FIT21: Crypto industry regulation—nine dragons ruling the water, yet the water remains uncontrolled

TechFlow Selected TechFlow Selected

FIT21: Crypto industry regulation—nine dragons ruling the water, yet the water remains uncontrolled

If FIT21 can officially become law, industry participants will have clearer legal guidance to prevent improper practices, and consumers will receive better protection under this regulatory framework.

Author: Melrose

TL;DR

-

The FIT21 Act establishes, for the first time, a comprehensive and clear regulatory framework for the crypto industry. It passed in the House of Representatives on May 22. If formally signed into law, it will have profound implications for the entire crypto sector.

-

For a long time, the U.S. has adopted a fragmented regulatory model where different federal agencies apply their own rules to the crypto industry, resulting in a “siloed” environment. Without a clear legal pathway, federal agencies have struggled to coordinate jurisdictional claims, leaving the U.S. crypto industry in a state of confusion and poor oversight.

-

FIT21 addresses core regulatory issues by clearly designating the SEC and CFTC as the primary regulators of the crypto industry and, for the first time, clarifying the classification of cryptocurrencies as either securities or commodities—resolving a long-standing central conflict in crypto regulation.

-

The bill details registration requirements for crypto entities with the SEC and CFTC, providing clearer regulatory guidance. It also includes robust consumer protections, such as a 12-month lock-up period for tokens issued by project teams, aimed at curbing short-term speculation and safeguarding industry health.

-

Congress expresses an optimistic stance toward the crypto industry in the bill, actively encouraging U.S. companies to innovate using blockchain technology, and urging the SEC and CFTC to study DeFi to support future regulation.

-

If FIT21 becomes law, industry participants will benefit from clearer legal guidance to avoid missteps, while consumers will enjoy stronger protections under this regulatory framework. The market could see rapid growth on both the consumer and innovation fronts, accelerating the industry’s exit from over a decade of regulatory Wild West conditions and bringing cryptocurrencies into the mainstream.

-

The passage of FIT21 is primarily due to strong Republican leadership and sustained bipartisan support. Initially introduced by a Republican-led committee, nearly all Republican House members voted in favor, along with several moderate Democrats. Leading crypto firms also rallied behind the bill, underscoring its significance.

-

With national elections approaching, the growing influence of the crypto sector has made it a key battleground for political support. Candidates with favorable crypto policies are likely to gain voter appeal, which positively influences the prospects of FIT21's passage.

-

FIT21 has not yet been signed into law. Next, it will move to the Senate for voting, followed by final text reconciliation and presidential signature. Patrick McHenry recently stated at the CoinDesk Consensus conference that the bill is expected to be signed into law within the next year.

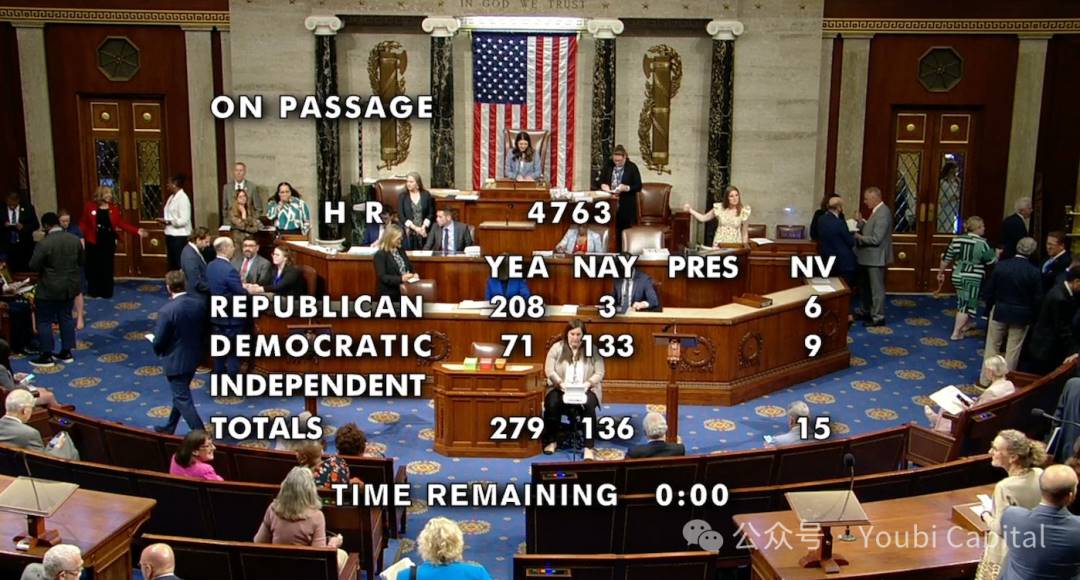

On May 22, local time in the United States, the Republican-led FIT21 Act passed the U.S. House of Representatives with 279 votes in favor and 136 opposed. This marks an extremely significant moment for the crypto industry, symbolizing a major legislative victory and demonstrating that the industry has reached the highest levels of U.S. political power. As the first comprehensive regulatory framework for the crypto sector, FIT21 represents the first successful step toward moving the industry out of the regulatory Wild West era.

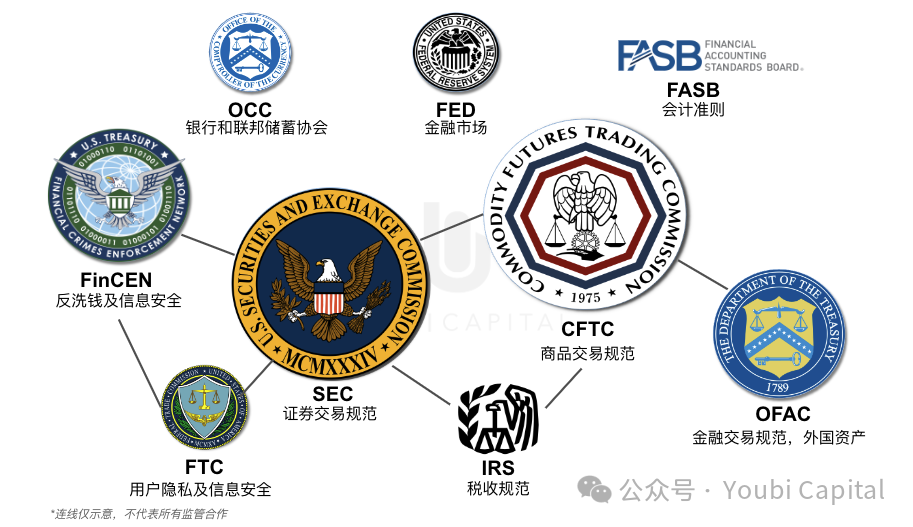

1 Current State of Crypto Regulation in the U.S.

The crypto industry has evolved to include numerous services such as centralized exchanges, mining, staking, and various smart contract-based applications. The U.S. currently employs a joint regulatory model, allowing different federal agencies to regulate activities within their respective jurisdictions. Key agencies—including the SEC (Securities and Exchange Commission), CFTC (Commodity Futures Trading Commission), FinCEN (Financial Crimes Enforcement Network), and OFAC (Office of Foreign Assets Control)—participate in monitoring and enforcing actions against illegal conduct in the crypto space, each exerting varying degrees of influence on the industry.

1.1 Fragmented Regulatory Oversight

Figure 1: Current Crypto Regulatory Landscape

Due to the lack of a systematic regulatory framework and the use of a joint oversight model, regulatory fragmentation and conflicting enforcement approaches among agencies are common.

The SEC plays a crucial role in crypto regulation, primarily defining whether specific crypto assets qualify as securities, typically applying the Howey Test to determine if they fall under its jurisdiction. To assist market participants in determining whether their digital assets constitute "investment contracts" and thus should be classified as "securities," the SEC released in 2019 a guidance document titled "Framework for 'Investment Contract' Analysis of Digital Assets." Although non-binding, this framework provides important interpretive guidance.

The CFTC has clearly stated on its website that virtual assets, includingall virtual currencies, are considered commodities, giving the CFTC authority to oversee manipulation and fraud in digital asset futures markets. Later, through amendments to the 2022 Digital Commodities Consumer Protection Act, the CFTC was granted exclusive jurisdiction over "digital commodity" trading and platforms, including authority to register and regulate spot exchanges—meaning these exchanges must follow the same rules as traditional commodity exchanges.

FinCEN focuses on anti-money laundering (AML), counter-terrorism financing, and KYC compliance. Its authority stems primarily from the Bank Secrecy Act (BSA), which mandates that any crypto-related business involved in the production, transfer, or exchange of virtual currency must comply with BSA regulations. In 2013, FinCEN issued a regulatory framework for virtual currencies and designated crypto asset exchange service providers as Money Services Businesses (MSBs), effectively treating virtual assets as money. Crypto exchanges must obtain FinCEN approval and implement anti-money laundering programs.

OFAC oversees all financial transactions in the U.S. and imposes sanctions on individuals, organizations, or nations deemed threatening. With the rise of digital assets, their technical features have enabled new methods for evading detection, increasing enforcement challenges for OFAC. Unlike the SEC and CFTC, OFAC primarily targets transactions involving sanctioned regions and money laundering support for illicit activities outside the U.S.

Thus, each agency maintains its own regulatory approach and perspective toward the crypto industry, leading to a fragmented and uncoordinated oversight system. This often results in regulatory conflicts, making it difficult for crypto operators to comply legally and exposing them to unjust litigation, ultimately hindering industry development.

Historical enforcement actions by these agencies are detailed in the appendix.

1.2 SEC’s “Intimidation-Style” Enforcement

Beyond its statutory jurisdiction, the SEC uses “Regulation by Enforcement” to assert whether a cryptocurrency qualifies as a “security.” Since court precedents serve as critical jurisdictional references, the SEC files civil lawsuits or administrative penalties against founders and executives for alleged violations of U.S. securities laws, relying on judicial rulings to establish its authority over specific crypto assets. For example, in December 2020, the SEC sued Ripple, alleging unregistered issuance and sale of XRP violated securities laws. Additionally, the SEC targets operational aspects of crypto businesses—for instance, in June 2023, it sued Coinbase for allegedly operating an unregistered securities business. Courts largely upheld the SEC’s claims, highlighting how the SEC continuously expands its regulatory reach through administrative channels. Given the ambiguity in the current regulatory framework, such enforcement easily creates an atmosphere of intimidation. Industry participants struggle to defend themselves with reliable legal standards, severely impacting innovation and growth in the crypto sector.

1.3 Regulatory Conflicts

The current fragmented regulatory landscape inevitably leads to jurisdictional conflicts between agencies, most notably between the SEC and CFTC, as both target the core issue of crypto asset classification. The SEC tends to classify most digital assets as securities, as they often pass the Howey Test, whereas the CFTC treats most cryptocurrencies as commodities. This divergence leads to overlapping jurisdiction when regulating certain tokens. Without a unified framework, delineating authority becomes difficult. Moreover, both agencies’ oversight of crypto businesses often overlaps. For example, in the 2023 case against Binance, both the SEC and CFTC filed lawsuits with highly similar allegations. Overlapping enforcement risks unnecessary fines and, under unclear regulations, significantly burdens the industry.

For a long time, the U.S. crypto industry has operated in a chaotic and poorly regulated environment, lacking a coherent legal pathway and causing federal agencies to fail in coordinating jurisdictional claims. Resulting regulatory conflicts have created severe instability, and without a clear framework, crypto firms struggle to defend themselves against unreasonable charges—hindering flexibility, innovation, and development in the U.S. The FIT21 Act marks the beginning of change to this disordered status quo.

2 Understanding the FIT21 Act

FIT21 stands for the Financial Innovation and Technology for the 21st Century Act (H.R. 4763). It redefines the jurisdictional boundaries between the SEC and CFTC over crypto assets, establishing a clearer and more comprehensive legal framework for the industry. It also includes consumer protection measures and provisions addressing the unique structural challenges of digital assets, making it the most significant crypto legislation to date due to its clarity and breadth.

FIT21 was first introduced on July 20, 2023, by Glenn Thompson (Chair of the House Committee on Agriculture), Patrick McHenry (Chair of the House Committee on Financial Services), Tom Emmer (Republican Conference Chair), and three other House members. During committee review, it passed unanimously in the House Agriculture Committee with bipartisan support. It later passed the House Financial Services Committee with backing from all Republicans and six Democratic members. This highlights that FIT21 is not only a product of collaboration between two House committees but also enjoys broad bipartisan support. Notably, the CFTC and SEC are overseen by the Agriculture and Financial Services Committees respectively, making these bodies natural leaders in advancing FIT21.

Figure 2: FIT21 Sponsors

2.1 Bill Content

Spanning 253 pages, FIT21 establishes preliminary regulations across six areas: definition and registration of digital assets, division of powers between the SEC and CFTC, and innovation guidance for the crypto industry. Below is a summary and analysis of each section.

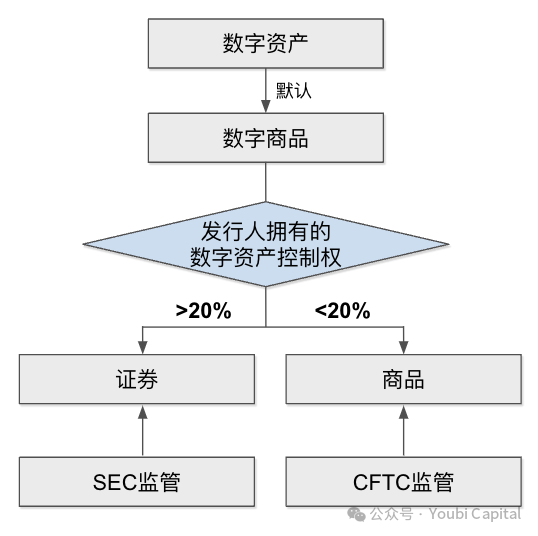

PART 1: Asset Definitions and Regulatory Responsibilities

In its first section, FIT21 draws on three securities and commodities laws to define key terms such as “blockchain protocol,” “decentralized governance system,” and “decentralized trading system.” Most importantly, it defines “digital asset” as “a digital representation of value that can be held or transferred without intermediaries, with all transactions recorded on a distributed ledger secured by cryptography”. Another notable term is “digital commodity,” which, though complex in original wording, can be simplified as “any digital asset obtained through legal issuance or purchased and held on an exchange.” This does not fundamentally alter the definition of digital assets, implying they are default commodities. However, FIT21 explicitly names the CFTC and SEC as the primary regulators of digital assets, requiring them to jointly refine all related terminology—indicating definitions will be further refined.

More critically, the bill clarifies cryptocurrency classification. If a blockchain running a digital asset is functional and decentralized, the asset is deemed a commodity regulated by the CFTC; otherwise, it is treated as a security under SEC oversight. A decentralized system is defined as one where no individual holds unilateral control over the blockchain, and no issuer controls 20% or more of the asset or voting rights. This standard is highly significant, clearly demarcating SEC and CFTC jurisdictions and greatly reducing regulatory overlap and conflict.

Figure 3: Asset Definition and Regulation

PART 2: Clarity on Investment Contract Assets

Given the unique structure and nature of crypto assets, FIT21 amends federal securities laws, particularly refining the definition and treatment of “investment contract assets” to bring greater clarity to certain market segments.

The bill makes two key amendments to the Securities Act of 1933: first, it explicitly excludes “investment contract assets” from the definition of “securities,” creating a distinct category, so that an asset classified as an investment contract won’t automatically be treated as a traditional security. The second amendment adds criteria for defining “investment contract assets”:

-

The asset must be a transferable digital value unit recorded on a public, cryptographically secured distributed ledger without intermediaries.

-

The asset must have been sold or transferred, or intended to be sold or transferred, as part of an investment contract.

-

The asset is not considered a security under the 1933 Securities Act

Previously, under SEC guidance, if an asset passed the Howey Test and was deemed an “investment contract,” it would be classified as a security and fall under SEC jurisdiction. However, due to the unique nature of digital assets, a digital asset may be considered a commodity while also being offered as part of an investment contract—the relationship between investment contracts and securities is not absolute. Traditional categories don't fully fit crypto regulation. Thus, FIT21’s exclusion of “investment contract assets” from the definition of securities grants greater regulatory flexibility for cryptocurrencies, avoiding rigid classification solely via the Howey Test, improving accuracy in asset categorization, and increasing tolerance for structural nuances to prevent unjust classification as securities.

Moreover, separating “investment contract assets” from securities resolves current regulatory splits for the same digital asset. For example, in the Ripple case mentioned earlier, courts ruled that XRP private sales to institutional investors met three Howey Test criteria and constituted “securities,” while other XRP sales did not. This led to fragmented and ambiguous oversight across distribution channels. Under FIT21, different conditions for “investment contract assets” would have clearer regulatory assignments, clarifying agency responsibilities, improving enforcement efficiency, reducing jurisdictional confusion during different issuance phases, and offering greater regulatory flexibility for market participants.

Figure 4: Howey Test Logic

PART 3: Exemptions and Lock-Up Requirements for Digital Asset Issuance

Regarding digital asset offerings, FIT21 outlines exemptions, disclosure obligations, and certification procedures. On exemptions, issuances valued under $75 million and where no single buyer acquires more than 10% of the offering are exempt from registration. The bill also sets baseline requirements and strengthens disclosure rules, mandating issuers to provide source code, token transaction history, and tokenomics. These align well with current industry practices and further protect consumer interests.

More importantly, the bill introduces lock-up requirements for issuing entities. All parties associated with a token issuer must hold their tokens for 12 months before selling. This mandatory rule deters short-term speculation, prevents market overheating, protects consumers, promotes long-term innovation, and helps retain genuine innovators and long-term stakeholders.

PART 4 and PART 5: SEC and CFTC Oversight of Crypto Firms

Parts four and five define the regulatory scope of the SEC and CFTC over digital assets and set registration requirements for industry participants. The bill explicitly states that crypto exchanges, brokers, and dealers are subject to regulatory oversight. Entities dealing in securities-type or commodity-type crypto assets must register separately with the SEC or CFTC, and a single entity may register with both. Additionally, the SEC and CFTC focus on different aspects: the SEC requires exchanges to submit relevant transaction data and records and assess system security and integrity, while the CFTC emphasizes custody of customer funds. The CFTC also regulates Commodity Pool Operators (CPOs) and Commodity Trading Advisors (CTAs).

Currently, DeFi activities are excluded from the bill’s scope, with future detailed rules to be developed jointly by the SEC and CFTC.

PART 6: Congressional Outlook and Innovation Oversight

In its final section, the bill summarizes Congress’s views on crypto technology. Congress acknowledges that entrepreneurs and innovators in the crypto space are building and deploying the next-generation internet, recognizing the potential of digital asset ecosystems to enhance social management, resource allocation, and decision-making efficiency. It stresses that the U.S. should explore the potential and opportunities offered by the crypto industry, urging American companies to innovate by integrating blockchain technology to create novel user engagement models. While affirming innovation, Congress also calls for collaboration with industry participants to build frameworks addressing blockchain risks and investor protection. Overall, Congress holds an optimistic view of digital assets and the crypto industry, supporting innovation while advocating for structured oversight to maximize blockchain’s unique benefits.

To better respond to blockchain advancements and digital asset impacts, the bill proposes expanding the mandate of the SEC’s FinHub and CFTC’s LabCFTC to study the crypto industry and assist committees in policy formulation and supervision systems. Additionally, it calls for establishing a joint CFTC-SEC Digital Assets Advisory Committee dedicated to researching digital asset issues, enhancing inter-agency coordination, and appointing at least 20 industry professionals to strengthen ties with the sector.

This section also mandates research into DeFi and NFTs: the SEC and CFTC must jointly study DeFi protocols’ use cases, scale, advantages, disadvantages, and potential risks or improvements to financial stability. Research on NFTs will be led by the U.S. Comptroller General, focusing on practical applications and integration with traditional markets.

2.2 Industry Significance

The House passage of FIT21 is a pivotal moment for the crypto industry, marking a major legislative victory and signaling that the industry has reached the highest echelons of U.S. political power.

As previously discussed, the fragmented U.S. crypto regulatory system allows different agencies to independently propose rules or guidance, leading to jurisdictional conflicts, inconsistent enforcement, and a flood of litigation that severely challenges industry sustainability and innovation. Meanwhile, practitioners lack reliable legal frameworks for proactive compliance or defense. The industry has long suffered under unclear regulation—and FIT21 is changing that.

First, FIT21 is the first-ever comprehensive regulatory framework for the crypto industry. Its provisions directly address core industry challenges, such as clearly identifying the SEC and CFTC as the primary regulators and establishing the first formal classification system for whether cryptocurrencies are securities or commodities. No longer will SEC and CFTC offer conflicting interpretations for the same token.

Additionally, the bill offers robust consumer protections. Clear registration rules for crypto firms, token lock-ups for issuers, and enhanced disclosure requirements further safeguard consumers, promote market health, and deter bad actors from exploiting regulatory gaps to launch harmful products and tokens.

Furthermore, Congress’s optimistic stance encourages innovation while pushing the SEC and CFTC to study DeFi for better future regulation—critical for ongoing innovation and more nuanced legislation.

If FIT21 becomes law, industry participants will have clearer legal guidance to avoid missteps, benefiting enterprise growth and innovation. Consumers will gain stronger protections, and given crypto’s growing influence, the market could experience rapid growth on both the consumer and innovation fronts, finally bringing cryptocurrencies into the mainstream.

Great trees stand tall because their roots run deep. FIT21 is precisely that foundational first step—a cornerstone for future comprehensive legislation, paving the way for innovation under clear regulatory guardrails, helping the industry accelerate beyond over a decade of regulatory Wild West conditions and shaping the future of the entire sector.

3 Key Drivers Behind FIT21

3.1 Republican Leadership with Bipartisan Support

Politically, Republicans played a crucial role as the main drivers. The bill initially passed through the House Agriculture and Financial Services Committees, both dominated by Republicans with 28 and 29 Republican members respectively. This numerical advantage allowed Republicans to advance the bill through committee and to the House floor. Though Republicans led the effort, notably, all Democratic members on the Agriculture Committee also voted in favor, indicating early bipartisan support. Ultimately, FIT21 received 208 Republican and 71 Democratic votes in the House, clearly showing strong Republican backing and shifting attitudes among some Democrats. Combined with Trump’s recent pro-crypto stance, the Republican Party has significantly advanced the crypto industry.

Figure 5: FIT21 Voting Results

3.2 High Industry Engagement

Given the bill’s significance, crypto industry players and firms paid close attention. On May 16, Crypto Council for Innovation (CCI), joined by 60 other companies, issued a joint letter urging swift passage of FIT21. Signatories included major players like a16z, Coinbase, Circle, and Block, emphasizing FIT21’s importance and the U.S.’s lagging regulatory environment, and calling on lawmakers to support H.R. 4763 to establish a clear regulatory framework.

Figure 6: Joint Advocacy Letter

3.3 Growing Influence of the Crypto Industry

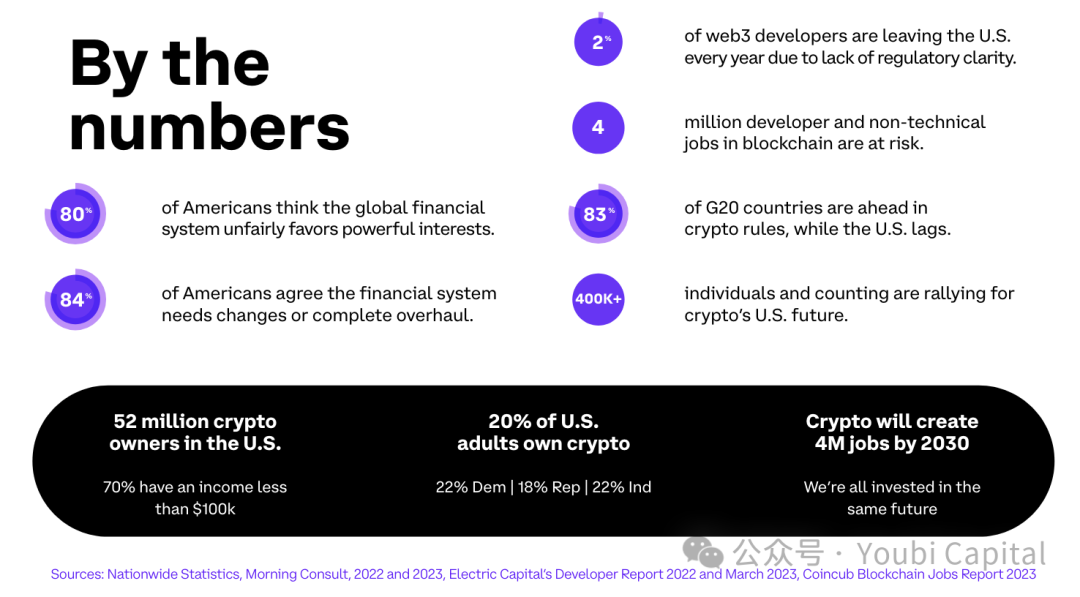

Beyond party and industry support, the expanding influence of crypto and the U.S. political climate are key driving forces. According to Stand With Crypto, a nonprofit, 52 million Americans currently hold crypto, and another survey suggests about 20% of U.S. citizens own digital assets. Despite discrepancies, both figures show that crypto holders are no longer a niche group. The industry is projected to create 4 million jobs by 2030, positively impacting the U.S. labor market. Yet, the current regulatory environment lags behind 83% of G20 countries, putting millions of blockchain jobs at risk and prompting many professionals to leave the U.S. due to regulatory uncertainty. These factors compel lawmakers to prioritize crypto regulation, making FIT21 especially critical.

Figure 7: Stand With Crypto Public Opinion Poll

3.4 Crypto as a Political Battleground Ahead of Elections

With the U.S. election in full swing, the growing clout of the crypto sector has turned it into a key battleground for political influence. Polls commissioned by Grayscale, DCG, and Paradigm indicate that at least 20% of voters hold and closely follow crypto. This sizable demographic cannot be ignored. In multiple swing states, a significant number of voters consider crypto a key election issue, making political candidates’ stances on crypto a crucial political lever, profoundly influencing related legislation. Thus, partisan competition may strongly favor the advancement of FIT21.

-

A poll commissioned by crypto investment firm Paradigm, released on Thursday (March 14), found that 20% of U.S. voters hold crypto.

-

A Harris poll funded by Grayscale, a Bitcoin ETF issuer, showed rising voter interest in crypto, with 33% saying they’d consider a candidate’s crypto stance before voting.

-

A poll by Digital Currency Group (DCG) revealed that in key swing states, over 20% of voters see crypto as a critical issue in the upcoming U.S. election.

-

Grayscale poll: Nearly half of U.S. voters expect their portfolios to include crypto.

4 Next Steps

Committee Review → Bicameral Vote → Presidential Signature

FIT21 has passed the House and now moves to the Senate. The U.S. legislative process involves three stages: committee review, bicameral voting, and final reconciliation and presidential signing. A bill is first introduced and reviewed in a committee. Upon approval, it proceeds to a vote in its originating chamber. Then, it must go to the other chamber for review. Since FIT21 passed the House, it now heads to the Senate. However, this transition is lengthy and complex. FIT21 faces two possible paths in the Senate: First, the Senate may choose to draft a new version of the bill, restarting the process with committee review before Senate voting. Alternatively, even if the bill goes directly to a Senate vote, it may face amendments and revisions, then return to the House for reconciliation. According to CoinDesk, the Senate is likely to draft its own version of FIT21, meaning the path to enactment remains long. In the final stage, even if the president vetoes the bill, Congress can override with a two-thirds majority in both chambers, giving FIT21 considerable leeway. Currently, the White House has not threatened a veto, suggesting engagement and willingness to participate in policy formation.

Patrick McHenry, a lead sponsor of FIT21, recently stated at the CoinDesk Consensus conference that the bill is expected to be signed into law within the next year. While the crypto industry’s growing influence and its role in the upcoming election increase the likelihood of passage, the U.S. government’s stance on crypto remains ambiguous. For instance, Biden recently vetoed a resolution overturning the SEC’s SAB 121 crypto accounting rule but has taken a neutral stance on FIT21. With the election underway, the FIT21 process may carry over to the next Congress. If Trump wins, his continued support for crypto legislation remains uncertain. Nevertheless, given crypto’s rising political importance, FIT21’s outlook remains relatively positive.

Appendix

SEC (Securities and Exchange Commission)

-

In December 2020, the SEC sued Ripple for failing to register the issuance and sale of XRP, violating securities laws. The court later ruled that XRP private sales to institutional investors met three Howey Test criteria and constituted “securities,” while other sales did not. The SEC has since appealed.

-

In June 2023, the SEC sued Coinbase for illegally operating a crypto securities business without registration. The court largely upheld the SEC’s claims.

-

In November 2023, the SEC sued Kraken for facilitating unregistered crypto securities trades and operating 11 unregistered securities. State officials accused the SEC of overreach, claiming it was expanding the definition of “investment contract” to automatically classify crypto assets as securities. Kraken later settled, paying $30 million.

-

The SEC’s reach extends beyond U.S. borders. For Telegram’s Gram token, issued to U.S. citizens, the SEC enforced action to protect American investors—even though Telegram was registered in the UK. Telegram eventually returned raised funds and paid an $18.5 million fine.

CFTC (Commodity Futures Trading Commission)

-

On September 14, 2021, the CFTC sued Tether and Bitfinex, accusing them of falsifying trading volumes, misappropriating customer funds, and violating AML laws. They settled in October 2022, with Tether paying $41 million and Bitfinex $1.5 million.

-

In October 2020, the CFTC, FBI, and DOJ jointly sued BitMEX and its executives, alleging failure to register as a commodity futures dealer. They reached a settlement, with BitMEX paying a $100 million fine.

FinCEN (Financial Crimes Enforcement Network)

-

In 2015, FinCEN fined Ripple Labs Inc. $700,000 for operating without an MSB license and failing to establish AML mechanisms.

-

In 2020, FinCEN imposed a $60 million civil penalty on the developers and operators of Helix and Coin Ninja mixers, accusing Coin Ninja of violating BSA’s AML requirements.

-

In 2023, FinCEN and OFAC sued Binance for violating BSA and failing to meet AML obligations.

OFAC (Office of Foreign Assets Control)

-

In December 2020, OFAC and BitGo settled allegations that BitGo violated sanctions against Crimea, Iran, Syria, and Cuba from 2015 to 2019. BitGo agreed to pay a $98,830 fine.

-

Later, OFAC sued platforms like Kraken, CoinList, and Binance for similar allegations of processing transactions for sanctioned-region users, resolving all via fines and settlements.

FTC (Federal Trade Commission)

The FTC primarily handles consumer privacy and information security. In July 2023, it sued Celsius Network and affiliated executives, accusing them of deceiving consumers into transferring assets by falsely claiming deposits were safe, while actually misusing funds and lacking liquidity. The FTC and Celsius reached a settlement, permanently banning the platform from handling consumer assets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News