Rigidity, bubble, crisis, breaking the ice

TechFlow Selected TechFlow Selected

Rigidity, bubble, crisis, breaking the ice

ETF is merely a "slow-release ibuprofen capsule," while the trend of crypto becoming Americanized stocks has become a "tightening curse" on the industry's growth potential.

Author: YBB Capital Researcher Ac-Core

TL;DR

-

Unlike the previous bull market driven by macroeconomic prosperity, this round of crypto market is primarily affected by macroeconomic uncertainty;

-

ETFs are merely a "slow-release ibuprofen capsule," and the trend of crypto becoming more like U.S. stocks has become a "tightening headband" restricting the industry's growth potential;

-

The current bull market is almost entirely limited to Bitcoin; the main reasons for poor altcoin performance lie in overall industry innovation stagnation, insufficient liquidity, high valuations in the primary market, limited capital momentum, making it difficult for the market to sustain broad gains;

-

Under conditions of stalled industry innovation, traditional institutions such as BlackRock may bring incremental capital upon entry, but they cannot reverse the market's increasingly competitive and self-reinforcing dynamics—old tunes can't support sustained growth.

I. Can the Cyclical Rally from the Four-Year Halving Repeat Itself?

1.1 A Fundamentally Different Starting Point for This Bull Market

Perhaps coincidentally born amid a global economic crisis as resistance against sovereign currency over-issuance and monetary policy intervention, Bitcoin once saw China as a major driver before its nationwide ban in 2021. Chinese miners alone once accounted for two-thirds of global mining output. Meanwhile, China’s economy was rapidly expanding, fueled by real estate and internet booms, with favorable macroeconomic conditions and loose monetary policies stimulating investment enthusiasm prior to 2021. However, after 2020, as the real estate sector cooled and the broader economy slowed,some market liquidity began to be drained.

Looking back, DeFi Summer powered Ethereum's internal economic cycle and served as its main catalyst for growth, followed by NFTs, MEMEs, and GameFi breaking into mainstream awareness, attracting massive traffic and sparking a digital collectibles craze. The rise in market cap drove an industry-wide boom. Yet,this wave of innovation has mostly been "replaying old tunes", lacking substantive breakthroughs. Perhaps the true bull market hasn’t arrived yet, or new narratives haven’t gained enough traction.

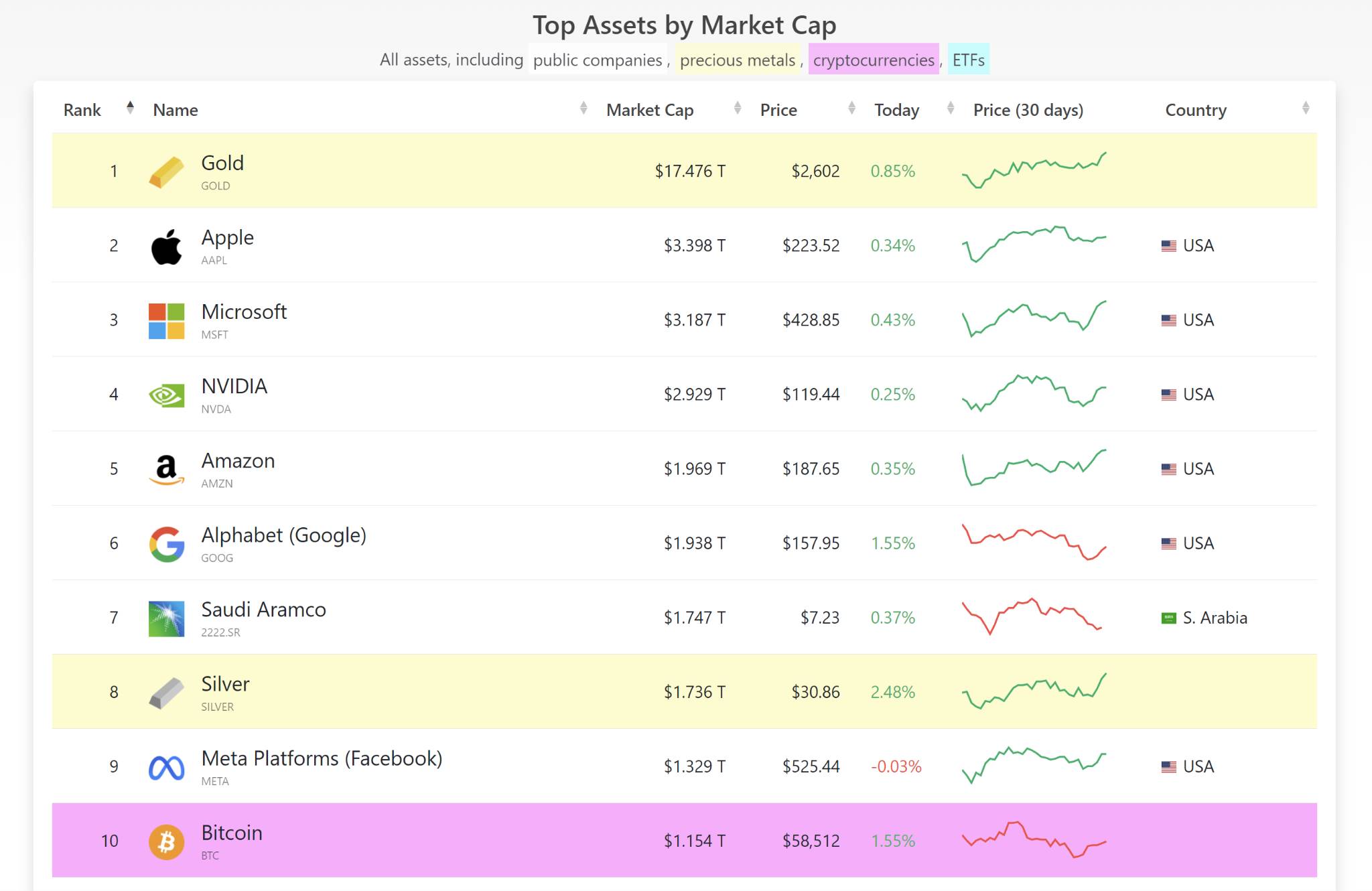

If we consider early 2019 to early 2021 as the start of the last bull run, Bitcoin traded between $4K–$10K and Ethereum between $130–$330, with the entire crypto market still relatively small and offering vast upside potential. But according to CompaniesMarketCap data, Bitcoin’s market cap now ranks 10th globally, just behind Facebook, with about three times room to grow compared to Apple and roughly 15 times compared to gold. Nevertheless, compared to the previous cycle,the expected growth space has significantly shrunk.

The Bitcoin halving narrative will be the final source of upward momentum. The cyclical growth of the crypto market has always been closely tied to macroeconomic trends. Since Bitcoin’s genesis block in 2009, its ability to surpass a $1 trillion market cap has relied heavily on periodic monetary easing. Yet, the only constant in financial markets is “change.” Even if one marks the spot on the boat, one cannot know how deep the water runs beneath.

Data Source: CompaniesMarketCap

Data Source: CompaniesMarketCap

1.2 Where Does Bitcoin Stand, and How Much Room Does It Have to Grow?

Is Bitcoin’s Safe-Haven Status Only a Consensus Within the Crypto Community?

To date, the U.S. dollar maintains control over the global economy through pricing power, while gold remains the traditional "safe haven" for hedging risk and preserving value—its historical highs consistently aligning with major crises. The first surge followed WWII and the collapse of the Bretton Woods system, decoupling the dollar from gold, driven by geopolitical tensions and inflation. The second began around 2005, when funds flooded into gold after the subprime crisis, peaking during the 2011 Libyan war, again highlighting geopolitics as a key factor. The third surge started post-2018, propelled by the pandemic and regional geopolitical conflicts. Overall, gold has remained the top choice for risk hedging, with Federal Reserve quantitative easing (expanding money supply) and geopolitical instability serving as primary drivers of price increases.

According to reports on Thursday, September 12 (Beijing time), spot gold closed up 1.84% at $2,558.07 per ounce, hitting a record high. Spot silver rose 4.19% to $29.8792 per ounce. COMEX gold futures gained 1.78%, closing at $2,587.6 per ounce, also setting a new historical record (source: Qianzhan Network Research Bulletin). Bitcoin’s positioning as a safe-haven asset alongside gold appears to have broken down—gold surged while Bitcoin failed to follow, instead tracking U.S. equities more closely.

Bitcoin’s Greatest Value: A Tool Against Economic Sanctions and Distrust in Fiat Currencies

In the context of economic globalization, countries strive to internationalize their fiat currencies for circulation, reserves, and settlement. However, the trilemma among monetary sovereignty, free capital flow, and fixed exchange rates persists. Drawing from my reading of “Currency Wars,” paper money itself holds no intrinsic value—it relies solely on national credit backing. Those who control currency issuance effectively stand above the law. Even the dominance of the U.S. dollar cannot indefinitely sustain such large-scale credit backing. Behind global economic globalization lies an irresolvable contradiction between currency globalization and national interests. For example, El Salvador adopted a “dual legal tender” system to promote nationwide Bitcoin use and reduce reliance on the dollar, while Russia has allowed residents to trade cryptocurrencies and use them for settlements since September 2024 to evade sanctions.

Bitcoin’s dilemma lies in this: its value stems from hedging against distrust in fiat currencies, yet its upward momentum depends on policies of powerful nations, adoption by monopolistic capital, and macroeconomic conditions. This dual dependency means that while Bitcoin challenges traditional finance, it remains constrained by its rules.

II. ETFs Are Just Short-Term Pain Relief, Not a Cure

2.1 The Post-ETF Era: A Failed Resistance Against Power

Image source: The Guardian-News

Image source: The Guardian-News

Bitcoin emerged coincidentally during a global economic crisis, and blockchain’s unique attributes hold potential to resist sovereign currency over-issuance and monetary policy interference. Anti-authority, pro-freedom, decentralization were once the industry’s creed. Yet, most players in the space are driven by speculation—get-rich-quick dreams seem to be the primary engine of development. While the launch of Bitcoin ETFs is positive news, it remains a one-off event that cannot sustainably support the market long-term.

Once, many of us held firm beliefs in resisting authority. Now, we pin our hopes on the very powers we once opposed. In our utopia, profit seems to matter more than direction. Markets echo with cheers over ETF approvals, everyone hoping more capital will pour in to take over our positions. Yet, those of us who once fiercely resisted authority are now gradually handing our achievements over to it. This transformation reflects a profound contradiction between ideals and reality.

BlackRock, Vanguard, State Street—these giants already dominate the world, and now BlackRock is taking control of Bitcoin.

The most influential companies in the world aren’t Apple, Tesla, Google, Amazon, or Microsoft—they’re the largest global asset managers. BlackRock is a prime example, having ranked as the world’s largest asset manager for 14 consecutive years from 2009 to 2023, managing trillions in assets. Compared to tech giants, these firms wield deeper economic influence through global capital flows.

The immediate impact of the post-ETF era is that crypto asset prices will increasingly mirror traditional financial markets. Only those holding larger positions will have greater influence in the industry. Today, the U.S. is gradually shaping crypto development through ideological control. According to QCP Capital on September 10, macroeconomic uncertainty has become the dominant force in the crypto market, with BTC’s 30-day correlation to the MSCI World Stock Index reaching 0.6—the highest level in nearly two years. This indicates Bitcoin’s price movements are increasingly influenced by global stock market performance.

While the crypto industry initially sprouted domestically, the “big players” have changed. More sophisticated competitors are emerging. Going forward, beyond selecting strong IPs and sectors, participants must also possess strong trading and execution capabilities. The Matthew effect will permeate every corner of the industry, and the crypto world is gradually approaching “Wall Street-level” trading difficulty.

2.2 The Metaphor of the Gold Rush

Recall the California Gold Rush over a century ago, when hundreds of thousands of fortune-seekers flocked from around the world, only for most to return empty-handed—or worse, losing their lives. In contrast, Levi Strauss took a different path: using surplus canvas to make durable pants sold to miners, which became wildly popular. He later refined the design, founding what would become the globally renowned Levi’s brand.

Interestingly, PoW Bitcoin mining and PoS Ethereum staking resemble this dynamic. PoW mining sent “prospectors” lugging hardware across landscapes, while PoS staking requires participants to stake their own capital. Yet, figures like “Levi Strauss” are everywhere—in this game, you dream of getting rich overnight, while I’m focused on your principal. Blockchain’s 24/7 global trading brings endless opportunities to “prospectors,” but also leads to extreme volatility—high risk with high returns, constantly testing courage and diligence.

Behind the fast-paced, non-stop, highly volatile trading lies both tempting traps and infinite opportunities—this is the greatest allure of crypto. Strong financial attributes combined with low entry barriers make crypto a natural, rich gold mine. We once cheered ETF approvals for bringing in more off-market capital, but ETFs also open doors wider for more “Levi Strausses,” creating more arbitrage and indirect profit opportunities.

More “Levi Strausses” Will Enter the Crypto Market

ETFs bring not just capital ready to “take over positions,” but also more risk-hedging and trading activity. Blockchain’s biggest innovation so far has been putting finance on-chain, creating a self-sustaining economic loop within crypto and successfully blocking direct intervention by authorities and traditional capital. However, in the post-ETF era, the crypto market is effectively surrendering its full suite of financial derivatives, attracting more arbitrageurs and large capital inflows, further compressing already limited profit margins, weakening innovation incentives, and reducing market freedom.

III. The Primary Market Struggles to Break Through

Primary Market: High FDV, Low Circulation

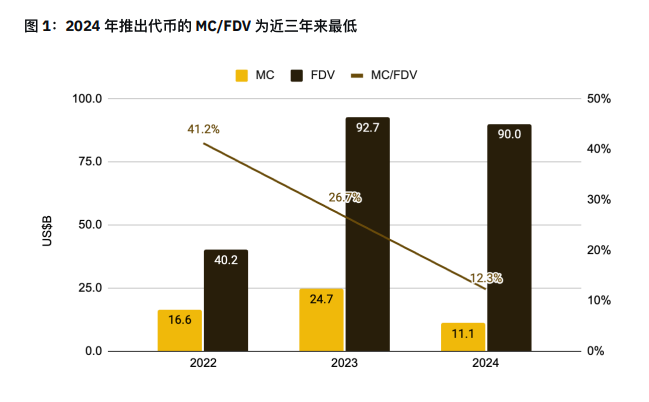

Recently, fundraising in the primary market has seen significant changes compared to the past. Newly launched tokens generally exhibit extremely high FDV (fully diluted valuation) and low liquidity. According to Binance’s report “Observations and Reflections on High Valuation, Low Circulating Tokens,” the market cap (MC) to FDV ratio for tokens launched in 2024 is the lowest in recent years. This suggests a large volume of tokens will continue to unlock, and the total FDV of tokens issued in early 2024 is already close to the full-year total of 2023.

Image source: @thedefivillain, CoinMarketCap, and Binance Research, data released April 14, 2024

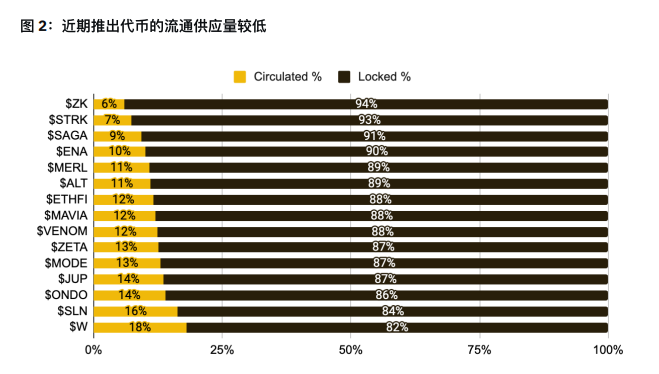

In a broadly illiquid market, tokens gradually unlock post-TGE (Token Generation Event), creating substantial selling pressure. But have VCs actually profited in this cycle? Not necessarily. Typically, compliant and regulated projects require at least a one-year cliff before token unlocks. However, when projects feature high FDV and low liquidity, post-unlock price drops (breaking below initial price) are common. That said, some smaller VCs may still profit by dumping on secondary markets or through early OTC sales. As shown in the chart below, circulating supply ratios for these tokens are generally below 20%, with the lowest at just 6%—highlighting the severity of the high-FDV phenomenon.

Image source: CoinMarketCap and Binance Research, data released May 14, 2024

Image source: CoinMarketCap and Binance Research, data released May 14, 2024

Currently, the effectiveness of capital-driven growth has clearly stalled. Beyond the above reasons, several objective factors contribute to today’s low-circulation, high-FDV market environment:

1. Fragmented Market, Too Many Predators, Not Enough Prey: During the last bull run, global capital collectively hyped DeFi and public chains. This time, however, capital and participants are too scattered, narratives are fragmented, Eastern and Western capital don’t back each other’s plays, often leaving newly launched tokens without sufficient buyers—the market is deeply divided;

2. No Altseason, Lack of Hype Momentum: EVM-based public chain infrastructure is largely mature, with capital and projects competing in the same crowded space. The so-called “Ethereum killers” have brought no real breakthroughs. Without an altcoin bull run, once a flagship project emerges, copycats flood in, intensifying the value洼effect;

3. Simplifying Simple Things, Storytelling Complex Ones: Pseudo-innovation is rampant—simple things are artificially complicated just to sell bigger dreams, essentially repackaging old ideas;

4. Matthew Effect Intensifies: After nearly 16 years of development, crypto has seen entrenched dominance form. Survivors—whether in tech, projects, or funding—are stronger than ever, while the weak fall further behind. Market话语权of leading players grows increasingly solidified;

5. Innovation and Liquidity Starved: The primary challenge facing the current market is the lack of innovation and insufficient liquidity, preventing broad-based price rallies and trapping overall development in a bottleneck.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News