Creating new markets and discovering new assets are the perpetual engines of the crypto market.

TechFlow Selected TechFlow Selected

Creating new markets and discovering new assets are the perpetual engines of the crypto market.

Your application will thrive indefinitely on a blockchain network with economic security assured—this is the most optimistic future of crypto.

Author: @long_solitude

Translation: TechFlow

Since 2016–2017, the trend of crypto entrepreneurship has continued. In each cycle, cryptocurrency gains greater visibility, more people enter the space, and potential returns gradually diminish. By now, everyone has heard of cryptocurrency.

Like any emerging industry, the most promising ideas don't require massive capital at first. But after initial excitement and astonishing returns, capital becomes more accessible and the barrier to investment ideas lowers. As long as capital flows, anyone can become a founder.

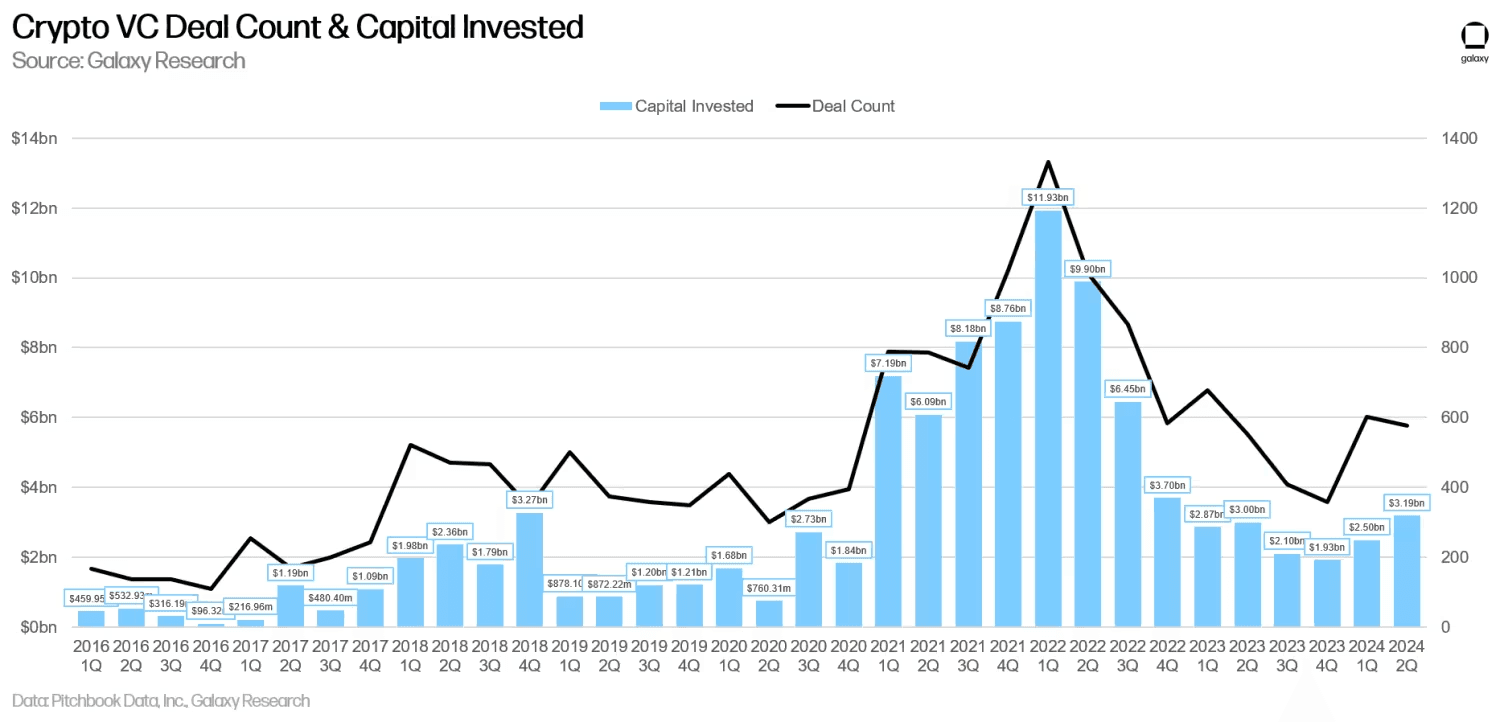

Since 2016, $100 billion in venture capital has flowed into private crypto markets, and founders have used tokens to enter nearly every possible sector. As Abraham Maslow said: "If the only tool you have is a hammer, you tend to see every problem as a nail." That torch has now passed to AI.

From finance and payments to identity, social networks, media and entertainment, gaming, cloud computing, artificial intelligence, healthcare and science, supply chains, storage, gambling, art, various types of physical infrastructure networks, even satellites in space—crypto has touched every domain. No area has been left untouched.

Today, excluding Bitcoin (BTC) and Ethereum (ETH), the circulating market cap of other altcoins stands at $700 billion, while Coinbase’s stock market cap is $40 billion. For simplicity, assume investors own 30% of the networks, ignoring unvested tokens; in Coinbase’s case, investors held about 50% at its direct listing.

This implies roughly $230 billion in liquid value available to venture capitalists (VCs). Of course, this isn’t entirely accurate—we’re not accounting for all public companies, firms that haven’t issued tokens yet, or instances where investors sold stakes at different points across cycles.

But realistically, much of that $230 billion (against $100 billion invested) has been driven by outliers like Solana and Coinbase, initial coin offerings (ICOs), and meme coins where VCs didn’t have exclusive allocations. Do the math yourself—you’ll find outlier importance in crypto is as high, if not higher, than elsewhere.

Unique Properties of Crypto

It should now be clear that cryptocurrency isn’t a panacea for all global problems. The blockchain-based distributed systems we refer to possess some very unique properties—properties that have remained largely unchanged since Ethereum’s invention.

The foundation of blockchains lies in strong financial primitives securing network safety, so it shouldn’t surprise us that sustainable use cases also gravitate toward this direction. This explains why certain categories of projects produce lasting winners while others do not.

From 2017 to 2018, billions flowed into crypto products spanning finance and consumer sectors—the only surviving ones were fundamentally financial in nature.

Now the main trend is shifting back to consumer and social domains, yet surviving products still remain limited to financial categories.

The less glamorous truth, lost in the void of CT

What are these unique properties? While not exhaustive, we believe the key ones are:

-

Permissionless capital formation, and by extension, token distribution;

-

Global consensus on a distributed ledger for financial assets.

Permissionless capital formation is crypto’s most important and universally applicable product-market fit (PMF). This is why ICOs broadly succeeded. It's why pump.fun drove a bull run across the entire Solana ecosystem and earned more in 8 months than 99% of all crypto projects combined. It's why crypto capital is funding network states and longevity experiments. The creative space is infinite, and every funded asset will be recorded on-chain, preserving provenance for its owner.

Global consensus and distributed ledgers enable open, permissionless finance. Founders have built all components of decentralized finance (DeFi)—lending, savings, trading, payments/stablecoins, and debit cards for spending. From BlackRock and major banks to VISA and Mastercard, institutions are watching crypto and DeFi features closely, seeking ways to integrate them. Perhaps one day bureaucracy itself can be outsourced at scale to global consensus.

Thus, when we hear founders complain about the Ethereum Foundation’s adversarial stance toward DeFi, we question whether they're ready to abandon what may be crypto’s second-best product-market fit (PMF)—second only to Bitcoin’s store-of-value function.

If the only thing keeping your chain alive over the past five years has been DeFi, and your best response is barely tolerating it, then you’re anti-DeFi. I'm sorry, but the default position should be wholeheartedly supporting and encouraging it.

While Vitalik argues DeFi is Ouroboros, a snake eating its own tail, we believe the opposite. DeFi might be the only positive-sum category in crypto! It creates new capital markets, enables access to credit, and facilitates consumption. Credit expansion is the fundamental force behind creating both consumption and investment. That’s why the U.S. abandoned the gold standard—and instead of collapsing, its markets rose dramatically over decades. The key to economics is maintaining circulation for growth. Why can’t DeFi be circular?

Since the market bottom in November 2022, which projects have most successfully leveraged crypto’s unique properties? Unquestionably, they’ve all focused on decentralized finance (DeFi) or capital formation:

-

Solana has appreciated 15x, consistently prioritizing DeFi. In fact, it was conceived from the start as a “decentralized Nasdaq.”

-

Pump.fun earned over $100 million in fees and generated nearly $1 billion in ecosystem value by enabling frictionless capital formation for speculative assets;

-

Ethena scaled its basis trade to tens of billions in volume;

-

Polymarket opened up new speculative markets for users;

-

Additionally, we have several centralized finance (CeFi) businesses such as Tether and Coinbase, which provide financial services and significantly increased their market share.

One of the most compelling narratives this year has been the shift toward consumer-facing crypto. We can broadly divide this into hyper-speculative games (like bonding curves, casinos, memes) and digitally ownership-driven products (like Farcaster, Zora, etc.).

We first mentioned the need for consumer applications at the end of 2022 in The Fappening, when we felt the market had become overly infrastructure-focused. Now, it seems all attention is on building consumer apps in crypto—but often without questioning what unique functionality the app actually enables.

Are mini-games on TON more enabling and durable than mundane borderless crypto payments? Probably not. Not that mini-games serve no purpose—they just fail to fully leverage crypto’s unique attributes, since high-integrity financial data isn’t essential for these games. It’s the token distribution—the core principle of crypto capital formation—that initially made them interesting.

Crypto Creates New Markets

Now that we've established crypto excels at capital formation and facilitating financial transactions, where does that lead us? To new markets.

Despite lacking ocean access compared to Genoa and Venice, Florence became a commercial superpower in medieval Europe—largely due to innovations in banking and financial instruments. The Florentine gold florin quickly became the dominant trade currency in the Western world.

Crypto’s superpower has always been assigning prices to assets that previously couldn’t be priced. In other words, creating markets where none existed before—or at least drastically improving trading experiences by providing rich liquidity in illiquid areas. Crypto acts as a coordination tool for trading in opaque and emerging domains that require deep specialization and suffer from bureaucracy and multiple layers of intermediaries.

Here are a few examples: Kettle is building a marketplace for tokenized watches, with its team actively working in New York’s diamond district handling authentication, custody, and logistics. Baxus solves similar problems for collectible wines, managing authentication and operating a central vault controlling humidity, temperature, and more. Eventually, they could replace Sotheby’s. In the physical world, many highly specialized operations are underway, and the crypto element—payment and coordination—enables earlier solutions to cold-start problems. We’ll see the physical world and crypto realm advancing each other.

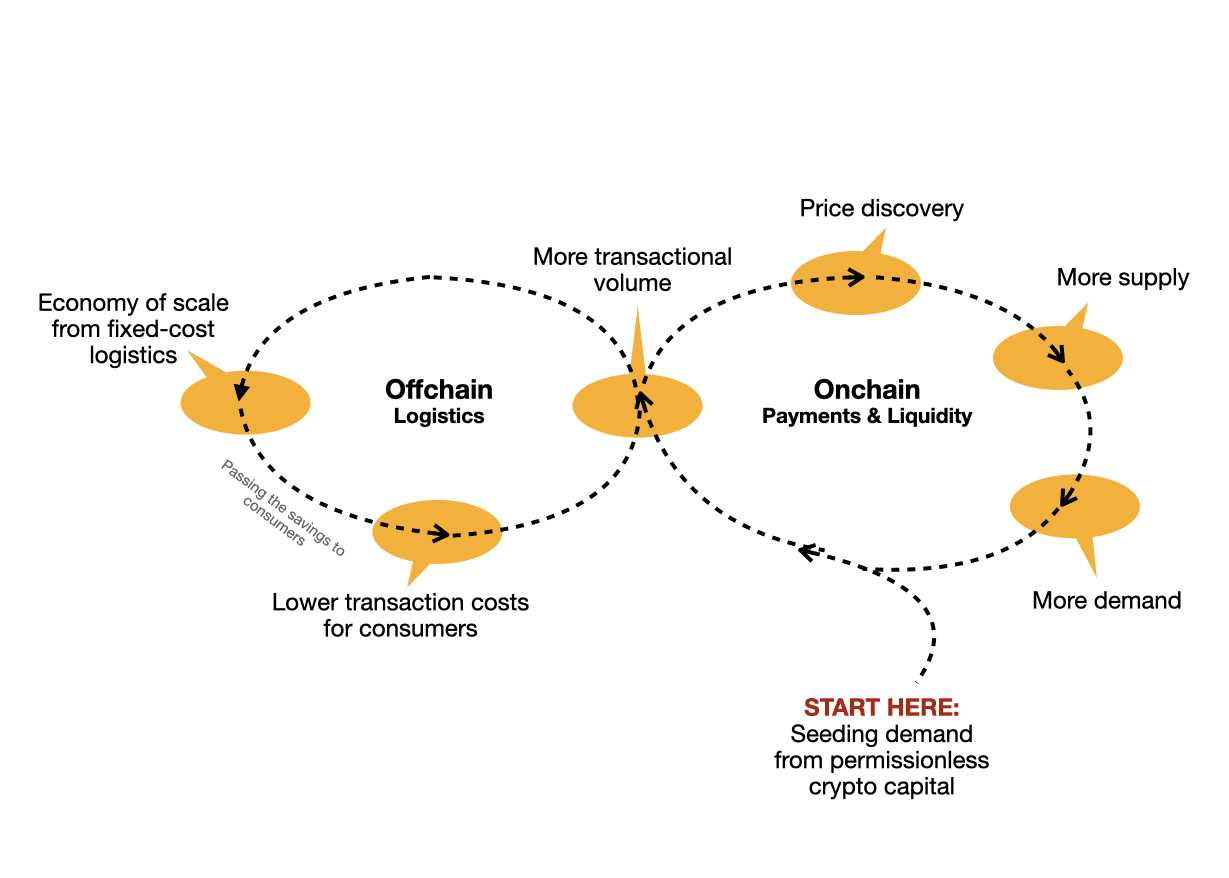

On-chain and off-chain components complement each other, as both benefit from higher transaction volumes.

Crypto enables people to pay attention to things they didn’t know existed before. Uniswap brought attention to ERC20 tokens, and Opensea highlighted NFTs.

A new favorite example of ours is SkyTrade, which allows landowners to sell or lease air rights above their properties. These air rights are tokenized as NFTs and auctioned to real estate developers and drone delivery companies like Walmart, Amazon, or future specialized aerial transport firms. Most property owners aren’t aware that a) they own air rights, and b) those rights hold value for certain parties. As the hottest form of capital, crypto can quickly prove this point.

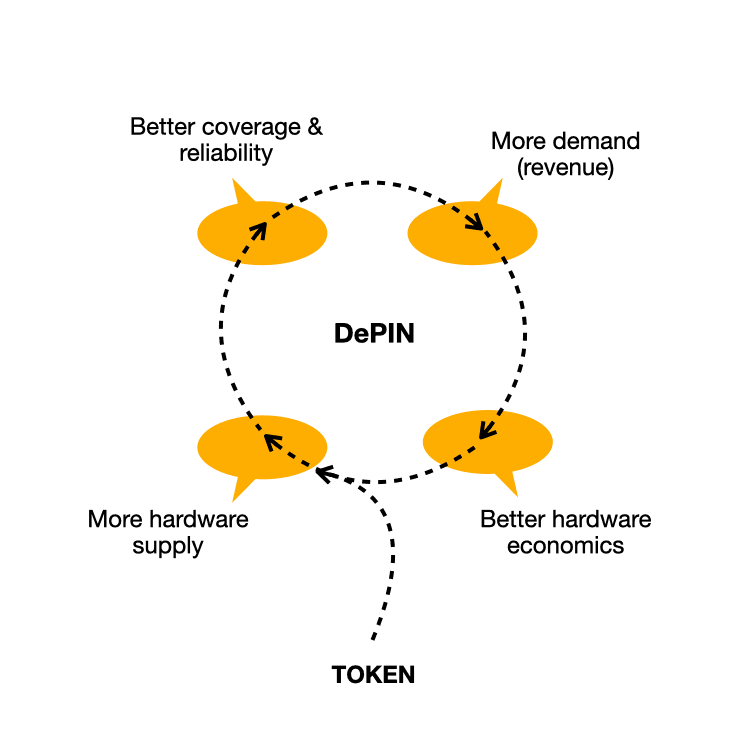

The Market for DePIN

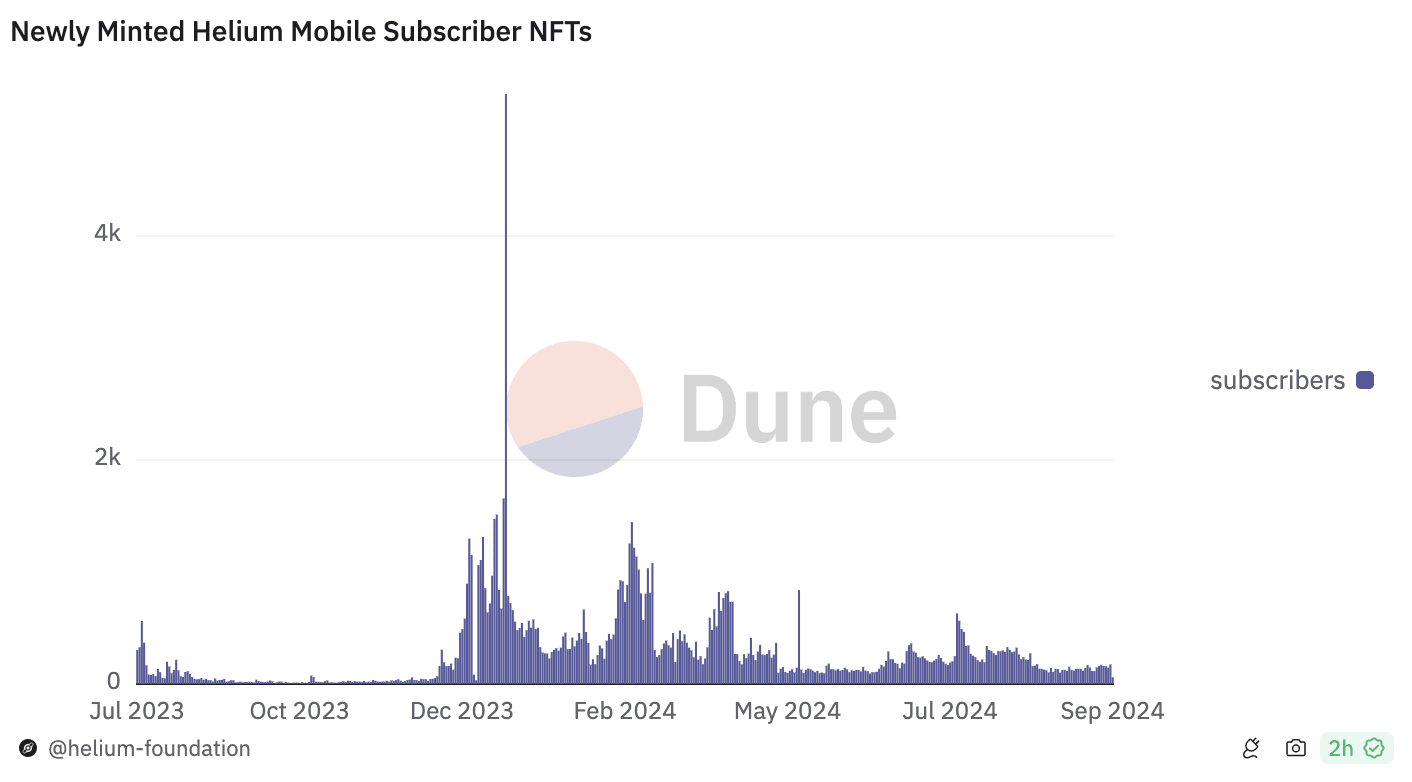

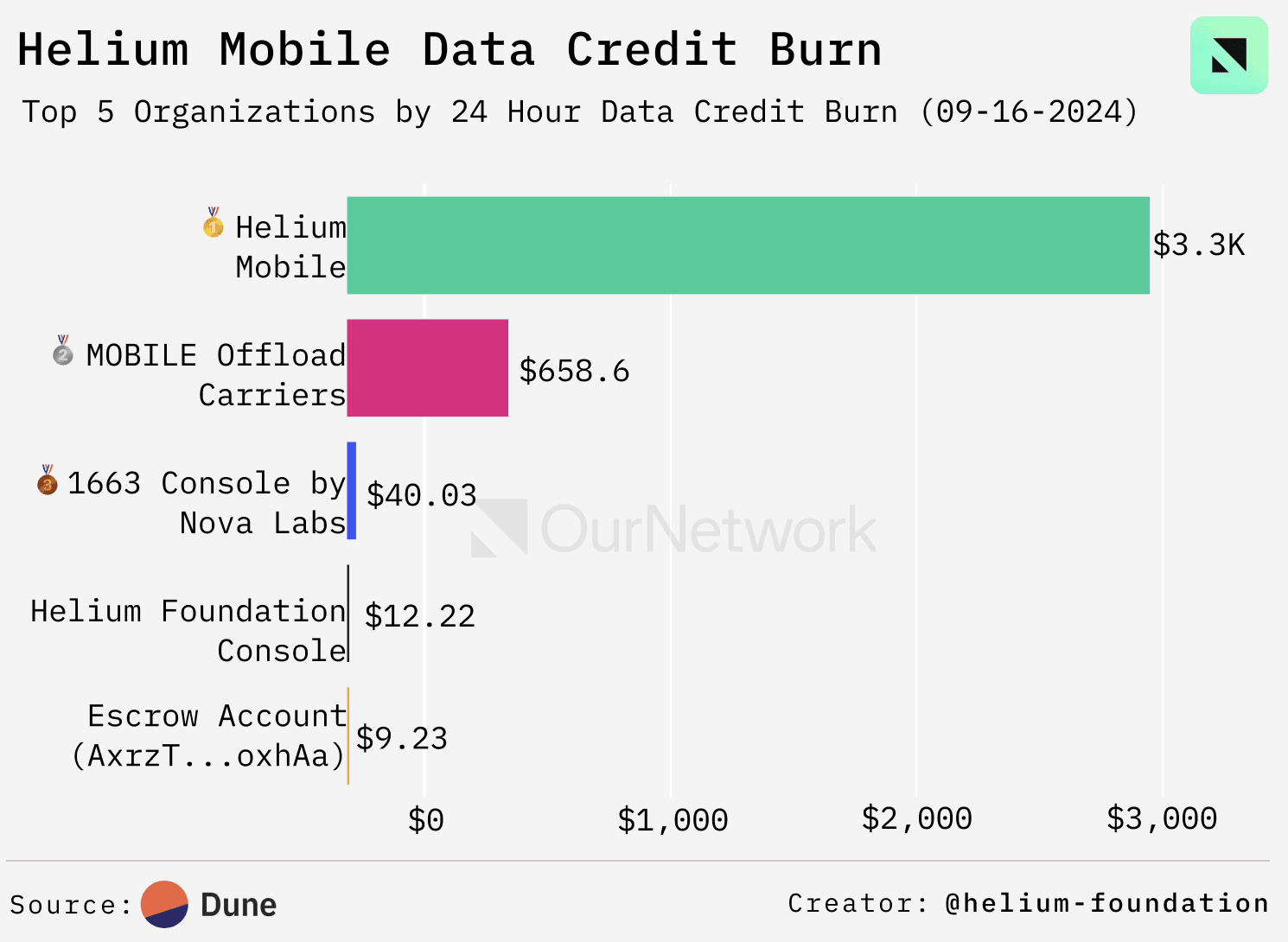

Another market segment with strong transactional characteristics is DePIN—decentralized physical infrastructure networks. The supply side typically leverages existing or idle physical hardware, making it the easier side to bootstrap in a two-sided market. Demand, however, remains unproven—we can only infer its potential based on demand for analogous centralized services.

In essence, DePIN is a marketplace for service transactions. Unfortunately, we still lack sufficient demand and transaction value to confirm product-market fit (PMF).

Source: Dune and Helium Foundation

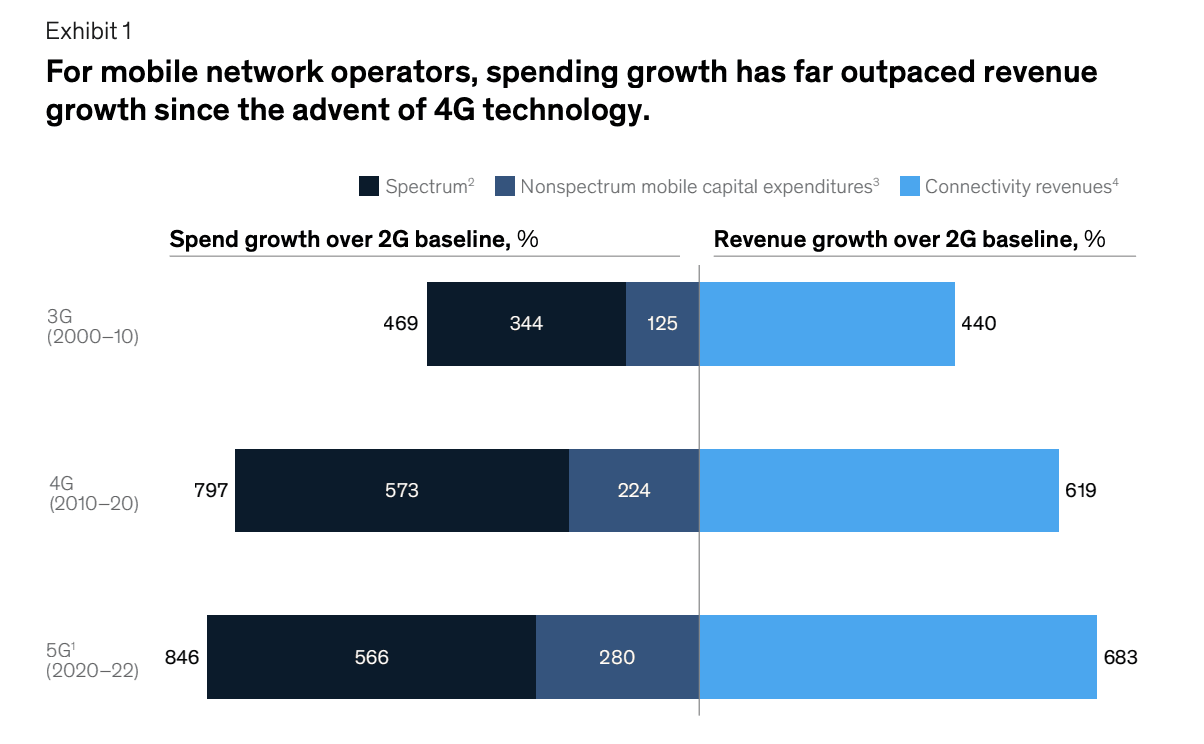

One of DePIN’s primary value propositions is shifting infrastructure investment and maintenance to decentralized networks. Centralized entities face rising costs doing this—capital expenditures (capex) grow faster than revenues. Higher spending means consumers must pay more for services. And the better the network coverage, the higher the cost, especially in rural areas where last-mile expenses grow exponentially. Without price discrimination, someone inevitably ends up subsidizing the service.

Source: "The Imperfect Present and Promising Future of DePIN: A Compound Deep Dive"

Another factor is network resilience—an excellent example being the U.S. power grid. Even the grid isn’t a single, monolithic network. No single company maintains it. Instead, it consists of numerous different utility companies (both private and municipally owned), overseen by federal and state regulators. The grid is already fragmented, precisely for resilience. And as long as affordability and resilience goals are met, while allowing infrastructure operators to earn required cost of capital, further fragmentation is feasible.

How does DePIN effectively overcome upfront hardware costs? Because capital formation allows projects to rapidly deploy and distribute tokens to hardware operators.

To be sure, relying solely on tokens isn’t enough. But it’s sufficient to get 100 genuinely interested supply-side users active, to test whether demand and revenue exist. If they do, as demand and network coverage grow, unit economics improve and reliance on token incentives decreases. Ultimately, all sustainable crypto markets will compete on a) price, and b) reliability and/or customer service—with revenue becoming the single most important metric.

Again, crypto’s role is to help markets—and by extension, DePIN—reach critical traction early through coordination of resources and payments.

Creating Markets People Want to Trade In

After multiple cycles of crypto investing, we’ve come to realize that ideation in crypto is constrained by the unique properties crypto enables—those we discussed earlier.

The permissionless nature of crypto capital is both a blessing and a curse. The design space for crypto startups seems infinite—until you realize these ideas must contain strong, explicit financial elements.

We believe the answer is clear: identify assets and markets people want to trade in, before everyone else realizes it. Such ideas always sound controversial—whether it was Helium (or earlier, Uniswap) in the last cycle, or SkyTrade today. But that’s exactly the sign you’re onto something worth pursuing.

Unfortunately, not all asset types will be traded. Again and again, we see users don’t value their data, privacy, or in-game swords. Markets around “ownership” and equitable creator compensation schemes have failed. Enough time has passed in crypto for some domains to prove ineffective, while great companies have emerged in others. Across every cycle, explicit financial elements have proven stronger than ever.

Crypto doesn’t fix economically unsound ideas—in fact, it amplifies well-known capitalist traits. More money, more trades, higher yields, and faster speed. Crypto is pushing us further down a path known and traveled since late medieval capitalism began forming.

Create new markets, discover new assets, and your application will thrive long-term on blockchain networks where economic security is ensured. This is crypto’s most optimistic future.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News