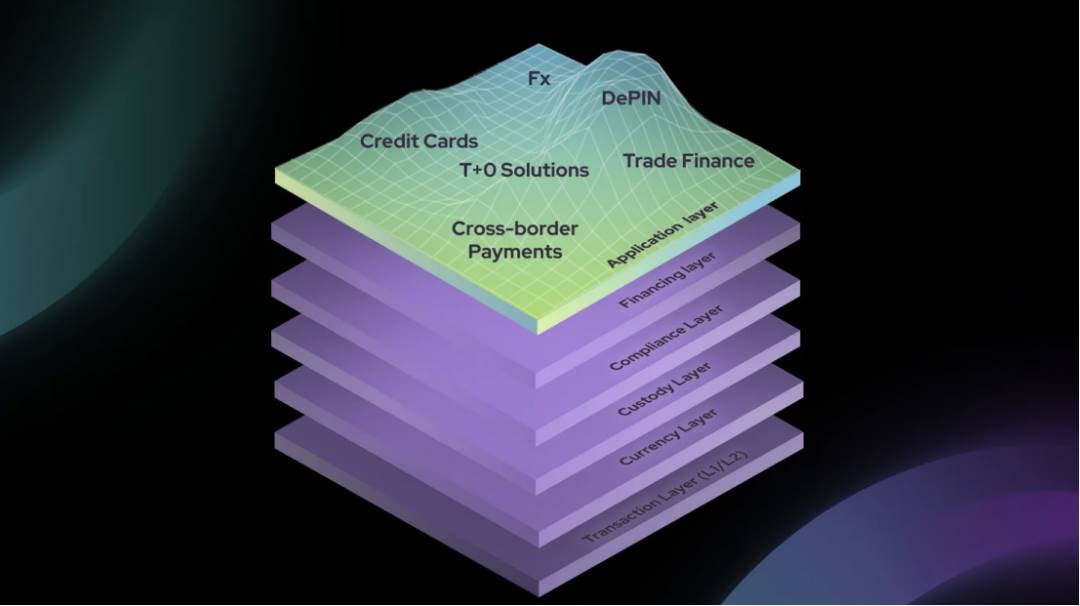

Beyond that, we can analyze it from the perspective of the PayFi stack: what kind of infrastructure does PayFi require?

4.1 Transaction Layer (Blockchain Settlement Layer)

While many blockchain settlement networks exist, Solana stands out. Its high throughput, low cost, fast settlement, and upcoming Firedancer upgrade—which promises even greater performance—enable rapid deployment of PayFi projects.

4.2 Currency Layer

Beyond efficient underlying infrastructure, robust liquidity is essential—especially in the form of stablecoins serving as on-chain transaction media. We see Solana partnering with Ondo Finance, Visa, Circle, and Stripe, along with the launch of PYUSD in June this year.

According to DefiLlama data, in August, PYUSD on Solana captured 64% of the market share, compared to Ethereum’s 36%. Since 2023, on-chain stablecoin volume on Solana has grown steadily from $1.8 billion to $3.6 billion today, including USDC, USDT, PYUSD, and USDY.

4.3 Custody Layer

Asset custody is critical in finance—both on-chain and off-chain. For blockchain-based PayFi, ensuring smart contract security, private key management, and compatibility with both traditional finance and DeFi is paramount.

On-chain custody is key to achieving personal sovereignty: Not your keys, not your coins.

4.4 Compliance Layer

It's well known that user compliance is essential for healthy growth in financial payment ecosystems. This layer fundamentally requires adherence to KYC, AML, and CTF regulations, while aligning with local jurisdictional laws.

4.5 Application Layer

Only atop these foundational layers can real-world PayFi applications thrive.

At the recent Breakpoint event in Singapore, Solana demonstrated numerous consumer-facing use cases built on its infrastructure. Its Consumer segment has evolved into a coordinated force, far exceeding other blockchains in development depth and readiness.

As noted by @ZKwifgut, payment use cases at Breakpoint included:

-

Scenarios: Online shopping, social commerce, offline events, gaming

-

Payment methods: PayPal’s PYUSD (used to buy merchandise on-site); MakerDAO bridging stablecoins to Solana via Wormhole; SOL debit card by Sanctum; Fusewallet virtual Visa card; Kast bank card;

-

Payment gateways: Using stablecoins for purchases via Shopify Blinks; accepting stablecoin payments for flight/hotel bookings via Helio Pay/Solana Pay;

-

Merchant offerings: Consumer hardware (phones, SIM cards, watches), event tickets, merchandise, e-commerce goods (integrated with Shopify), in-game items;

-

Payment hardware: Second-gen Solana phone “Seeker”; Showtime smartwatch.

Solana is also actively expanding into B2B markets, providing liquidity support via RWA fundraising for cross-border trade and supply chain finance.

While Ethereum remains positioned as an “asset chain,” Solana is solidifying its role as a “payment chain”—currently the optimal blockchain solution for consumer retail and payment-related products and services. As @ZKwifgut put it:

“PayFi and DeFi are the two legs of Solana’s vast crypto ecosystem. Right now, no other ecosystem has such a clear strategy: using DeFi to build an on-chain economy, and PayFi to achieve mass adoption.”

(Solana Breakpoint 2024 is underway)

5. Final Thoughts

In the long term, the entire Web3 industry’s shift toward off-chain and real-world consumption is inevitable. Whether it’s “making DeFi great again” or “driving crypto toward mass adoption,” slogans frequently echoed in the market can finally find tangible realization through PayFi.

This time, the wolf has truly arrived.

Blockchain and smart contract technologies can make traditional payments faster and cheaper than ever before. While these use cases benefit traditional B2B payment providers by cutting costs and boosting efficiency—and that’s good—they don’t represent the full transformation we envision.

PayFi can genuinely bridge traditional and crypto financial markets, accelerating the integration of payments and financial services through the rise of stablecoins—not just improving efficiency, but creating an entirely new financial market. In this market, you have me, and I have you.

In the future financial ecosystem, PayFi will be a pivotal driving force.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News