cmDeFi: A Deep Offensive into the Stablecoin Market Initiated by Ethena

TechFlow Selected TechFlow Selected

cmDeFi: A Deep Offensive into the Stablecoin Market Initiated by Ethena

Combining yield and scalability, USDe could become a high-yield stablecoin with limited scale in the short term and market-following growth in the long term.

Author: Chen Mo cmDeFi

Core Thesis: A crypto-native synthetic dollar stablecoin, functioning as a structured passive yield product positioned between centralized and decentralized models—securing assets on-chain while maintaining stability through delta neutrality and generating yield.

-

The project emerged amid market dominance by centralized stablecoins such as USDT and USDC, increasing centralization of DAI’s collateral base, and the collapse of algorithmic stablecoin LUNA/UST after it rapidly rose to become one of the top five stablecoins by market cap. Ethena represents a compromise and balance between DeFi and CeFi markets.

-

Institutional-provided OES services hold assets on-chain and map balances to centralized exchanges (CEXs) as margin. This preserves DeFi principles by isolating on-chain funds from exchanges, reducing risks like fund misappropriation or insolvency, while also retaining CeFi advantages such as deep liquidity.

-

Yield is generated from staking rewards via Ethereum liquid staking derivatives and funding rate income earned by opening hedged positions on exchanges—a model often described as a structured, mass-scale funding rate arbitrage product.

-

Currently incentivizing liquidity via a points-based system.

Its ecosystem includes:

-

USDe – A stablecoin minted 1:1 against USD by depositing stETH (with potential for future expansion to other assets and derivatives).

-

sUSDe – A receipt token received upon staking USDe.

-

ENA – The protocol and governance token, currently entering circulation through periodic point redemptions; locking ENA grants accelerated points accrual.

Research Report

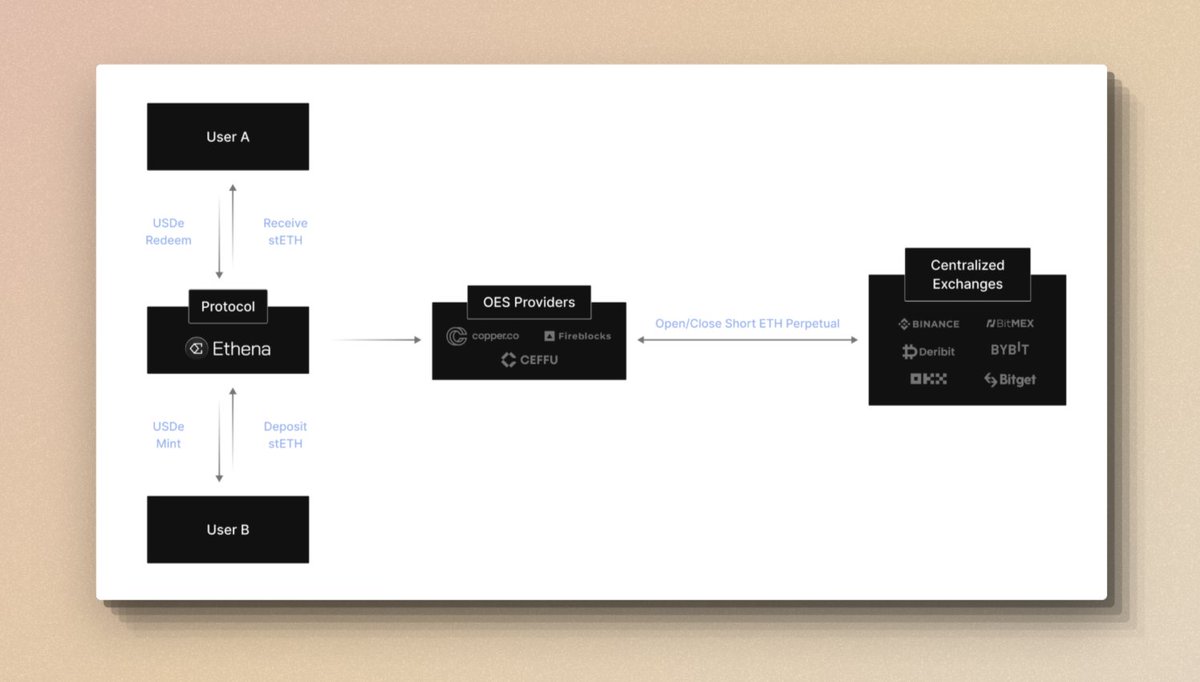

1/6 • How USDe Stablecoin is Minted and Redeemed

Users deposit stETH into the Ethena protocol to mint USDe at a 1:1 USD ratio. The deposited stETH is sent to third-party custodians and its balance is mapped to centralized exchanges via "Off-exchange Settlement" (OES). Ethena then opens short ETH perpetual positions on CEXs to maintain delta neutrality, ensuring the collateral value remains stable in USD terms.

-

General users can obtain USDe through permissionless external liquidity pools.

-

KYC/KYB-verified, whitelisted institutional participants can directly mint and redeem USDe via Ethena smart contracts at any time.

-

Assets remain in transparent, on-chain custody addresses, eliminating reliance on traditional banking infrastructure and avoiding risks associated with exchange fund misuse or bankruptcy.

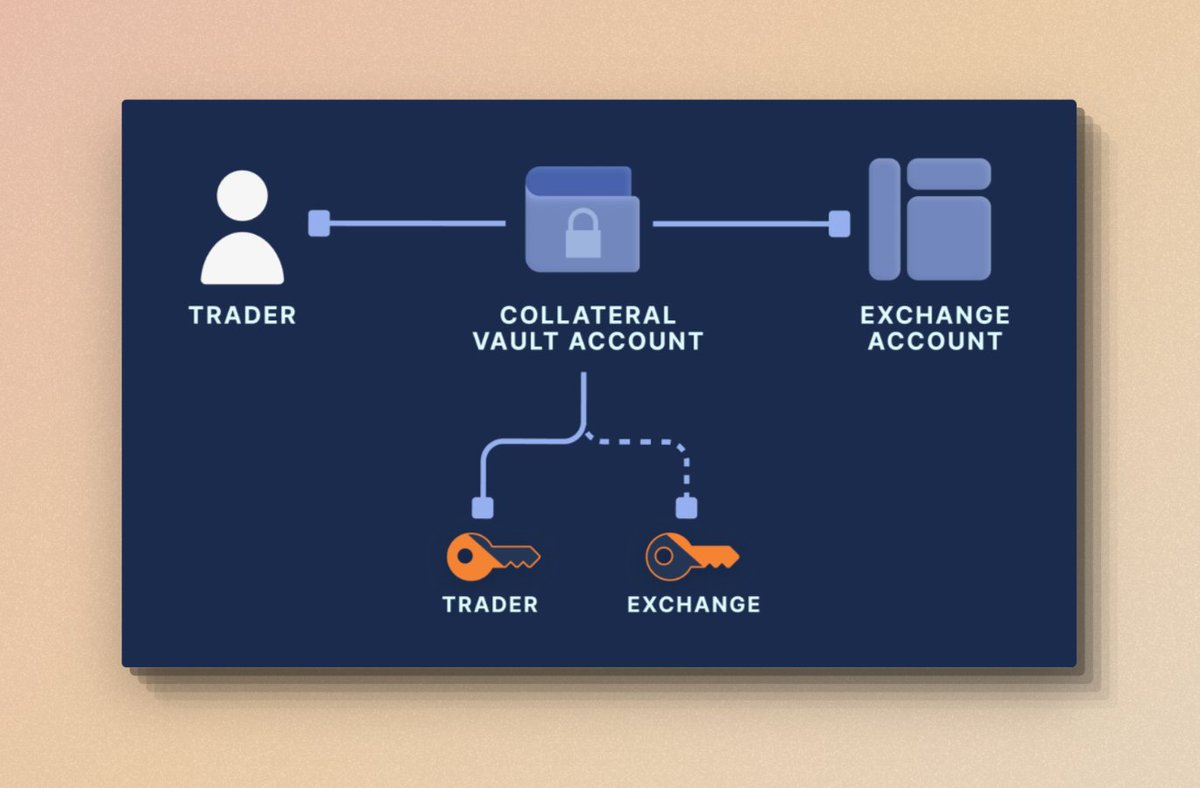

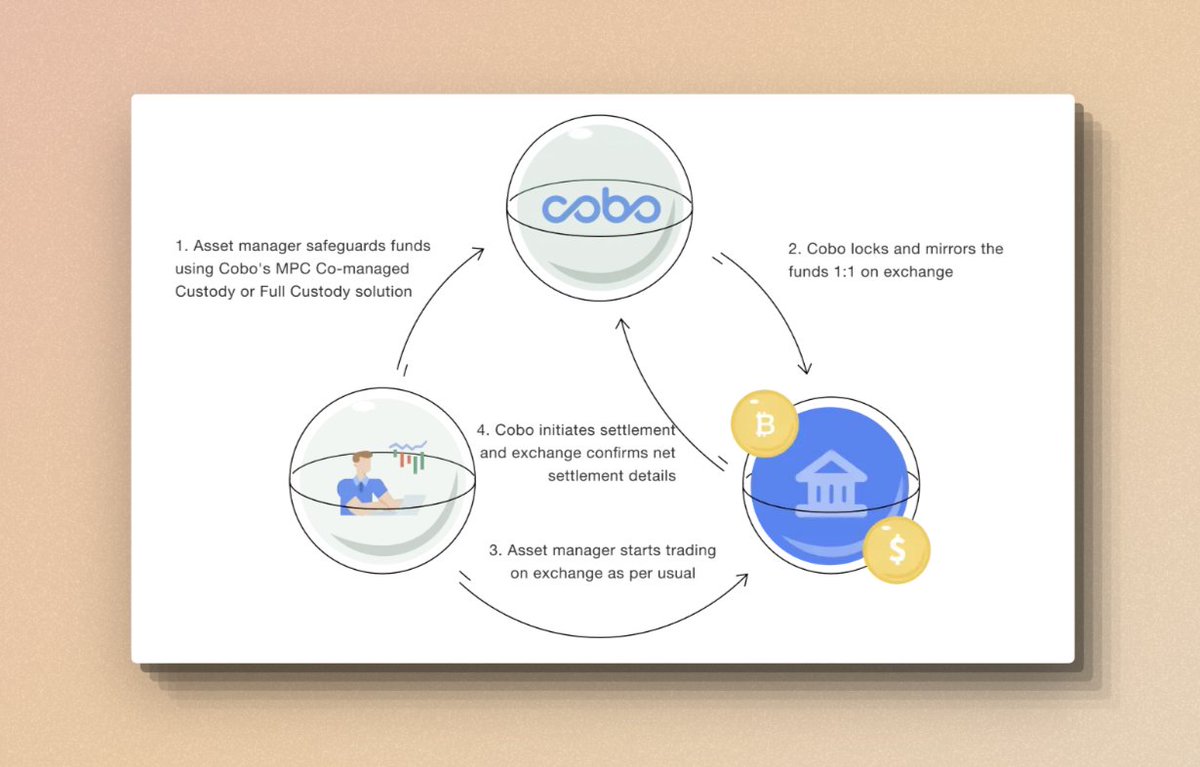

2/6 • OES – The ceDeFi Custody Model

OES (Off-exchange Settlement) is a custodial settlement mechanism that combines on-chain transparency and traceability with the capital efficiency of centralized exchanges.

-

Using MPC technology, OES creates custody wallets where user assets are stored on-chain, preserving transparency and decentralization. Access is jointly managed by users and custodial institutions, mitigating counterparty risk, security vulnerabilities, and potential fund misuse—ensuring maximum asset control remains with users.

-

OES providers typically partner with exchanges, enabling traders to map wallet balances to exchange accounts for trading and financial services. For example, this allows Ethena to hold funds off-exchange while still using them as collateral for delta-hedged derivative positions on exchanges.

MPC wallets are widely regarded as the ideal solution for consortium-controlled management of a single crypto asset pool. In an MPC model, a single private key is split into separate shards distributed among multiple parties, who collectively manage the custody address.

Fireblocks Off-exchange Settlement

Cobo SuperLoop

3/6 • Revenue Generation

-

Ethereum staking yield from ETH liquid staking derivatives.

-

Funding rate income from short perpetual positions opened on exchanges—also known as basis spread (basis trade) yield.

“Funding rate” refers to periodic payments exchanged between long and short holders based on the price difference between spot and perpetual futures markets. Traders pay or receive funds depending on demand for long or short positions. When the funding rate is positive, longs pay shorts; when negative, shorts pay longs. This mechanism ensures prices across markets remain aligned.

“Basis” refers to the price divergence between spot and futures markets, which are traded separately. As futures contracts approach expiration, their prices tend to converge toward spot prices. At expiry, long position holders must buy the underlying asset at the predetermined contract price. Therefore, as expiration nears, the basis should trend toward zero.

By leveraging mapped exchange balances, Ethena executes various arbitrage strategies, delivering diversified yield to sUSDe holders on-chain.

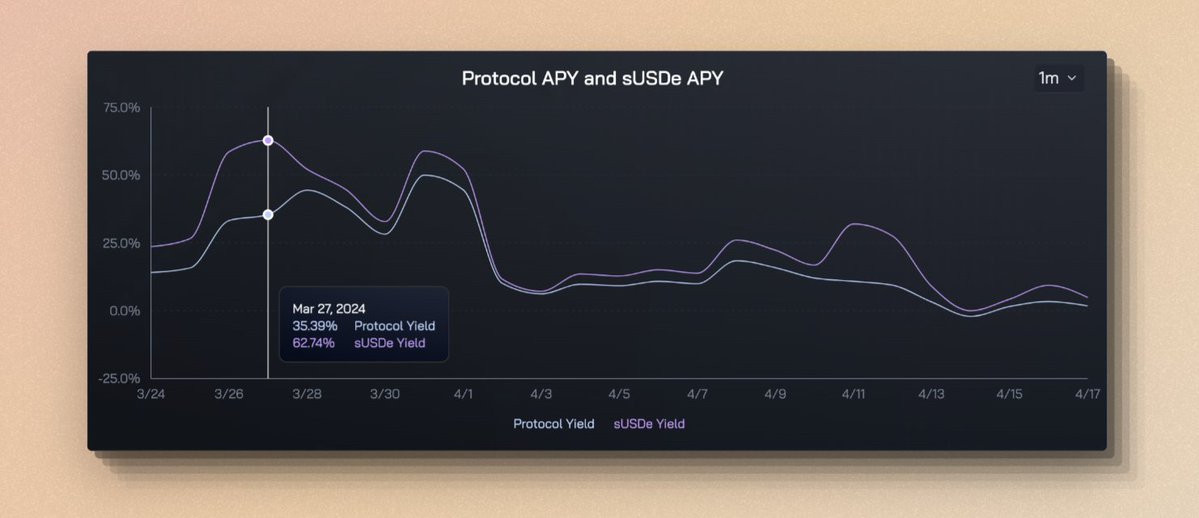

4/6 • Yield and Sustainability

In terms of yield, the protocol achieved up to 35% annualized revenue over the past month, with sUSDe yields reaching 62%. The gap exists because not all USDe is staked into sUSDe—in practice, full staking rates are nearly impossible. If only 50% of USDe is converted to sUSDe, that portion captures 100% of the total yield. Since USDe is used within DeFi protocols like Curve and Pendle, this satisfies diverse use cases while potentially amplifying sUSDe yields.

However, as market enthusiasm cools and long-side funding declines, funding rate income decreases. Since April, overall yields have shown a clear downward trend, with Protocol Yield now at 2% and sUSDe Yield at 4%.

Thus, USDe's yield heavily depends on conditions in CEX perpetual futures markets and is inherently limited by the size of these markets. Once USDe issuance exceeds available futures market capacity, further expansion becomes unfeasible.

5/6 • Scalability

Scalability—the ability to increase stablecoin supply—is critical.

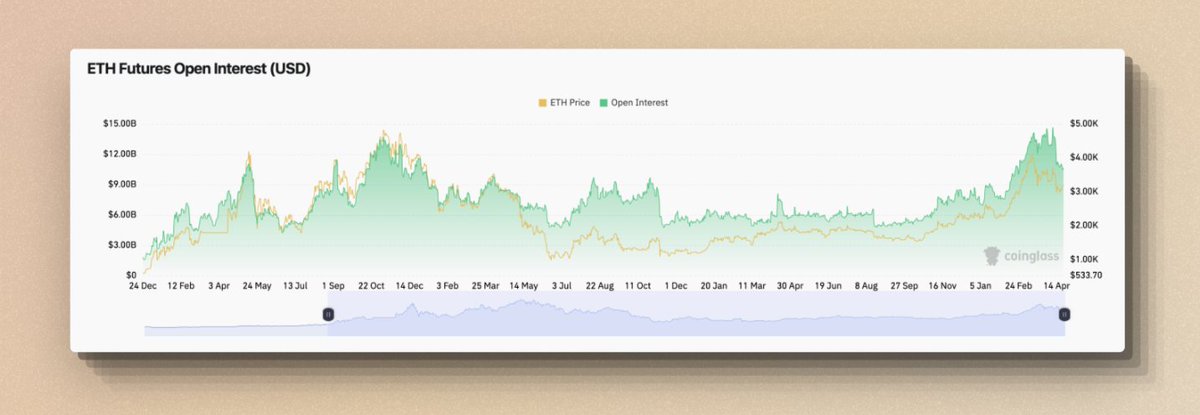

Stablecoin protocols like Maker are typically constrained by over-collateralization requirements, needing more than $1 in collateral to mint $1. Ethena’s scalability bottleneck is primarily determined by open interest in ETH perpetual markets.

Open Interest (OI) refers to the total value of outstanding derivative contracts on an exchange. Here, it specifically denotes the total notional value of ETH perpetual contracts on centralized exchanges. Currently, this stands at approximately $12 billion (as of April 2024), reflecting current market exposure to ETH.

Compared to early 2024, ETH OI has grown from $8 billion to $12 billion. Recently, Ethena expanded to BTC markets, where OI is around $30 billion. USDe’s current supply is about $2.3 billion—driven by multiple factors including organic user growth and rising ETH/BTC prices. The key takeaway is that USDe’s scalability is tightly linked to perpetual market depth.

This explains why Ethena partners with centralized exchanges. In 2023, Solana-based stablecoin UXD Protocol used a similar delta-neutral model but executed hedging on-chain via decentralized exchanges. However, due to limited on-chain liquidity, large-scale shorting eventually led to negative funding rates and high costs. Additionally, UXD relied on Mango, a leveraged protocol on Solana, which was later hacked. These compounding issues caused the project’s failure.

Could USDe reach the market cap scale of USDT or DAI?

Currently, USDe’s market cap is around $2.3 billion, ranking fifth among all stablecoins—surpassing most decentralized stablecoins but still $300 million behind DAI.

ETH OI is near historical highs, and BTC OI has already reached record levels. Further USDe expansion would require correspondingly larger short positions in existing markets—posing challenges for current growth. Funding rate, the primary yield source for USDe, is a mechanism designed to align perpetual prices with spot prices through regular transfers between longs and shorts. Over-issuance of USDe increases net short exposure, potentially driving funding rates down or even negative. This would reduce Ethena’s income stream.

Assuming constant market sentiment, this becomes a classic supply-demand equilibrium problem—requiring balance between expansion and yield sustainability. In a bullish environment with strong long sentiment, theoretical USDe issuance capacity increases. Conversely, in bearish conditions with weak long demand, issuance capacity shrinks.

Combining yield dynamics and scalability constraints, USDe may evolve into a high-yield stablecoin with limited short-term scale, growing in tandem with broader market cycles over the long term.

6/6 • Risk Analysis

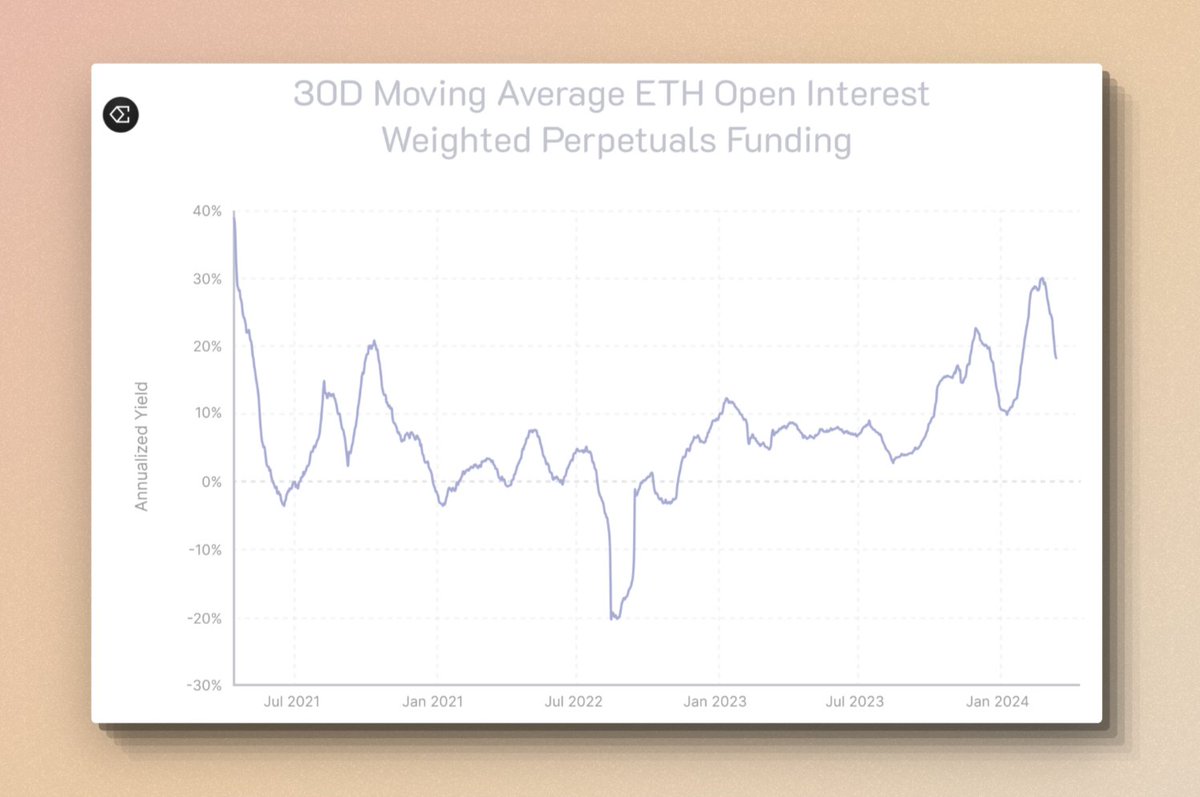

Funding Rate Risk – When long-side demand is insufficient or USDe is over-issued, funding rates may turn negative, forcing Ethena—as a net short—to pay longs. While historical data suggests markets spend most time in positive funding territory, and stETH collateral provides a 3–5% yield buffer to absorb negative funding, it’s worth noting that previous attempts to scale synthetic dollar stablecoins have failed due to yield inversion.

ETH Open Interest Weighted Perpetuals Funding

Custody Risk – Custody relies on OES and centralized service providers. Exchange insolvency could result in unrealized profit losses, while OES provider bankruptcy might delay fund access. Although MPC and minimal-trust designs are employed, theoretical risks of fund theft still exist.

Liquidity Risk – Rapid position adjustments or liquidations involving large capital amounts may face liquidity shortages, especially during market stress or panic. Ethena seeks to mitigate this through partnerships with CEXs—using gradual unwinds, stepwise closures, or preferential policies to minimize market impact. While these relationships offer flexibility, they also introduce centralization risks.

Asset Peg Risk – stETH is theoretically pegged 1:1 to ETH, though brief depegs have occurred historically—most notably before the Shanghai upgrade. Future risks in Ethereum’s liquid staking layer remain possible. A significant depeg could trigger exchange-level liquidations.

To address these risks, Ethena has established an insurance fund, capitalized by allocating a portion of protocol revenue each cycle.

cmDeFi Research

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News