RWA 10,000-Word Research Report: The First Wave of Tokenization Has Arrived

TechFlow Selected TechFlow Selected

RWA 10,000-Word Research Report: The First Wave of Tokenization Has Arrived

This article attempts to examine the potential benefits and long-standing challenges that tokenization could bring, using McKinsey's analytical framework for tokenization and viewing it from the perspective of traditional finance.

Author: Will Awang

If I were to envision how future finance should operate, I would undoubtedly incorporate the many advantages offered by digital currencies and blockchain technology: 24/7 availability, instant global liquidity, permissionless fair access, asset composability, and transparent asset management. This envisioned future of finance is gradually being built through tokenization.

BlackRock CEO Larry Fink emphasized the importance of tokenization for the future of finance in early 2024: "We believe the next step in financial services will be the tokenization of financial assets, meaning every stock, every bond, every financial asset will run on a single shared ledger."

While asset digitization can scale broadly as technology matures and measurable economic benefits emerge, widespread adoption of asset tokenization won’t happen overnight. One of the most challenging aspects lies in upgrading traditional financial infrastructure within a heavily regulated industry, which requires participation from all players across the entire value chain.

Nevertheless, we are already witnessing the first wave of tokenization, primarily driven by investment returns under current high-interest-rate environments and real-world use cases such as stablecoins and tokenized U.S. Treasuries. The second wave may be propelled by use cases involving asset classes that currently have smaller market share, less obvious yields, or more significant technical hurdles.

This article attempts to examine the potential benefits and persistent challenges of tokenization from a traditional finance perspective, using McKinsey & Co.’s analytical framework for tokenization, while incorporating real-world examples. The conclusion: despite ongoing challenges, the first wave of tokenization has already arrived.

TL;DR

-

Tokenization refers to the process of creating a digital representation of an asset on a blockchain;

-

Tokenization offers numerous advantages: 24/7 availability, instant global liquidity, permissionless fair access, asset composability, and transparency in asset management;

-

Within financial services, focus is shifting toward “blockchain, not cryptocurrency”;

-

Despite existing challenges, the first wave of tokenization has arrived, driven by widespread stablecoin adoption, major launches of tokenized U.S. Treasuries, and clearer regulatory frameworks;

-

McKinsey estimates that by 2030, the total market capitalization of tokenized assets could reach approximately $2 trillion to $4 trillion (excluding cryptocurrencies and stablecoins);

-

Comparing the current state of tokenization with other major technological paradigm shifts indicates we are still in the early stages of the market;

-

The next wave of tokenization may be led by financial institutions and market infrastructure participants.

1. What is Tokenization?

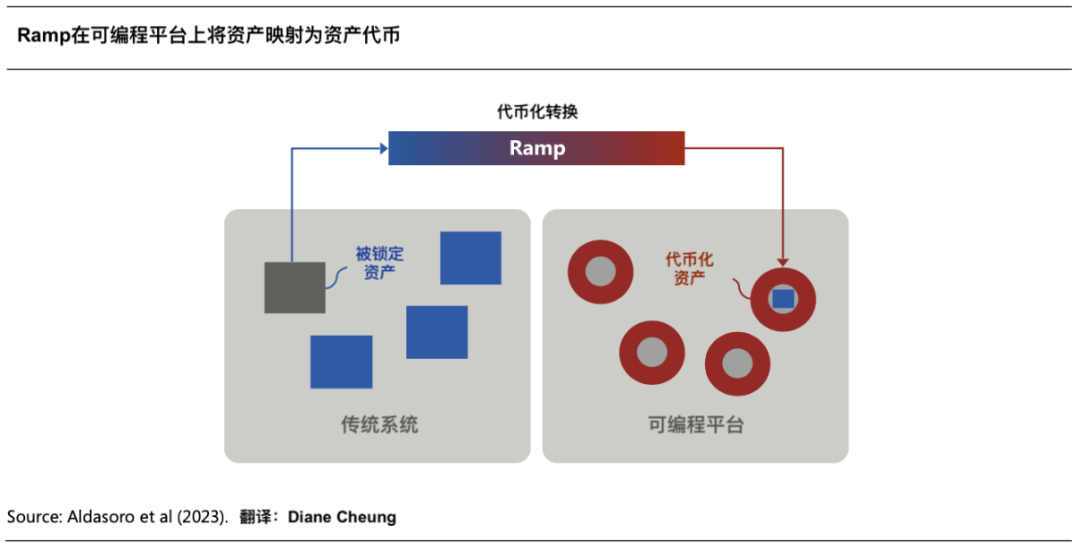

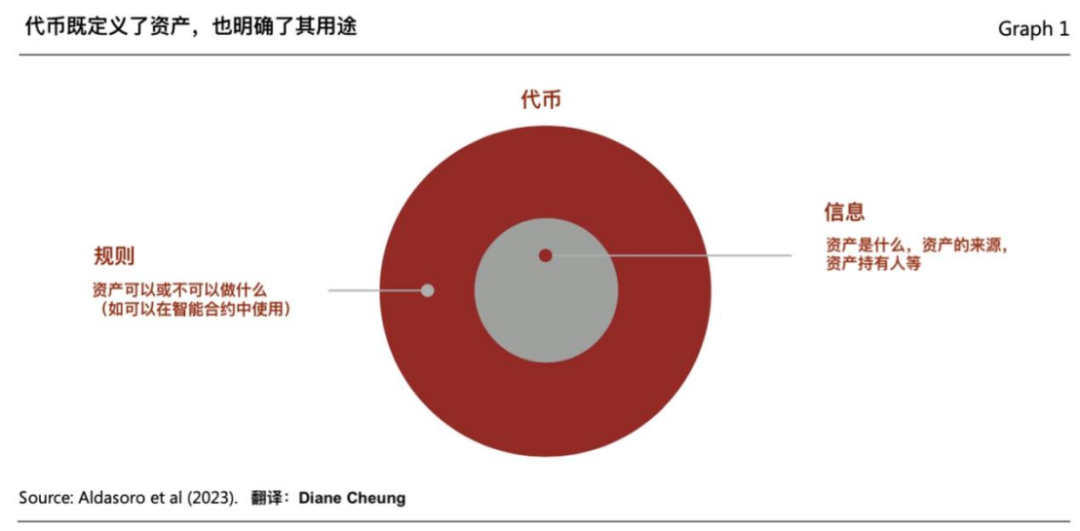

"Tokenization" refers to the process of recording ownership claims on financial or real-world assets—previously held on traditional ledgers—onto a programmable blockchain platform, thereby creating a digital representation of the asset. These assets can include traditional tangible assets (such as real estate, agricultural or mining commodities, physical artworks), financial assets (stocks, bonds), or intangible assets (such as digital art and other intellectual property).

The resulting "token" is a tradable ownership claim recorded on a programmable blockchain. Tokens are more than just digital certificates—they typically embed the rules and logic governing the transfer of the underlying asset previously managed on traditional ledgers. Thus, tokens are programmable and customizable to meet specific use cases and regulatory compliance requirements.

(Tokenization and Unified Ledger – Blueprint for the Future Monetary System)

The process of asset "tokenization" involves four key steps:

1.1 Identify the Underlying Asset

The process begins when an asset owner or issuer determines that the asset could benefit from tokenization. This step requires clarifying the structure of tokenization, as specific details will shape the overall design—for example, tokenizing a money market fund differs significantly from tokenizing carbon credits. The design is critical, helping determine whether the tokenized asset will be classified as a security or commodity, which regulatory frameworks apply, and which partners need to be involved.

1.2 Token Issuance and Custody

Creating a blockchain-based digital representation of an asset first requires securing the underlying physical or financial asset corresponding to the digital token. This involves transferring the asset into a controllable environment—either physical or virtual—typically managed by qualified custodians or licensed trust companies.

Next, a specific type of token is created on the blockchain to represent the underlying asset digitally, embedding code to execute predefined rules. To do this, asset owners select a token standard (e.g., ERC-20 or ERC-3643), a network (private or public blockchain), and desired features (e.g., transfer restrictions, freeze functions, recovery mechanisms), often implemented via third-party tokenization service providers.

1.3 Token Distribution and Trading

Tokenized assets can be distributed to end investors through traditional channels or new platforms like digital asset exchanges. Investors must set up an account or wallet to hold the digital assets, while any equivalent physical assets remain locked in the issuer’s traditional custodial accounts. This step often involves intermediaries such as distributors (e.g., private wealth divisions of large banks), transfer agents, or trading brokers.

Depending on the issuer and asset class, these tokenized assets may also be listed on secondary markets to create liquidity post-issuance.

1.4 Asset Servicing and Data Reconciliation

Even after distribution, digital assets require ongoing servicing, including regulatory, tax, and accounting reporting, as well as regular net asset value (NAV) calculations. The nature of servicing depends on the asset class—for instance, servicing carbon credit tokens requires different audits than fund tokens. These services must coordinate off-chain and on-chain activities and manage diverse data sources.

Current tokenization processes are complex. In a money market fund tokenization example, up to nine parties may be involved—including asset owners, issuers, traditional custodians, tokenization providers, transfer agents, digital asset custodians or brokers, secondary markets, distributors, and end investors—two more than in traditional asset workflows.

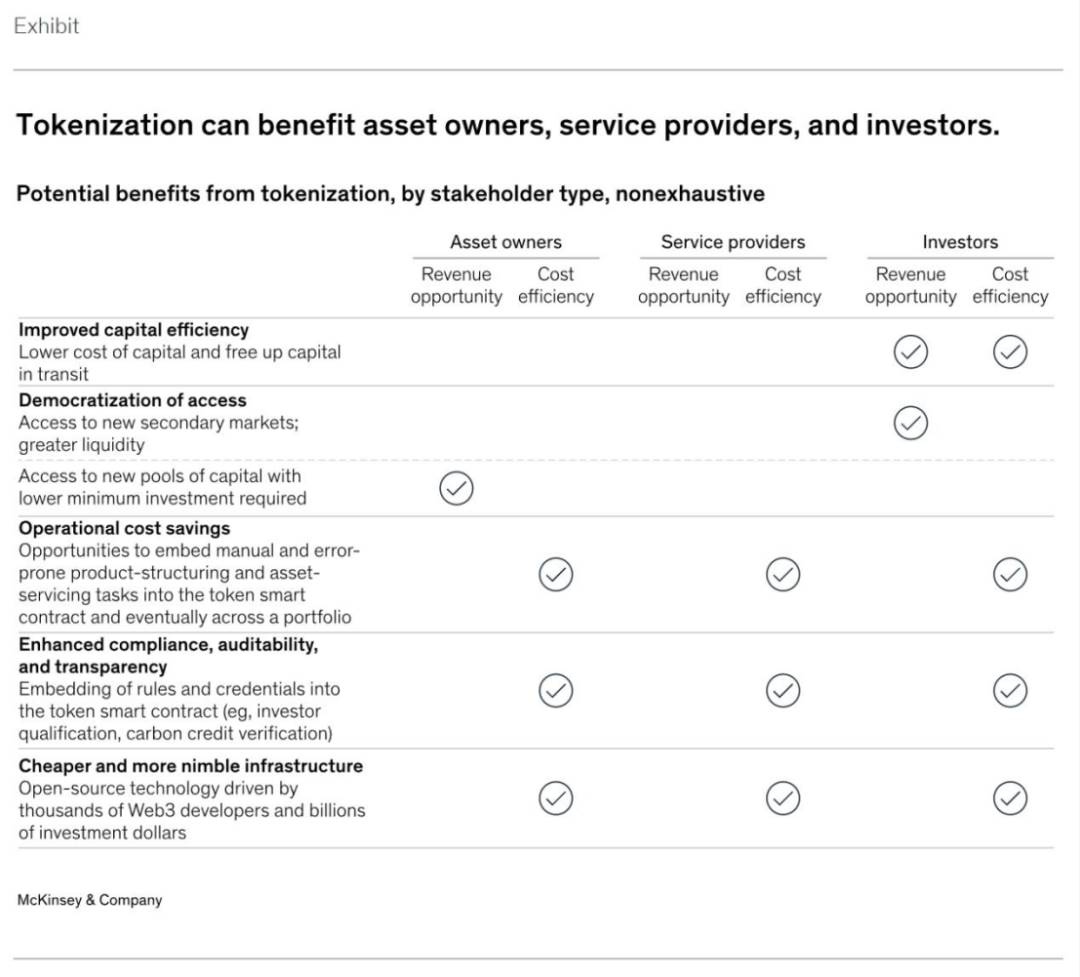

2. Benefits of Tokenization

Tokenization unlocks the vast potential of digital currencies and blockchain technology. Broadly speaking, these benefits include 24/7 operations, enhanced data availability, and instant atomic settlement. Additionally, tokenization enables programmability—the ability to embed code into tokens—and composability—the ability of tokens to interact with smart contracts—enabling higher levels of automation.

More specifically, as tokenization scales beyond proof-of-concept trials, the following advantages become increasingly evident:

2.1 Improved Capital Efficiency

Tokenization can significantly enhance capital efficiency in markets. For example, tokenized repurchase agreements (Repos) or money market fund redemptions can achieve near-instant T+0 settlement within minutes, compared to the current T+2 standard. In today’s high-interest-rate environment, shorter settlement times translate into substantial cost savings. For investors, these savings may explain the recent impact of tokenized U.S. Treasury products.

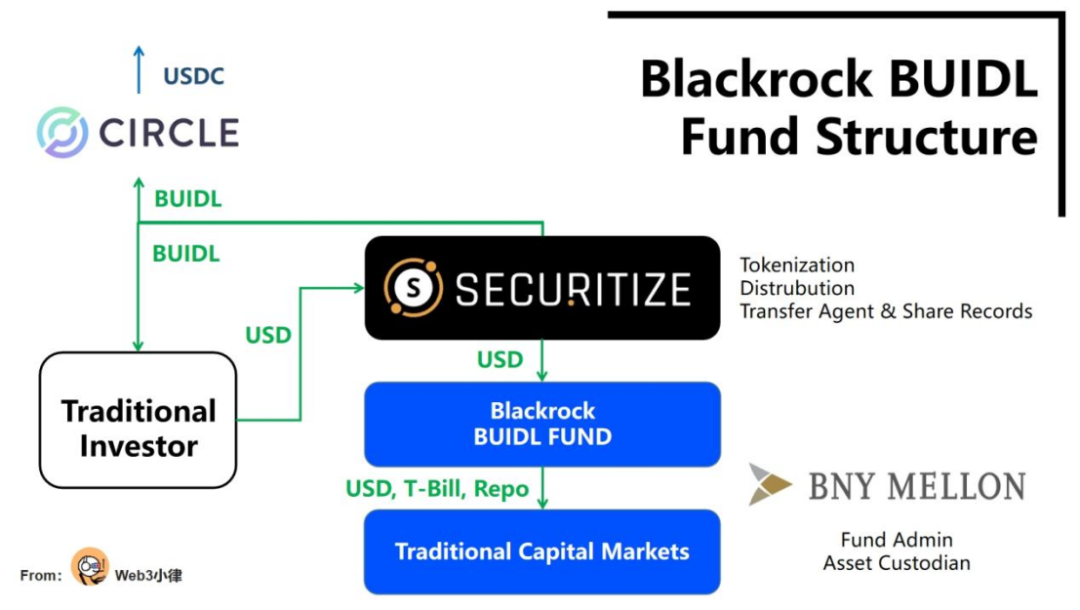

On March 21, 2024, BlackRock partnered with Securitize to launch BUIDL, its first tokenized fund, on a public blockchain—Ethereum. By enabling real-time settlement on a unified ledger, the tokenized fund drastically reduces transaction costs and improves capital efficiency. It allows (1) 24/7/365 fiat USD subscriptions and redemptions with instant settlement—a feature highly sought after by traditional financial institutions. Additionally, through collaboration with Circle, it enables (2) 1:1 real-time exchange between USDC stablecoin and BUIDL fund tokens, available 24/7/365.

Such tokenized funds bridging traditional and digital finance represent a landmark innovation for the financial industry.

(Decoding BlackRock’s Tokenized Fund BUIDL: Opening a Beautiful New World of RWA Assets to DeFi)

2.2 Permissionless Democratic Access

One of the most celebrated benefits of tokenization—or blockchain—is democratized access. The permissionless nature of entry, combined with fractional ownership (dividing ownership into smaller shares), can lower investment barriers and potentially increase asset liquidity—provided tokenized markets gain sufficient traction.

In certain asset classes, simplifying labor-intensive manual processes via smart contracts can dramatically improve unit economics, making services viable for smaller investors. However, access may still face regulatory restrictions, meaning many tokenized assets may only be available to accredited investors.

For example, leading private equity firms Hamilton Lane and KKR have partnered with Securitize to tokenize feeder funds of their private equity portfolios, offering broader investors an affordable way to participate in top-tier PE funds. Minimum investment thresholds have dropped from an average of $5 million to just $20,000. Still, individual investors must pass accredited investor verification on Securitize’s platform, indicating some barriers remain.

(RWA Deep Dive: The Value, Exploration, and Practice of Fund Tokenization)

2.3 Operational Cost Savings

Asset programmability can be another source of cost reduction, especially for asset classes where servicing or issuance is highly manual, error-prone, and involves numerous intermediaries—such as corporate bonds and other fixed-income products. These products often involve custom structures, imprecise interest calculations, and coupon payment complexities. Embedding interest calculations and coupon payments into smart contracts automates these functions, significantly reducing costs. Automation via smart contracts can also lower service costs for securities lending and repo transactions.

The Bank for International Settlements (BIS) and the Hong Kong Monetary Authority conducted the Evergreen project in 2022, using tokenization and a unified ledger to issue green bonds. The project leveraged a distributed unified ledger to integrate all participants onto a single data platform, supporting multi-party workflows with authorized real-time validation and signing capabilities. This improved processing efficiency, achieved Delivery-versus-Payment (DvP) settlement, reduced settlement delays and risks, and enhanced transparency through real-time data updates.

(https://www.hkma.gov.hk/media/chi/doc/key-information/press-release/2023/20230824c3a1.pdf)

Over time, the programmability of tokenized assets can also generate portfolio-level efficiencies, enabling asset managers to automatically rebalance portfolios in real time.

2.4 Enhanced Compliance, Auditability, and Transparency

Current compliance systems often rely on manual checks and retrospective analysis. Issuers can automate compliance by embedding relevant rules—such as transfer restrictions—directly into tokenized assets. Moreover, the 24/7 data availability of blockchain systems creates opportunities for streamlined consolidated reporting, immutable recordkeeping, and real-time auditability.

(Tokenization and Unified Ledger – Blueprint for the Future Monetary System)

A clear example is carbon credits. Blockchain technology can provide immutable and transparent records of credit purchases, transfers, and retirements, with transfer restrictions and Measurement, Reporting, and Verification (MRV) functions embedded directly into smart contracts. When a carbon token trade initiates, the token can automatically verify the latest satellite imagery to ensure the underlying emissions reduction project remains active, enhancing trust in the project and its ecosystem.

2.5 Cheaper and More Flexible Infrastructure

Blockchain is inherently open-source, continuously evolving thanks to thousands of Web3 developers and billions in venture capital. If financial institutions choose to operate on public-permissionless or hybrid public-private blockchains, they can rapidly adopt innovations like smart contracts and token standards, further reducing operational costs.

(Tokenization: A digital-asset déjà vu)

Given these advantages, it’s no surprise that many large banks and asset managers are highly interested in this technology.

However, due to limited use cases and adoption scale so far, many of these listed benefits remain theoretical.

3. Challenges to Mass Adoption

Despite its many potential benefits, very few assets have been widely tokenized to date. Key factors include:

3.1 Immature Technology and Infrastructure

Adoption of tokenization is hindered by limitations in existing blockchain infrastructure. These include a persistent shortage of institutional-grade digital asset custody and wallet solutions capable of offering sufficient flexibility in managing account policies, such as transaction limits.

Additionally, blockchain technology—especially permissionless public blockchains—has limited capacity to maintain system uptime under high transaction throughput, making it unsuitable for certain use cases, particularly in mature capital markets.

Finally, fragmented private blockchain infrastructures—including developer tools, token standards, and smart contract guidelines—pose interoperability risks and challenges among traditional financial institutions, such as cross-chain communication, protocols, and liquidity management.

3.2 Limited Business Case and High Implementation Costs

Many of the potential economic benefits of tokenization only materialize at scale. However, transitioning to new workflows not originally designed for tokenized assets may require an education cycle. This implies unclear short-term benefits and difficulty gaining organizational buy-in for the business case.

Not everyone grasps digital currency and blockchain technology immediately. During the transition, operations may become complex, possibly requiring parallel systems (e.g., digital vs. traditional settlement, on-chain vs. off-chain data coordination and compliance, digital vs. traditional custody and asset servicing).

Lastly, many traditional capital market clients have yet to express interest in 24/7 trading infrastructure or enhanced liquidity, posing further challenges to product go-to-market strategies.

3.3 Market Ecosystem Still Developing

Faster settlement and higher capital efficiency require instant cash settlement. Yet, despite progress, there is no large-scale interbank solution today: tokenized deposits are only piloted within a few banks; stablecoins lack regulatory clarity to be treated as bearer instruments and cannot offer real-time universal settlement. Furthermore, tokenization service providers are still nascent and unable to deliver integrated, mature one-stop solutions. There is also a lack of large-scale distribution channels for retail investors to access digital assets, contrasting sharply with the established distribution networks used by wealth and asset managers.

3.4 Regulatory Uncertainty

To date, regulatory frameworks for tokenization vary by region or are entirely absent. U.S. participants face particular challenges, including unclear settlement finality, lack of legal enforceability of smart contracts, and ambiguous qualified custodian requirements. Many unknowns remain regarding capital treatment of digital assets. For instance, the SEC’s SAB 121 mandates that digital assets used in custody services must appear on balance sheets—a stricter standard than for traditional assets—making it prohibitively expensive for banks to hold or distribute digital assets.

3.5 Industry Coordination Required

Capital market infrastructure participants have not shown consistent willingness to build or migrate markets on-chain, despite their critical role as recognized holders of assets on ledgers. Motivations for moving to on-chain infrastructure are misaligned, especially given that many financial intermediaries’ roles would undergo significant changes—or even be disintermediated.

Even relatively new asset classes like carbon credits have faced challenges establishing themselves on blockchains. Despite clear benefits such as enhanced transparency, only Gold Standard currently publicly supports tokenized carbon credits.

4. The First Wave of Tokenization Has Arrived

Despite the above challenges and unknown unknowns, recent trends and increasing adoption show that tokenization has reached a turning point in certain asset classes and use cases. The first wave of tokenization has arrived (Tokenization in Waves).

4.1 Widespread Adoption of Stablecoins

24/7, instant-settlement tokenized assets require support from tokenized cash, with stablecoins serving as its representative—the most critical component of the tokenized market.

Stablecoin Definition: Most cryptocurrencies are too volatile for payments—Bitcoin, for example, can swing dramatically in a single day. Stablecoins are digital currencies designed to maintain stable value, typically pegged 1:1 to fiat currencies like the U.S. dollar. They combine the best of both worlds: low daily volatility and the benefits of blockchain—efficient, low-cost, and globally accessible.

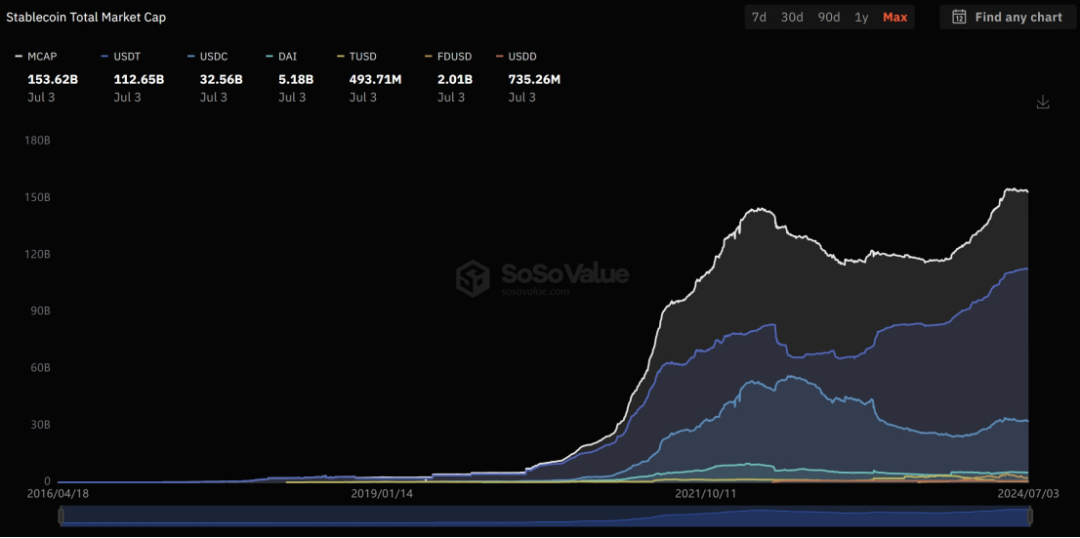

According to SoSoValue data, approximately $153 billion in tokenized cash circulates today in the form of stablecoins (e.g., USDC, USDT). Some banks have launched or are preparing to launch tokenized deposit features to improve cash settlement in commercial transactions. These emerging systems are far from perfect—liquidity remains fragmented, and stablecoins are not yet recognized as bearer instruments. Nevertheless, they have proven sufficient to support meaningful transaction volumes in digital asset markets. Monthly on-chain stablecoin transaction volume often exceeds $500 billion.

(https://sosovalue.xyz/dashboard/Stablecoin_Total_Market_Cap)

4.2 Tokenized U.S. Treasuries Driven by Short-Term Commercial Demand

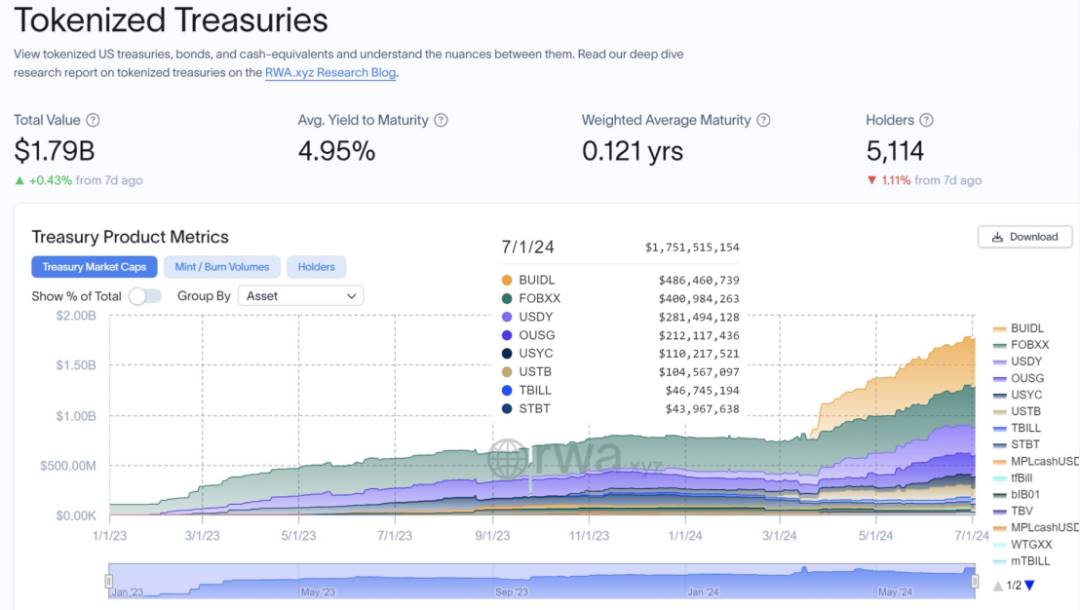

Current high interest rates have drawn significant market attention to tokenized U.S. Treasury use cases, whose products demonstrably deliver economic benefits and improve capital efficiency. According to RWA.XYZ data, the tokenized U.S. Treasury market has grown from $770 million at the start of 2024 to $1.75 billion as of July 1—an increase of 227%.

(https://app.rwa.xyz/treasuries)

Meanwhile, short-term liquidity trades—such as tokenized repos and securities lending—become more attractive during rising rate periods. JPMorgan’s institutional blockchain payment network Onyx currently handles $2 billion in daily transactions. Onyx’s volume can be attributed to JPMorgan’s “Coin System” and “Digital Assets” solutions.

Additionally, in the U.S., traditional banks are acquiring large (and often profitable) digital asset clients, such as stablecoin issuers. Retaining these clients requires 24/7 value and tokenized cash flow, further strengthening the business case for accelerating tokenization capabilities.

4.3 Gradual Clarification of Regulatory Frameworks

By late June, the EU had implemented MiCA’s stablecoin regulations, while Hong Kong solicited feedback on stablecoin regulation. Japan, Singapore, UAE, and the UK also released new guidelines to enhance regulatory transparency for digital assets. Even in the U.S., market participants are exploring various tokenization and distribution methods, leveraging existing rules to mitigate current regulatory uncertainty.

Following the House Financial Services Subcommittee on Digital Assets, Financial Technology, and Inclusion’s hearing on June 7 titled “Next-Generation Infrastructure: How Can Tokenizing Real-World Assets Make Markets Work Better?” SEC Commissioner Mark Uyeda highlighted the transformative potential of tokenization for capital markets during a securities event on June 14. As digital currency becomes a prominent topic in the U.S. election cycle, traditional financial capital is shifting from viewing crypto negatively as “speculative” to actively exploring how to “constructively” transform traditional finance, driven by both innovation needs and regulatory openness.

4.4 Market Penetration and Infrastructure Maturation

Over the past five years, many traditional financial services firms have expanded their digital asset talent and capabilities. Numerous banks, asset managers, and capital market infrastructure firms now have digital asset teams of 50 or more people—and these teams continue to grow. At the same time, understanding of the technology and its potential among established market players continues to deepen.

(Coinbase, The State of Crypto: The Fortune 500 Moving Onchain)

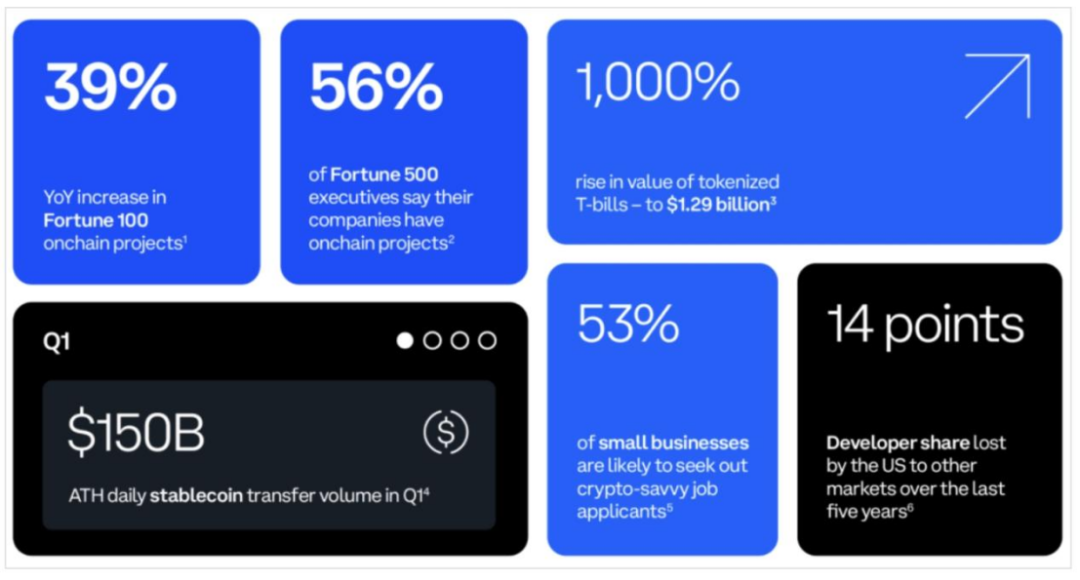

According to Coinbase’s Q2 State of Crypto report, 35% of Fortune 500 companies are considering launching tokenization projects. Seven of the top ten Fortune 500 executives are learning more about stablecoin use cases, particularly their low-cost, real-time settlement benefits. 86% of Fortune 500 executives recognize the potential benefits of asset tokenization for their companies, and 35% say they are currently planning to launch tokenization initiatives (including stablecoins).

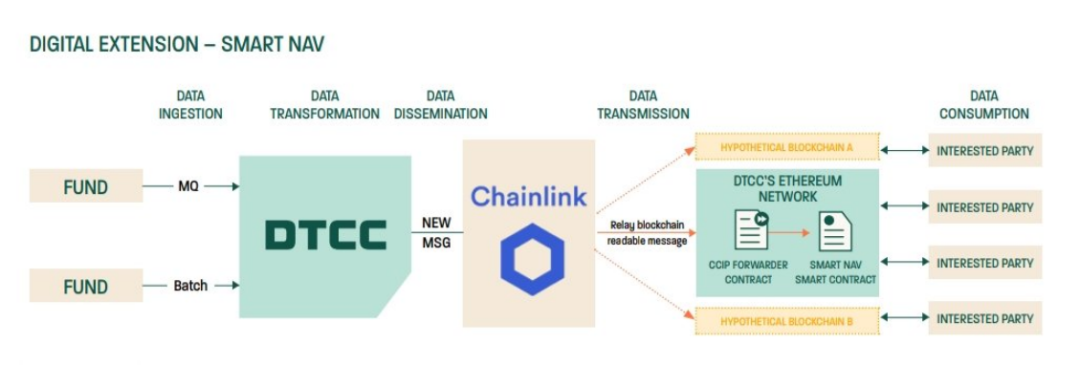

Moreover, we are seeing important financial market infrastructures conducting more experiments and planning functional expansions. On May 16, DTCC—the world’s largest securities settlement system, processing over $200 trillion in transactions annually—completed a pilot of its Smart NAV project with Chainlink. Using Chainlink’s Cross-Chain Interoperability Protocol (CCIP), the project delivered mutual fund Net Asset Value (NAV) pricing data to nearly any private or public blockchain.

Participants included American Century Investments, BNY Mellon, Edward Jones, Franklin Templeton, Invesco, JPMorgan, MFS Investment Management, MidAtlantic Trust Company, State Street, and Bank of America. The pilot found that providing structured data on-chain and defining standard roles and processes enabled foundational data to be embedded into multiple on-chain use cases, opening innovative applications for fund tokenization.

(DTCC, Smart NAV Pilot Report: Bringing Trusted Data to the Blockchain Ecosystem)

Although tokenization has not yet reached the scale needed to fully realize all its benefits, the ecosystem is maturing, challenges are becoming clearer, and the business case for adoption is steadily growing.

Especially under current high-interest-rate conditions, the argument that tokenization enhances capital efficiency has gained strong support from real-world cases—BlackRock’s successful launch of a tokenized fund (from a traditional finance perspective) and Ondo Finance’s widely adopted tokenized U.S. Treasury products (from a crypto-native perspective), along with strong market demand for the $ONDO token. Indeed, the first wave of tokenization has arrived.

As for the subsequent argument that tokenization could bring liquidity to traditionally illiquid assets, further market validation is required. That argument hinges on broader adoption of tokenized assets.

Regardless, these real-world use cases indicate that tokenization will continue to attract attention and generate meaningful positive value for global markets over the next two to five years.

5. Asset Classes with the Highest Adoption Potential

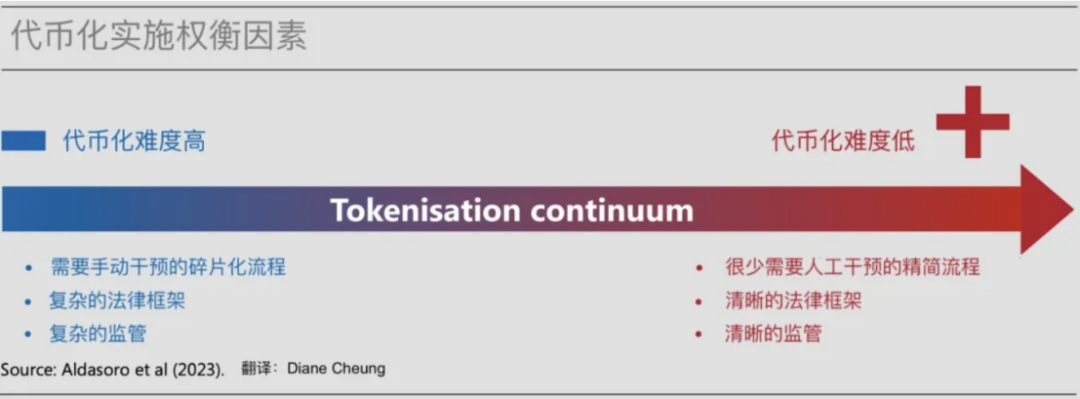

Asset classes with larger market sizes, greater value chain friction, less mature traditional infrastructure, or lower liquidity may stand to gain the most from tokenization. However, highest potential does not necessarily mean earliest implementation.

The pace and timing of adoption depend on each asset class’s characteristics, including expected benefits, feasibility, timing of impact, and risk appetite of market participants. These factors will determine whether and when a given asset class achieves mass adoption.

Specific asset classes can lay the groundwork for others by introducing clearer regulation, more mature infrastructure, better interoperability, and faster, easier investment. Adoption will also vary by region, influenced by dynamic macro environments including market conditions, regulatory frameworks, and buyer demand. Finally, the success or failure of flagship projects may accelerate or constrain further adoption.

(Tokenization and Unified Ledger – Blueprint for the Future Monetary System)

5.1 Mutual Funds

Tokenized money market funds have attracted over $1 billion in assets under management, indicating strong demand from on-chain investors in high-interest-rate environments. Investors can choose funds managed by established firms such as BlackRock, WisdomTree, Franklin Templeton, or Web3-native projects like Ondo Finance, Superstate, and Maple Finance. The underlying assets of these tokenized money market funds are predominantly U.S. Treasuries.

This represents the first wave of tokenization—widespread adoption of tokenized funds. As the scope and scale of tokenized funds expand, additional related products and operational advantages will follow.

Just as PayPal’s launch of its stablecoin on Solana at the end of May illustrates: the first step toward mass adoption is awareness—simply introducing people to the existence of new technology. The next step is utility—transforming initial awareness into practical, real-life applications. PayPal’s approach to driving stablecoin adoption can also be applied to scaling the tokenized market.

(Analyzing PayPal’s Stablecoin Payment Logic and the Path Toward Mass Adoption)

Transitioning to on-chain tokenized funds can greatly enhance fund utility, including instant 24/7 execution, immediate settlement, and using tokenized fund shares as payment instruments. Beyond that, leveraging on-chain composability, Web3-native issuers are enhancing token utility based

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News