Layer2 Sector Mid-Year Review: Are the Growth Numbers Real or Fake?

TechFlow Selected TechFlow Selected

Layer2 Sector Mid-Year Review: Are the Growth Numbers Real or Fake?

Arbitrum, Optimism, zkSync, Starknet, Base, Taiko, and Scroll.

Written by: LINDABELL

In March 2024, Ethereum completed the Dencun upgrade, bringing renewed attention back to the Layer2 space. Meanwhile, in the first half of the year, Starknet and zkSync both rolled out their airdrop programs, marking the point at which all four major mainstream Layer2 projects had issued tokens. Additionally, some emerging Layer2 projects performed notably well in 2024—for example, Base achieved significant traffic growth in the first half of the year, surpassing Optimism to become the second-largest Layer2.

Despite strong growth trends in the Layer2 sector, questions remain about the authenticity of reported data. Previously, concerns were raised regarding zkSync’s daily transaction volume and number of active addresses. So, do these surface-level signs of prosperity truly reflect actual network usage?

TL;DR:

-

In the first half of 2024, Arbitrum maintained its lead with a total value locked (TVL) of $17.15 billion, capturing 40% of the market share and solidifying its position as the top Layer2.

-

Base surpassed Optimism with a TVL of $7 billion, becoming the second-largest Layer2 platform. Additionally, as of July 28, Base's average daily transactions reached 4 million—nearly double that of Arbitrum—and its number of active addresses exceeded Arbitrum’s, surpassing 600,000.

-

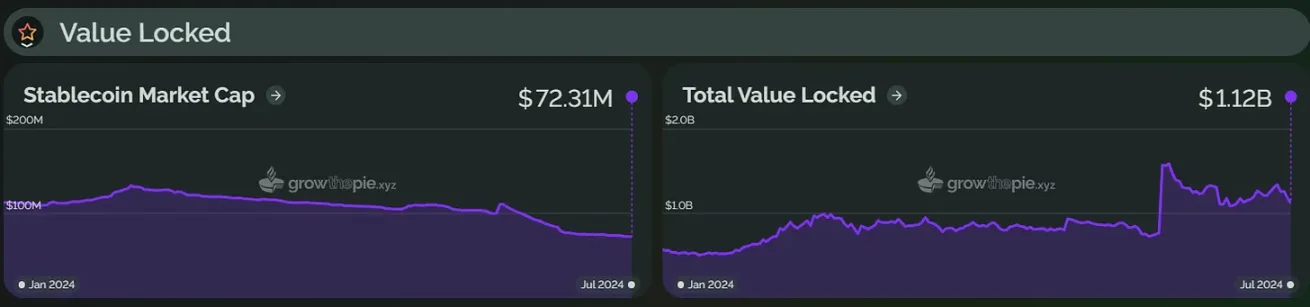

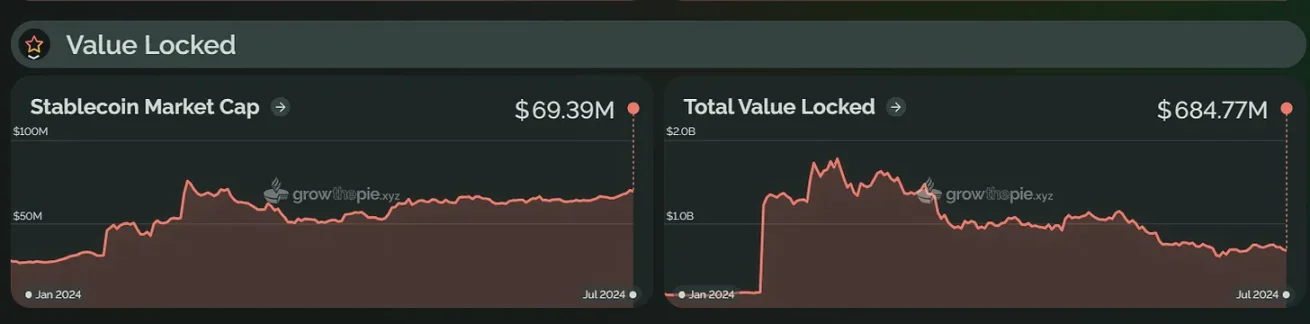

zkSync’s TVL reached $1.12 billion in the first half of 2024, up approximately 99% from the beginning of the year. However, after its airdrop, the number of active addresses dropped by 83.5%, and average daily transactions declined by 86%. Similarly, Starknet’s TVL peaked at $1.776 billion in March before falling to $685 million. Its number of active addresses decreased by 92%, while daily transactions fell by 64.2%.

-

Taiko launched its mainnet in May 2024, reaching a TVL peak of $190 million on June 5, later retreating to $163.45 million. The number of active addresses declined by 78.3% from its peak in June.

-

Scroll saw a year-on-year TVL increase of 1,544%, but growth in active addresses and daily transactions was relatively modest—up 13.4% and 27.7% respectively compared to the start of the year.

(Data sources for this article: L2BEAT, growthepie, and DeFiLlama)

Total Value Locked (TVL)

Arbitrum Leads, Base Overtakes Optimism to Become Second-Largest Layer2

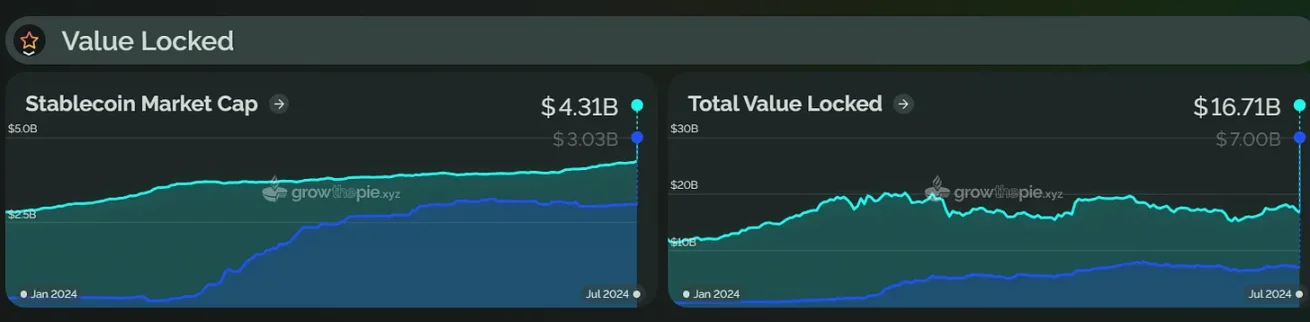

In the first half of 2024, the total value locked across the Layer2 ecosystem grew from approximately $22.8 billion at the end of January to $42.97 billion—an increase of about 88%. Among them, Arbitrum, Optimism, and Base were the primary contributors.

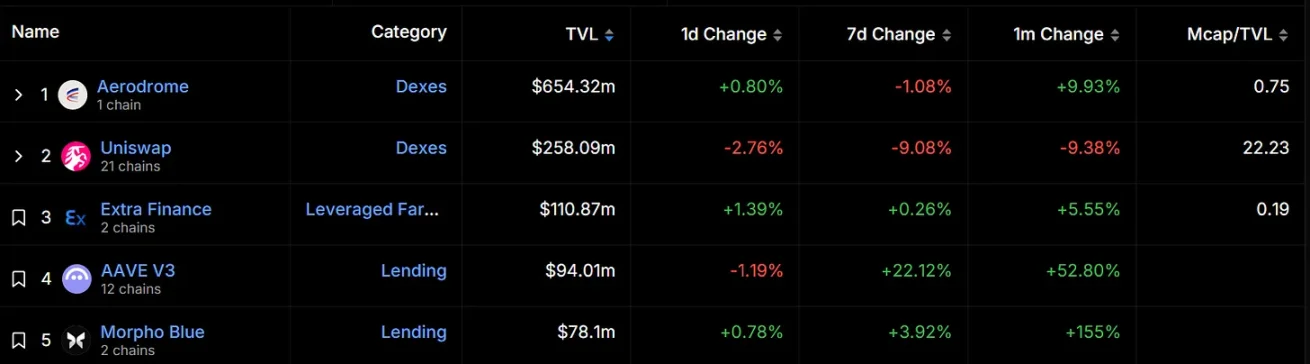

Since the beginning of 2024, Arbitrum has consistently maintained the leading position in TVL. As of July 28, Arbitrum’s TVL reached approximately $17.15 billion, securing first place with around 40% market share—over 2.4 times larger than Base, the second-ranked project. According to DeFiLlama, AAVE holds the highest TVL on Arbitrum at $812.62 million, followed by GMX and Uniswap at $513.89 million and $325.43 million respectively.

Additionally, as shown in the chart below, Arbitrum’s TVL showed a declining trend between March and May. This was likely due to a large unlock of ARB tokens for the team and investors in March. According to Token Unlocks data, as of July 28, 34% of ARB tokens have been unlocked.

As a rising contender, Base has maintained an upward trajectory since the beginning of 2024 and overtook Optimism in June to become the second-largest Layer2. Currently, Base’s TVL stands at approximately $7 billion—an increase of about 716% from the start of the year. As seen in the chart below, Base experienced a notable TVL surge in March, possibly driven by Farcaster’s continued growth, reduced gas fees following the Dencun upgrade, and the popularity of meme tokens, all contributing to increased on-chain liquidity and higher TVL. However, Base’s TVL has slightly retreated since then, down about 6.6% from its June peak.

According to DefiLlama, Base currently has $1.67 billion in DeFi TVL, dominated by native DeFi projects such as Aerodrome ($654 million) and Extra Finance ($110 million). Aerodrome is currently the dApp with the highest TVL on Base, more than doubling Uniswap, which ranks second.

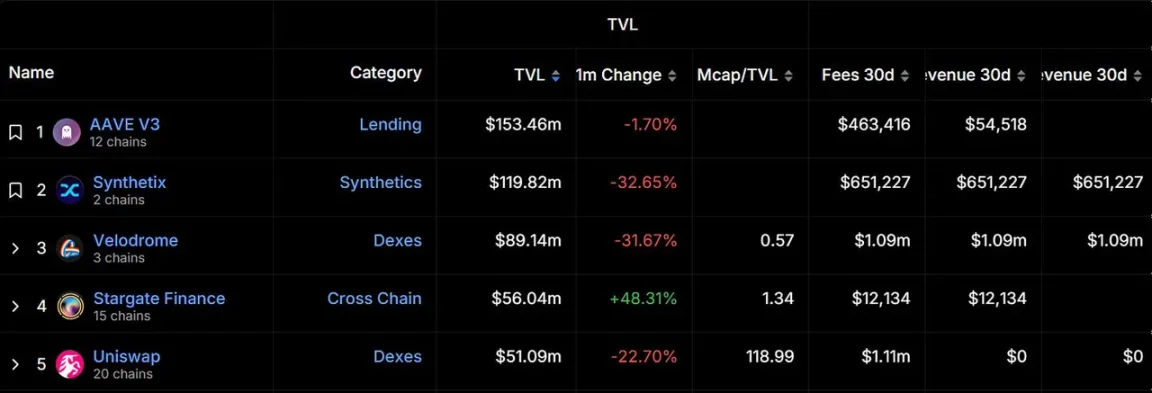

Optimism ranks third in total value locked, reaching its first-half high on March 10, 2024, before experiencing a slight decline. Although overall stability was maintained, it was ultimately overtaken by Base in June. According to DeFiLlama, the top three projects by TVL in the Optimism ecosystem are AAVE v3, Synthetix, and Velodrome. However, all three have seen declining TVL over the past month.

Scroll Reaches New Highs, Taiko’s TVL Peaks Then Retreats

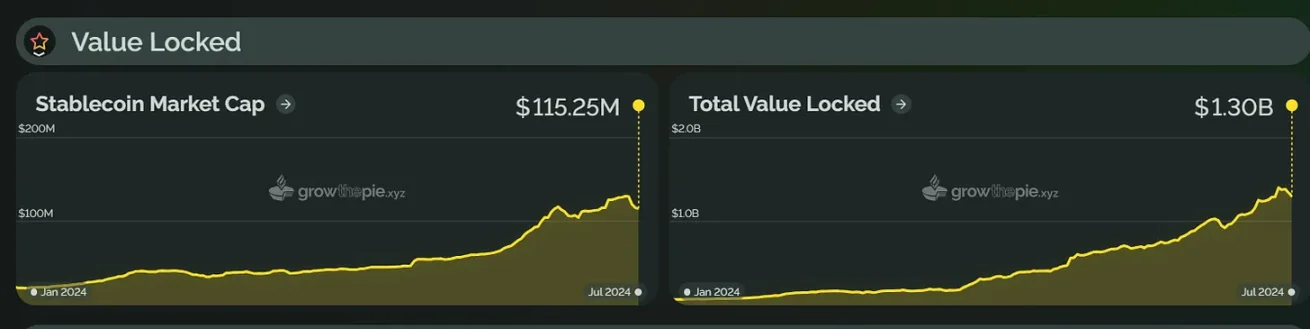

On the other hand, Scroll has set repeated TVL records throughout 2024 and now stands at $1.3 billion—the fourth-highest among the Layer2s analyzed here—with a staggering 1,544% increase. This growth may be attributed to various initiatives launched by Scroll targeting users and developers. In April, Scroll introduced Scroll Sessions and launched Session One on June 21, specifically designed to reward DeFi users providing liquidity on DEXs. Additionally, Scroll launched the “Level Up with Scroll” platform, allowing developers to apply for ecosystem grants.

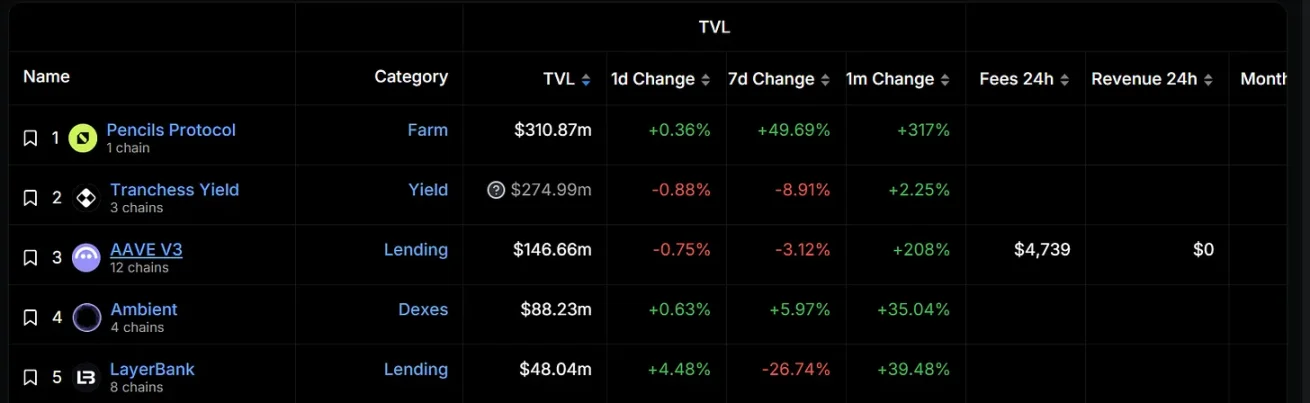

According to DeFiLlama, Pencils Protocol, a native project within the Scroll ecosystem, leads in TVL at $310.87 million, with a 317% increase over the past month. Notably, Scroll’s total DeFi TVL is $769.02 million, and the top three projects account for over 95% of the ecosystem’s market share.

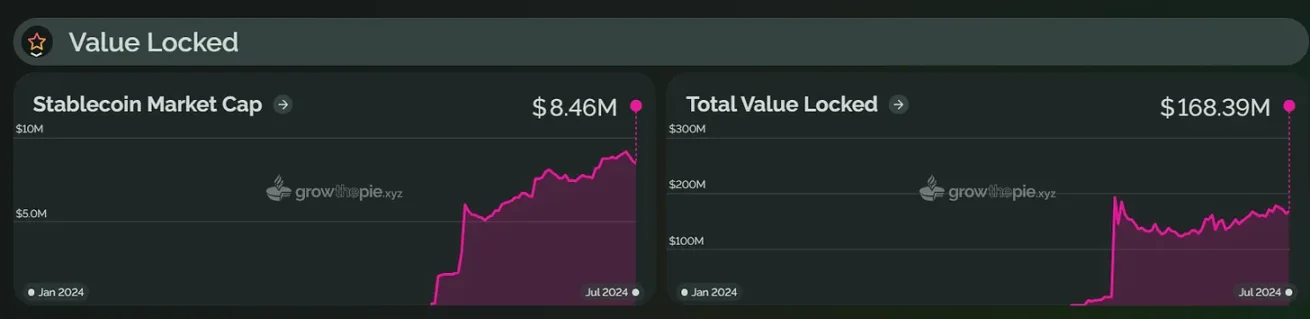

Taiko launched its mainnet on May 27, 2024. As shown in the chart below, Taiko’s TVL peaked at approximately $190 million on June 5 and has since declined to $163.45 million. As a newly launched Layer2, Taiko’s TVL remains low compared to other well-known Layer2s, but it is actively expanding its ecosystem. For instance, in terms of DeFi applications, Taiko has integrated over 80 projects including LayerZero, Stargate, and Oku Trade.

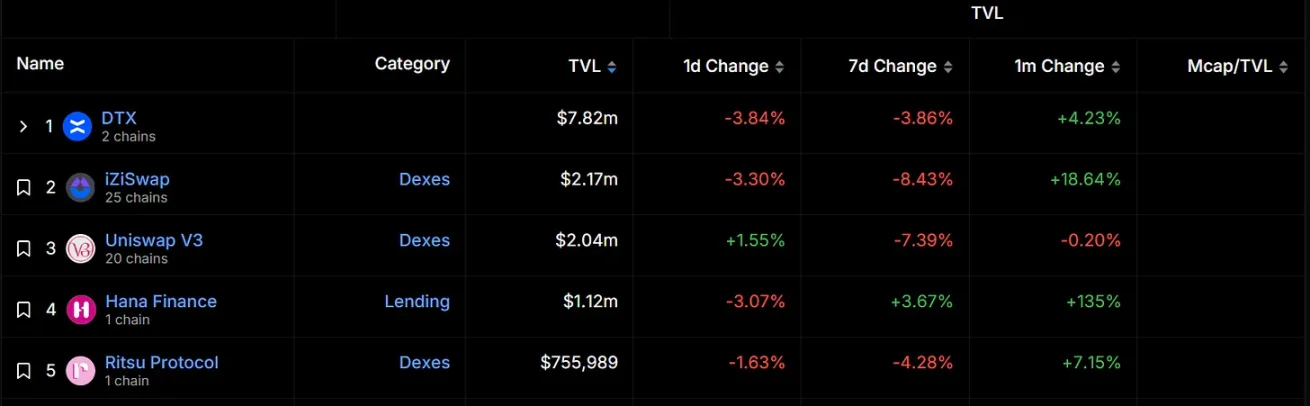

According to DeFiLlama, the top three projects by TVL on Taiko are DTX, a decentralized perpetual trading platform; iZUMi Finance’s multichain DEX iZiSwap; and Uniswap V3. Overall, TVL for projects in the Taiko ecosystem remains relatively low, with DTX holding a dominant market share.

zkSync and Starknet Face Ecosystem Challenges, With Post-Airdrop TVL Declines

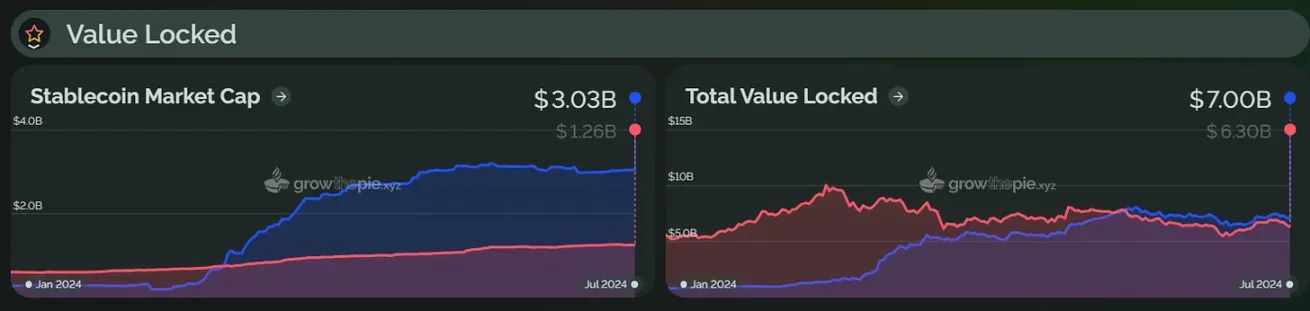

As of now, zkSync’s total value locked stands at $1.12 billion, up approximately 99% from the beginning of the year. As shown in the chart below, zkSync’s TVL saw a significant rise in June, primarily due to its announced airdrop program on June 11. Under this plan, zkSync distributed 3.6 billion tokens to community members on June 17, benefiting 695,232 eligible wallet addresses. However, Nansen data shows that over 40% of major recipients sold all their allocated tokens, while 41.4% sold part of them. Only 17.9% still hold their tokens.

Moreover, although the zkSync ecosystem has integrated over 200 projects, only two have TVL exceeding $10 million. SyncSwap leads with $35.17 million in TVL, clearly dominating the ecosystem. Additionally, the top three projects—SyncSwap, Koi Finance, and zkSwap Finance—all saw declines in TVL over the past month. Overall, the post-airdrop effect for zkSync is just beginning, and ecosystem health and sustainability remain key challenges.

Similarly, in the first half of 2024, Starknet’s TVL began rising significantly starting February 20 and hit an all-time high of $1.776 billion on March 14. This surge was driven by the STRK token airdrop and the “Starknet Spring DeFi Incentives Program” launched by the Starknet Foundation. However, as of now, Starknet’s TVL has fallen to approximately $685 million—about 61% lower than its peak.

In terms of ecosystem development, Starknet has now integrated over 100 applications. The top five projects by TVL on Starknet are all native to the ecosystem. Leading is lending protocol Nostra with $164.6 million in TVL; second is decentralized exchange Ekubo, whose TVL grew 61.95% last month to $77.98 million; third is lending protocol zkLend with $26.7 million in TVL. However, only four projects in Starknet’s ecosystem exceed $10 million in TVL, with fifth-ranked lending protocol Vesu at just $3.77 million.

Active Addresses and Transaction Volume

Beyond TVL, a network’s number of active addresses and average daily transactions reflect actual usage and user engagement. In the first half of 2024, Arbitrum and Base demonstrated high user activity, while zkSync and Starknet showed clear downward trends. Optimism and Scroll exhibited steady growth, albeit with smaller increases.

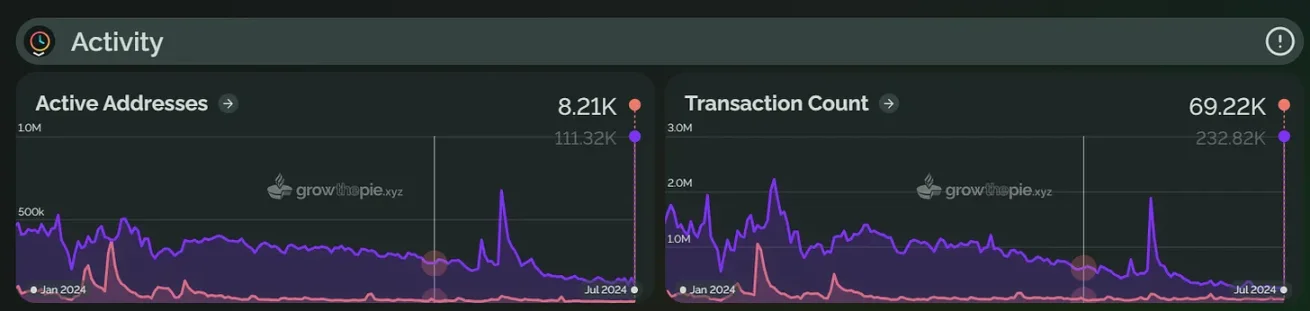

Arbitrum Active Addresses Surge 140.7%, Base Daily Transactions Exceed 4 Million

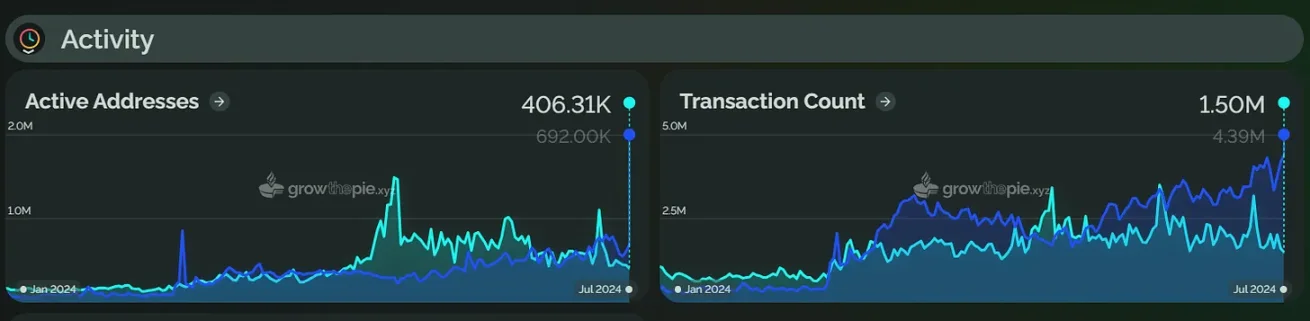

Since the beginning of 2024, Arbitrum’s number of active addresses has grown by 140.7%. This growth stems from large-scale subsidies and funding initiatives implemented by Arbitrum. For example, in June, the Arbitrum community approved a proposal to support gaming projects within the ecosystem with 200 million ARB tokens over three years, along with $25 million allocated for project management and operations. Additionally, in May, the Arbitrum Foundation provided funding to 13 projects including DODO and Double. However, Arbitrum’s average daily transactions increased by only 43.7% compared to the start of the year—less than the growth in active addresses. This may indicate that many new users created addresses but did not transact frequently, or engaged in mostly low-frequency activities.

Currently, both Base’s average daily transactions and number of active addresses exceed those of Arbitrum. As shown in the chart below, at the beginning of 2024, Base processed only 330,000 daily transactions, while Arbitrum handled around one million. Starting in March 2024, Base’s daily transaction volume began rising sharply, setting a new record on June 27. As of July 22, Base’s daily transactions exceeded 4 million—nearly double that of Arbitrum. Simultaneously, Base’s number of active addresses has also risen, now surpassing Arbitrum with over 600,000 active addresses. Beyond the influence of meme coins and SocialFi, Coinbase’s smart wallet has played a significant role in enhancing user experience and boosting transaction volume. The smart wallet offers a simplified, gas-free on-chain experience, enabling users to create free, secure, self-custodial wallets within seconds, greatly improving transaction convenience.

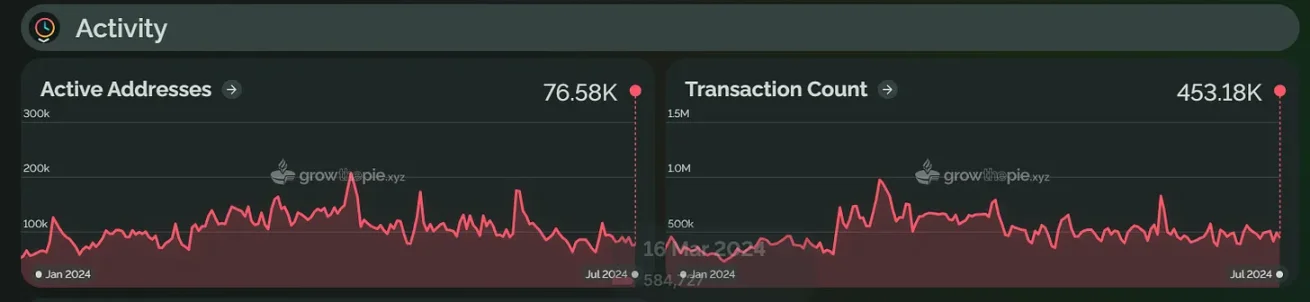

zkSync and Starknet See Significant Drops in Active Addresses and Daily Transactions

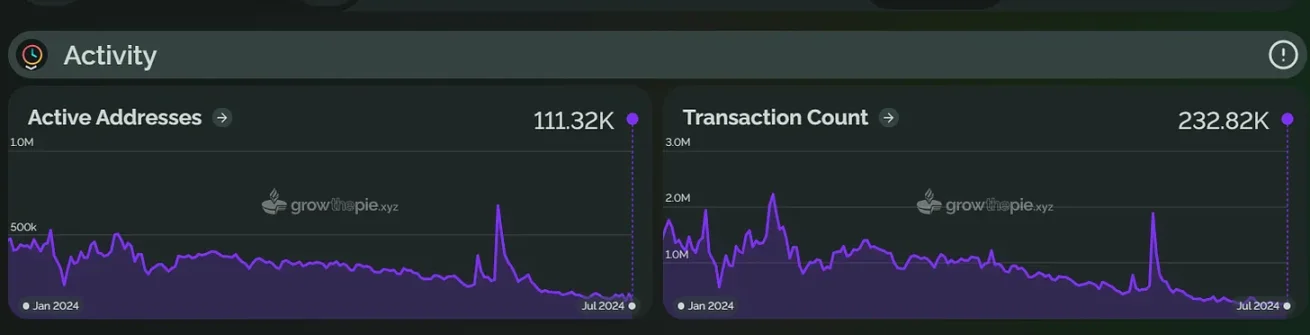

In the first half of 2024, both the number of active addresses and daily transaction volume in the zkSync ecosystem declined significantly. At the beginning of the year, zkSync led in active addresses, but numbers gradually dropped afterward. As shown in the chart below, within one month of zkSync’s airdrop on June 17, the number of active addresses on the network decreased by approximately 83.5%, indicating most users participated solely to claim the airdrop. Additionally, zkSync’s average daily transactions have declined since the beginning of the year, currently down about 86% from initial levels. Similar to active addresses, average daily transactions saw a sharp drop within a month after the airdrop.

On July 2, zkSync announced zkSync 3.0 Elastic Chain—a ZK Rollup network capable of infinite scalability. zkSync claims this solution enables native, trustless, low-cost interoperability between ZK chains. However, whether it can capture market share from Optimism’s Superchain and Polygon’s AggLayer remains to be seen.

Similar to zkSync, Starknet also experienced declines in average daily transactions and active addresses during the first half of 2024. As of now, Starknet’s average daily transactions are down approximately 64.2% from the start of the year, while active addresses have dropped by about 92%. Among the Layer2 solutions analyzed here, Starknet ranks last in both daily transactions and active addresses. As seen in the chart, Starknet saw a small uptick in early January, primarily due to its February airdrop, but both metrics began declining after the airdrop. Looking ahead, Starknet plans to distribute another $400 million worth of STRK tokens in future airdrops.

However, Starknet has several updates planned for the second half of the year. The Starknet community released updates for v0.13.2 and its summer roadmap, expecting to launch v0.13.2 in August and v0.13.3 between October and November. At the recent ETHCC summit in Brussels, Eli Ben-Sasson also announced that Starknet will open staking by the end of 2024.

Optimism and Scroll Show Steady Growth, Active Addresses Up 35% and 13.4% Respectively

Optimism’s development in the first half of 2024 remained relatively stable. Both average daily transactions and active addresses saw modest increases, with active addresses up 35% and daily transactions up 14% from the start of the year. As shown in the chart below, there were minor peaks in Optimism’s active addresses and transaction volume, likely tied to specific developments or market events. For example, in May, Optimism announced that L3s built using OP Stack could now join the Superchain and qualify for Retro funding, airdrops, and growth initiatives. Additionally, Optimism’s Retro Funding program began distributing 850 million OP tokens in four rounds starting in May, supporting projects and individuals within the ecosystem. These incentives likely contributed to the growth in active addresses.

In the first half of 2024, Scroll’s number of active addresses increased by 13.4% from the start of the year, while average daily transactions rose by 27.7%. Unlike its substantial TVL growth, the increases in active addresses and transaction volume were relatively modest.

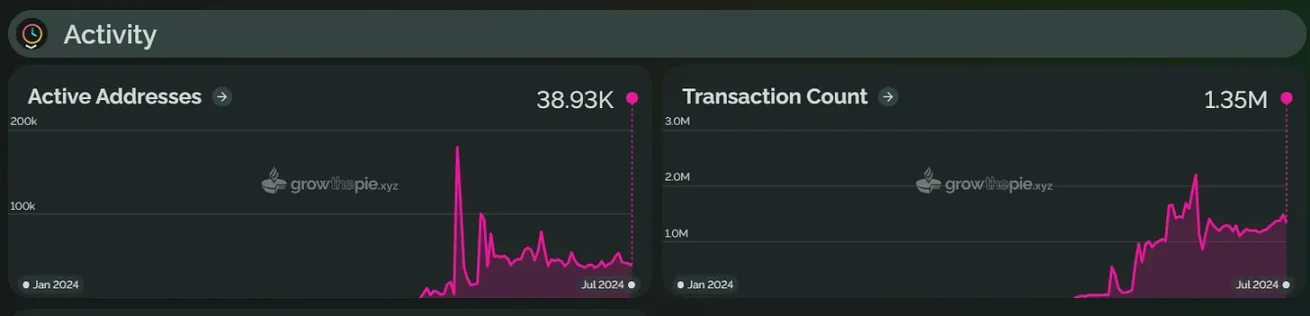

Taiko’s Active Addresses Drop 78.3% From Peak After Mainnet Launch

As shown in the chart below, Taiko’s number of active addresses surged sharply between June 4 and 5, then began to decline—likely due to TAIKO token listings on exchanges such as Bitget on June 5. Afterward, active addresses retreated, showing a brief rebound after June 11 before declining again. The current count is around 40,000—down 78.3% from its peak. Additionally, Taiko’s average daily transactions reached a historical high on June 30 and currently stand at 1.35 million, down approximately 38.4% from the peak.

Additionally, after mainnet launch, some community members noted that Taiko’s fees were higher compared to other Ethereum L2 protocols. In response, Taiko explained this was mainly due to additional logic and storage requirements. The current implementation uses multiple upgradable proxies, adding extra delegate call costs. Furthermore, Taiko blocks are not proposed or proven in batches, requiring proposers to interact more frequently with Ethereum to compete for block space and ensure chain activity. Storage write costs are also higher because the on-chain ring buffer has not yet been exhausted. Taiko stated this situation would improve within approximately 40 to 60 days. Notably, Taiko successfully upgraded its mainnet to version v1.7.0 on July 2, which is expected to significantly reduce gas consumption for Rollup protocols on Ethereum.

Conclusion

Overall, whether established or emerging Layer2 projects, the first half of 2024 showcased diverse development trajectories. However, certain issues persist—such as declining user engagement post-airdrop observed in zkSync and Starknet, reflecting overreliance on short-term incentives. Meanwhile, Scroll and Taiko, despite significant TVL growth, face challenges in sustaining user activity, highlighting the need for more comprehensive ecosystem development. This suggests that as the market evolves, Layer2 projects must continue innovating and expanding to ensure sustainable growth and long-term user engagement.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News