This generation of crypto VCs has already started asserting their rights.

TechFlow Selected TechFlow Selected

This generation of crypto VCs has already started asserting their rights.

The market needs a "meme coin season" to rescue the trapped crypto VCs.

“These past few days I’ve been talking with some peers—this cycle’s crypto VCs are basically all dead. Fortunately, we didn’t invest much in the primary market and instead shifted to secondary.”

“I spoke with a market maker who felt sorry for us VCs. In the first year after a project launches, only market makers, the project team, and exchanges hold tokens—VCs get nothing. Yet when prices crash, it’s the VCs who take the blame and are mocked for holding ‘VC coins.’”

At a cryptocurrency event in Hong Kong, Yi Lihua, founder of LD Capital, voiced frustration on behalf of crypto VCs. In his view, VCs have become the biggest scapegoats in this market cycle—losing money and still getting blamed.

Entering 2024, multiple seasoned professionals from crypto VC firms have left their roles to join projects or move into the secondary market—the reason being simple: it’s not profitable.

Today, crypto VCs face multiple challenges: they can’t find suitable investment opportunities; the projects they do like carry sky-high valuations; existing portfolio projects struggle to exit, and the broader altcoin secondary market suffers from severe illiquidity—some investments lose 50%–90% in value immediately upon listing. Even if a VC backs a promising project, token lockups may extend for years, leaving everything uncertain by the time unlock happens…

Many crypto VCs rely on external limited partners (LPs) for funding and must maintain a “brand image,” pretending to thrive even when half-dead internally.

When projects fail to gain liquidity in the secondary market, VCs themselves become the source of exit liquidity.

This generation of crypto VCs is now on a path toward investor activism.

VC Activism Underway

“Do you know what despair feels like? It’s the day ZKX launched,” said investor DAVID, expressing deep embarrassment over having backed the project.

ZKX tokens, purchased at a $1 investment cost, plunged from an opening price of $0.60 to just $0.20 on their first day of trading—a 80% paper loss. But that wasn’t the end. The token continued falling, eventually hitting $0.000618, nearly zero.

Just months earlier, ZKX had been a well-known star project—an emerging derivatives platform built on StarkNet, backed by top-tier investors including GCR, Amber Group, Crypto.com, Hashkey, StarkWare, and OrangeDAO, raising $7.6 million in total.

On July 31, ZKX founder Eduard announced the platform would shut down due to an inability to identify a viable economic model.

All investors were blindsided, shocked by the sudden collapse.

Jin Kang, partner at Perlone Capital, lashed out on X, calling ZKX a scam.

The team shut down the project just six weeks after its token generation event (TGE); changed the token unlocking schedule unexpectedly at TGE; and circulated significantly more tokens than stated in official documentation… Jin Kang asked, “If this isn’t a scam, then what is?”

Answering Jin Kang’s call, numerous ZKX investors united to pursue collective action. To date, the维权 group has gathered 42 individuals, all actively brainstorming next steps.

Some investors recognize that under the current SAFT agreement framework, recovering funds is nearly impossible, so they’re pushing instead to pressure the Starknet Foundation to provide compensation grants to affected investors.

During the维权 process, external teams have reached out, offering to take over and relaunch the ZKX platform, providing new trading mechanisms for the existing ZKX community.

ZKX is merely one example among many ongoing VC维权 cases. One investor told TechFlow they’ve already paused new primary investments and redirected focus toward “post-investment management”—assessing the progress of existing portfolio companies. For those showing no development, they initiate维权 efforts to reclaim capital. Most of these are legacy projects invested in during 2022, including high-profile names like Coinbase Ventures, often hyped around concepts like the metaverse, which have since lost momentum and abandoned social media presence…

However,维权 is far from easy…

The Difficulty of Crypto Investor Activism

Crypto维权 is harder than scaling the heavens.

Yi Lihua, who has years of experience in crypto维权, admits he’s participated in维权 actions across multiple projects, but few have succeeded.

Primary market investing operates on the principle of “you win some, you lose some,” especially since most crypto primary investments use SAFT/SAFE agreements, with investment entities registered in offshore jurisdictions like BVI, creating legal loopholes. Investors are scattered globally, making legal recourse extremely difficult. For VCs,维权 typically means banding together with other investors to collectively pressure the project team—appealing emotionally and logically. But ultimately, control remains firmly in the hands of the project founders.

Yi Lihua notes that in most维权 cases, founders simply ignore you—you can’t do anything about it. At best, some founders, wanting to save face, might refund half the investment, which is already considered generous.

A VC partner involved in the ZKX维权 admitted that despite shared grievances, different investors have divergent interests and stakes. Some VCs didn’t invest large amounts and aren’t willing to go “all in” to fight for recovery.

Moreover, most VCs want to preserve basic dignity, so they’re reluctant to burn bridges with project teams unless absolutely necessary.

In contrast, individual investors who shed concerns about reputation and persistently push back tend to achieve higher维权 success rates. What starts as a rational appeal often devolves into a battle of “who is less ashamed and more persistent.”

It’s not just VCs—many crypto KOLs are now also pursuing维权.

Crypto professional ALEX once co-led a KOL round for a crypto project.

When ALEX approached the team requesting a refund—or else threatening coordinated FUD from KOLs—the project responded cheerfully, welcoming the negative publicity, saying it would bring attention and hype to the project.

Crypto VCs: A Vulnerable Group?

Leo Tolstoy wrote, “All happy families resemble one another; each unhappy family is unhappy in its own way.”

In crypto, successful VCs look similar; struggling VCs each lose money in their own unique way.

Based on accounts from several VC practitioners, problematic projects requiring维权 can be grouped into three main categories.

Projects like ZKX—launching with immediate price collapse followed by an official shutdown—are labeled the “Rug faction.”

The second type is the “Give-Up faction,” treating listing as the finish line, then allowing the token price to plummet through the floor. Investors haven’t even received their tokens yet, but already face paper losses exceeding 90%.

At this point, project teams often claim, “Market conditions are bad, but we’re still building.” Investors want to维权 but lack clear grounds—left helpless and heartbroken.

The third category is the “Zombie faction,” where teams go silent after fundraising, surviving bull and bear cycles without a trace—raising suspicions that they entered crypto merely to witness history unfold.

Some of these projects keep up social media activity to signal they’re alive, but in terms of narrative, operations, and technical progress, they’re functionally undead—barely breathing, indistinguishable from being dead.

Whether traditional or crypto-native, VCs follow the 80-20 rule: most projects will fail, and profitability depends on the top 20% covering costs and generating returns.

Yet in crypto, even when a VC backs a “good project,” profits aren’t guaranteed.

One VC partner recalled investing early in a game project with strong momentum. After listing on a Tier-1 exchange, however, the team suddenly demanded contract revisions—claiming exchange requirements necessitated extended token lockup periods.

Although the investment remains in the green on paper, the steady decline of altcoins has erased over 80% from its peak. With future unlocks shrouded in uncertainty, the partner lamented, “VC lockups are becoming stricter than those in A-shares or U.S. stocks.”

In July, LD Capital partner Li Xi noted, “All our portfolio projects launching this year show paper profits—but zero unlocked. Stop saying VCs are making money. The real profits go to project teams and exchanges. Except for the well-connected VCs who organize deals, most are just bagholders. This cycle’s primary market is hellishly difficult.”

Beyond changing lockup terms, some projects unilaterally raise the effective cost basis of VC-held tokens, artificially inflating their entry price. Others buy back earlier investment tranches—some at fair market value, others demanding steep discounts…

Thus, many VC practitioners see themselves as the industry’s vulnerable class. To put it pretentiously, in the four-way博弈 between projects, VCs, exchanges, and retail investors, VCs lack leverage and话语权—they’re forced into passive compliance.

To retail investors, “VC tokens” have become a derogatory term. Attitudes toward VCs have shifted from admiration to disillusionment—and even disdain.

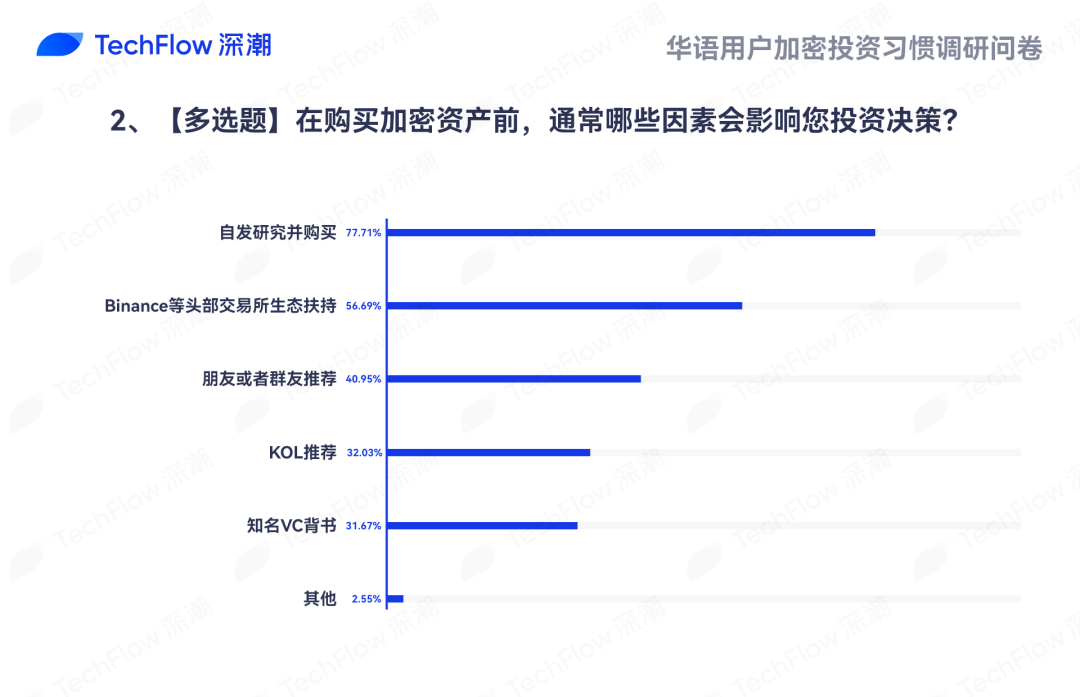

According to prior research by TechFlow, “backing by知名VCs” now influences investment decisions by only 31%—lower than recommendations from KOLs.

From the project team’s perspective, most VCs offer little unique value-added, lack independent decision-making ability, and hesitate to lead rounds. Instead, they ask, “Which other institutions have invested? If XX is in, we’ll join too.”

With primary markets facing unprecedented difficulty this year, many crypto VCs are adapting: some now deeply engage in project incubation to gain influence, evolving into “deal-scouting” VCs; others have abandoned primary investing altogether and moved into the secondary market…

But perhaps all complaints come down to one root cause: a weak market. Another major bull run could resolve most of these conflicts.

The market needs an “altseason” to rescue trapped crypto VCs.

That’d be great—if it comes. But what if it doesn’t?

Crypto markets evolve rapidly. Beyond project teams, perhaps crypto VCs must also embrace change proactively.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News