Hidden Concerns Beneath Solana's Prosperity

TechFlow Selected TechFlow Selected

Hidden Concerns Beneath Solana's Prosperity

Those who sell shovels make more money than those who dig for gold.

Written by: Flip Research

Translated by: Luffy, Foresight News

Recently, my Twitter feed has been flooded with bullish Solana narratives, often centered around memecoin hype. I started to believe that memecoins truly have a supercycle and that Solana might replace Ethereum as the most important L1. But then I began digging into the data—and what I found is deeply concerning. In this article, I’ll walk through my findings and explain why Solana may be a house of cards.

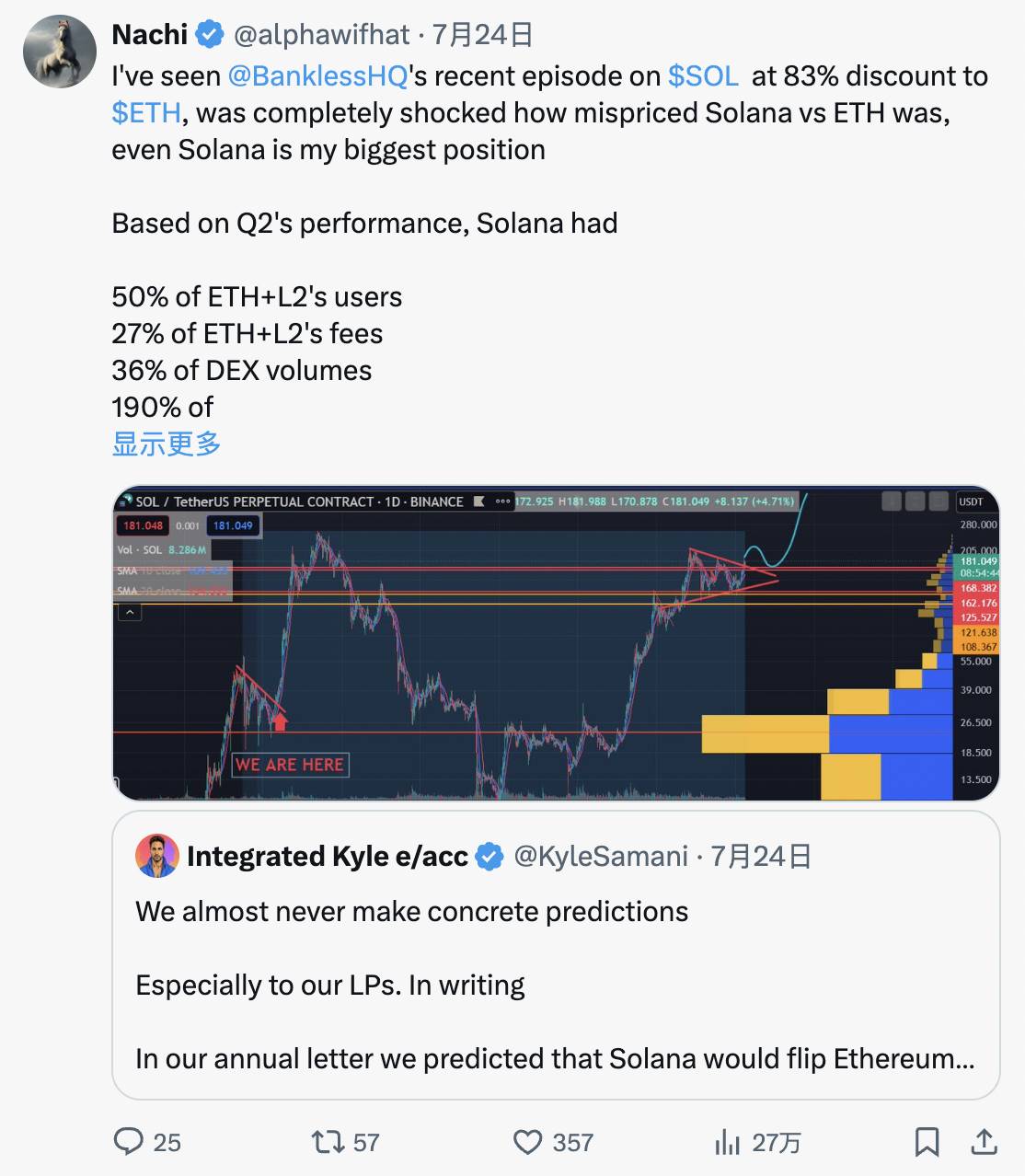

First, let’s look at the current bull market narrative, succinctly summarized by @alphawifhat:

https://x.com/alphawifhat/status/1816136696758735266

In Q2, Solana:

-

Had 50% of the users of Ethereum + L2s;

-

Generated 27% of the transaction fees of Ethereum + L2s;

-

Accounted for 36% of DEX trading volume;

-

Saw stablecoin transaction volume at 190% of Ethereum + L2s.

User Base Comparison

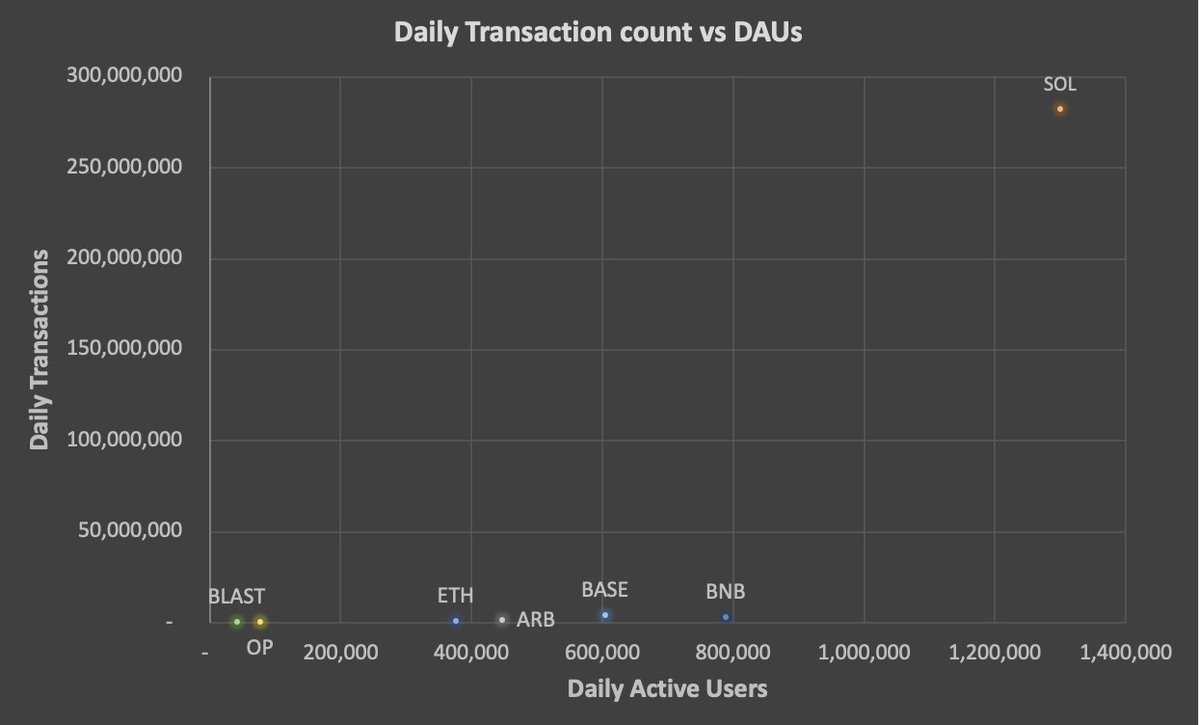

Below is a comparison of user activity on Ethereum mainnet versus Solana (mainnet only, since post-Dencun the vast majority of fees come from mainnet; source: @tokenterminal):

Ethereum active users and transaction count

Solana active users and transaction count

At first glance, Solana’s numbers look impressive—over 1.3 million daily active users (DAU) compared to Ethereum’s 376,300. However, when we examine transaction volume alongside user counts, some anomalies emerge. On July 26, Ethereum recorded 1.1 million transactions with 376,300 DAU, averaging about 2.92 transactions per user. In contrast, Solana had 282.2 million transactions with 1.3 million DAU, averaging 217 transactions per user. One might argue this reflects Solana’s low fees enabling more frequent trading and increased arbitrage bot activity. To test this, I compared it with Arbitrum—one of the most popular low-cost chains. Yet, Arbitrum averaged only 4.46 transactions per user on the same day. Similar patterns hold across other chains:

Given Solana’s higher user count, I also compared Google Trends data between Ethereum and Solana:

Surprisingly, Ethereum either matches or exceeds Solana in search interest. Given the DAU gap and the intense memecoin-driven hype around Solana, this result was unexpected. So what’s really going on?

DEX Trading Volume Analysis

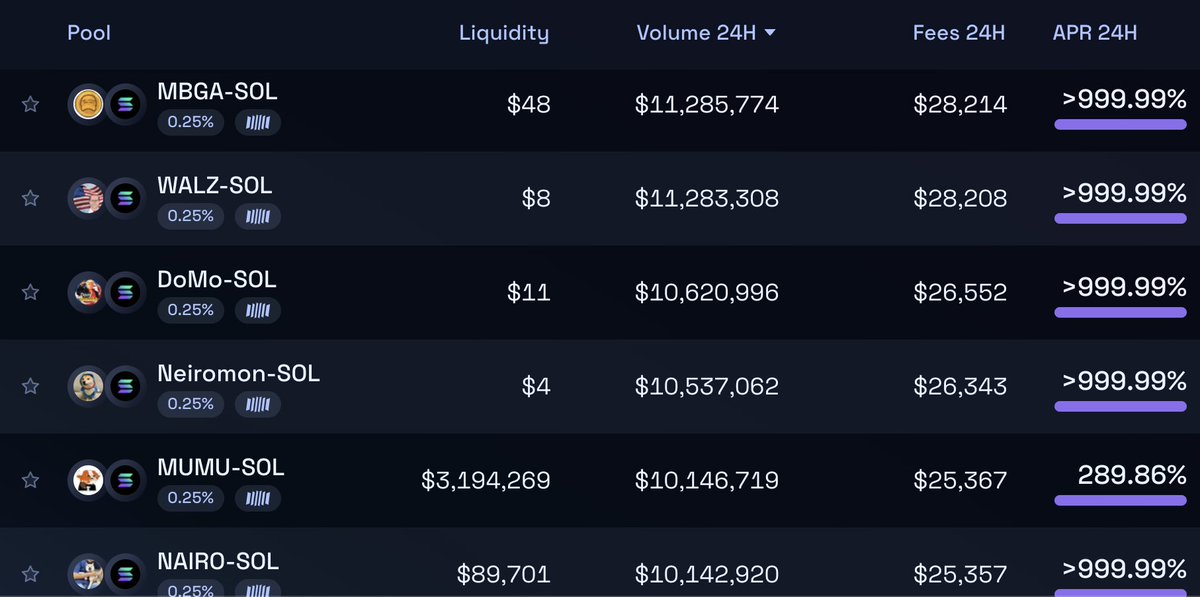

To understand the transaction discrepancy, examining liquidity pools on Raydium helps. A quick glance reveals clear red flags:

Initially, I thought these were just low-liquidity spoof trades designed to lure memecoin degens. But the reality is far worse:

Behind each low-liquidity pool is a project that rug-pulled within the last 24 hours. Take MBGA: in the past day, Raydium recorded 46,000 trades worth $10.8M, involving 2,845 unique wallets and generating over $28,000 in fees. (For context, a similarly sized legitimate pool like MEW generated only 11.2K trades.)

Looking at participating wallets, most appear to be bots operating within the same network, contributing tens of thousands of transactions. These bots generate fake volume independently—randomizing SOL amounts and trade frequency—until a project collapses, then move to the next one. In the last 24 hours alone, over 50 Raydium pools with >$2.5M in volume have been rug-pulled, collectively generating over $200M in volume and $500K in fees. Orca and Meteora show significantly fewer such pools, while Uniswap on Ethereum rarely sees similar scams.

The scale of Solana’s rug problem has wide-ranging implications:

-

Given the abnormally high transactions-per-user ratio and the volume of on-chain spoofing and fraudulent trades, it's clear that the vast majority of Solana’s transactions are inorganic. Among Ethereum L2s, Blast has the highest daily transaction-to-user ratio (15), which makes sense given its low fees and ongoing Season 2 airdrop farming. As a rough estimate, if Solana’s real transaction/user ratio were similar to Blast’s, over 93% of Solana’s transactions (and fees) would be inorganic.

-

These scams exist solely because they’re profitable. Therefore, user losses equal at least the fees generated plus trading costs—amounting to millions of dollars lost daily.

-

Once deploying these scams becomes unprofitable (when real users grow tired of losing money), transaction volume and fee revenue on Solana will inevitably decline.

-

Thus, Solana’s actual user base, organic fee income, and DEX trading volume are all vastly overstated.

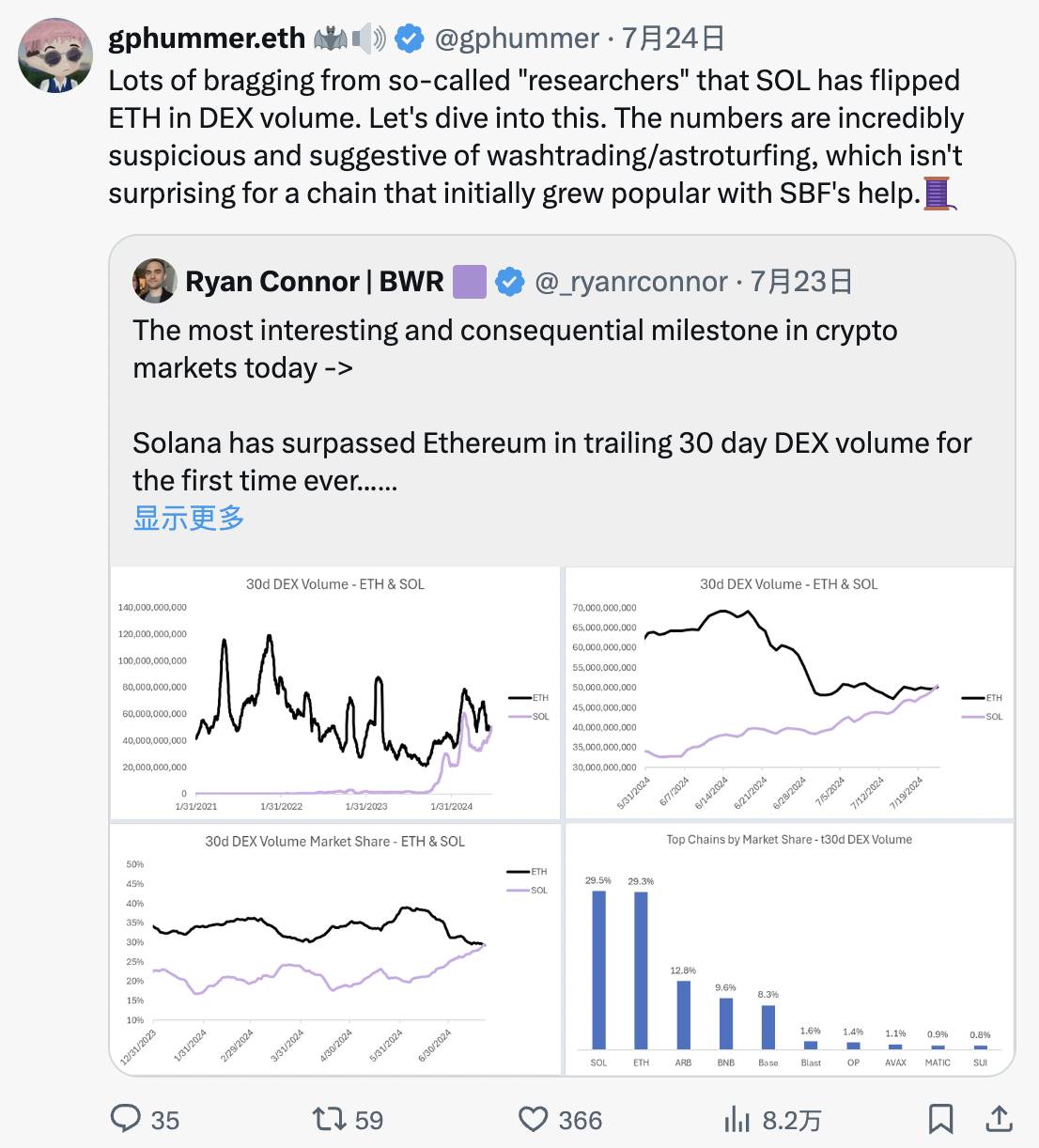

I’m not alone in reaching these conclusions. @gphummer recently shared similar insights:

https://x.com/gphummer/status/1816122702564131095

MEV on Solana

MEV on Solana exists in a unique state. Unlike Ethereum, Solana lacks a native mempool. Instead, entities like Jito have created (now deprecated) off-protocol infrastructure to simulate mempool functionality, enabling MEV strategies like frontrunning and sandwich attacks. Helius Labs published an in-depth article detailing MEV on Solana.

The issue on Solana is that most traded tokens are highly volatile, low-liquidity memecoins, and traders often set slippage above 10% to ensure execution. This creates fertile ground for MEV exploitation:

Examining block space profitability, it's evident that most value today comes from MEV extraction:

While technically “real” value, MEV only persists as long as it remains profitable—i.e., as long as retail continues chasing memecoins. Once memecoin mania cools, MEV fee income will collapse.

Many talk about how Solana’s focus will eventually shift to infrastructure tokens like JUP and JTO. That may happen, but these assets have lower volatility and higher liquidity, offering far less MEV potential than memecoins.

Experienced players are racing to build the best infrastructure to capture this opportunity. During my research, I heard rumors that some are investing heavily to control mempool access and plan to sell it to third parties. I can't verify this, but the incentives are clear: by steering as much memecoin activity as possible to Solana, savvy insiders profit from MEV, insider trading, and SOL price appreciation.

Stablecoins

When it comes to stablecoin trading volume and TVL, another oddity emerges on Solana. Stablecoin volume on Solana is visibly higher than on Ethereum, yet DefiLlama shows Ethereum with $80B in stablecoin TVL versus Solana’s $3.2B.

I believe stablecoin TVL is a harder metric to manipulate than trading volume or fee income on low-cost platforms. The dynamics of stablecoin trading support this: @WazzCrypto noted a sharp drop in Solana’s stablecoin volume following the CFTC’s announcement of an investigation into Jump:

https://x.com/WazzCrypto/status/1817560196073292033

Retail Is Losing Money

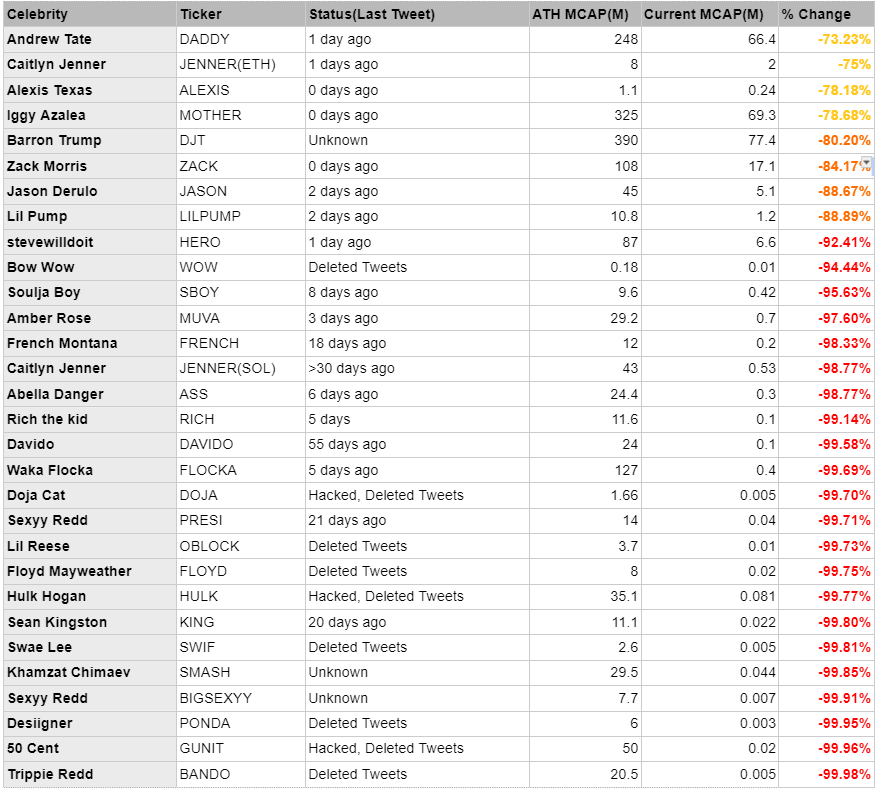

Beyond rugs and MEV, the outlook for retail traders remains bleak. Celebrities have chosen Solana as their go-to chain for launching memecoins—with poor results:

Andrew Tate’s DADDY is the top-performing celebrity token—but still down 73%.

A quick Twitter search also reveals rampant insider trading and evidence of developers dumping tokens on retail investors:

You might ask, “My feed is full of people making millions trading memes on Solana. How does that align with your claims?”

I don’t believe KOLs’ tweets reflect the broader user base. In the current frenzy, it’s easy for them to get early positions, promote their tokens, profit from followers, and repeat. There’s clear survivorship bias: winners shout louder than losers, distorting perception. Objectively, retail appears to lose millions daily—to scammers, devs, insiders, MEV, and KOLs—without even considering that most things traded on Solana are memecoins with no underlying value. It’s hard to deny that most memecoins eventually go to zero.

Other Considerations

Markets evolve quickly. When sentiment shifts, factors previously ignored become glaring:

-

Poor network stability with frequent outages

-

High transaction failure rate

-

Unreadable block explorers

-

High development barrier; Rust is far less user-friendly than Solidity

-

Poorer interoperability compared to EVM. I believe competition among multiple interoperable blockchains is healthier than being locked into a single chain.

-

Low probability of ETF approval from both regulatory and demand perspectives. This thread explains why institutional demand remains low under Solana’s current conditions.

-

Massive issuance of 67,000 SOL/day ($12.4M)

-

41M SOL ($7.6B) from FTX holdings remain locked. 7.5M ($1.4B) will unlock in March 2025, followed by monthly unlocks of 609K ($113M) until 2028. These SOL were purchased at ~$64 each.

Conclusion

As always, shovel sellers will profit from the Solana memecoin craze while speculators get rekt—often without realizing it. I believe standard Solana metrics are severely inflated. Moreover, the majority of genuine users are rapidly losing money to bad actors. Fortunately, we’re currently in a mania phase where retail inflows still exceed outflows from seasoned players. But once users grow weary of constant losses, many metrics will collapse rapidly. As outlined, Solana also faces structural headwinds that will become apparent when market sentiment shifts. Any price increase will worsen inflationary and unlock pressures. Ultimately, I believe SOL is fundamentally overvalued. While current sentiment and momentum may push prices higher in the short term, the long-term outlook is far less certain.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News