The circle of U.S. stock new issue “gods” is the largest source of alpha.

TechFlow Selected TechFlow Selected

The circle of U.S. stock new issue “gods” is the largest source of alpha.

Anyone can read the paper, but you can’t enter the circle.

Author: Kuli, TechFlow

Every time someone makes big money in U.S. equities, onlookers always do the same thing first: they dig up their latest SEC filing to find the next stock to buy.

The most scrutinized filing lately belongs to a 24-year-old German named Leopold Aschenbrenner.

In March this year, Chinese media ran a wave of reports about him, all with similar headlines—e.g., “The OpenAI-fired prodigy who wrote a 165-page paper predicting AI trends and launched a hedge fund managing $5.5 billion…”

But labels are just labels. What truly sets his fund apart is that it avoids NVIDIA, OpenAI, and any company building AI models. Instead, it invests exclusively in what AI literally cannot live without: power generation, chip manufacturing, optical communications, data centers…

As he puts it in his own paper: “AI’s bottleneck lies not in algorithms—but in electricity and compute. The entire fund is a bet on that statement being true.”

On social media, investment bloggers call him “the U.S. equity version of the Son of AI” or “AI’s Warren Buffett.” That moniker has resurfaced recently—because the scale of his accuracy is starting to border on uncanny.

According to data released by copy-trading platform Autopilot on May 1, a simulated portfolio replicating his holdings surged 61% over two months. Extrapolating from that, his fund’s assets under management are now approaching $9 billion.

Where did the money come from? Primarily from two top holdings. Bloom Energy—a fuel-cell company supplying off-grid power to AI data centers—has seen its stock rise 239% year-to-date.

Per its publicly disclosed holdings as of end-2024, he held $875 million worth of Bloom Energy stock and options—an amount now swollen to nearly $3 billion.

And Intel. The same filing shows he bought 20.2 million Intel call options in Q1 2025, when Intel’s share price hovered near $20 and Wall Street consensus widely viewed the company as struggling.

Last week, Intel hit $113—a 25-year high. In less than a year, its stock nearly quintupled. His option returns dwarf even that gain.

I understand the onlookers’ impulse. U.S. investing site Motley Fool published four deep-dive articles on his positions in a single day; Reddit’s r/investing is debating whether to copy his trades. Everyone is scouring his filings for the next Intel.

But here’s the catch: SEC filings lag by 45 days. By the time you see what he bought, half the move is already over.

More crucially—even if you knew his positions in real time, you still couldn’t replicate the reason he keeps hitting home runs.

Networks Are the Greatest Alpha

First, what feels most “supernatural” about Leopold Aschenbrenner is the AI paper he wrote at age 24—a paper that almost perfectly anticipated today’s AI development trajectory and investment themes.

Its core thesis can be distilled into one sentence: AI model training compute grows roughly half an order of magnitude annually; at that pace, Artificial General Intelligence (AGI)—with human-level capability—will emerge around 2027.

Yet sustaining that growth hinges not on algorithmic advances but on physical constraints: electricity supply, semiconductor fabrication capacity, and physical infrastructure. Power consumption per training cluster will jump from megawatt-scale to gigawatt-scale—approaching the output of a large nuclear plant.

That insight forms the bedrock of his entire fund. “AI’s pace is dictated by physical bottlenecks—so invest directly in those bottlenecks.”

This sounds like the conclusion of a brilliant mind who spent months in his study doing deep research and rigorous extrapolation. In reality, I believe it was his network that shaped this view.

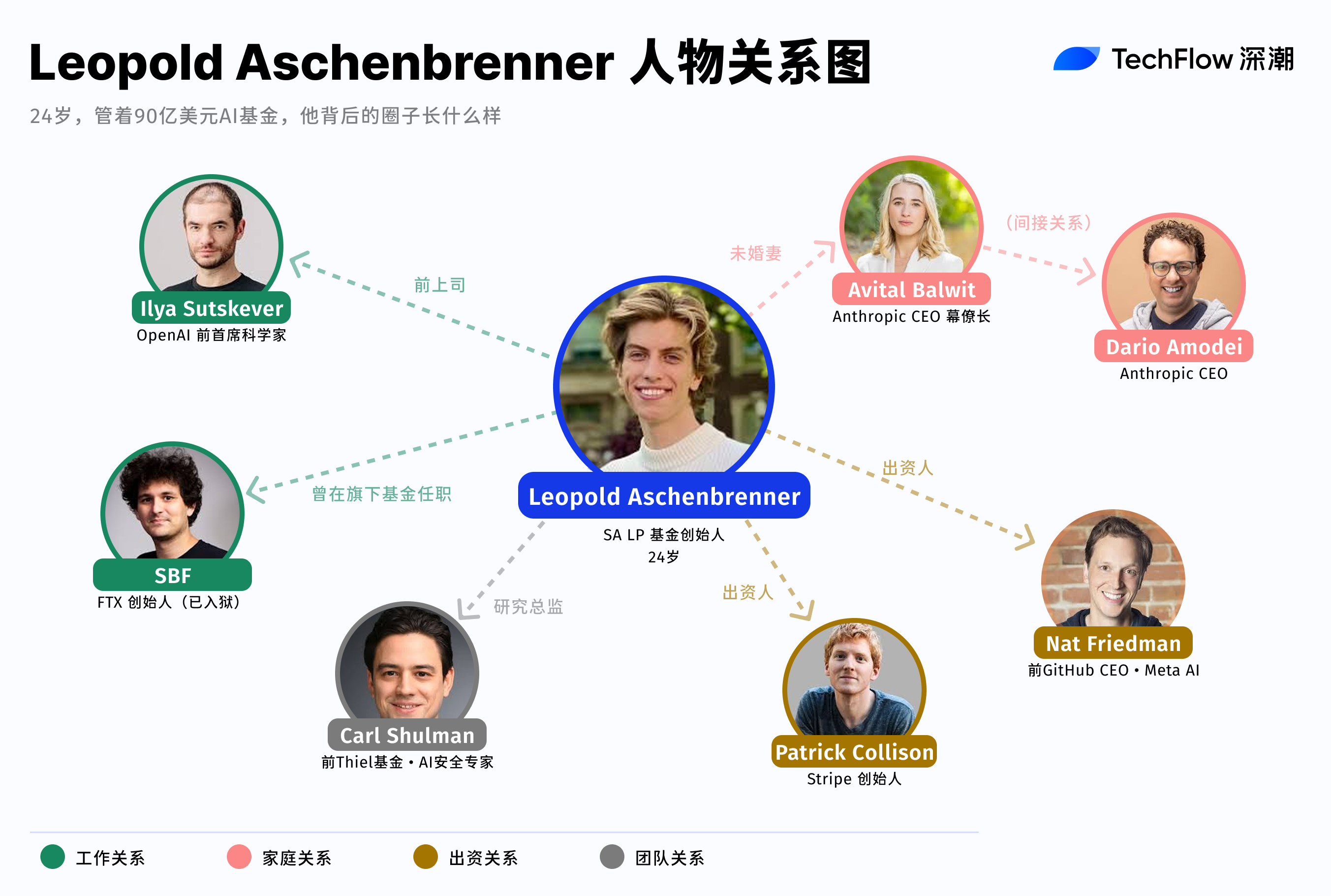

Before writing the paper, he spent a year at OpenAI’s Superalignment team—the group tasked with developing methods to control AI systems smarter than humans—and reported directly to Chief Scientist Ilya Sutskever.

During that year, he saw internal training roadmaps, actual compute consumption figures, and concrete power and chip requirements for next-generation models. When he wrote “gigawatt-scale power demand,” he likely drew from internal lab roadmaps—not abstract theory.

In April 2024, OpenAI fired him after he sent the board an internal memo warning that the company’s safety protocols were inadequate and vulnerable to infiltration by foreign intelligence agencies.

The memo triggered tensions between management and the board. OpenAI subsequently terminated him citing “information disclosure.”

Two months later, the paper was published. Less an independent academic work, it reads more like a declassified public version of his insider understanding at OpenAI.

The paper answered “where to look.” But investing requires far more than directional insight.

Many analysts declared in 2024 that AI would demand more power. What’s valuable isn’t the idea—it’s timing and conviction. For example: Would you dare commit $20 million in call options on Intel at $20/share?

That confidence doesn’t stem solely from belief in AI’s macro trend. It comes from knowing which companies are signing multi-gigawatt power purchase agreements, which data centers are expanding, and exactly how massive the demand surge really is.

Leopold Aschenbrenner’s fund, Situational Awareness, counts among its limited partners (LPs) people seated front-row at precisely those decisions.

Its LPs include Stripe’s two co-founders—whose company processes payments for most of Silicon Valley’s tech firms and thus directly senses accelerating infrastructure spending;

And Nat Friedman, former GitHub CEO and current Head of AI Product at Meta—someone who participates daily in compute procurement decisions.

They bring more than initial capital: they provide a continuously updated information pipeline.

Also critical is his fund’s Research Director, Carl Shulman—a veteran in AI safety who previously worked at Peter Thiel’s hedge fund Clarium Capital, where his role was specifically to translate AI-community insights into executable trading strategies.

His portfolio also contains an easily overlooked crypto corner.

End-2024 filings show new positions in CleanSpark and Bitfarms—two Bitcoin mining firms now converting BTC mining facilities into AI compute centers.

Crypto mining sites naturally possess large-scale power infrastructure and thermal management systems—precisely the scarcest resources for AI data centers.

Interestingly, he’s no stranger to crypto. In 2022, he worked for nine months at FTX’s charitable arm, the Future Fund—founded by Sam Bankman-Fried—and left just before FTX collapsed.

Whether that experience directly influenced his view on mining firms remains unknown. But it’s certain he’s among the rare few with deep exposure to both cutting-edge AI labs and the crypto industry—a cross-disciplinary vantage point that confers unique cognitive leverage and network access.

Another telling detail: his fiancée, Avital Balwit, serves as Chief of Staff to Anthropic CEO Dario Amodei. Anthropic—the maker of Claude—is OpenAI’s most direct competitor.

He worked at OpenAI; his fiancée works at Anthropic’s CEO’s side. He holds hands-on experience at one of the two AGI frontrunners—and daily access to the other.

Last year, Fortune magazine interviewed over a dozen insiders who’d interacted with him—and concluded he excels at “packaging ideas brewing in Silicon Valley labs into compelling narratives.”

The author finds that description too polite. What he actually does is far more direct: he places bets in public markets using insights gleaned from private networks. His published AI paper is the sanitized version; his hedge fund is the full, unredacted edition.

A Positive-Feedback Loop Closed to Outsiders

Looking back, Leopold Aschenbrenner’s fund adopted an unusual structure.

Most AI-related capital flows through venture capital—betting on early-stage startups to become the next OpenAI. He rejected that path entirely. As Fortune reported, he explicitly ruled out VC when launching his fund, arguing that AGI’s impact is so vast that only the most liquid public markets can fully express such an investment thesis.

This choice alone reveals a shared consensus within his circle: the biggest AI-era investment opportunities may reside not in startups—but in legacy companies already owning physical infrastructure.

Think of a fuel-cell firm with ready grid interconnection, a chip giant with wafer-fab capacity, or a Bitcoin miner with land, power, and cooling systems. These companies have traded publicly for years—highly liquid—but most analysts still value them using outdated frameworks, failing to incorporate “AI infrastructure necessity” as a material variable.

That gap is his arbitrage opportunity.

Insiders already know the rhythm and scale of AI infrastructure expansion; public markets still price using old logic. The spread between those two views is where profit lives.

This informational edge has another feature: it self-reinforces.

The better the fund performs, the more industry insiders want to become LPs. The more LPs join, the denser the decision-maker intelligence flowing into the fund. The richer the intelligence, the sharper the bets. It’s a positive-feedback loop—and for outsiders, the entry barrier only rises over time.

Of course, the loop has vulnerabilities. Highly concentrated positions plus significant leverage mean the fund is extremely sensitive to a single narrative. So long as “AI infrastructure continues expanding” holds true, everything sails smoothly.

But if AI’s pace slows—or if a technological breakthrough bypasses the energy bottleneck—the speed of drawdown in his concentrated positions could vastly exceed the speed of accumulation. He’s betting not just on direction—but on timing. A misstep in timing turns consensus into collective blind spots.

Returning to the original question:

Everyone studies his filings, trying to replicate his moves. Yet behind those god-tier returns lies a structural advantage.

The paper is public. The filings are public. His investment logic is laid bare in podcasts and interviews. Even if you fully grasp every one of his judgments, you still cannot replicate the vantage point from which he formed them.

You can trace the positions. You can envy the returns. But you cannot share the source of the insight. That asymmetry—perhaps—is the most valuable one of our era.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News